Phoenix Publishing & Media(PPM) Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

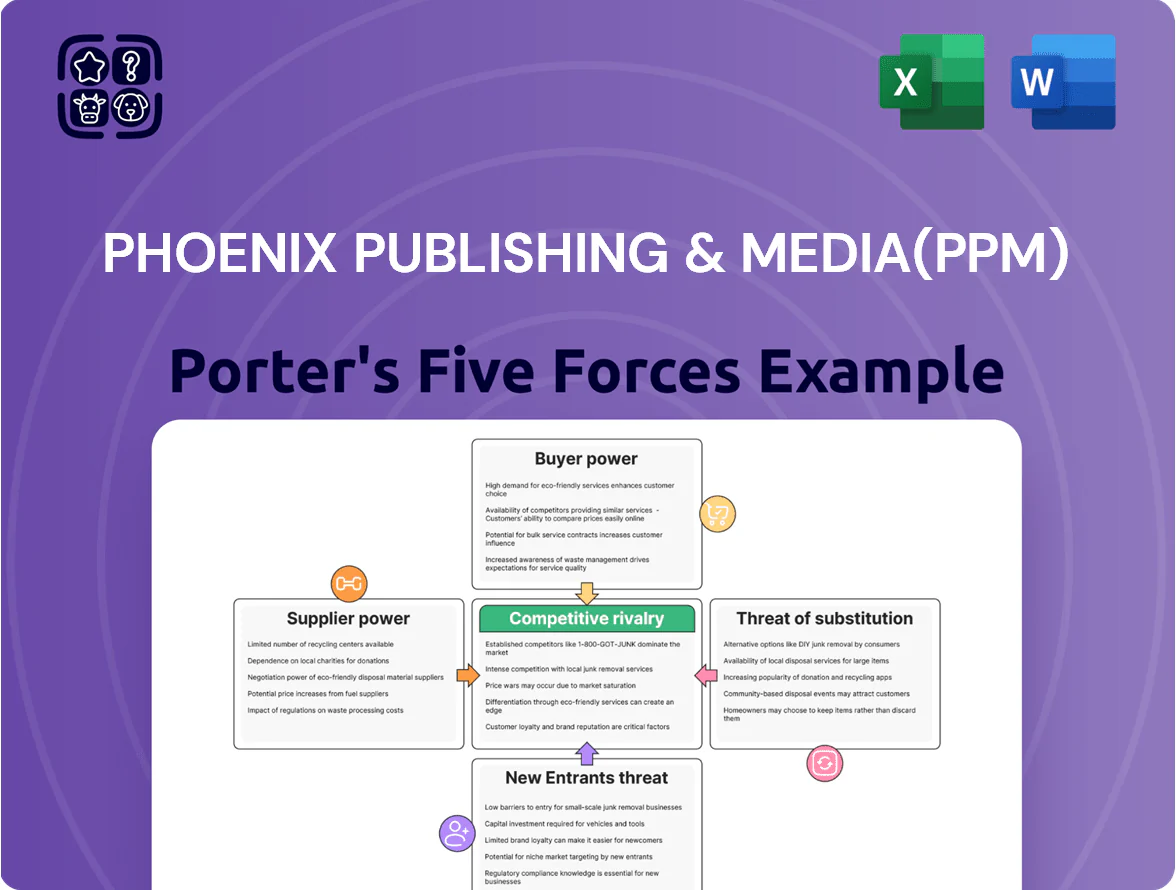

Phoenix Publishing & Media (PPM) faces moderate supplier power, intense buyer expectations for digital content, rising substitute threats from online platforms, and fragmented rivalry among domestic peers—while regulatory and scale barriers temper new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Phoenix Publishing & Media(PPM)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of paper and raw material providers

The cost of paper stayed a key expense for Phoenix Publishing & Media in 2025, roughly 18–22% of production costs per industry estimates; PPM's scale helps, but China’s top 5 paper mills now control over 60% of domestic capacity, giving them pricing leverage. Global pulp prices rose ~12% in 2024–25 and tighter environmental rules cut usable output, causing supply volatility that squeezes PPM’s gross margins by an estimated 1–2 percentage points.

Reliance on high-profile authors and IP creators

Securing exclusive rights to best-selling authors and prestigious IP is critical for Phoenix Publishing & Media to protect its 2024 mainland China market share, where top 20 titles generated roughly 28% of trade book sales; losing exclusives risks steep revenue drops. Top-tier writers now command more leverage, choosing between legacy houses and digital self-publishing—global indie author revenues rose to $1.2bn in 2023, boosting bargaining power. PPM must offer competitive royalties (often 15–25% for print, higher for digital) and robust marketing spends—successful campaigns spend up to 10% of projected book revenue—to retain these creators and IP.

Digital infrastructure and cloud service providers

As Phoenix Publishing & Media (PPM) grows digital content and education services, reliance on cloud providers (AWS, Alibaba Cloud, Tencent Cloud) rose—cloud spend likely exceeds 15% of IT budget, raising supplier leverage.

High switching costs for migrating petabyte-scale archives and custom LMS platforms give vendors pricing power; multi-year contracts and data egress fees lock in providers.

PPM needs long-term strategic partnerships, SLAs, and hybrid multi-cloud setups to secure uptime and integration; in 2024 industry uptime targets averaged 99.95%.

Printing and logistics specialized equipment vendors

The maintenance and upgrading of PPMs advanced printing facilities depend on a few global vendors supplying presses and color management tech, giving suppliers pricing and service leverage; in 2024 China print-capex imports rose 6% while global press makers consolidated to 3–4 majors. PPM reduces risk by diversifying equipment brands and scaling domestic technical teams, cutting third-party service spend by an estimated 12% in 2023.

- Limited vendors: 3–4 global majors

- 2024 China print-capex imports +6%

- Long-term service contracts drive switching costs

- PPM reduced third-party spend ~12% in 2023

Acquisition of international copyrights

For global expansion and translated works, Phoenix Publishing & Media (state-owned) depends on international literary agencies and foreign publishers who control access to high-demand titles and can set terms on distribution rights and revenue splits; in 2024 China imported roughly $1.2bn in book rights, concentrating bargaining with a few major agencies.

PPM offsets supplier power via state backing and a 50,000+ retail network and 2,000+ e-distribution partners, keeping it a preferred licensee despite royalty rates of 10–25% on major titles.

- Few suppliers control hit titles

- 2024 China book-rights imports ~$1.2bn

- PPM: state-owned, 50,000+ outlets

- Typical royalties 10–25%

High supplier leverage: paper, pulp, cloud & royalties squeeze margins despite state support

Suppliers wield moderate-to-high power: paper and pulp costs (paper ~18–22% of production; pulp +12% in 2024–25) and 60% domestic paper capacity concentration raise input risk, while 3–4 global press vendors and cloud providers (cloud >15% IT spend) add vendor leverage; author/IP suppliers demand 10–25% royalties, and 2024 book-rights imports ≈$1.2bn—PPM offsets this with state backing and 50,000+ retail outlets.

| Metric | Value (2024–25) |

|---|---|

| Paper share of costs | 18–22% |

| Domestic paper capacity (top5) | >60% |

| Pulp price change | +12% |

| Cloud spend | >15% IT budget |

| Book-rights imports | $1.2bn |

| Typical royalties | 10–25% |

What is included in the product

Tailored Porter's Five Forces analysis for Phoenix Publishing & Media (PPM) uncovering key competitive drivers, buyer and supplier power, threat of substitutes and entrants, and strategic levers to defend market share and profitability.

A compact Porter's Five Forces snapshot for Phoenix Publishing & Media that highlights competitive threats and buyer/supplier pressure—ideal for swift strategic decisions.

Customers Bargaining Power

Centralized government procurement for educational materials

Dominance of major e-commerce and digital platforms

Large online retailers and digital reading platforms like JD.com, Taobao (Alibaba) and Tencent’s China Literature control roughly 60–70% of China's digital book sales as of 2024, giving them strong leverage over pricing and placement.

They push deep discounts and heavy promotions—often 20–50% off—and require cooperative marketing, which has squeezed publisher gross margins by an estimated 5–12 percentage points for many houses.

PPM must keep visibility on these platforms to capture reach, and simultaneously scale its own DTC channels—subscriptions, app sales, and official stores—to reclaim pricing power and protect a 10–15% target margin uplift.

Institutional library and academic budget constraints

Public and academic libraries are core buyers for PPM’s specialist content but face tight budgets—US public library materials spending fell 2.5% to $1.34B in 2023, and global academic library subscription spend grew only 1.8% in 2024, pushing institutions toward bundled digital subscriptions.

PPM must offer flexible, high-volume licenses and campus-wide digital access; otherwise procurement favors big aggregators—over 60% of North American universities now prefer multi-title deals, so single-title sales risk decline.

Individual consumer price sensitivity in digital media

Individual readers in digital media are highly price-sensitive as free and low-cost content grew 18% in consumption from 2020–2024, and 62% of Chinese users comparison-shop across storefronts in 2025, pressuring Phoenix Publishing & Media (PPM) margins.

Consumers now expect rich multimedia: video, interactivity, and AR, raising per-unit delivery costs by an estimated 12% versus text-only content.

PPM must deploy advanced analytics and tiered loyalty programs—targeting a 5–10% uplift in retention—to stay competitive in a price-driven retail market.

- Free/low-cost content +18% (2020–2024)

- 62% of users comparison-shop (2025)

- Multimedia delivery costs +12%

- Target retention uplift 5–10% via analytics & loyalty

Corporate and B2B cultural service contracts

- Volume discounts: 10–25% typical

- Contract length: 3–5 years common

- Market entrants: ~15% annual growth in 2023 (major cities)

- Margin impact: compresses gross margins by several percentage points

PPM margins squeezed by buyers—DTC, analytics & tiered pricing can reclaim 10–15%

| Metric | Value |

|---|---|

| Govt textbook share (2024) | 30–40% |

| Digital retail share (2024) | 60–70% |

| Platform discounts | 20–50% |

| Paper/print cost rise (2023–24) | 8–12% |

| Multimedia cost uplift | +12% |

| Users comparison-shop (2025) | 62% |

| Target margin uplift via DTC | 10–15% |

Same Document Delivered

Phoenix Publishing & Media(PPM) Porter's Five Forces Analysis

This preview shows the exact Phoenix Publishing & Media Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s the fully formatted, ready-to-use document. The report covers threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and industry rivalry with actionable insights and evidence-based conclusions. Upon payment you’ll get instant access to this same file for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Phoenix Publishing & Media (PPM) faces moderate supplier power, intense buyer expectations for digital content, rising substitute threats from online platforms, and fragmented rivalry among domestic peers—while regulatory and scale barriers temper new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Phoenix Publishing & Media(PPM)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of paper and raw material providers

The cost of paper stayed a key expense for Phoenix Publishing & Media in 2025, roughly 18–22% of production costs per industry estimates; PPM's scale helps, but China’s top 5 paper mills now control over 60% of domestic capacity, giving them pricing leverage. Global pulp prices rose ~12% in 2024–25 and tighter environmental rules cut usable output, causing supply volatility that squeezes PPM’s gross margins by an estimated 1–2 percentage points.

Reliance on high-profile authors and IP creators

Securing exclusive rights to best-selling authors and prestigious IP is critical for Phoenix Publishing & Media to protect its 2024 mainland China market share, where top 20 titles generated roughly 28% of trade book sales; losing exclusives risks steep revenue drops. Top-tier writers now command more leverage, choosing between legacy houses and digital self-publishing—global indie author revenues rose to $1.2bn in 2023, boosting bargaining power. PPM must offer competitive royalties (often 15–25% for print, higher for digital) and robust marketing spends—successful campaigns spend up to 10% of projected book revenue—to retain these creators and IP.

Digital infrastructure and cloud service providers

As Phoenix Publishing & Media (PPM) grows digital content and education services, reliance on cloud providers (AWS, Alibaba Cloud, Tencent Cloud) rose—cloud spend likely exceeds 15% of IT budget, raising supplier leverage.

High switching costs for migrating petabyte-scale archives and custom LMS platforms give vendors pricing power; multi-year contracts and data egress fees lock in providers.

PPM needs long-term strategic partnerships, SLAs, and hybrid multi-cloud setups to secure uptime and integration; in 2024 industry uptime targets averaged 99.95%.

Printing and logistics specialized equipment vendors

The maintenance and upgrading of PPMs advanced printing facilities depend on a few global vendors supplying presses and color management tech, giving suppliers pricing and service leverage; in 2024 China print-capex imports rose 6% while global press makers consolidated to 3–4 majors. PPM reduces risk by diversifying equipment brands and scaling domestic technical teams, cutting third-party service spend by an estimated 12% in 2023.

- Limited vendors: 3–4 global majors

- 2024 China print-capex imports +6%

- Long-term service contracts drive switching costs

- PPM reduced third-party spend ~12% in 2023

Acquisition of international copyrights

For global expansion and translated works, Phoenix Publishing & Media (state-owned) depends on international literary agencies and foreign publishers who control access to high-demand titles and can set terms on distribution rights and revenue splits; in 2024 China imported roughly $1.2bn in book rights, concentrating bargaining with a few major agencies.

PPM offsets supplier power via state backing and a 50,000+ retail network and 2,000+ e-distribution partners, keeping it a preferred licensee despite royalty rates of 10–25% on major titles.

- Few suppliers control hit titles

- 2024 China book-rights imports ~$1.2bn

- PPM: state-owned, 50,000+ outlets

- Typical royalties 10–25%

High supplier leverage: paper, pulp, cloud & royalties squeeze margins despite state support

Suppliers wield moderate-to-high power: paper and pulp costs (paper ~18–22% of production; pulp +12% in 2024–25) and 60% domestic paper capacity concentration raise input risk, while 3–4 global press vendors and cloud providers (cloud >15% IT spend) add vendor leverage; author/IP suppliers demand 10–25% royalties, and 2024 book-rights imports ≈$1.2bn—PPM offsets this with state backing and 50,000+ retail outlets.

| Metric | Value (2024–25) |

|---|---|

| Paper share of costs | 18–22% |

| Domestic paper capacity (top5) | >60% |

| Pulp price change | +12% |

| Cloud spend | >15% IT budget |

| Book-rights imports | $1.2bn |

| Typical royalties | 10–25% |

What is included in the product

Tailored Porter's Five Forces analysis for Phoenix Publishing & Media (PPM) uncovering key competitive drivers, buyer and supplier power, threat of substitutes and entrants, and strategic levers to defend market share and profitability.

A compact Porter's Five Forces snapshot for Phoenix Publishing & Media that highlights competitive threats and buyer/supplier pressure—ideal for swift strategic decisions.

Customers Bargaining Power

Centralized government procurement for educational materials

Dominance of major e-commerce and digital platforms

Large online retailers and digital reading platforms like JD.com, Taobao (Alibaba) and Tencent’s China Literature control roughly 60–70% of China's digital book sales as of 2024, giving them strong leverage over pricing and placement.

They push deep discounts and heavy promotions—often 20–50% off—and require cooperative marketing, which has squeezed publisher gross margins by an estimated 5–12 percentage points for many houses.

PPM must keep visibility on these platforms to capture reach, and simultaneously scale its own DTC channels—subscriptions, app sales, and official stores—to reclaim pricing power and protect a 10–15% target margin uplift.

Institutional library and academic budget constraints

Public and academic libraries are core buyers for PPM’s specialist content but face tight budgets—US public library materials spending fell 2.5% to $1.34B in 2023, and global academic library subscription spend grew only 1.8% in 2024, pushing institutions toward bundled digital subscriptions.

PPM must offer flexible, high-volume licenses and campus-wide digital access; otherwise procurement favors big aggregators—over 60% of North American universities now prefer multi-title deals, so single-title sales risk decline.

Individual consumer price sensitivity in digital media

Individual readers in digital media are highly price-sensitive as free and low-cost content grew 18% in consumption from 2020–2024, and 62% of Chinese users comparison-shop across storefronts in 2025, pressuring Phoenix Publishing & Media (PPM) margins.

Consumers now expect rich multimedia: video, interactivity, and AR, raising per-unit delivery costs by an estimated 12% versus text-only content.

PPM must deploy advanced analytics and tiered loyalty programs—targeting a 5–10% uplift in retention—to stay competitive in a price-driven retail market.

- Free/low-cost content +18% (2020–2024)

- 62% of users comparison-shop (2025)

- Multimedia delivery costs +12%

- Target retention uplift 5–10% via analytics & loyalty

Corporate and B2B cultural service contracts

- Volume discounts: 10–25% typical

- Contract length: 3–5 years common

- Market entrants: ~15% annual growth in 2023 (major cities)

- Margin impact: compresses gross margins by several percentage points

PPM margins squeezed by buyers—DTC, analytics & tiered pricing can reclaim 10–15%

| Metric | Value |

|---|---|

| Govt textbook share (2024) | 30–40% |

| Digital retail share (2024) | 60–70% |

| Platform discounts | 20–50% |

| Paper/print cost rise (2023–24) | 8–12% |

| Multimedia cost uplift | +12% |

| Users comparison-shop (2025) | 62% |

| Target margin uplift via DTC | 10–15% |

Same Document Delivered

Phoenix Publishing & Media(PPM) Porter's Five Forces Analysis

This preview shows the exact Phoenix Publishing & Media Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s the fully formatted, ready-to-use document. The report covers threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and industry rivalry with actionable insights and evidence-based conclusions. Upon payment you’ll get instant access to this same file for download and use.