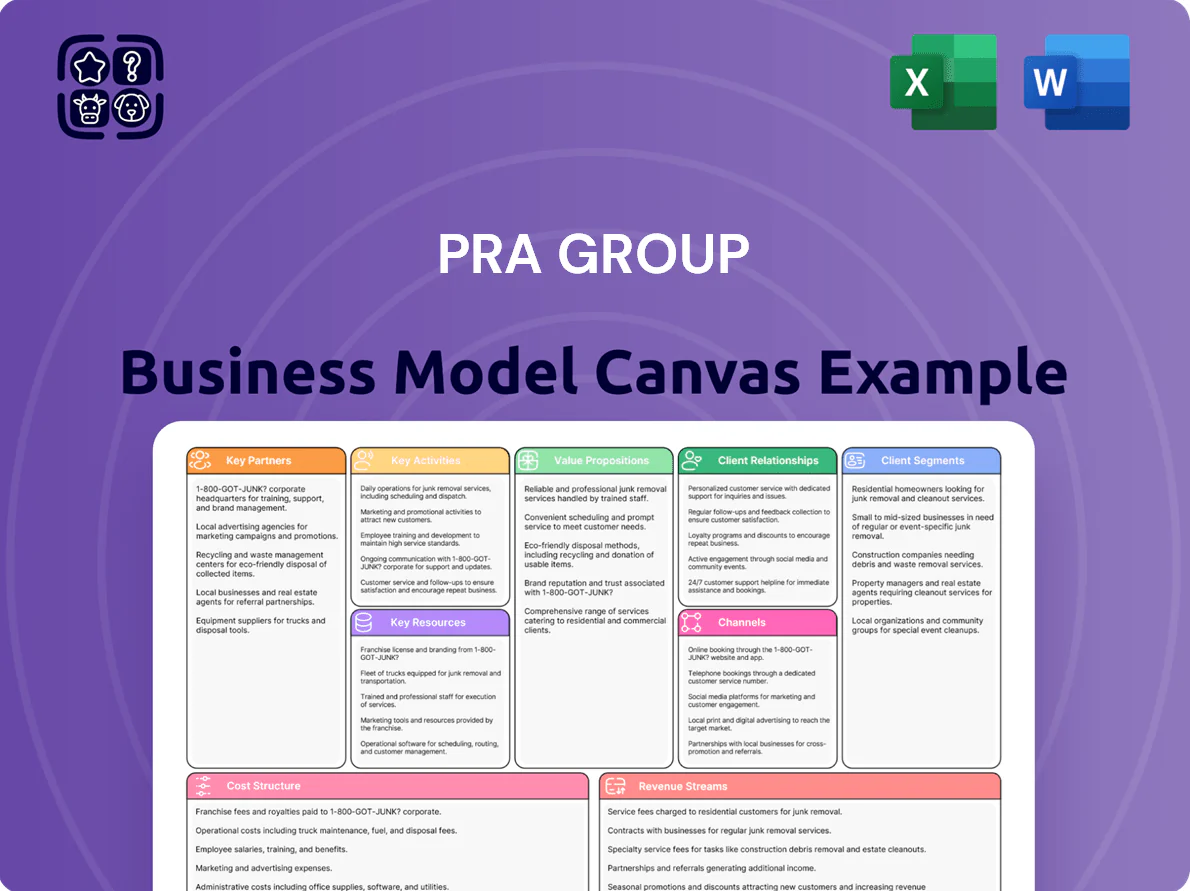

PRA Group Business Model Canvas

PRA Group BMC: How debt buying + analytics drive cash flow & margins

Explore PRA Group’s strategic core with our concise Business Model Canvas—see how debt purchasing, analytics-driven sourcing, and collection operations create consistent cash flow and margin advantages.

Purchase the full Canvas to get a section-by-section breakdown, actionable insights, and editable Word/Excel files ideal for investors, consultants, and planners.

Partnerships

Financial Institution Debt Sellers

Financial institution debt sellers include global banks, credit unions, and retail lenders that sell nonperforming loan portfolios to PRA Group to clean balance sheets; PRA bought $1.3 billion of receivables in 2024 across North America and Europe, ensuring volume.

Strong, ongoing relationships with originators secure a steady acquisition pipeline and are governed by rigorous due diligence and long-term reliability standards in the secondary debt market.

External Legal Counsel

PRA Group partners with a network of third-party law firms to handle litigation and legal recoveries when voluntary arrangements fail, providing local expertise across 20+ U.S. states and multiple international jurisdictions; in 2024 judicial recoveries represented roughly 18% of total collections, supporting $1.1 billion in recoveries company-wide. This outsourced model keeps fixed legal headcount low, scaling capacity for court filings and compliance with regional statutes while containing operating costs.

Credit Reporting Agencies

Partnerships with Equifax, Experian, and TransUnion give PRA Group access to consumer credit files and let it report payments or account resolutions—critical for valuing portfolios and driving recoveries; in 2024 PRA reported $1.06B revenue, where bureau data helped prioritize high-probability accounts. These agencies also supply skip-trace databases and behavioral scoring feeds that improve recovery rates and offer consumers a clear credit improvement incentive upon payment.

Technology and Data Analytics Providers

PRA Group partners with specialized software vendors and data providers to boost its proprietary scoring models and cut operational costs, using AI/ML tools that improved predictive accuracy by ~12% and reduced collector time per account by 9% in 2024.

By integrating external tech, PRA sustains an edge in portfolio valuation—helping lift recoveries per dollar purchased by ~7% and enabling dynamic resource allocation across ~$2.6B of purchased debt in 2024.

Regulatory and Compliance Bodies

Engaging financial regulators and industry associations keeps PRA Group aligned with shifting U.S. and U.K. consumer-protection rules, reducing the risk of fines—U.S. CFPB enforcement actions totaled $1.25 billion in 2023—while helping PRA shape fair-collection standards that matter to banks when selling portfolios.

These partnerships signal ethical practices, strengthening bids for large portfolios (PRA reported $1.6B purchased receivables in 2024) and lowering reputational and compliance costs through ongoing dialogue.

- Reduces fine risk (CFPB $1.25B, 2023)

- Supports $1.6B portfolio purchases (PRA, 2024)

- Enhances bids vs peers via ethical standards

- Ongoing dialogue cuts reputational costs

PRA Group: $1.6B NPLs, AI +12% → +7% recoveries, $1.06B revenue, 18% judicial wins

PRA Group secures nonperforming loan supply from banks and lenders ( $1.6B bought, 2024), uses bureau data (supports $1.06B revenue, 2024) and AI vendors (+12% model accuracy) to boost recoveries (~+7% per dollar) while outsourcing legal work (judicial recoveries ≈18%, $1.1B, 2024) to scale cost-effectively.

| Metric | 2024 |

|---|---|

| Purchased receivables | $1.6B |

| Revenue supported | $1.06B |

| Judicial recoveries | 18% ($1.1B) |

| AI accuracy lift | +12% |

| Recovery uplift | +7% |

What is included in the product

A concise Business Model Canvas for PRA Group detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and metrics, aligned to real-world debt purchasing and recovery operations and designed for presentations, investment discussions, and strategic analysis with embedded competitive advantages and SWOT insights.

High-level view of PRA Group’s business model with editable cells to quickly map revenue streams, customer segments, and recovery operations—ideal for boardrooms, team collaboration, and fast executive summaries.

Activities

Portfolio Valuation and Acquisition

PRA Group uses advanced statistical and machine-learning models to price nonperforming loan (NPL) portfolios, combining vintage loss curves, recovery timelines, and macro variables like U.S. unemployment (3.7% Dec 2025) to forecast IRR for each deal.

Investment teams target acquisition prices that secure mid-teens net returns; in 2024 PRA purchased $1.4B of receivables, yielding portfolio recovery rates and margin assumptions that guide bid discipline.

Data-Driven Debt Collection

PRA Group uses proprietary algorithms to segment accounts and score repayment likelihood, prioritizing roughly 25–35% of accounts that drive ~70% of recoveries; outreach is then tailored by channel and cadence to each consumer. By 2025 the firm reported call-center efficiency gains of ~18% and digital recovery growth of 22%, boosting portfolio yield while reducing cost-per-dollar-collected.

Legal Recovery Management

When voluntary collections fail, PRA Group runs legal recovery via in-house counsel and ~2,000 external firms, filing suits, securing judgments, and enforcing garnishments or liens under state law; this process recovered about $650M of net collections in 2024, or roughly 18% of total net collections, making legal recovery essential for non-responsive portfolios.

Regulatory Compliance and Auditing

Maintaining a robust compliance framework is continuous: PRA Group monitors consumer interactions and processes for FDCPA (Fair Debt Collection Practices Act) adherence and other laws, runs monthly internal audits, and delivers quarterly training to staff and vendors to reduce regulatory violations.

This protects PRA’s license, limits fines (debt-collector fines averaged $45m industry-wide in 2024) and preserves relationships with debt sellers and regulators.

- Monthly audits

- Quarterly trainings

- FDCPA monitoring

- Vendor oversight

- Reduces fines, protects license

Capital Allocation and Treasury Management

PRA Group manages capital to fund large-scale NPL (non-performing loan) purchases while keeping liquidity; as of FY 2024 it held $1.1 billion of available liquidity and $3.2 billion total debt, using revolvers and bond issuance to time buys when yields widen.

Strategic treasury ensures flexibility for high-volume windows—PRA targets cash coverage for 6–12 months of purchases and paces acquisitions to match credit facility covenants and market spreads.

- Available liquidity: $1.1B (FY2024)

- Total debt: $3.2B (FY2024)

- Cash coverage target: 6–12 months

- Uses revolver, bonds, timed purchases

PRA Group: ML‑priced NPLs, $1.4B buys, mid‑teens IRR, $650M legal recoveries, $1.1B liquidity

PRA Group prices NPLs with machine learning and macro-driven vintage models, targeting mid-teens net IRR; 2024 purchases $1.4B, recovery-driven bid discipline. Operations: prioritize 25–35% accounts for ~70% recoveries, 2024 legal recoveries $650M (18% net), compliance monthly audits/quarterly training. Liquidity: $1.1B available, $3.2B debt, 6–12 months cash cover.

| Metric | 2024 |

|---|---|

| Purchases | $1.4B |

| Legal recoveries | $650M |

| Available liquidity | $1.1B |

| Total debt | $3.2B |

What You See Is What You Get

Business Model Canvas

The preview shown is the actual PRA Group Business Model Canvas—you’re not looking at a mockup or sample; it’s a direct snapshot of the full deliverable.

When you purchase, you’ll receive this exact document—complete, editable, and formatted the same way—ready for download in Word and Excel for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

PRA Group BMC: How debt buying + analytics drive cash flow & margins

Explore PRA Group’s strategic core with our concise Business Model Canvas—see how debt purchasing, analytics-driven sourcing, and collection operations create consistent cash flow and margin advantages.

Purchase the full Canvas to get a section-by-section breakdown, actionable insights, and editable Word/Excel files ideal for investors, consultants, and planners.

Partnerships

Financial Institution Debt Sellers

Financial institution debt sellers include global banks, credit unions, and retail lenders that sell nonperforming loan portfolios to PRA Group to clean balance sheets; PRA bought $1.3 billion of receivables in 2024 across North America and Europe, ensuring volume.

Strong, ongoing relationships with originators secure a steady acquisition pipeline and are governed by rigorous due diligence and long-term reliability standards in the secondary debt market.

External Legal Counsel

PRA Group partners with a network of third-party law firms to handle litigation and legal recoveries when voluntary arrangements fail, providing local expertise across 20+ U.S. states and multiple international jurisdictions; in 2024 judicial recoveries represented roughly 18% of total collections, supporting $1.1 billion in recoveries company-wide. This outsourced model keeps fixed legal headcount low, scaling capacity for court filings and compliance with regional statutes while containing operating costs.

Credit Reporting Agencies

Partnerships with Equifax, Experian, and TransUnion give PRA Group access to consumer credit files and let it report payments or account resolutions—critical for valuing portfolios and driving recoveries; in 2024 PRA reported $1.06B revenue, where bureau data helped prioritize high-probability accounts. These agencies also supply skip-trace databases and behavioral scoring feeds that improve recovery rates and offer consumers a clear credit improvement incentive upon payment.

Technology and Data Analytics Providers

PRA Group partners with specialized software vendors and data providers to boost its proprietary scoring models and cut operational costs, using AI/ML tools that improved predictive accuracy by ~12% and reduced collector time per account by 9% in 2024.

By integrating external tech, PRA sustains an edge in portfolio valuation—helping lift recoveries per dollar purchased by ~7% and enabling dynamic resource allocation across ~$2.6B of purchased debt in 2024.

Regulatory and Compliance Bodies

Engaging financial regulators and industry associations keeps PRA Group aligned with shifting U.S. and U.K. consumer-protection rules, reducing the risk of fines—U.S. CFPB enforcement actions totaled $1.25 billion in 2023—while helping PRA shape fair-collection standards that matter to banks when selling portfolios.

These partnerships signal ethical practices, strengthening bids for large portfolios (PRA reported $1.6B purchased receivables in 2024) and lowering reputational and compliance costs through ongoing dialogue.

- Reduces fine risk (CFPB $1.25B, 2023)

- Supports $1.6B portfolio purchases (PRA, 2024)

- Enhances bids vs peers via ethical standards

- Ongoing dialogue cuts reputational costs

PRA Group: $1.6B NPLs, AI +12% → +7% recoveries, $1.06B revenue, 18% judicial wins

PRA Group secures nonperforming loan supply from banks and lenders ( $1.6B bought, 2024), uses bureau data (supports $1.06B revenue, 2024) and AI vendors (+12% model accuracy) to boost recoveries (~+7% per dollar) while outsourcing legal work (judicial recoveries ≈18%, $1.1B, 2024) to scale cost-effectively.

| Metric | 2024 |

|---|---|

| Purchased receivables | $1.6B |

| Revenue supported | $1.06B |

| Judicial recoveries | 18% ($1.1B) |

| AI accuracy lift | +12% |

| Recovery uplift | +7% |

What is included in the product

A concise Business Model Canvas for PRA Group detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and metrics, aligned to real-world debt purchasing and recovery operations and designed for presentations, investment discussions, and strategic analysis with embedded competitive advantages and SWOT insights.

High-level view of PRA Group’s business model with editable cells to quickly map revenue streams, customer segments, and recovery operations—ideal for boardrooms, team collaboration, and fast executive summaries.

Activities

Portfolio Valuation and Acquisition

PRA Group uses advanced statistical and machine-learning models to price nonperforming loan (NPL) portfolios, combining vintage loss curves, recovery timelines, and macro variables like U.S. unemployment (3.7% Dec 2025) to forecast IRR for each deal.

Investment teams target acquisition prices that secure mid-teens net returns; in 2024 PRA purchased $1.4B of receivables, yielding portfolio recovery rates and margin assumptions that guide bid discipline.

Data-Driven Debt Collection

PRA Group uses proprietary algorithms to segment accounts and score repayment likelihood, prioritizing roughly 25–35% of accounts that drive ~70% of recoveries; outreach is then tailored by channel and cadence to each consumer. By 2025 the firm reported call-center efficiency gains of ~18% and digital recovery growth of 22%, boosting portfolio yield while reducing cost-per-dollar-collected.

Legal Recovery Management

When voluntary collections fail, PRA Group runs legal recovery via in-house counsel and ~2,000 external firms, filing suits, securing judgments, and enforcing garnishments or liens under state law; this process recovered about $650M of net collections in 2024, or roughly 18% of total net collections, making legal recovery essential for non-responsive portfolios.

Regulatory Compliance and Auditing

Maintaining a robust compliance framework is continuous: PRA Group monitors consumer interactions and processes for FDCPA (Fair Debt Collection Practices Act) adherence and other laws, runs monthly internal audits, and delivers quarterly training to staff and vendors to reduce regulatory violations.

This protects PRA’s license, limits fines (debt-collector fines averaged $45m industry-wide in 2024) and preserves relationships with debt sellers and regulators.

- Monthly audits

- Quarterly trainings

- FDCPA monitoring

- Vendor oversight

- Reduces fines, protects license

Capital Allocation and Treasury Management

PRA Group manages capital to fund large-scale NPL (non-performing loan) purchases while keeping liquidity; as of FY 2024 it held $1.1 billion of available liquidity and $3.2 billion total debt, using revolvers and bond issuance to time buys when yields widen.

Strategic treasury ensures flexibility for high-volume windows—PRA targets cash coverage for 6–12 months of purchases and paces acquisitions to match credit facility covenants and market spreads.

- Available liquidity: $1.1B (FY2024)

- Total debt: $3.2B (FY2024)

- Cash coverage target: 6–12 months

- Uses revolver, bonds, timed purchases

PRA Group: ML‑priced NPLs, $1.4B buys, mid‑teens IRR, $650M legal recoveries, $1.1B liquidity

PRA Group prices NPLs with machine learning and macro-driven vintage models, targeting mid-teens net IRR; 2024 purchases $1.4B, recovery-driven bid discipline. Operations: prioritize 25–35% accounts for ~70% recoveries, 2024 legal recoveries $650M (18% net), compliance monthly audits/quarterly training. Liquidity: $1.1B available, $3.2B debt, 6–12 months cash cover.

| Metric | 2024 |

|---|---|

| Purchases | $1.4B |

| Legal recoveries | $650M |

| Available liquidity | $1.1B |

| Total debt | $3.2B |

What You See Is What You Get

Business Model Canvas

The preview shown is the actual PRA Group Business Model Canvas—you’re not looking at a mockup or sample; it’s a direct snapshot of the full deliverable.

When you purchase, you’ll receive this exact document—complete, editable, and formatted the same way—ready for download in Word and Excel for immediate use.