Premier Investments Boston Consulting Group Matrix

Unlock Strategic Clarity

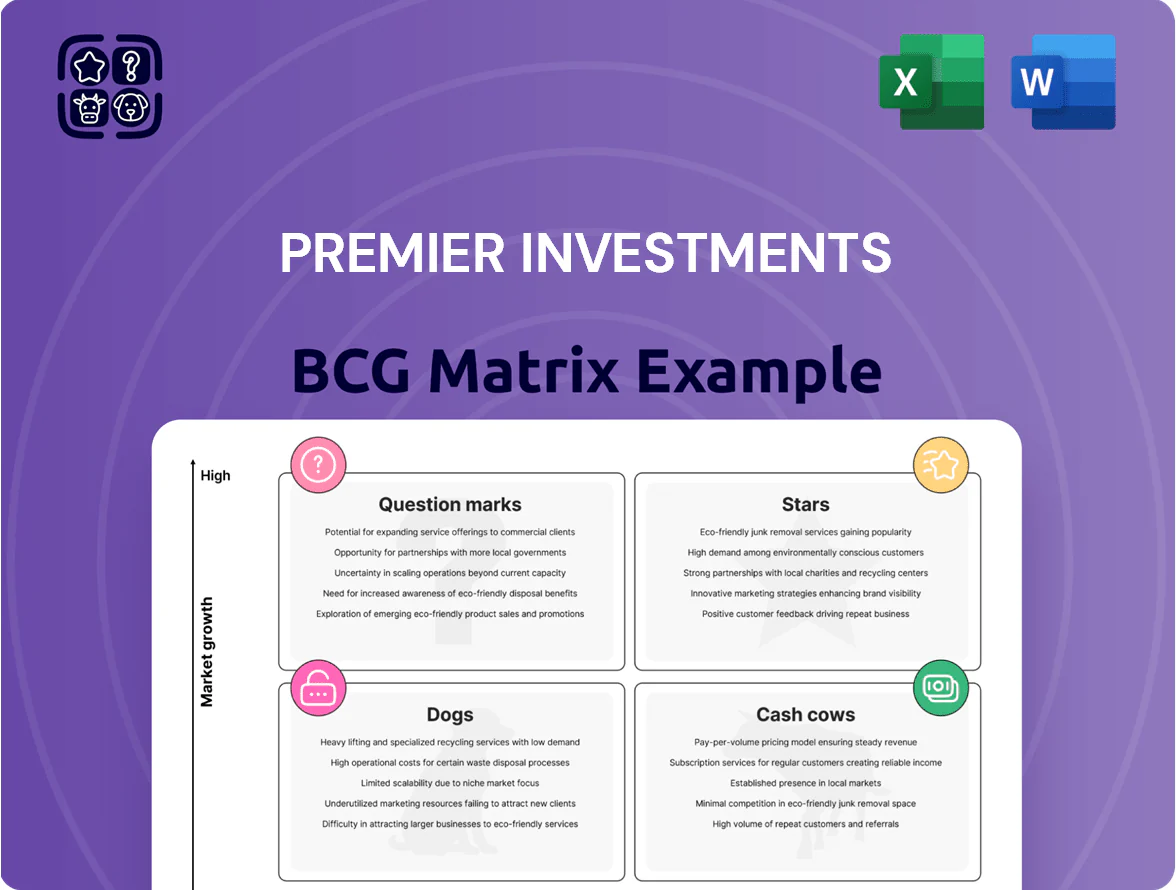

Premier Investments’ BCG Matrix preview highlights how flagship brands like Just Group and Smiggle may sit among Stars or Cash Cows while niche lines risk becoming Dogs or Question Marks; understanding these placements clarifies where growth capital and divestment should flow. This concise snapshot shows market share and growth trends, but the full BCG Matrix delivers quadrant-level data, prioritized strategic moves, and actionable allocation guidance. Purchase the complete report for a Word narrative plus an Excel summary to make fast, confident product and investment decisions.

Stars

Peter Alexander Global Expansion

Peter Alexander is a Star after its 2024 UK launch with stores and a dedicated e-commerce site, driving record FY25 sales of $548 million, up 7.7% year-on-year.

Early FY26 growth of 9.2% shows momentum; as a design-led lifestyle brand with dominant sleepwear share, it needs heavy capital for international scale but offers high long-term returns.

E-commerce and Omnichannel Platforms

Premier’s online channels now exceed 20% of group sales and have grown faster than stores, delivering higher EBIT margins—online EBIT margin reported at ~12% vs group retail ~7% in FY2025.

The company is scaling digital infrastructure and launched the Peter's Dreamers loyalty program in October 2025 to raise repeat purchase rates and AOV (average order value).

This high-growth, digital-first segment builds on Premier’s market leadership but requires ongoing tech investment—estimated CAPEX for ecommerce and IT rose to AU$45m in FY2025 to protect margin and growth.

Smiggle International Wholesale Partnerships

Smiggle's wholesale and capital-light entry into the Middle East and Indonesia is a Star: retail stores matured, but partnerships target high-growth markets with lower risk, backing plans for 100+ Indonesia stores and 60 stores across UAE and Qatar announced in 2024.

Breville Group Limited Strategic Stake

Premier’s 25.4% stake in Breville Group Limited, valued at ~ $1.17 billion in late 2025, remains a Star due to Breville’s strong global product innovation and premium positioning.

The stake delivers capital appreciation and rising dividends—cash returns reached $12.8 million in FY25—and benefits as Breville enters new premium geographies, supporting future revenue growth.

- 25.4% stake ≈ $1.17B (late 2025)

- Dividends FY25: $12.8M

- Star: global innovation + premium expansion

New Market Entry Initiatives

Premier Investments classifies Peter Alexander's Europe push and potential Smiggle restarts in Asia as Stars: high-growth regional units with heavy upfront spend—the UK launch cost $10.9 million—and targeting expanding retail segments where market growth exceeds 8–12% annually.

These Stars require sustained marketing and capex to scale; successful execution aims to mirror Peter Alexander’s ~30% domestic category share and lift group international revenue contribution above its current ~18% (FY2024).

- High initial spend: $10.9M UK launch

- Target markets: Europe (Peter Alexander), Asia (Smiggle)

- Growth outlook: retail segments +8–12% CAGR

- Goal: replicate ~30% domestic share; raise intl revenue >18%

Peter Alexander, Smiggle & Breville stake shine: strong FY25 sales, expansion & AU$45M digital push

Peter Alexander, Smiggle and Breville stake are Stars: FY25 sales Peter Alexander $548M (+7.7%), FY26 early growth +9.2%; online EBIT ~12% vs group retail ~7%; ecommerce/IT CAPEX AU$45M FY2025; Smiggle expansion: 100+ Indonesia, 60 UAE/Qatar (2024); Breville stake 25.4% ≈ $1.17B (late 2025), dividends $12.8M FY25.

| Asset | Key 2025–25 | Metric |

|---|---|---|

| Peter Alexander | UK launch 2024 | Sales $548M; +7.7% |

| Smiggle | Intl stores | 100+ ID, 60 MENA |

| Breville stake | 25.4% value | $1.17B; Div $12.8M |

| Group digital CAPEX | FY2025 | AU$45M; online EBIT ~12% |

What is included in the product

Comprehensive BCG Matrix for Premier Investments: quadrant-by-quadrant analysis, strategic actions (invest/hold/divest), and macro/micro context.

One-page BCG matrix mapping Premier Investments’ brands by market share and growth for quick C-level decisions.

Cash Cows

Peter Alexander ANZ Domestic Market

In ANZ, Peter Alexander leads the leisurewear market with 140+ stores and estimated FY2025 domestic revenue ~AUD 220m, delivering high gross margins near 62% and operating cashflow that consistently funds Premier Investments’ international roll‑out and dividends.

Smiggle ANZ Core Retail Operations

Smiggle ANZ core retail, the market leader in novelty stationery across Australia and New Zealand, delivered A$285m in FY2024 sales—down 4% year-on-year—yet remains top in category share (~35%).

These mature stores drive steady cash flow with ~18% EBITDA margins in FY2024, supported by high-margin proprietary SKUs and a hardened supply chain.

Smiggle functions as Premier Investments’ primary liquidity engine, funding pushes into higher-growth channels and store formats.

Strategic Property Portfolio

Premier Investments owns its Melbourne global head office and Australian Distribution Centre recorded at $68.1m historical cost but likely worth well over $120m on market estimates, eliminating rent and cutting operating costs.

These assets act as Cash Cows by providing stable operations, lowering occupancy expense and serving as collateral that supports the group’s lean debt—net debt/EBITDA was ~0.6x in FY2024.

The infrastructure lets Premier fund retail brands with minimal large capital injections; capex averaged A$30–40m annually from 2022–2024, focused on efficiency upgrades.

Investment Dividend Streams

The consistent flow of fully franked dividends from Premier Investments’ strategic stake in Breville provided $12.8 million in cash in FY25, acting as a reliable cash-generating unit the board directs to corporate costs and shareholder returns.

This passive income needs no operational oversight, qualifying it as a classic Cash Cow that strengthens the group’s balance sheet and supports the $333.3 million cash reserve.

- FY25 dividends from Breville: $12.8 million

- Used for corporate costs and shareholder returns

- No operational oversight required

- Supports $333.3 million cash reserve

Established Multi-Channel Distribution Centers

Premier Investments’ centralized distribution hubs in Australia and New Zealand run at high efficiency after years of process optimization and scale, handling roughly 150–200 million units annually and lowering unit logistics costs to under A$0.80 per unit in FY2024.

These multi-channel centers serve both 900+ physical stores and e-commerce, adding incremental margin by keeping marginal fulfilment costs low—e-commerce order fulfilment costs were ~18% of sales in FY2024 versus retail store handling at ~5%.

By sustaining high throughput in a mature Tasman logistics market, the hubs convert fixed-cost capacity into higher profit per sale, supporting group gross margin resilience amid flat like-for-like store growth.

- ~150–200M units/year throughput

- Unit logistics cost < A$0.80 (FY2024)

- 900+ stores supported

- E-commerce fulfilment ≈18% of sales (FY2024)

Strong cash flow: ~18% EBITDA, A$333m cash, low leverage and steady dividends

Peter Alexander and Smiggle supply steady cash—FY24 EBITDA ~18%, FY25 Breville dividends A$12.8m, net debt/EBITDA ~0.6x, A$333.3m cash reserve, capex A$30–40m pa, logistics

| Metric | Value |

|---|---|

| EBITDA margin | ~18% (FY24) |

| Breville dividends | A$12.8m (FY25) |

| Net debt/EBITDA | ~0.6x (FY24) |

| Cash reserve | A$333.3m |

| Capex | A$30–40m pa (2022–24) |

| Logistics cost/unit |

Preview = Final Product

Premier Investments BCG Matrix

The file you’re previewing on this page is the exact Premier Investments BCG Matrix report you’ll receive after purchase—no watermarks, no sample content, just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Premier Investments’ BCG Matrix preview highlights how flagship brands like Just Group and Smiggle may sit among Stars or Cash Cows while niche lines risk becoming Dogs or Question Marks; understanding these placements clarifies where growth capital and divestment should flow. This concise snapshot shows market share and growth trends, but the full BCG Matrix delivers quadrant-level data, prioritized strategic moves, and actionable allocation guidance. Purchase the complete report for a Word narrative plus an Excel summary to make fast, confident product and investment decisions.

Stars

Peter Alexander Global Expansion

Peter Alexander is a Star after its 2024 UK launch with stores and a dedicated e-commerce site, driving record FY25 sales of $548 million, up 7.7% year-on-year.

Early FY26 growth of 9.2% shows momentum; as a design-led lifestyle brand with dominant sleepwear share, it needs heavy capital for international scale but offers high long-term returns.

E-commerce and Omnichannel Platforms

Premier’s online channels now exceed 20% of group sales and have grown faster than stores, delivering higher EBIT margins—online EBIT margin reported at ~12% vs group retail ~7% in FY2025.

The company is scaling digital infrastructure and launched the Peter's Dreamers loyalty program in October 2025 to raise repeat purchase rates and AOV (average order value).

This high-growth, digital-first segment builds on Premier’s market leadership but requires ongoing tech investment—estimated CAPEX for ecommerce and IT rose to AU$45m in FY2025 to protect margin and growth.

Smiggle International Wholesale Partnerships

Smiggle's wholesale and capital-light entry into the Middle East and Indonesia is a Star: retail stores matured, but partnerships target high-growth markets with lower risk, backing plans for 100+ Indonesia stores and 60 stores across UAE and Qatar announced in 2024.

Breville Group Limited Strategic Stake

Premier’s 25.4% stake in Breville Group Limited, valued at ~ $1.17 billion in late 2025, remains a Star due to Breville’s strong global product innovation and premium positioning.

The stake delivers capital appreciation and rising dividends—cash returns reached $12.8 million in FY25—and benefits as Breville enters new premium geographies, supporting future revenue growth.

- 25.4% stake ≈ $1.17B (late 2025)

- Dividends FY25: $12.8M

- Star: global innovation + premium expansion

New Market Entry Initiatives

Premier Investments classifies Peter Alexander's Europe push and potential Smiggle restarts in Asia as Stars: high-growth regional units with heavy upfront spend—the UK launch cost $10.9 million—and targeting expanding retail segments where market growth exceeds 8–12% annually.

These Stars require sustained marketing and capex to scale; successful execution aims to mirror Peter Alexander’s ~30% domestic category share and lift group international revenue contribution above its current ~18% (FY2024).

- High initial spend: $10.9M UK launch

- Target markets: Europe (Peter Alexander), Asia (Smiggle)

- Growth outlook: retail segments +8–12% CAGR

- Goal: replicate ~30% domestic share; raise intl revenue >18%

Peter Alexander, Smiggle & Breville stake shine: strong FY25 sales, expansion & AU$45M digital push

Peter Alexander, Smiggle and Breville stake are Stars: FY25 sales Peter Alexander $548M (+7.7%), FY26 early growth +9.2%; online EBIT ~12% vs group retail ~7%; ecommerce/IT CAPEX AU$45M FY2025; Smiggle expansion: 100+ Indonesia, 60 UAE/Qatar (2024); Breville stake 25.4% ≈ $1.17B (late 2025), dividends $12.8M FY25.

| Asset | Key 2025–25 | Metric |

|---|---|---|

| Peter Alexander | UK launch 2024 | Sales $548M; +7.7% |

| Smiggle | Intl stores | 100+ ID, 60 MENA |

| Breville stake | 25.4% value | $1.17B; Div $12.8M |

| Group digital CAPEX | FY2025 | AU$45M; online EBIT ~12% |

What is included in the product

Comprehensive BCG Matrix for Premier Investments: quadrant-by-quadrant analysis, strategic actions (invest/hold/divest), and macro/micro context.

One-page BCG matrix mapping Premier Investments’ brands by market share and growth for quick C-level decisions.

Cash Cows

Peter Alexander ANZ Domestic Market

In ANZ, Peter Alexander leads the leisurewear market with 140+ stores and estimated FY2025 domestic revenue ~AUD 220m, delivering high gross margins near 62% and operating cashflow that consistently funds Premier Investments’ international roll‑out and dividends.

Smiggle ANZ Core Retail Operations

Smiggle ANZ core retail, the market leader in novelty stationery across Australia and New Zealand, delivered A$285m in FY2024 sales—down 4% year-on-year—yet remains top in category share (~35%).

These mature stores drive steady cash flow with ~18% EBITDA margins in FY2024, supported by high-margin proprietary SKUs and a hardened supply chain.

Smiggle functions as Premier Investments’ primary liquidity engine, funding pushes into higher-growth channels and store formats.

Strategic Property Portfolio

Premier Investments owns its Melbourne global head office and Australian Distribution Centre recorded at $68.1m historical cost but likely worth well over $120m on market estimates, eliminating rent and cutting operating costs.

These assets act as Cash Cows by providing stable operations, lowering occupancy expense and serving as collateral that supports the group’s lean debt—net debt/EBITDA was ~0.6x in FY2024.

The infrastructure lets Premier fund retail brands with minimal large capital injections; capex averaged A$30–40m annually from 2022–2024, focused on efficiency upgrades.

Investment Dividend Streams

The consistent flow of fully franked dividends from Premier Investments’ strategic stake in Breville provided $12.8 million in cash in FY25, acting as a reliable cash-generating unit the board directs to corporate costs and shareholder returns.

This passive income needs no operational oversight, qualifying it as a classic Cash Cow that strengthens the group’s balance sheet and supports the $333.3 million cash reserve.

- FY25 dividends from Breville: $12.8 million

- Used for corporate costs and shareholder returns

- No operational oversight required

- Supports $333.3 million cash reserve

Established Multi-Channel Distribution Centers

Premier Investments’ centralized distribution hubs in Australia and New Zealand run at high efficiency after years of process optimization and scale, handling roughly 150–200 million units annually and lowering unit logistics costs to under A$0.80 per unit in FY2024.

These multi-channel centers serve both 900+ physical stores and e-commerce, adding incremental margin by keeping marginal fulfilment costs low—e-commerce order fulfilment costs were ~18% of sales in FY2024 versus retail store handling at ~5%.

By sustaining high throughput in a mature Tasman logistics market, the hubs convert fixed-cost capacity into higher profit per sale, supporting group gross margin resilience amid flat like-for-like store growth.

- ~150–200M units/year throughput

- Unit logistics cost < A$0.80 (FY2024)

- 900+ stores supported

- E-commerce fulfilment ≈18% of sales (FY2024)

Strong cash flow: ~18% EBITDA, A$333m cash, low leverage and steady dividends

Peter Alexander and Smiggle supply steady cash—FY24 EBITDA ~18%, FY25 Breville dividends A$12.8m, net debt/EBITDA ~0.6x, A$333.3m cash reserve, capex A$30–40m pa, logistics

| Metric | Value |

|---|---|

| EBITDA margin | ~18% (FY24) |

| Breville dividends | A$12.8m (FY25) |

| Net debt/EBITDA | ~0.6x (FY24) |

| Cash reserve | A$333.3m |

| Capex | A$30–40m pa (2022–24) |

| Logistics cost/unit |

Preview = Final Product

Premier Investments BCG Matrix

The file you’re previewing on this page is the exact Premier Investments BCG Matrix report you’ll receive after purchase—no watermarks, no sample content, just the fully formatted, analysis-ready document designed for strategic clarity and immediate use.