Premier Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

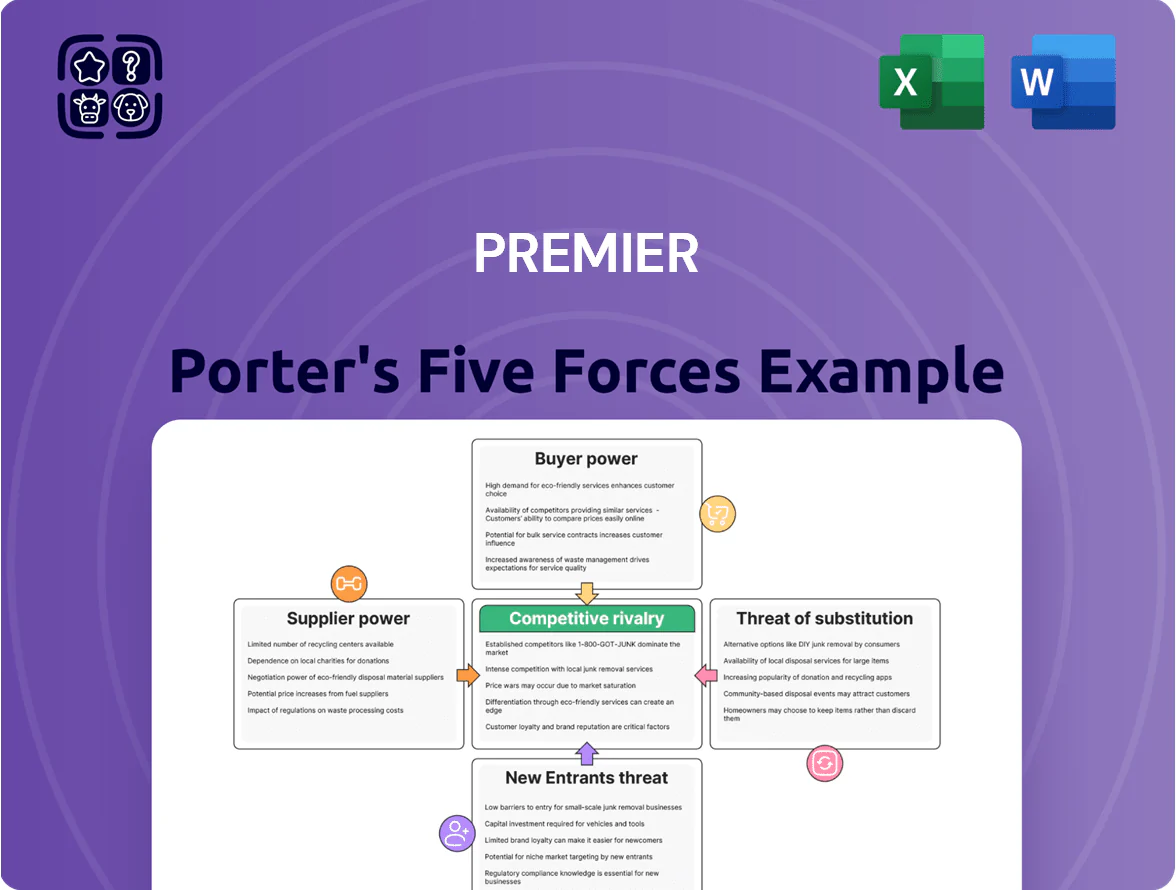

Premier faces moderate buyer power, concentrated supplier influence, and looming threats from agile entrants and substitutes that compress margins and shape strategy—this snapshot highlights key tensions and competitive levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Premier for smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentration of medical manufacturers

The healthcare supply chain is concentrated: top 10 pharma firms held ~55% of global prescription drug sales in 2024 and the top device makers control key niche markets, giving suppliers strong pricing power for patented products.

Premier counters this by pooling purchasing across its ~4,000 member hospitals and health systems, negotiating savings reported at $1.3 billion in 2024 and securing volume-based rebates and contract terms that blunt supplier leverage.

Dependency on technology and cloud infrastructure

As Premier shifts deeper into data and analytics, reliance on cloud giants like Microsoft Azure and AWS grows, with cloud spend rising to an estimated $120–150M in 2025, giving suppliers leverage. Switching costs for petabyte-scale datasets and rearchitecting pipelines run into tens of millions and months of downtime, so migration is prohibitive. Specialized AI/ML tools—NVIDIA GPUs, Azure OpenAI, AWS SageMaker—are concentrated among top vendors, further consolidating supplier power.

Specialized labor and consulting expertise

The advisory segment at Premier relies on data scientists and healthcare consultants; US demand for data scientists grew 35% from 2018–2023 with median pay >$120,000 in 2024, giving employees and specialty staffing firms significant leverage in wage and contract talks. High turnover raises replacement costs—estimated at 20–30% of annual salary—so retaining intellectual capital is critical to preserve Premier’s strategic insight quality and client margins.

Product differentiation and patent protection

Suppliers of innovative medical devices often hold patents that block generics; for example, 60% of Class III device revenues in the US were patent-protected in 2024, keeping alternatives scarce.

That uniqueness prevents Premier from forcing prices down via competitive bids, so supplier leverage stays high until patents expire or a new entrant gains >5% market share.

- High patent coverage: ~60% of Class III device revenue (US, 2024)

- Limited alternatives: few competitors with >5% share

- Price pressure low until patent expiry or new entrant

Impact of global supply chain volatility

Raw material suppliers and logistics providers drive Premier’s cost base; in 2024 freight rate spikes raised procurement costs by ~18% for medical-supply groups, showing suppliers can set terms when capacity tightens.

Recent shocks—COVID-19 aftereffects and Red Sea disruptions—pushed lead times +35% and input-price volatility, so Premier must diversify suppliers and use long-term contracts to limit margin pressure.

- 2024 freight rates up ~18%

- Lead times +35% after 2022–24 shocks

- Diversify suppliers, secure long-term contracts

Suppliers Dominate: Patents & Cloud Costs Drive Power; Premier Counters with Pooled Buying

Suppliers hold high bargaining power: top pharma/device firms control patents (60% of US Class III device revenue, 2024) and cloud/AI vendors concentrate infrastructure (estimated $120–150M cloud spend for Premier, 2025). Premier offsets power via pooled purchasing (~4,000 members; $1.3B savings, 2024), long-term contracts, diversification, and retention strategies for data talent (median pay >$120k, 2024).

| Metric | Value |

|---|---|

| Top pharma share | 55% (2024) |

| Class III patent cover | 60% (US, 2024) |

| Premier members savings | $1.3B (2024) |

| Estimated cloud spend | $120–150M (2025) |

What is included in the product

Comprehensive Porter's Five Forces analysis for Premier that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptors to clarify risks and strategic opportunities.

Premier Porter's Five Forces delivers a one-sheet, editable summary of competitive pressures with a radar chart and clean layout—easy to copy into decks, tweak for scenarios, and integrate into Excel dashboards for fast, board-ready strategic decisions.

Customers Bargaining Power

Consolidation of large health systems

The 2020s wave of hospital consolidation produced systems controlling 40%+ of US inpatient beds in some states; by 2024 the top 100 health systems accounted for roughly 60% of acute-care admissions, giving them strong internal purchasing power.

These large systems can push for 5–15% deeper discounts or threaten to switch GPOs, pressuring Premier’s margin on key contracts.

Premier must prove superior total cost savings—Premier reported $2.6B in member savings in 2023—to retain high-volume members and avoid attrition.

Member ownership and equity influence

A large share of Premier’s customers are member-owners holding equity, giving them voting rights and board representation; as of FY2024 about 38% of customers held membership shares, representing $1.2B in member equity.

That dual role lets members influence governance, strategic priorities, and fee policies directly, creating a non-price bargaining lever beyond ordinary customer negotiation.

High switching costs for data platforms

Price transparency and regulatory pressure

New federal and state price-transparency rules (CMS rules expanded 2024) let hospitals compare supplier costs; studies show 68% of procurement teams now use public price data when evaluating GPO contracts.

That visibility lets hospital buyers push back on Premier’s pricing, citing market benchmarks and alternative vendors; Premier must continuously validate that its negotiated discounts — often 10–25% off list for top categories — remain best-in-class.

- 68% of procurement teams use public price data

- CMS rule expansion: 2024

- Premier discount range commonly 10–25%

- Continuous benchmarking required

Shift toward value-based care models

Providers now tie payments to outcomes: value-based care made up 34% of US healthcare spend in 2023 and is projected to exceed 40% by 2026, so customers prioritize partners that improve quality and lower total cost of care.

Premier must shift from low-cost supply pitches to measurable performance solutions—clinical analytics, care pathways, and TCO (total cost of ownership) reductions—to hold bargaining power as buyers reward outcome-linked vendors.

Premier’s scale slashes prices 5–15% as buyers push outcome-linked deals

Large systems (top 100 = ~60% acute admissions in 2024) and 38% member-owners wield strong price and governance leverage, pushing 5–15% deeper discounts; Premier’s $2.6B member savings (2023) and $1.2B revenue (FY2024) help retention, but switching costs ($2–5M TCO, >12 months) and 68% procurement use of public pricing plus CMS 2024 rules raise buyer pressure toward outcome-linked offerings.

| Metric | Value |

|---|---|

| Top-100 share | ~60% admissions (2024) |

| Member-owners | 38% (FY2024), $1.2B equity |

| Premier savings | $2.6B (2023) |

| Revenue | $1.2B (FY2024) |

| Discount pressure | 5–15% |

| Switching cost | $2–5M, >12 months |

| Procurement data use | 68% |

| Value-based spend | 34% (2023), >40% by 2026 |

Full Version Awaits

Premier Porter's Five Forces Analysis

This preview shows the exact Premier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.

You'll get the same professionally written document upon payment, complete with industry context, competitive insights, and actionable implications for strategy and valuation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Premier faces moderate buyer power, concentrated supplier influence, and looming threats from agile entrants and substitutes that compress margins and shape strategy—this snapshot highlights key tensions and competitive levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Premier for smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentration of medical manufacturers

The healthcare supply chain is concentrated: top 10 pharma firms held ~55% of global prescription drug sales in 2024 and the top device makers control key niche markets, giving suppliers strong pricing power for patented products.

Premier counters this by pooling purchasing across its ~4,000 member hospitals and health systems, negotiating savings reported at $1.3 billion in 2024 and securing volume-based rebates and contract terms that blunt supplier leverage.

Dependency on technology and cloud infrastructure

As Premier shifts deeper into data and analytics, reliance on cloud giants like Microsoft Azure and AWS grows, with cloud spend rising to an estimated $120–150M in 2025, giving suppliers leverage. Switching costs for petabyte-scale datasets and rearchitecting pipelines run into tens of millions and months of downtime, so migration is prohibitive. Specialized AI/ML tools—NVIDIA GPUs, Azure OpenAI, AWS SageMaker—are concentrated among top vendors, further consolidating supplier power.

Specialized labor and consulting expertise

The advisory segment at Premier relies on data scientists and healthcare consultants; US demand for data scientists grew 35% from 2018–2023 with median pay >$120,000 in 2024, giving employees and specialty staffing firms significant leverage in wage and contract talks. High turnover raises replacement costs—estimated at 20–30% of annual salary—so retaining intellectual capital is critical to preserve Premier’s strategic insight quality and client margins.

Product differentiation and patent protection

Suppliers of innovative medical devices often hold patents that block generics; for example, 60% of Class III device revenues in the US were patent-protected in 2024, keeping alternatives scarce.

That uniqueness prevents Premier from forcing prices down via competitive bids, so supplier leverage stays high until patents expire or a new entrant gains >5% market share.

- High patent coverage: ~60% of Class III device revenue (US, 2024)

- Limited alternatives: few competitors with >5% share

- Price pressure low until patent expiry or new entrant

Impact of global supply chain volatility

Raw material suppliers and logistics providers drive Premier’s cost base; in 2024 freight rate spikes raised procurement costs by ~18% for medical-supply groups, showing suppliers can set terms when capacity tightens.

Recent shocks—COVID-19 aftereffects and Red Sea disruptions—pushed lead times +35% and input-price volatility, so Premier must diversify suppliers and use long-term contracts to limit margin pressure.

- 2024 freight rates up ~18%

- Lead times +35% after 2022–24 shocks

- Diversify suppliers, secure long-term contracts

Suppliers Dominate: Patents & Cloud Costs Drive Power; Premier Counters with Pooled Buying

Suppliers hold high bargaining power: top pharma/device firms control patents (60% of US Class III device revenue, 2024) and cloud/AI vendors concentrate infrastructure (estimated $120–150M cloud spend for Premier, 2025). Premier offsets power via pooled purchasing (~4,000 members; $1.3B savings, 2024), long-term contracts, diversification, and retention strategies for data talent (median pay >$120k, 2024).

| Metric | Value |

|---|---|

| Top pharma share | 55% (2024) |

| Class III patent cover | 60% (US, 2024) |

| Premier members savings | $1.3B (2024) |

| Estimated cloud spend | $120–150M (2025) |

What is included in the product

Comprehensive Porter's Five Forces analysis for Premier that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptors to clarify risks and strategic opportunities.

Premier Porter's Five Forces delivers a one-sheet, editable summary of competitive pressures with a radar chart and clean layout—easy to copy into decks, tweak for scenarios, and integrate into Excel dashboards for fast, board-ready strategic decisions.

Customers Bargaining Power

Consolidation of large health systems

The 2020s wave of hospital consolidation produced systems controlling 40%+ of US inpatient beds in some states; by 2024 the top 100 health systems accounted for roughly 60% of acute-care admissions, giving them strong internal purchasing power.

These large systems can push for 5–15% deeper discounts or threaten to switch GPOs, pressuring Premier’s margin on key contracts.

Premier must prove superior total cost savings—Premier reported $2.6B in member savings in 2023—to retain high-volume members and avoid attrition.

Member ownership and equity influence

A large share of Premier’s customers are member-owners holding equity, giving them voting rights and board representation; as of FY2024 about 38% of customers held membership shares, representing $1.2B in member equity.

That dual role lets members influence governance, strategic priorities, and fee policies directly, creating a non-price bargaining lever beyond ordinary customer negotiation.

High switching costs for data platforms

Price transparency and regulatory pressure

New federal and state price-transparency rules (CMS rules expanded 2024) let hospitals compare supplier costs; studies show 68% of procurement teams now use public price data when evaluating GPO contracts.

That visibility lets hospital buyers push back on Premier’s pricing, citing market benchmarks and alternative vendors; Premier must continuously validate that its negotiated discounts — often 10–25% off list for top categories — remain best-in-class.

- 68% of procurement teams use public price data

- CMS rule expansion: 2024

- Premier discount range commonly 10–25%

- Continuous benchmarking required

Shift toward value-based care models

Providers now tie payments to outcomes: value-based care made up 34% of US healthcare spend in 2023 and is projected to exceed 40% by 2026, so customers prioritize partners that improve quality and lower total cost of care.

Premier must shift from low-cost supply pitches to measurable performance solutions—clinical analytics, care pathways, and TCO (total cost of ownership) reductions—to hold bargaining power as buyers reward outcome-linked vendors.

Premier’s scale slashes prices 5–15% as buyers push outcome-linked deals

Large systems (top 100 = ~60% acute admissions in 2024) and 38% member-owners wield strong price and governance leverage, pushing 5–15% deeper discounts; Premier’s $2.6B member savings (2023) and $1.2B revenue (FY2024) help retention, but switching costs ($2–5M TCO, >12 months) and 68% procurement use of public pricing plus CMS 2024 rules raise buyer pressure toward outcome-linked offerings.

| Metric | Value |

|---|---|

| Top-100 share | ~60% admissions (2024) |

| Member-owners | 38% (FY2024), $1.2B equity |

| Premier savings | $2.6B (2023) |

| Revenue | $1.2B (FY2024) |

| Discount pressure | 5–15% |

| Switching cost | $2–5M, >12 months |

| Procurement data use | 68% |

| Value-based spend | 34% (2023), >40% by 2026 |

Full Version Awaits

Premier Porter's Five Forces Analysis

This preview shows the exact Premier Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.

You'll get the same professionally written document upon payment, complete with industry context, competitive insights, and actionable implications for strategy and valuation.