PRA Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

PRA Group faces intense buyer scrutiny and regulatory oversight alongside moderate supplier leverage and growing substitute risks from fintech solutions, shaping a challenging competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PRA Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Financial Institutions

The supply of nonperforming loans (NPLs) is concentrated: as of 2024 roughly 60–70% of US consumer NPL sales came from a handful of banks and card issuers (JPMorgan Chase, Bank of America, Citigroup, Discover), giving these sellers strong leverage over price and portfolio quality.

These institutions control both volume and vintage: they decide batch size, charge-offs, and documentation quality, which directly affects yield and recovery timelines for PRA Group.

PRA Group must sustain top-tier institutional ties and compliance credentials; losing preferred-buyer status could cut available supply by an estimated 30–50% for certain asset classes.

Regulatory Pressure on Debt Originators

Banks face rising regulatory pressure to offload nonperforming loans—UK PRA and US regulators pushed higher CET1 targets in 2024, driving a 12–18% uptick in NPL sales volume; that favors buyers like PRA Group by increasing supply.

Still, sellers exert power by demanding strict compliance, AML and servicer standards and reputational safeguards, narrowing eligible buyers and raising onboarding costs by an estimated $0.5–1.2M per portfolio.

Pricing Control through Auction Processes

Most debt portfolios sell via competitive bidding or bilateral deals where sellers set initial terms; in 2024 about 68% of US unsecured consumer debt portfolios used auctions, per industry reports. Suppliers can time sales or pull assets if bids fall below internal recovery thresholds, shifting supply and causing quarterly price swings up to 12%. That market-entry control forces PRA Group to update pricing models frequently—often weekly—and stress-test bids against recovery curves and discount rates.

Data Quality and Information Asymmetry

Data quality and information asymmetry materially affect PRA Group’s purchase valuations because debt buyers price portfolios based on documentation and payment histories; industry studies show portfolios with >95% complete file documentation sell at premiums up to 15% (2024 market data).

Financial institutions wield bargaining power by restricting access to due-diligence data rooms, and limited transparency raises estimated loss rates and required yields for PRA Group.

When files are incomplete, PRA Group often applies haircut adjustments—commonly 10–30%—to account for higher recovery uncertainty, making supplier reliability a direct driver of deal price.

- Complete docs >95% → price premium ≈15% (2024)

- Incomplete files → typical haircuts 10–30%

- Data-room opacity increases required yields and loss estimates

Switching Costs for Financial Institutions

Banks face high reputational and operational risks when switching debt buyers; integrating data feeds and compliance reporting creates stickiness—US banks reported 28% higher reconciliation costs when changing vendors in 2024.

Large buyers like PRA Group (2024 revenue $1.2bn) are selectable, but failure on compliance lets banks move quickly to competitors, so suppliers retain leverage despite switching frictions.

- High reputational risk

- Data/integration stickiness

- 28% higher costs switching (2024)

- PRA revenue $1.2bn (2024)

- Compliance failures shift power

Top banks dominate US NPLs (60–70%); data quality drives ±15% pricing, auctions 68%

Supplier power is high: major banks (JPMorgan, BofA, Citi, Discover) supplied ~60–70% of US consumer NPLs in 2024, letting them set terms, batch quality, and timing; loss of preferred-buyer status can cut supply 30–50% for some classes. Data completeness (>95%) yields ~15% premium; incomplete files trigger 10–30% haircuts and raise onboarding costs $0.5–1.2M. PRA Group revenue 2024 $1.2bn; auctions ~68% of deals; price swings up to 12% Q/Q.

| Metric | 2024 Value |

|---|---|

| Share from top banks | 60–70% |

| Auction usage | 68% |

| Complete-doc premium | ≈15% |

| Haircuts (incomplete) | 10–30% |

| Onboarding cost | $0.5–1.2M |

| Q/Q price swing | up to 12% |

| PRA Group revenue | $1.2bn |

What is included in the product

Tailored Porter's Five Forces analysis for PRA Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic implications to safeguard market share and profitability.

PRA Group Porter's Five Forces condensed into a single, deck-ready sheet—map competitive intensity across debt buying, collection, and regulatory exposure for faster strategic decisions.

Customers Bargaining Power

Regulatory Empowerment of Debtors

Regulatory protections like the US Fair Debt Collection Practices Act and EU rules let individual debtors dispute debts and limit contact methods, shifting power to consumers; CFPB reported 200,000+ collection complaints in 2024 and a 14% rise in dispute filings year-over-year, forcing PRA Group to invest in compliance and reducing aggressive collection leverage.

Financial Capacity and Economic Sensitivity

Customer ability to pay ties directly to macro factors: US unemployment fell to 3.7% in Dec 2025 and CPI inflation slowed to 3.1% year-over-year in 2025, so in stronger conditions PRA Group (PRA) gains leverage to push for higher recoveries and fewer discounts.

When unemployment or inflation rises, disposable income drops and customer bargaining power increases; during 2020–2022 downturns PRA accepted deeper settlements as recoveries fell by double digits.

Availability of Debt Counseling and Settlement Services

The rise of third-party debt settlement firms and non-profit credit counselors gives consumers stronger negotiation clout; as of 2024 about 2.1 million U.S. households used such services, and median settlements often cut principal by 30–50%. PRA Group must outcompete these intermediaries to sign debtors directly before consolidation occurs, since intermediaries both reduce recoverable balances and lengthen resolution timelines.

Legal Protections and Bankruptcy Options

Consumers can discharge qualifying unsecured debts through Chapter 7 or reorganize under Chapter 13, causing PRA Group to potentially realize a total loss; U.S. consumer bankruptcy filings were ~390,000 in 2024, a 6% rise from 2023 per Epiq data.

The bankruptcy threat strengthens debtors' leverage in settlements, pushing PRA to offer discounts to secure partial recovery rather than face zero recovery in court.

PRA must calibrate collections—intense pressure raises bankruptcy filing risk, while measured offers can preserve recoveries and reduce legal write-offs.

- ~390,000 U.S. filings in 2024 (Epiq)

- Chapter 7 = potential total loss

- Settlements often preferable to litigation

- Balance pressure to avoid forced bankruptcy

Digital Transparency and Social Media

Digital transparency empowers PRA Group debtors: 78% of consumers use social media or forums for financial advice (Pew Research, 2023), and common shared settlement rates cluster around 20–60% of purchased principal, cutting collectors’ informational edge.

Online reviews and Reddit/Twitter threads amplify negotiation tactics and sample settlement letters, increasing debtor confidence and lowering average recovery per account for buyers like PRA.

- 78% consult social media for finance (Pew, 2023)

- Typical shared settlement range: 20–60% of principal

- Transparency narrows collectors’ information advantage

Consumers’ rising power forces deeper settlements, higher compliance for PRA

Customers wield moderate-to-high bargaining power vs PRA due to strong regulation (FDCPA/CFPB complaints 200k+ in 2024), rising bankruptcy filings (~390,000 US filings in 2024), growth of settlement counselors (~2.1M households using services in 2024), and digital transparency (78% seek finance advice online), forcing deeper settlements (typical 20–60% of principal) and higher compliance costs.

| Metric | 2024/25 Value |

|---|---|

| CFPB collection complaints | 200,000+ |

| US bankruptcy filings (Epiq) | ~390,000 (2024) |

| Households using settlement services | ~2.1M (2024) |

| Consumers using social media for finance | 78% (Pew, 2023) |

| Typical settlement range | 20–60% of principal |

What You See Is What You Get

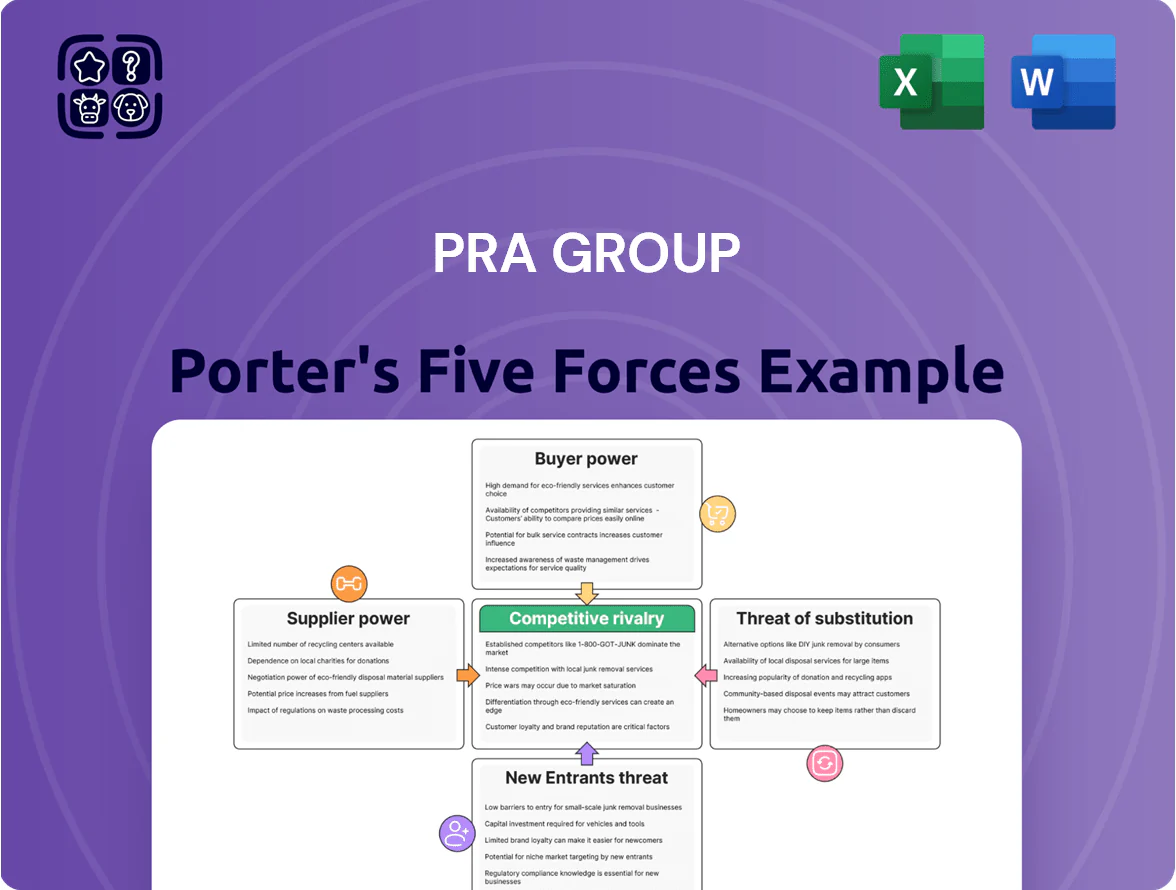

PRA Group Porter's Five Forces Analysis

This preview shows the exact PRA Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

PRA Group faces intense buyer scrutiny and regulatory oversight alongside moderate supplier leverage and growing substitute risks from fintech solutions, shaping a challenging competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PRA Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Financial Institutions

The supply of nonperforming loans (NPLs) is concentrated: as of 2024 roughly 60–70% of US consumer NPL sales came from a handful of banks and card issuers (JPMorgan Chase, Bank of America, Citigroup, Discover), giving these sellers strong leverage over price and portfolio quality.

These institutions control both volume and vintage: they decide batch size, charge-offs, and documentation quality, which directly affects yield and recovery timelines for PRA Group.

PRA Group must sustain top-tier institutional ties and compliance credentials; losing preferred-buyer status could cut available supply by an estimated 30–50% for certain asset classes.

Regulatory Pressure on Debt Originators

Banks face rising regulatory pressure to offload nonperforming loans—UK PRA and US regulators pushed higher CET1 targets in 2024, driving a 12–18% uptick in NPL sales volume; that favors buyers like PRA Group by increasing supply.

Still, sellers exert power by demanding strict compliance, AML and servicer standards and reputational safeguards, narrowing eligible buyers and raising onboarding costs by an estimated $0.5–1.2M per portfolio.

Pricing Control through Auction Processes

Most debt portfolios sell via competitive bidding or bilateral deals where sellers set initial terms; in 2024 about 68% of US unsecured consumer debt portfolios used auctions, per industry reports. Suppliers can time sales or pull assets if bids fall below internal recovery thresholds, shifting supply and causing quarterly price swings up to 12%. That market-entry control forces PRA Group to update pricing models frequently—often weekly—and stress-test bids against recovery curves and discount rates.

Data Quality and Information Asymmetry

Data quality and information asymmetry materially affect PRA Group’s purchase valuations because debt buyers price portfolios based on documentation and payment histories; industry studies show portfolios with >95% complete file documentation sell at premiums up to 15% (2024 market data).

Financial institutions wield bargaining power by restricting access to due-diligence data rooms, and limited transparency raises estimated loss rates and required yields for PRA Group.

When files are incomplete, PRA Group often applies haircut adjustments—commonly 10–30%—to account for higher recovery uncertainty, making supplier reliability a direct driver of deal price.

- Complete docs >95% → price premium ≈15% (2024)

- Incomplete files → typical haircuts 10–30%

- Data-room opacity increases required yields and loss estimates

Switching Costs for Financial Institutions

Banks face high reputational and operational risks when switching debt buyers; integrating data feeds and compliance reporting creates stickiness—US banks reported 28% higher reconciliation costs when changing vendors in 2024.

Large buyers like PRA Group (2024 revenue $1.2bn) are selectable, but failure on compliance lets banks move quickly to competitors, so suppliers retain leverage despite switching frictions.

- High reputational risk

- Data/integration stickiness

- 28% higher costs switching (2024)

- PRA revenue $1.2bn (2024)

- Compliance failures shift power

Top banks dominate US NPLs (60–70%); data quality drives ±15% pricing, auctions 68%

Supplier power is high: major banks (JPMorgan, BofA, Citi, Discover) supplied ~60–70% of US consumer NPLs in 2024, letting them set terms, batch quality, and timing; loss of preferred-buyer status can cut supply 30–50% for some classes. Data completeness (>95%) yields ~15% premium; incomplete files trigger 10–30% haircuts and raise onboarding costs $0.5–1.2M. PRA Group revenue 2024 $1.2bn; auctions ~68% of deals; price swings up to 12% Q/Q.

| Metric | 2024 Value |

|---|---|

| Share from top banks | 60–70% |

| Auction usage | 68% |

| Complete-doc premium | ≈15% |

| Haircuts (incomplete) | 10–30% |

| Onboarding cost | $0.5–1.2M |

| Q/Q price swing | up to 12% |

| PRA Group revenue | $1.2bn |

What is included in the product

Tailored Porter's Five Forces analysis for PRA Group, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic implications to safeguard market share and profitability.

PRA Group Porter's Five Forces condensed into a single, deck-ready sheet—map competitive intensity across debt buying, collection, and regulatory exposure for faster strategic decisions.

Customers Bargaining Power

Regulatory Empowerment of Debtors

Regulatory protections like the US Fair Debt Collection Practices Act and EU rules let individual debtors dispute debts and limit contact methods, shifting power to consumers; CFPB reported 200,000+ collection complaints in 2024 and a 14% rise in dispute filings year-over-year, forcing PRA Group to invest in compliance and reducing aggressive collection leverage.

Financial Capacity and Economic Sensitivity

Customer ability to pay ties directly to macro factors: US unemployment fell to 3.7% in Dec 2025 and CPI inflation slowed to 3.1% year-over-year in 2025, so in stronger conditions PRA Group (PRA) gains leverage to push for higher recoveries and fewer discounts.

When unemployment or inflation rises, disposable income drops and customer bargaining power increases; during 2020–2022 downturns PRA accepted deeper settlements as recoveries fell by double digits.

Availability of Debt Counseling and Settlement Services

The rise of third-party debt settlement firms and non-profit credit counselors gives consumers stronger negotiation clout; as of 2024 about 2.1 million U.S. households used such services, and median settlements often cut principal by 30–50%. PRA Group must outcompete these intermediaries to sign debtors directly before consolidation occurs, since intermediaries both reduce recoverable balances and lengthen resolution timelines.

Legal Protections and Bankruptcy Options

Consumers can discharge qualifying unsecured debts through Chapter 7 or reorganize under Chapter 13, causing PRA Group to potentially realize a total loss; U.S. consumer bankruptcy filings were ~390,000 in 2024, a 6% rise from 2023 per Epiq data.

The bankruptcy threat strengthens debtors' leverage in settlements, pushing PRA to offer discounts to secure partial recovery rather than face zero recovery in court.

PRA must calibrate collections—intense pressure raises bankruptcy filing risk, while measured offers can preserve recoveries and reduce legal write-offs.

- ~390,000 U.S. filings in 2024 (Epiq)

- Chapter 7 = potential total loss

- Settlements often preferable to litigation

- Balance pressure to avoid forced bankruptcy

Digital Transparency and Social Media

Digital transparency empowers PRA Group debtors: 78% of consumers use social media or forums for financial advice (Pew Research, 2023), and common shared settlement rates cluster around 20–60% of purchased principal, cutting collectors’ informational edge.

Online reviews and Reddit/Twitter threads amplify negotiation tactics and sample settlement letters, increasing debtor confidence and lowering average recovery per account for buyers like PRA.

- 78% consult social media for finance (Pew, 2023)

- Typical shared settlement range: 20–60% of principal

- Transparency narrows collectors’ information advantage

Consumers’ rising power forces deeper settlements, higher compliance for PRA

Customers wield moderate-to-high bargaining power vs PRA due to strong regulation (FDCPA/CFPB complaints 200k+ in 2024), rising bankruptcy filings (~390,000 US filings in 2024), growth of settlement counselors (~2.1M households using services in 2024), and digital transparency (78% seek finance advice online), forcing deeper settlements (typical 20–60% of principal) and higher compliance costs.

| Metric | 2024/25 Value |

|---|---|

| CFPB collection complaints | 200,000+ |

| US bankruptcy filings (Epiq) | ~390,000 (2024) |

| Households using settlement services | ~2.1M (2024) |

| Consumers using social media for finance | 78% (Pew, 2023) |

| Typical settlement range | 20–60% of principal |

What You See Is What You Get

PRA Group Porter's Five Forces Analysis

This preview shows the exact PRA Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for download.