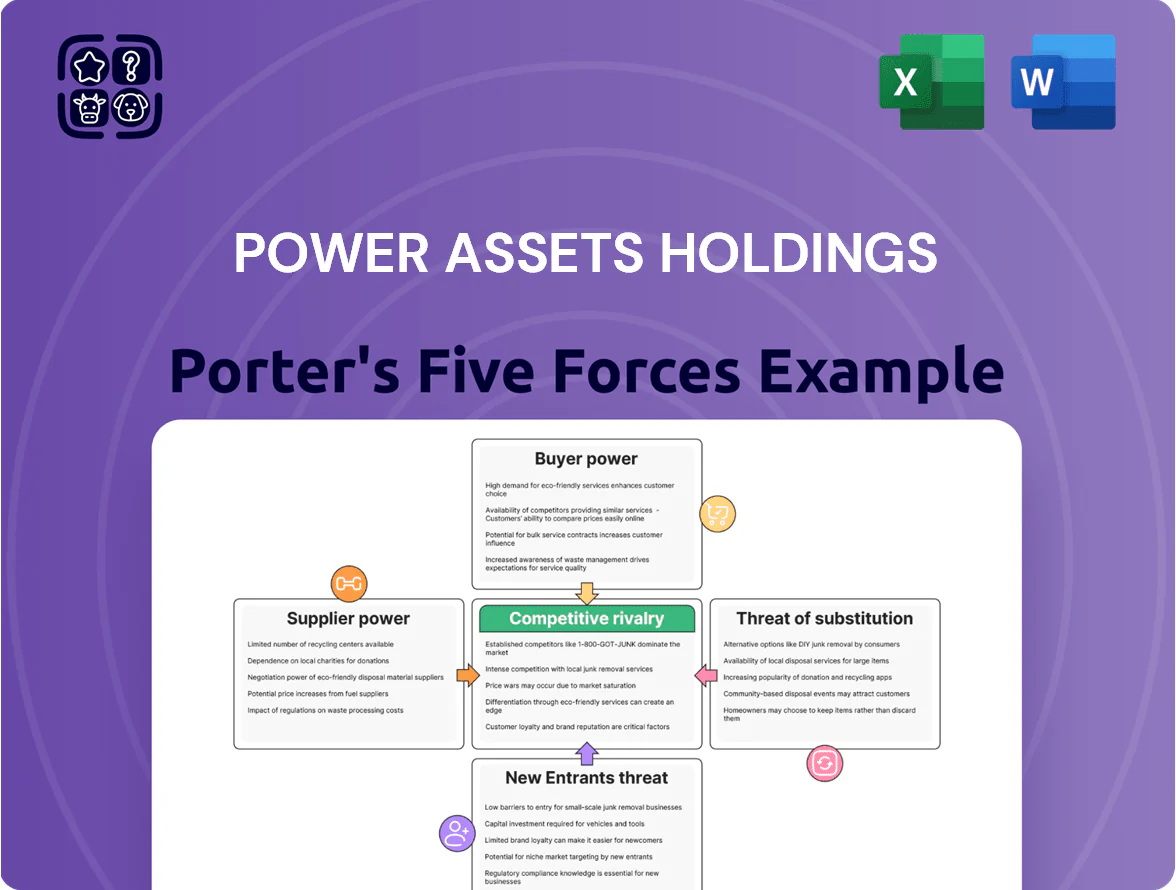

Power Assets Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Power Assets Holdings faces moderate supplier and buyer power, regulated barriers limiting new entrants, and evolving substitute threats from renewables—creating a balanced but shifting competitive landscape that rewards strategic adaptability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Power Assets Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Equipment Providers

The global market for high-voltage equipment is highly concentrated: the top 5 suppliers (Siemens Energy, GE Vernova, Hitachi Energy, ABB, and Toshiba) held roughly 60% of transmission equipment revenue in 2024, raising supplier leverage for Power Assets Holdings as it scales smart grids and offshore wind.

Volatility in Global Fuel Supply Markets

Thermal assets at Power Assets Holdings remain exposed to natural gas and coal price swings; in 2024 Asian LNG spot prices averaged ~USD 12/MMBtu, up 35% vs 2022, while Australian thermal coal rose ~22% in 2023, squeezing margins if costs can't be passed to tariffs.

Labor Market Tightness for Specialized Engineering

The shift to green energy demands engineers skilled in renewables, storage, and grid modernization, and Power Assets faces tight labor supply across the UK, Australia, and Hong Kong where vacancy rates for specialist engineers hit 6–9% in 2024 and salaries rose 8–12% year-over-year. This scarcity boosts bargaining power for unions and niche firms, pushing up wage bills and contracting premiums—estimates show project O&M costs can rise 3–5% from higher labor rates. In markets with 70–85% retention challenges for technical staff, contract flexibility and long-term talent partnerships become essential to control costs and delivery risk.

Dependence on Renewable Technology Manufacturers

Dependence on a few dominant manufacturers for wind turbines, solar PV and battery systems raises supplier power for Power Assets Holdings; global decarbonization drove 2024 orders—wind +17% and solar +18% YoY—tightening lead times to 12–24 months for large turbines.

Power Assets competes with utilities worldwide for priority delivery and discounts, raising capex risk: a 2024 IEA estimate put battery raw-material price volatility at ±25% over 12 months.

- Lead times 12–24 months for large turbines

- Wind orders +17% and solar +18% YoY in 2024

- Battery raw-material price volatility ~±25% (2024 IEA)

- Semiconductor/rare-earth bottlenecks raise capex per MW

Regulatory Influence on Supplier Standards

Governments where Power Assets Holdings (Hong Kong-listed 00006.HK) operates tightened supply-chain ESG rules in 2024–2025, shrinking eligible suppliers by an estimated 25% in Hong Kong and 30% in Australia, raising compliant supplier premiums ~10–15%.

That shortage boosts compliant suppliers’ bargaining power, letting them demand higher prices and stricter contract terms because alternative green-certified vendors are scarce.

- 25% fewer eligible HK suppliers (2024)

- 30% fewer in Australia (2025)

- 10–15% price premium for certified suppliers

Supplier squeeze: concentrated HV supply, long lead times, volatile batteries, rising O&M

Supplier power is high: top 5 HV suppliers held ~60% of 2024 market, turbine lead times 12–24 months, battery material price volatility ±25% and certified suppliers priced 10–15% higher after 25–30% cuts in eligible vendors (HK 2024, Australia 2025), while engineer scarcity (6–9% vacancies) lifts O&M costs ~3–5%.

| Metric | 2024–25 |

|---|---|

| Top‑5 market share | ~60% |

| Turbine lead times | 12–24 months |

| Battery volatility | ±25% |

| Eligible suppliers cut | HK 25%, AU 30% |

| Certified premium | 10–15% |

| Engineer vacancies | 6–9% |

| O&M cost rise | 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Power Assets Holdings that uncovers competitive intensity, customer and supplier power, entry barriers, and substitute threats, highlighting strategic risks and opportunities to protect profitability and market position.

Instantly view Power Assets Holdings’ competitive pressures across all five forces—clear, one-sheet analysis ideal for quick strategic decisions or inclusion in investor decks.

Customers Bargaining Power

Regulated Pricing Frameworks

In Hong Kong, the Scheme of Control Agreement caps allowed returns—Power Assets Holdings faces a permitted return around 9.99% on regulated operations under recent SCAs, which limits pricing power but stabilizes revenue.

That stability shifts pricing influence to the government regulator, acting for consumers, so customers exercise power indirectly through tariff approvals and service standards.

Regulators focus on affordability and reliability over profit, constraining upside: tariffs rose ~2.5% CAGR 2015–2023 while margins stayed narrow for regulated segments.

Availability of Decentralized Energy Solutions

By end-2025 residential solar plus battery costs fell ~30% vs 2020, letting commercial/domestic users cut grid reliance; US median residential system+storage now ≈ $15,000–$20,000 after incentives, enabling meaningful self-generation.

As affordability rises, customers force utilities to revise tariffs and offer services; utility customer churn risk grows—10–15% higher in regions with >20% rooftop uptake.

Customers shift from passive buyers to active market players, choosing behind-the-meter generation, demand response, or PPA-style contracts, increasing bargaining power over price and service terms.

Industrial Customer Negotiation Leverage

Public and Political Pressure on Utility Rates

Public anger over energy bills—UK household energy bills rose ~40% in 2022 and Australia saw retail electricity prices jump ~20% in 2022–24—pushes politicians to block utility rate hikes for Power Assets Holdings, limiting pass-through of higher fuel and maintenance costs.

Consumer groups and MPs in the UK and Australia have prompted probes and proposals for windfall taxes (2022–25), so regulatory risk compresses margin flexibility and raises the cost of capital for price increases.

- UK household bills +40% in 2022 (Ofgem context)

- Australia retail electricity ~+20% 2022–24

- Windfall tax proposals 2022–25 increase political risk

- Limits on price pass-through compress margins

Energy Efficiency and Demand Response Programs

Technological advances like smart meters and home energy management systems let customers cut consumption in real time; by 2024, 220 million smart meters were installed globally, raising household control and lowering billed volumes.

Demand response programs—14 GW of residential capacity enrolled in the US by 2023—let customers shift load to avoid peak tariffs, reducing utilities’ billable energy and peak-margin revenue.

Greater visibility and control erode Power Assets Holdings’ pricing power, forcing moves toward value-added services and performance-based contracts.

- 220 million smart meters globally (2024)

- 14 GW residential DR capacity in US (2023)

- Lower peak margins; shift to service revenue

Rise of customer power: cheaper rooftop solar, PPAs cut utility margins

Customers’ bargaining power is rising: regulated returns (≈9.99% SCA) limit price moves while regulators and politics cap tariffs; rooftop solar+storage costs fell ~30% since 2020, driving commercial/household self‑supply and 10–15% higher churn where uptake>20%; C&I accounts (40–55% demand) secure PPAs with 5–20% discounts, forcing utilities toward service contracts.

| Metric | Value |

|---|---|

| Permitted return | ≈9.99% |

| Rooftop cost drop | ~30% vs 2020 |

| C&I demand share | 40–55% |

| PPA discounts | 5–20% |

Full Version Awaits

Power Assets Holdings Porter's Five Forces Analysis

This preview shows the exact Power Assets Holdings Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Power Assets Holdings faces moderate supplier and buyer power, regulated barriers limiting new entrants, and evolving substitute threats from renewables—creating a balanced but shifting competitive landscape that rewards strategic adaptability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Power Assets Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Equipment Providers

The global market for high-voltage equipment is highly concentrated: the top 5 suppliers (Siemens Energy, GE Vernova, Hitachi Energy, ABB, and Toshiba) held roughly 60% of transmission equipment revenue in 2024, raising supplier leverage for Power Assets Holdings as it scales smart grids and offshore wind.

Volatility in Global Fuel Supply Markets

Thermal assets at Power Assets Holdings remain exposed to natural gas and coal price swings; in 2024 Asian LNG spot prices averaged ~USD 12/MMBtu, up 35% vs 2022, while Australian thermal coal rose ~22% in 2023, squeezing margins if costs can't be passed to tariffs.

Labor Market Tightness for Specialized Engineering

The shift to green energy demands engineers skilled in renewables, storage, and grid modernization, and Power Assets faces tight labor supply across the UK, Australia, and Hong Kong where vacancy rates for specialist engineers hit 6–9% in 2024 and salaries rose 8–12% year-over-year. This scarcity boosts bargaining power for unions and niche firms, pushing up wage bills and contracting premiums—estimates show project O&M costs can rise 3–5% from higher labor rates. In markets with 70–85% retention challenges for technical staff, contract flexibility and long-term talent partnerships become essential to control costs and delivery risk.

Dependence on Renewable Technology Manufacturers

Dependence on a few dominant manufacturers for wind turbines, solar PV and battery systems raises supplier power for Power Assets Holdings; global decarbonization drove 2024 orders—wind +17% and solar +18% YoY—tightening lead times to 12–24 months for large turbines.

Power Assets competes with utilities worldwide for priority delivery and discounts, raising capex risk: a 2024 IEA estimate put battery raw-material price volatility at ±25% over 12 months.

- Lead times 12–24 months for large turbines

- Wind orders +17% and solar +18% YoY in 2024

- Battery raw-material price volatility ~±25% (2024 IEA)

- Semiconductor/rare-earth bottlenecks raise capex per MW

Regulatory Influence on Supplier Standards

Governments where Power Assets Holdings (Hong Kong-listed 00006.HK) operates tightened supply-chain ESG rules in 2024–2025, shrinking eligible suppliers by an estimated 25% in Hong Kong and 30% in Australia, raising compliant supplier premiums ~10–15%.

That shortage boosts compliant suppliers’ bargaining power, letting them demand higher prices and stricter contract terms because alternative green-certified vendors are scarce.

- 25% fewer eligible HK suppliers (2024)

- 30% fewer in Australia (2025)

- 10–15% price premium for certified suppliers

Supplier squeeze: concentrated HV supply, long lead times, volatile batteries, rising O&M

Supplier power is high: top 5 HV suppliers held ~60% of 2024 market, turbine lead times 12–24 months, battery material price volatility ±25% and certified suppliers priced 10–15% higher after 25–30% cuts in eligible vendors (HK 2024, Australia 2025), while engineer scarcity (6–9% vacancies) lifts O&M costs ~3–5%.

| Metric | 2024–25 |

|---|---|

| Top‑5 market share | ~60% |

| Turbine lead times | 12–24 months |

| Battery volatility | ±25% |

| Eligible suppliers cut | HK 25%, AU 30% |

| Certified premium | 10–15% |

| Engineer vacancies | 6–9% |

| O&M cost rise | 3–5% |

What is included in the product

Tailored Porter's Five Forces analysis for Power Assets Holdings that uncovers competitive intensity, customer and supplier power, entry barriers, and substitute threats, highlighting strategic risks and opportunities to protect profitability and market position.

Instantly view Power Assets Holdings’ competitive pressures across all five forces—clear, one-sheet analysis ideal for quick strategic decisions or inclusion in investor decks.

Customers Bargaining Power

Regulated Pricing Frameworks

In Hong Kong, the Scheme of Control Agreement caps allowed returns—Power Assets Holdings faces a permitted return around 9.99% on regulated operations under recent SCAs, which limits pricing power but stabilizes revenue.

That stability shifts pricing influence to the government regulator, acting for consumers, so customers exercise power indirectly through tariff approvals and service standards.

Regulators focus on affordability and reliability over profit, constraining upside: tariffs rose ~2.5% CAGR 2015–2023 while margins stayed narrow for regulated segments.

Availability of Decentralized Energy Solutions

By end-2025 residential solar plus battery costs fell ~30% vs 2020, letting commercial/domestic users cut grid reliance; US median residential system+storage now ≈ $15,000–$20,000 after incentives, enabling meaningful self-generation.

As affordability rises, customers force utilities to revise tariffs and offer services; utility customer churn risk grows—10–15% higher in regions with >20% rooftop uptake.

Customers shift from passive buyers to active market players, choosing behind-the-meter generation, demand response, or PPA-style contracts, increasing bargaining power over price and service terms.

Industrial Customer Negotiation Leverage

Public and Political Pressure on Utility Rates

Public anger over energy bills—UK household energy bills rose ~40% in 2022 and Australia saw retail electricity prices jump ~20% in 2022–24—pushes politicians to block utility rate hikes for Power Assets Holdings, limiting pass-through of higher fuel and maintenance costs.

Consumer groups and MPs in the UK and Australia have prompted probes and proposals for windfall taxes (2022–25), so regulatory risk compresses margin flexibility and raises the cost of capital for price increases.

- UK household bills +40% in 2022 (Ofgem context)

- Australia retail electricity ~+20% 2022–24

- Windfall tax proposals 2022–25 increase political risk

- Limits on price pass-through compress margins

Energy Efficiency and Demand Response Programs

Technological advances like smart meters and home energy management systems let customers cut consumption in real time; by 2024, 220 million smart meters were installed globally, raising household control and lowering billed volumes.

Demand response programs—14 GW of residential capacity enrolled in the US by 2023—let customers shift load to avoid peak tariffs, reducing utilities’ billable energy and peak-margin revenue.

Greater visibility and control erode Power Assets Holdings’ pricing power, forcing moves toward value-added services and performance-based contracts.

- 220 million smart meters globally (2024)

- 14 GW residential DR capacity in US (2023)

- Lower peak margins; shift to service revenue

Rise of customer power: cheaper rooftop solar, PPAs cut utility margins

Customers’ bargaining power is rising: regulated returns (≈9.99% SCA) limit price moves while regulators and politics cap tariffs; rooftop solar+storage costs fell ~30% since 2020, driving commercial/household self‑supply and 10–15% higher churn where uptake>20%; C&I accounts (40–55% demand) secure PPAs with 5–20% discounts, forcing utilities toward service contracts.

| Metric | Value |

|---|---|

| Permitted return | ≈9.99% |

| Rooftop cost drop | ~30% vs 2020 |

| C&I demand share | 40–55% |

| PPA discounts | 5–20% |

Full Version Awaits

Power Assets Holdings Porter's Five Forces Analysis

This preview shows the exact Power Assets Holdings Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.