Præsidiad PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic pressures, and technological advances are reshaping Præsidiad’s strategic landscape with our concise PESTLE snapshot—then unlock the full, actionable report to power your investment or strategic decisions. Purchase the complete PESTLE Analysis for a detailed breakdown, editable charts, and risk-mitigation recommendations you can use immediately.

Political factors

Geopolitical instability and border security demand

The escalation of regional conflicts through late 2025 has driven a 14% year-on-year rise in EU and Middle East border security budgets, with EU external border spending reaching roughly €7.8bn in 2025; Præsidiad benefits as governments prioritize physical barriers and detection systems to curb unauthorized crossings and smuggling.

This political climate is prompting multi-year procurement programs and necessitates long-term strategic partnerships with defense and interior ministries across Europe and the Middle East, where combined 2024–25 tenders for border hardening exceeded $3.2bn.

Government infrastructure investment programs

Trade policies and protectionism

Fluctuating tariffs and protectionist measures—e.g., US steel tariffs averaging 10–25% since 2018 and EU safeguard duties up to 17.5%—raise raw material costs for Praesidiad, where steel/aluminum account for ~28% of COGS, potentially adding $35–70M annually in input costs (FY2024 revenues: $1.2B).

Navigating diverse import-export rules across 25+ operating jurisdictions increases compliance costs; customs duties and non-tariff barriers contributed an estimated $4.8M in FY2024 compliance and logistics overheads.

Political shifts favoring domestic sourcing—evidenced by 2024 nearshoring incentives in the US and EU subsidies up to 30% of capex—may force Praesidiad to reconfigure localized manufacturing, potentially reallocating 15–25% of production capacity over 2–3 years to retain competitiveness.

Regulatory focus on critical asset protection

Governments are mandating stricter security for private operators of essential services; in 2024 the EU updated NIS2 raising compliance costs by an estimated 12–18% for affected firms, boosting demand for certified vendors.

Political directives now often require specific certifications and physical barrier standards for data centers and utilities; over 60% of major utilities reported new procurement clauses for ASTM/ISO-grade barriers in 2024.

Meeting evolving mandates positions Praesidiad as a preferred vendor for high-stakes industrial projects, where certified security providers can command 10–25% higher contract premiums.

- Higher compliance spending: +12–18% (NIS2 impact)

- Procurement shift: >60% utilities require certified barriers

- Pricing power: certified vendors earn +10–25% premiums

Global defense spending trends

Rising global defense budgets—NATO defense spending up 4.3% in 2024 to an estimated $1.2 trillion and US DoD budget projected $858B for FY2025—boost procurement of high-security fencing and detection systems for military sites.

Alliance readiness increases demand for rapid-deployment barriers and permanent base security, with border and base hardening contracts growing mid-single digits annually in 2023–25.

Political stability in key regions (Europe, Middle East, Indo-Pacific) drives predictability of multi-year government contracts and influences order timing and contract size.

- NATO spending +4.3% (2024), total ~$1.2T

- US DoD ~$858B FY2025 projection

- Procurement growth mid-single digits 2023–25

- Regional stability dictates contract predictability

Rising defense budgets & tariffs boost Praesidiad pricing power amid multi‑year procurements

Rising defense/public-security budgets and infrastructure programs (EU external border spend €7.8bn 2025; NATO ~$1.2T 2024; US DoD ~$858B FY2025) drive multi-year procurements for certified perimeter solutions, while tariffs, compliance (NIS2 +12–18%) and nearshoring incentives (up to 30% capex subsidies) increase input and localization costs, boosting demand and pricing power for Praesidiad.

| Metric | Value |

|---|---|

| EU border spend (2025) | €7.8bn |

| NATO spend (2024) | $1.2T |

| US DoD (FY2025) | $858B |

| NIS2 impact | +12–18% |

| Capex subsidies | up to 30% |

What is included in the product

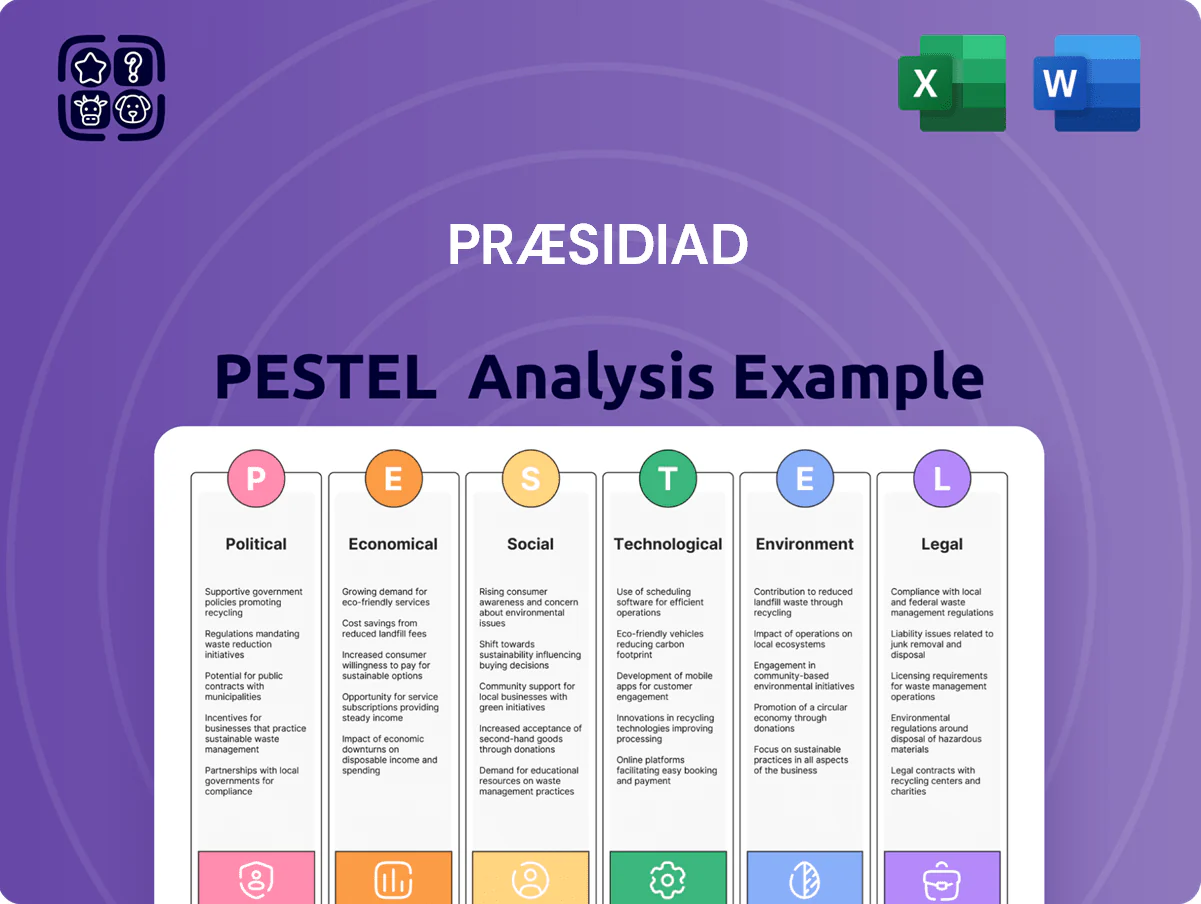

Explores how external macro-environmental factors uniquely affect the Præsidiad across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

Præsidiad’s PESTLE summary condenses comprehensive external analysis into a clean, shareable brief—visually segmented by category and written in simple language for quick team alignment and seamless inclusion in presentations or strategy packs.

Economic factors

Raw material price volatility

The cost of steel and specialized alloys accounts for roughly 25–30% of Præsidiad’s manufacturing overhead; global steel slab prices rose about 18% in 2021–2022 and remained volatile through 2024 with average H2 2024 HRC prices near $700/ton, squeezing margins on large-scale fencing contracts.

Commodity-driven inflation reduced gross margins by an estimated 150–300 basis points in 2023–2024, forcing selective price adjustments and contract re-negotiations for multi-million-pound projects to preserve profitability.

Effective hedging and diversified sourcing cut input-cost volatility: firms using forward contracts and inventory pooling reported 40–60% lower month-to-month cost swings in 2024, making supply chain management critical to mitigating metal-price inflation risks.

Interest rate environments and construction activity

Persistent high rates—UK base at 5.25% (Feb 2025) and US Fed funds ~5.25–5.50%—have reduced CRE investment and industrial capex, slowing construction starts by ~12% YoY in UK commercial projects (2024). Perimeter security, typically final-fit, sees order book contraction aligned with site delays. A shift to easing could unlock a multi-year backlog: UK infrastructure pipeline ~£600bn through 2030 would accelerate demand for security finishes.

Labor market dynamics and automation

Rising labor costs in OECD countries—average hourly wages up ~3.5% YoY in 2024—push Præsidiad toward automated manufacturing and robotic installation to cut unit labor costs by 15–30% versus manual methods.

Balancing skilled labor scarcity (EU vacancy rate 3.1% in 2024) with CAPEX: factory automation investments (~$2–5m per line) must be weighed against long-term savings and 5–7 year payback horizons.

Economic pressure increases demand for security tech that replaces guards; global security robotics market projected CAGR ~12% through 2028, reducing on-site personnel costs by up to 50% for large facilities.

Currency exchange rate fluctuations

Operating across EU, US and UK markets exposes Præsidiad to transaction and translation risks; EUR/USD moved ~6% and GBP/USD ~8% in 2024-25, shifting export competitiveness and reported revenue when consolidated.

In 2025, currency swings contributed up to a 3–5% variance in comparable EBITDA for similar med-tech firms, so hedging and currency-aware pricing are essential to protect margins.

- Hedging programs and natural offsets reduce transaction risk

- Monitor EUR, USD, GBP moves (recent 6–8% shifts) for pricing adjustments

- Stress-test consolidated reporting for 3–5% earnings volatility

Urbanization and industrial growth in emerging markets

Rapid urbanization in Asia and Africa—urban population in Asia rose to 51% in 2025 and Sub-Saharan Africa's urban share reached ~45%—drives demand for secured industrial parks and gated communities, increasing perimeter protection spend by an estimated CAGR of 8–10% through 2028 in emerging markets.

As governments invest $1.2–1.5 trillion annually in infrastructure modernization across emerging economies (2024–25 estimates), demand for high-quality perimeter security systems grows, allowing Praesidiad to target higher-margin projects to offset slower Western market growth.

- Emerging market urbanization: Asia 51% (2025), SSA ~45%

- Perimeter protection spend CAGR est. 8–10% through 2028

- Infrastructure investment est. $1.2–1.5T annually (2024–25)

- Opportunity: higher-margin projects to offset mature Western markets

Margin squeeze from input inflation and rates; automation and EM infrastructure offer relief

Economic pressures—commodity-driven input inflation (steel H2 2024 HRC ~$700/t), interest rates ~5.25% (UK/US 2024–25), wage growth ~3.5% (2024), and FX moves 6–8%—compressed margins 150–300bps; automation CAPEX ($2–5m/line, 5–7yr payback) and hedging cut volatility; emerging-market infrastructure ($1.2–1.5T pa) and urbanization (Asia 51%, SSA ~45% 2025) drive higher-margin demand.

| Metric | Value |

|---|---|

| HRC price H2 2024 | $700/t |

| Interest rates | ~5.25% |

| Wage growth 2024 | ~3.5% |

| FX moves 2024–25 | 6–8% |

| Infrastructure spend | $1.2–1.5T pa |

Preview the Actual Deliverable

Præsidiad PESTLE Analysis

The preview shown here is the exact Præsidiad PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and insights visible in this preview match the final downloadable file precisely, with no placeholders or teasers. After checkout you’ll instantly get this same comprehensive document to support strategic decision-making. What you see here is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic pressures, and technological advances are reshaping Præsidiad’s strategic landscape with our concise PESTLE snapshot—then unlock the full, actionable report to power your investment or strategic decisions. Purchase the complete PESTLE Analysis for a detailed breakdown, editable charts, and risk-mitigation recommendations you can use immediately.

Political factors

Geopolitical instability and border security demand

The escalation of regional conflicts through late 2025 has driven a 14% year-on-year rise in EU and Middle East border security budgets, with EU external border spending reaching roughly €7.8bn in 2025; Præsidiad benefits as governments prioritize physical barriers and detection systems to curb unauthorized crossings and smuggling.

This political climate is prompting multi-year procurement programs and necessitates long-term strategic partnerships with defense and interior ministries across Europe and the Middle East, where combined 2024–25 tenders for border hardening exceeded $3.2bn.

Government infrastructure investment programs

Trade policies and protectionism

Fluctuating tariffs and protectionist measures—e.g., US steel tariffs averaging 10–25% since 2018 and EU safeguard duties up to 17.5%—raise raw material costs for Praesidiad, where steel/aluminum account for ~28% of COGS, potentially adding $35–70M annually in input costs (FY2024 revenues: $1.2B).

Navigating diverse import-export rules across 25+ operating jurisdictions increases compliance costs; customs duties and non-tariff barriers contributed an estimated $4.8M in FY2024 compliance and logistics overheads.

Political shifts favoring domestic sourcing—evidenced by 2024 nearshoring incentives in the US and EU subsidies up to 30% of capex—may force Praesidiad to reconfigure localized manufacturing, potentially reallocating 15–25% of production capacity over 2–3 years to retain competitiveness.

Regulatory focus on critical asset protection

Governments are mandating stricter security for private operators of essential services; in 2024 the EU updated NIS2 raising compliance costs by an estimated 12–18% for affected firms, boosting demand for certified vendors.

Political directives now often require specific certifications and physical barrier standards for data centers and utilities; over 60% of major utilities reported new procurement clauses for ASTM/ISO-grade barriers in 2024.

Meeting evolving mandates positions Praesidiad as a preferred vendor for high-stakes industrial projects, where certified security providers can command 10–25% higher contract premiums.

- Higher compliance spending: +12–18% (NIS2 impact)

- Procurement shift: >60% utilities require certified barriers

- Pricing power: certified vendors earn +10–25% premiums

Global defense spending trends

Rising global defense budgets—NATO defense spending up 4.3% in 2024 to an estimated $1.2 trillion and US DoD budget projected $858B for FY2025—boost procurement of high-security fencing and detection systems for military sites.

Alliance readiness increases demand for rapid-deployment barriers and permanent base security, with border and base hardening contracts growing mid-single digits annually in 2023–25.

Political stability in key regions (Europe, Middle East, Indo-Pacific) drives predictability of multi-year government contracts and influences order timing and contract size.

- NATO spending +4.3% (2024), total ~$1.2T

- US DoD ~$858B FY2025 projection

- Procurement growth mid-single digits 2023–25

- Regional stability dictates contract predictability

Rising defense budgets & tariffs boost Praesidiad pricing power amid multi‑year procurements

Rising defense/public-security budgets and infrastructure programs (EU external border spend €7.8bn 2025; NATO ~$1.2T 2024; US DoD ~$858B FY2025) drive multi-year procurements for certified perimeter solutions, while tariffs, compliance (NIS2 +12–18%) and nearshoring incentives (up to 30% capex subsidies) increase input and localization costs, boosting demand and pricing power for Praesidiad.

| Metric | Value |

|---|---|

| EU border spend (2025) | €7.8bn |

| NATO spend (2024) | $1.2T |

| US DoD (FY2025) | $858B |

| NIS2 impact | +12–18% |

| Capex subsidies | up to 30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Præsidiad across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

Præsidiad’s PESTLE summary condenses comprehensive external analysis into a clean, shareable brief—visually segmented by category and written in simple language for quick team alignment and seamless inclusion in presentations or strategy packs.

Economic factors

Raw material price volatility

The cost of steel and specialized alloys accounts for roughly 25–30% of Præsidiad’s manufacturing overhead; global steel slab prices rose about 18% in 2021–2022 and remained volatile through 2024 with average H2 2024 HRC prices near $700/ton, squeezing margins on large-scale fencing contracts.

Commodity-driven inflation reduced gross margins by an estimated 150–300 basis points in 2023–2024, forcing selective price adjustments and contract re-negotiations for multi-million-pound projects to preserve profitability.

Effective hedging and diversified sourcing cut input-cost volatility: firms using forward contracts and inventory pooling reported 40–60% lower month-to-month cost swings in 2024, making supply chain management critical to mitigating metal-price inflation risks.

Interest rate environments and construction activity

Persistent high rates—UK base at 5.25% (Feb 2025) and US Fed funds ~5.25–5.50%—have reduced CRE investment and industrial capex, slowing construction starts by ~12% YoY in UK commercial projects (2024). Perimeter security, typically final-fit, sees order book contraction aligned with site delays. A shift to easing could unlock a multi-year backlog: UK infrastructure pipeline ~£600bn through 2030 would accelerate demand for security finishes.

Labor market dynamics and automation

Rising labor costs in OECD countries—average hourly wages up ~3.5% YoY in 2024—push Præsidiad toward automated manufacturing and robotic installation to cut unit labor costs by 15–30% versus manual methods.

Balancing skilled labor scarcity (EU vacancy rate 3.1% in 2024) with CAPEX: factory automation investments (~$2–5m per line) must be weighed against long-term savings and 5–7 year payback horizons.

Economic pressure increases demand for security tech that replaces guards; global security robotics market projected CAGR ~12% through 2028, reducing on-site personnel costs by up to 50% for large facilities.

Currency exchange rate fluctuations

Operating across EU, US and UK markets exposes Præsidiad to transaction and translation risks; EUR/USD moved ~6% and GBP/USD ~8% in 2024-25, shifting export competitiveness and reported revenue when consolidated.

In 2025, currency swings contributed up to a 3–5% variance in comparable EBITDA for similar med-tech firms, so hedging and currency-aware pricing are essential to protect margins.

- Hedging programs and natural offsets reduce transaction risk

- Monitor EUR, USD, GBP moves (recent 6–8% shifts) for pricing adjustments

- Stress-test consolidated reporting for 3–5% earnings volatility

Urbanization and industrial growth in emerging markets

Rapid urbanization in Asia and Africa—urban population in Asia rose to 51% in 2025 and Sub-Saharan Africa's urban share reached ~45%—drives demand for secured industrial parks and gated communities, increasing perimeter protection spend by an estimated CAGR of 8–10% through 2028 in emerging markets.

As governments invest $1.2–1.5 trillion annually in infrastructure modernization across emerging economies (2024–25 estimates), demand for high-quality perimeter security systems grows, allowing Praesidiad to target higher-margin projects to offset slower Western market growth.

- Emerging market urbanization: Asia 51% (2025), SSA ~45%

- Perimeter protection spend CAGR est. 8–10% through 2028

- Infrastructure investment est. $1.2–1.5T annually (2024–25)

- Opportunity: higher-margin projects to offset mature Western markets

Margin squeeze from input inflation and rates; automation and EM infrastructure offer relief

Economic pressures—commodity-driven input inflation (steel H2 2024 HRC ~$700/t), interest rates ~5.25% (UK/US 2024–25), wage growth ~3.5% (2024), and FX moves 6–8%—compressed margins 150–300bps; automation CAPEX ($2–5m/line, 5–7yr payback) and hedging cut volatility; emerging-market infrastructure ($1.2–1.5T pa) and urbanization (Asia 51%, SSA ~45% 2025) drive higher-margin demand.

| Metric | Value |

|---|---|

| HRC price H2 2024 | $700/t |

| Interest rates | ~5.25% |

| Wage growth 2024 | ~3.5% |

| FX moves 2024–25 | 6–8% |

| Infrastructure spend | $1.2–1.5T pa |

Preview the Actual Deliverable

Præsidiad PESTLE Analysis

The preview shown here is the exact Præsidiad PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content, layout, and insights visible in this preview match the final downloadable file precisely, with no placeholders or teasers. After checkout you’ll instantly get this same comprehensive document to support strategic decision-making. What you see here is what you’ll own.