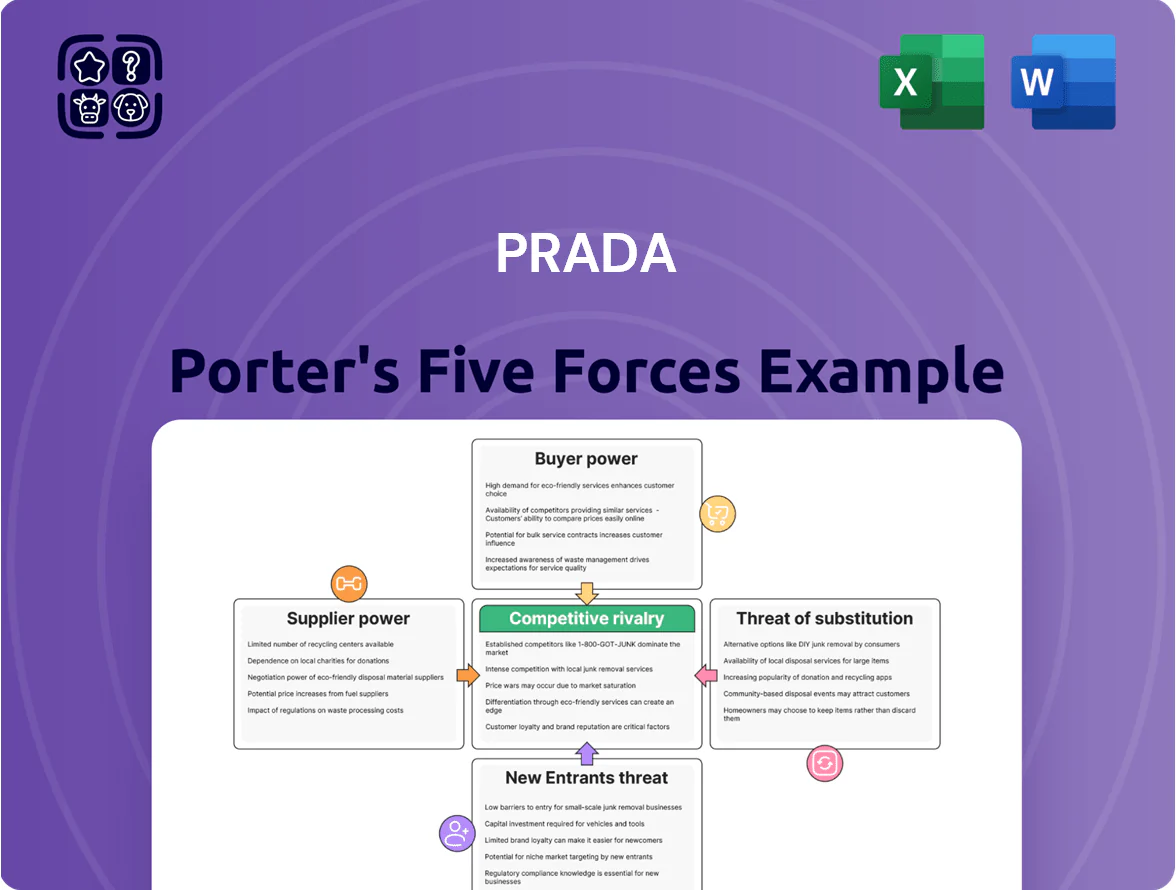

Prada Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Prada faces intense rivalry from luxury peers, rising buyer sophistication, and moderate supplier power—while high brand moat limits substitutes but e-commerce and fast-fashion spillover raise threats; regulatory and macro shifts add external pressure. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Prada’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of high-quality raw materials

The bargaining power of suppliers is moderate: Prada needs extremely high-grade leather and specialized textiles supplied by a few premium tanneries and mills, giving those sellers niche leverage. By year-end 2025 Prada completed strategic acquisitions of three Italian manufacturers, raising in-house sourcing to roughly 28% of leather and textile needs, cutting exposure to external price swings. Vertical integration thus lowers supplier power while stabilizing input costs.

Scarcity of skilled artisanal labor

High global demand for traditional Italian craftsmanship gives small artisan groups strong bargaining power; luxury peers bid for the same talent, pushing skilled labor costs up—craft wages rose ~8% in Italy’s luxury textiles sector in 2024, per Istat-linked reports, increasing Prada’s COGS pressure.

Prada counters by funding internal training academies and long-term contracts; Prada’s 2024 sustainability report shows ~€25m invested in skills and 1,200 trainees since 2019 to secure a steady artisan pipeline.

Strict ESG and traceability requirements

As of 2025, Prada enforces strict ESG and digital traceability rules that shrink its supplier pool to roughly 15–20% of luxury leather and textile vendors; certified suppliers often charge 8–12% higher margins to cover tech and audit costs. Prada offsets this by offering multi-year contracts (typically 3–5 years) covering ~60% of spend, creating mutual dependence that stabilizes lead times and limits supplier bargaining leverage.

Switching costs for specialized components

- Co-development timelines: 6–18 months

- Replacement cost uplift: ~15–30% of unit COGS

- Technical suppliers hold greater bargaining power vs commodity vendors

- Dependency risks: design compromise if swapped quickly

Impact of logistics and energy costs

Suppliers of logistics and energy saw bargaining power fluctuate through 2025 as freight rates fell 18% from 2022 highs while European wholesale gas prices remained 2–3x pre‑2021 levels, squeezing margins for luxury supply chains.

Prada, a significant client, still faces exposure to global carriers and regional energy tariffs; spot container rates can swing 30%+ seasonally and Italian industrial electricity prices averaged €160/MWh in 2024.

To reduce this, Prada expanded localized production: 25% of ready‑to‑wear capacity moved closer to EU markets by end‑2024, cutting transport spend on those lines by ~22%.

- Freight rates down 18% vs 2022

- EU gas 2–3x pre‑2021; electricity ~€160/MWh (2024)

- Spot container volatility >30% seasonally

- 25% production localized; ~22% transport cost cut

Prada halves supplier risk: 28% in‑house, 60% contracted, premiums and wages rise

Supplier power is moderate: Prada cut external sourcing to ~72% by 2025 after three Italian acquisitions, raising in‑house to ~28%, and uses 3–5 year contracts covering ~60% spend to curb price swings. Craft wages rose ~8% in 2024; certified vendors charge 8–12% premiums. Co‑development timelines 6–18 months; replacement costs +15–30% of unit COGS. Freight down 18% vs 2022; EU electricity ~€160/MWh (2024).

| Metric | Value |

|---|---|

| In‑house sourcing | 28% |

| Contracted spend | 60% |

| Craft wage rise (2024) | ~8% |

| Supplier premium | 8–12% |

| Co‑dev time | 6–18m |

| Replacement cost | +15–30% |

What is included in the product

Tailored exclusively for Prada, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, entry barriers, substitute threats, and disruptive risks shaping its luxury market positioning.

A concise Porter's Five Forces snapshot for Prada that highlights competitive threats and opportunities—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

Low switching costs in the luxury segment

Luxury buyers face almost no financial cost switching from Prada to Hermès, Chanel or Gucci, so buyer power is high—global luxury spending hit €323bn in 2023 and brand loyalties shift quickly.

Prada must keep innovating: in 2024 it increased marketing to €597m and elevated cultural relevance via collaborations and runway shows to protect desirability.

The firm builds emotional switching costs with exclusive events and bespoke services—Prada’s clienteling drove VIP sales growth of ~9% in 2024—discouraging brand hopping.

High price transparency via digital channels

By late 2025, instant price comparison via e-commerce and luxury aggregators (e.g., Farfetch, Yoox Net-a-Porter) means 67% of global luxury shoppers check multiple sites before buying, forcing Prada to counter visible seasonal markdowns and 8–12% regional price gaps. Prada’s strict MSRP control limits discounting, but transparency compels a tighter global pricing policy to avoid brand dilution and preserve a 20–30% luxury margin band.

The rise of the Very Important Client (VIC) segment

Influence of Gen Z and brand sentiment

Younger consumers, driven by Gen Z momentum and Miu Miu’s 2025 resurgence, wield strong bargaining power via social media: 68% of Gen Z report buying based on viral trends (Morning Consult, 2024) so demand can swing fast after a viral post or ethics backlash.

Prada counters with a responsive digital team, cultural collaborations, and real-time PR: Prada’s social engagement rose 22% YoY in 2024 after targeted campaigns, reducing short-term sales volatility.

- 68% Gen Z buy on viral trends

- Miu Miu 2025 resurgence raises youth influence

- Brand ethics/cool factor drive rapid demand shifts

- Prada social engagement +22% YoY 2024

Wholesale buyer consolidation

Prada’s shift to directly-operated stores reduces wholesale reliance, but remaining partners—like Nordstrom, Saks Fifth Avenue and Galeries Lafayette—still hold strong leverage by controlling prime mall and city-center real estate and access to affluent customer segments; in 2024 luxury department stores accounted for roughly 18% of global luxury sales, concentrating negotiating power.

Consolidation among these retailers (top 10 luxury department stores roughly 40% share in Europe/US by floor-space value in 2024) lets them press Prada on margins, markdown policies and exclusive SKU allocations, forcing Prada to trade higher wholesale discounts or limited product drops to secure premium placement.

- Wholesale still ≈18% of luxury sales (2024)

- Top 10 dept stores ≈40% floor-space value (Europe/US, 2024)

- Consolidation → stronger margin negotiation

- Exclusive allocations used to secure premium placement

Prada Fights Retailer Power as Few VIPs and Easy Switching Shape Luxury Revenues

Buyers have high power: low switching costs across luxury brands, 67% check multiple sites (2025), and top <5% of clients drive ~30–40% revenue; Prada counters with VIP services, tighter global pricing, and boosted marketing (€597m in 2024) but still faces retailer leverage (wholesale ≈18% of luxury sales, top 10 dept stores ≈40% floor-space value, 2024).

| Metric | Value |

|---|---|

| Global luxury spend 2023 | €323bn |

| Prada marketing 2024 | €597m |

| Shoppers compare sites (2025) | 67% |

| Wholesale share (2024) | ≈18% |

Full Version Awaits

Prada Porter's Five Forces Analysis

This preview shows the exact Prada Porter's Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Prada faces intense rivalry from luxury peers, rising buyer sophistication, and moderate supplier power—while high brand moat limits substitutes but e-commerce and fast-fashion spillover raise threats; regulatory and macro shifts add external pressure. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Prada’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of high-quality raw materials

The bargaining power of suppliers is moderate: Prada needs extremely high-grade leather and specialized textiles supplied by a few premium tanneries and mills, giving those sellers niche leverage. By year-end 2025 Prada completed strategic acquisitions of three Italian manufacturers, raising in-house sourcing to roughly 28% of leather and textile needs, cutting exposure to external price swings. Vertical integration thus lowers supplier power while stabilizing input costs.

Scarcity of skilled artisanal labor

High global demand for traditional Italian craftsmanship gives small artisan groups strong bargaining power; luxury peers bid for the same talent, pushing skilled labor costs up—craft wages rose ~8% in Italy’s luxury textiles sector in 2024, per Istat-linked reports, increasing Prada’s COGS pressure.

Prada counters by funding internal training academies and long-term contracts; Prada’s 2024 sustainability report shows ~€25m invested in skills and 1,200 trainees since 2019 to secure a steady artisan pipeline.

Strict ESG and traceability requirements

As of 2025, Prada enforces strict ESG and digital traceability rules that shrink its supplier pool to roughly 15–20% of luxury leather and textile vendors; certified suppliers often charge 8–12% higher margins to cover tech and audit costs. Prada offsets this by offering multi-year contracts (typically 3–5 years) covering ~60% of spend, creating mutual dependence that stabilizes lead times and limits supplier bargaining leverage.

Switching costs for specialized components

- Co-development timelines: 6–18 months

- Replacement cost uplift: ~15–30% of unit COGS

- Technical suppliers hold greater bargaining power vs commodity vendors

- Dependency risks: design compromise if swapped quickly

Impact of logistics and energy costs

Suppliers of logistics and energy saw bargaining power fluctuate through 2025 as freight rates fell 18% from 2022 highs while European wholesale gas prices remained 2–3x pre‑2021 levels, squeezing margins for luxury supply chains.

Prada, a significant client, still faces exposure to global carriers and regional energy tariffs; spot container rates can swing 30%+ seasonally and Italian industrial electricity prices averaged €160/MWh in 2024.

To reduce this, Prada expanded localized production: 25% of ready‑to‑wear capacity moved closer to EU markets by end‑2024, cutting transport spend on those lines by ~22%.

- Freight rates down 18% vs 2022

- EU gas 2–3x pre‑2021; electricity ~€160/MWh (2024)

- Spot container volatility >30% seasonally

- 25% production localized; ~22% transport cost cut

Prada halves supplier risk: 28% in‑house, 60% contracted, premiums and wages rise

Supplier power is moderate: Prada cut external sourcing to ~72% by 2025 after three Italian acquisitions, raising in‑house to ~28%, and uses 3–5 year contracts covering ~60% spend to curb price swings. Craft wages rose ~8% in 2024; certified vendors charge 8–12% premiums. Co‑development timelines 6–18 months; replacement costs +15–30% of unit COGS. Freight down 18% vs 2022; EU electricity ~€160/MWh (2024).

| Metric | Value |

|---|---|

| In‑house sourcing | 28% |

| Contracted spend | 60% |

| Craft wage rise (2024) | ~8% |

| Supplier premium | 8–12% |

| Co‑dev time | 6–18m |

| Replacement cost | +15–30% |

What is included in the product

Tailored exclusively for Prada, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer power, entry barriers, substitute threats, and disruptive risks shaping its luxury market positioning.

A concise Porter's Five Forces snapshot for Prada that highlights competitive threats and opportunities—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

Low switching costs in the luxury segment

Luxury buyers face almost no financial cost switching from Prada to Hermès, Chanel or Gucci, so buyer power is high—global luxury spending hit €323bn in 2023 and brand loyalties shift quickly.

Prada must keep innovating: in 2024 it increased marketing to €597m and elevated cultural relevance via collaborations and runway shows to protect desirability.

The firm builds emotional switching costs with exclusive events and bespoke services—Prada’s clienteling drove VIP sales growth of ~9% in 2024—discouraging brand hopping.

High price transparency via digital channels

By late 2025, instant price comparison via e-commerce and luxury aggregators (e.g., Farfetch, Yoox Net-a-Porter) means 67% of global luxury shoppers check multiple sites before buying, forcing Prada to counter visible seasonal markdowns and 8–12% regional price gaps. Prada’s strict MSRP control limits discounting, but transparency compels a tighter global pricing policy to avoid brand dilution and preserve a 20–30% luxury margin band.

The rise of the Very Important Client (VIC) segment

Influence of Gen Z and brand sentiment

Younger consumers, driven by Gen Z momentum and Miu Miu’s 2025 resurgence, wield strong bargaining power via social media: 68% of Gen Z report buying based on viral trends (Morning Consult, 2024) so demand can swing fast after a viral post or ethics backlash.

Prada counters with a responsive digital team, cultural collaborations, and real-time PR: Prada’s social engagement rose 22% YoY in 2024 after targeted campaigns, reducing short-term sales volatility.

- 68% Gen Z buy on viral trends

- Miu Miu 2025 resurgence raises youth influence

- Brand ethics/cool factor drive rapid demand shifts

- Prada social engagement +22% YoY 2024

Wholesale buyer consolidation

Prada’s shift to directly-operated stores reduces wholesale reliance, but remaining partners—like Nordstrom, Saks Fifth Avenue and Galeries Lafayette—still hold strong leverage by controlling prime mall and city-center real estate and access to affluent customer segments; in 2024 luxury department stores accounted for roughly 18% of global luxury sales, concentrating negotiating power.

Consolidation among these retailers (top 10 luxury department stores roughly 40% share in Europe/US by floor-space value in 2024) lets them press Prada on margins, markdown policies and exclusive SKU allocations, forcing Prada to trade higher wholesale discounts or limited product drops to secure premium placement.

- Wholesale still ≈18% of luxury sales (2024)

- Top 10 dept stores ≈40% floor-space value (Europe/US, 2024)

- Consolidation → stronger margin negotiation

- Exclusive allocations used to secure premium placement

Prada Fights Retailer Power as Few VIPs and Easy Switching Shape Luxury Revenues

Buyers have high power: low switching costs across luxury brands, 67% check multiple sites (2025), and top <5% of clients drive ~30–40% revenue; Prada counters with VIP services, tighter global pricing, and boosted marketing (€597m in 2024) but still faces retailer leverage (wholesale ≈18% of luxury sales, top 10 dept stores ≈40% floor-space value, 2024).

| Metric | Value |

|---|---|

| Global luxury spend 2023 | €323bn |

| Prada marketing 2024 | €597m |

| Shoppers compare sites (2025) | 67% |

| Wholesale share (2024) | ≈18% |

Full Version Awaits

Prada Porter's Five Forces Analysis

This preview shows the exact Prada Porter's Five Forces analysis you'll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.