Premier Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

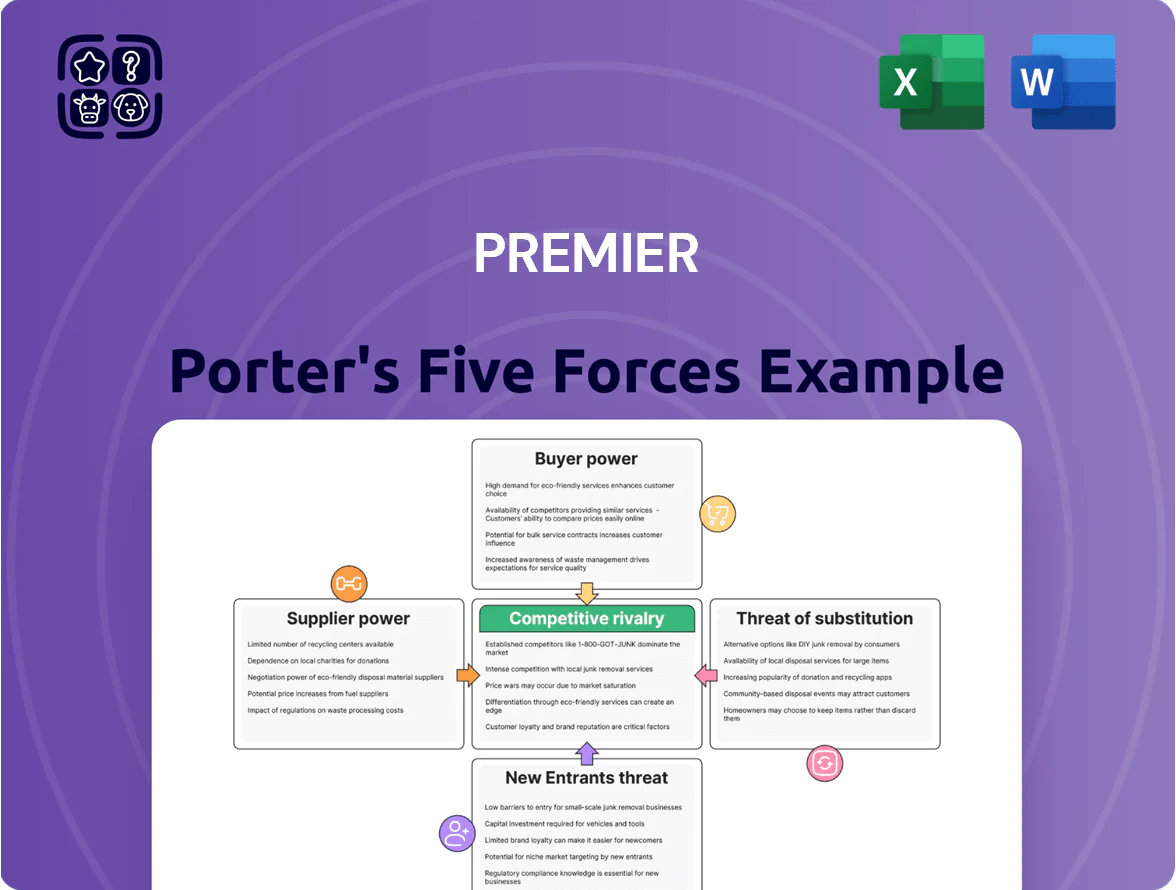

Premier faces a mix of concentrated buyer power, moderate supplier leverage, and evolving substitute threats that shape pricing and margins; competitive rivalry is intense but tempered by regulatory barriers and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Premier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Premier Group depends on wheat and maize for ~68% of input costs, exposing it to global price swings—wheat rose 28% YoY in 2024 and maize 22%—so high-quality grain suppliers can push prices or restrict supply. Premier uses strategic sourcing across 6 countries and hedged $120m of grain exposure in 2024, cutting volatility but not eliminating risk. Currency devaluation in key sourcing markets (e.g., 2023–24 FX drops of 12–18%) still amplifies import costs and supplier leverage.

Energy and Utility Costs

Suppliers of electricity and water in South Africa, mainly Eskom (state utility) and Rand Water, hold high bargaining power due to near-monopolies and limited large-scale alternatives, forcing Premier to accept price increases; Eskom raised average tariffs ~18% in 2023 and proposed further hikes into 2025.

Rising tariffs and chronic load shedding raise Premier’s raw-material and processing costs; load shedding caused estimated R175 billion GDP loss in 2023, increasing operational disruptions and maintenance spend.

To keep production steady, Premier must absorb costs or invest in self-generation: a 10 MW diesel/gas backup plant costs roughly ZAR 200–300 million upfront plus ZAR 100–200 million annual fuel/O&M, squeezing margins.

Concentration of Input Providers

Concentration of input providers is high: roughly 60–70% of bulk produce for large buyers comes from fewer than 200 commercial farms and cooperatives in key regions, letting suppliers set stricter pricing and contract terms. Premier’s $4.2bn annual procurement gives it leverage, but dependence on specific geographies (e.g., Central Valley, Brazil Mato Grosso) raises supply disruption risk from weather, labor, or export policy shocks.

Logistics and Fuel Providers

Logistics and fuel suppliers wield high bargaining power since Southern Africa's bulk food distribution depends on road and rail and on oil, which averaged $82/barrel in 2025, so sudden price swings raise transport costs fast.

Limited cost-effective alternatives and weak regional infrastructure (World Bank 2024: 46% of key corridors in poor condition) mean suppliers can pass costs to food processors immediately, lifting landed raw-material costs and retail prices.

- Few bulk alternatives: heavy road/rail reliance

- Oil price sensitivity: $82/barrel (2025 avg)

- Infrastructure strain: 46% corridors poor (World Bank 2024)

- Direct pass-through: transport cost → landed cost → retail price

Impact of Climate Change on Yields

Suppliers face rising pressure from unpredictable weather and droughts that cut crop yields; FAO reported a 5% global cereal production drop in 2023 linked to extreme weather, raising variability and lowering quality.

Scarcity boosts supplier bargaining power: during poor harvests suppliers can demand price premia — global grain prices rose ~20% in 2022–23, squeezing buyers.

Premier must build long-term, resilient supplier ties and invest in contract pricing, storage, and climate-resilient sourcing to stay prioritized when supply tightens.

- Weather-driven yield volatility up ~5% (FAO 2023)

- Grain prices +20% in 2022–23

- Strategy: long-term contracts, storage, diversified sourcing

Suppliers’ pricing power surges as grains, utilities and logistics drive rapid cost pass-through

Suppliers hold high bargaining power: wheat/maize ~68% input, global wheat +28% YoY 2024, maize +22%; Eskom/Rand Water near-monopolies (Eskom tariffs +18% in 2023); Premier hedged $120m grain exposure in 2024 but remains FX-vulnerable (2023–24 FX drops 12–18%); transport reliant on oil ~$82/bbl (2025) and 46% corridors poor (World Bank 2024), so suppliers can pass costs quickly.

| Metric | Value |

|---|---|

| Wheat/maize share | ~68% |

| Wheat YoY (2024) | +28% |

| Maize YoY (2024) | +22% |

| Grain hedged (2024) | $120m |

| Eskom tariff rise (2023) | ~+18% |

| Oil avg (2025) | $82/bbl |

| Corridors poor (World Bank 2024) | 46% |

What is included in the product

Tailored Five Forces analysis for Premier that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

Condense industry competitive dynamics into a single actionable sheet—helping teams quickly spot threats and opportunities and make confident strategic choices.

Customers Bargaining Power

Concentration of Retail Giants

Price Sensitivity of Low-Income Consumers

A significant share of Premier’s consumers are low-income and price-sensitive; 2024 household data shows 42% of spend in target regions goes to staples like bread and maize, making these goods highly elastic. Even a 5% price rise historically shifts buyers to cheaper brands or wholesaler bulk purchases, cutting retail volumes by up to 12% in quarterly sales. That limits Premier’s scope to pass on inflation without sizable volume loss.

Growth of Private Label Brands

Low Switching Costs for Households

Consumers face almost zero switching costs when choosing bread, flour, or maize meal, so price and shelf availability beat brand loyalty; NielsenIQ data (2024) shows 62% of South African shoppers pick on price/promotions at purchase.

This frictionless choice forces Premier to keep products widely stocked in formal supermarkets and 1.5M informal traders nationwide; losing shelf share quickly cuts volume and market share.

- Switching cost: ~0

- 62% choose by price (NielsenIQ, 2024)

- Distribution reach: formal + 1.5M informal traders

- Risk: rapid volume loss if off-shelf

Influence of the Informal Trade Sector

- Channel share: 30–40% in peri‑urban/rural (2024)

- Characteristic: fragmented, cash-first, immediate demand

- Risk: payment/default and logistics cost

- Action: flexible credit terms, micro‑deliveries, local brand activation

Retailer pressure squeezes Premier: heavy discounts, credit terms, and rising ad spend

| Metric | 2024 |

|---|---|

| Shoprite market share | ≈29% |

| Pick n Pay | ≈17% |

| Spar | ≈12% |

| Buy on price (NielsenIQ) | 62% |

| Informal channel share (peri‑urban alcohol) | 30–40% |

| Premier ad spend change | +14% |

Preview the Actual Deliverable

Premier Porter's Five Forces Analysis

This preview shows the exact Premier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed is the complete, professionally formatted report, ready for download and use the moment you buy.

You're viewing the final deliverable; once payment is completed, you'll have instant access to this same file for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Premier faces a mix of concentrated buyer power, moderate supplier leverage, and evolving substitute threats that shape pricing and margins; competitive rivalry is intense but tempered by regulatory barriers and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Premier’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Premier Group depends on wheat and maize for ~68% of input costs, exposing it to global price swings—wheat rose 28% YoY in 2024 and maize 22%—so high-quality grain suppliers can push prices or restrict supply. Premier uses strategic sourcing across 6 countries and hedged $120m of grain exposure in 2024, cutting volatility but not eliminating risk. Currency devaluation in key sourcing markets (e.g., 2023–24 FX drops of 12–18%) still amplifies import costs and supplier leverage.

Energy and Utility Costs

Suppliers of electricity and water in South Africa, mainly Eskom (state utility) and Rand Water, hold high bargaining power due to near-monopolies and limited large-scale alternatives, forcing Premier to accept price increases; Eskom raised average tariffs ~18% in 2023 and proposed further hikes into 2025.

Rising tariffs and chronic load shedding raise Premier’s raw-material and processing costs; load shedding caused estimated R175 billion GDP loss in 2023, increasing operational disruptions and maintenance spend.

To keep production steady, Premier must absorb costs or invest in self-generation: a 10 MW diesel/gas backup plant costs roughly ZAR 200–300 million upfront plus ZAR 100–200 million annual fuel/O&M, squeezing margins.

Concentration of Input Providers

Concentration of input providers is high: roughly 60–70% of bulk produce for large buyers comes from fewer than 200 commercial farms and cooperatives in key regions, letting suppliers set stricter pricing and contract terms. Premier’s $4.2bn annual procurement gives it leverage, but dependence on specific geographies (e.g., Central Valley, Brazil Mato Grosso) raises supply disruption risk from weather, labor, or export policy shocks.

Logistics and Fuel Providers

Logistics and fuel suppliers wield high bargaining power since Southern Africa's bulk food distribution depends on road and rail and on oil, which averaged $82/barrel in 2025, so sudden price swings raise transport costs fast.

Limited cost-effective alternatives and weak regional infrastructure (World Bank 2024: 46% of key corridors in poor condition) mean suppliers can pass costs to food processors immediately, lifting landed raw-material costs and retail prices.

- Few bulk alternatives: heavy road/rail reliance

- Oil price sensitivity: $82/barrel (2025 avg)

- Infrastructure strain: 46% corridors poor (World Bank 2024)

- Direct pass-through: transport cost → landed cost → retail price

Impact of Climate Change on Yields

Suppliers face rising pressure from unpredictable weather and droughts that cut crop yields; FAO reported a 5% global cereal production drop in 2023 linked to extreme weather, raising variability and lowering quality.

Scarcity boosts supplier bargaining power: during poor harvests suppliers can demand price premia — global grain prices rose ~20% in 2022–23, squeezing buyers.

Premier must build long-term, resilient supplier ties and invest in contract pricing, storage, and climate-resilient sourcing to stay prioritized when supply tightens.

- Weather-driven yield volatility up ~5% (FAO 2023)

- Grain prices +20% in 2022–23

- Strategy: long-term contracts, storage, diversified sourcing

Suppliers’ pricing power surges as grains, utilities and logistics drive rapid cost pass-through

Suppliers hold high bargaining power: wheat/maize ~68% input, global wheat +28% YoY 2024, maize +22%; Eskom/Rand Water near-monopolies (Eskom tariffs +18% in 2023); Premier hedged $120m grain exposure in 2024 but remains FX-vulnerable (2023–24 FX drops 12–18%); transport reliant on oil ~$82/bbl (2025) and 46% corridors poor (World Bank 2024), so suppliers can pass costs quickly.

| Metric | Value |

|---|---|

| Wheat/maize share | ~68% |

| Wheat YoY (2024) | +28% |

| Maize YoY (2024) | +22% |

| Grain hedged (2024) | $120m |

| Eskom tariff rise (2023) | ~+18% |

| Oil avg (2025) | $82/bbl |

| Corridors poor (World Bank 2024) | 46% |

What is included in the product

Tailored Five Forces analysis for Premier that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

Condense industry competitive dynamics into a single actionable sheet—helping teams quickly spot threats and opportunities and make confident strategic choices.

Customers Bargaining Power

Concentration of Retail Giants

Price Sensitivity of Low-Income Consumers

A significant share of Premier’s consumers are low-income and price-sensitive; 2024 household data shows 42% of spend in target regions goes to staples like bread and maize, making these goods highly elastic. Even a 5% price rise historically shifts buyers to cheaper brands or wholesaler bulk purchases, cutting retail volumes by up to 12% in quarterly sales. That limits Premier’s scope to pass on inflation without sizable volume loss.

Growth of Private Label Brands

Low Switching Costs for Households

Consumers face almost zero switching costs when choosing bread, flour, or maize meal, so price and shelf availability beat brand loyalty; NielsenIQ data (2024) shows 62% of South African shoppers pick on price/promotions at purchase.

This frictionless choice forces Premier to keep products widely stocked in formal supermarkets and 1.5M informal traders nationwide; losing shelf share quickly cuts volume and market share.

- Switching cost: ~0

- 62% choose by price (NielsenIQ, 2024)

- Distribution reach: formal + 1.5M informal traders

- Risk: rapid volume loss if off-shelf

Influence of the Informal Trade Sector

- Channel share: 30–40% in peri‑urban/rural (2024)

- Characteristic: fragmented, cash-first, immediate demand

- Risk: payment/default and logistics cost

- Action: flexible credit terms, micro‑deliveries, local brand activation

Retailer pressure squeezes Premier: heavy discounts, credit terms, and rising ad spend

| Metric | 2024 |

|---|---|

| Shoprite market share | ≈29% |

| Pick n Pay | ≈17% |

| Spar | ≈12% |

| Buy on price (NielsenIQ) | 62% |

| Informal channel share (peri‑urban alcohol) | 30–40% |

| Premier ad spend change | +14% |

Preview the Actual Deliverable

Premier Porter's Five Forces Analysis

This preview shows the exact Premier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed is the complete, professionally formatted report, ready for download and use the moment you buy.

You're viewing the final deliverable; once payment is completed, you'll have instant access to this same file for immediate application.