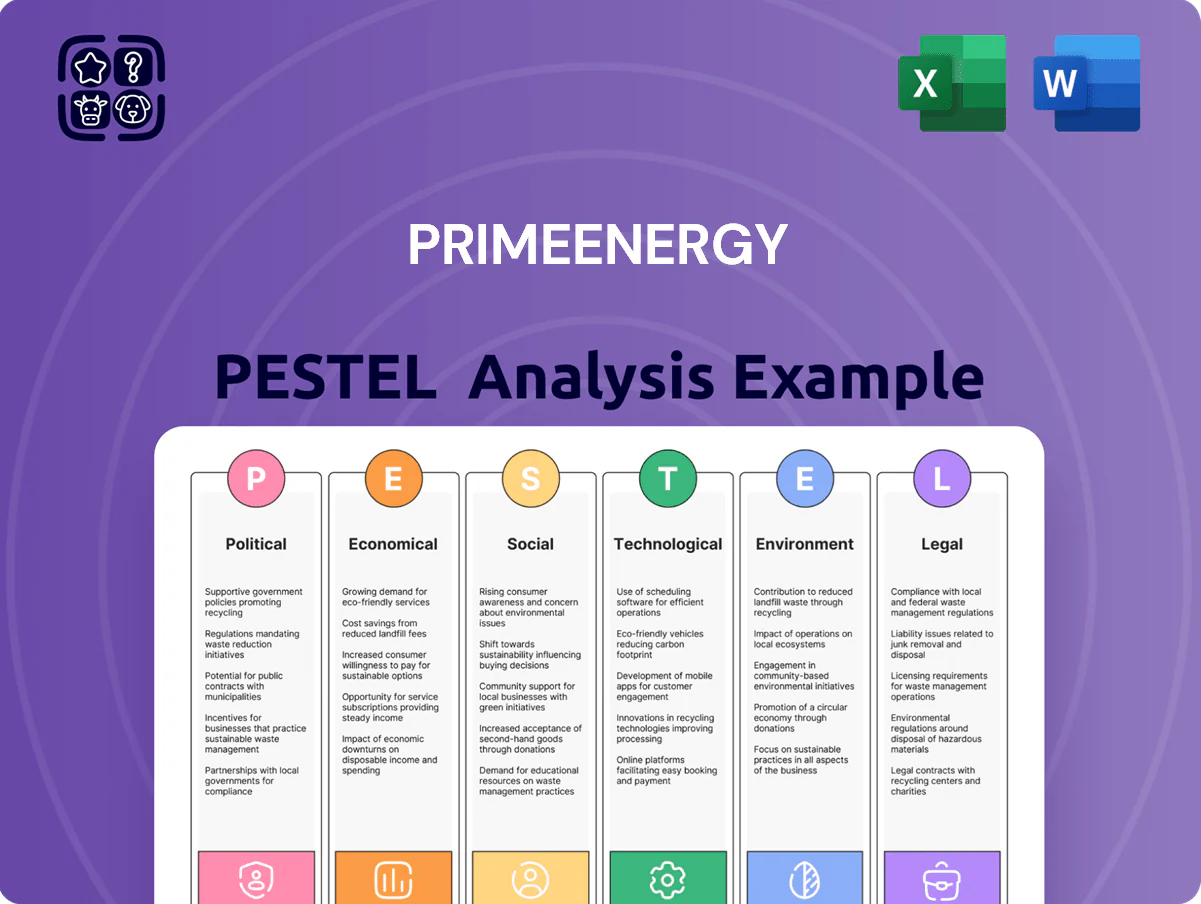

PrimeEnergy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and fast-moving technology trends are reshaping PrimeEnergy’s strategic outlook—our concise PESTLE highlights key risks and opportunities you need to know; purchase the full analysis to access the complete, actionable breakdown and ready-to-use insights for investment or strategy decisions.

Political factors

Federal energy policy shifts

Federal administration stance on domestic oil and gas heavily impacts PrimeEnergy via federal land leasing: 2024 DOI lease sales generated $1.2B in bids, shaping access to acreage and CAPEX plans.

Executive orders altering drilling permits or pipeline approvals—e.g., 2025 executive memo tightening NEPA reviews—can delay projects, raising project IRR hurdles by an estimated 200–400 basis points.

By late 2025 the tradeoff between energy security and transition goals dictates regulatory stability; shifts in policy risk ±15–25% variance in five-year production forecasts for firms like PrimeEnergy.

State level regulatory support

Operations in Texas, Oklahoma, and West Virginia benefit from localized political support where the energy sector contributes respectively about 17%, 14% and 12% of state GDP-related output; these states often streamline permitting—reducing approval times by up to 30% in some basins—and offer incentives (e.g., tax credits and cost-sharing for secondary recovery) that lower project breakevens by an estimated $3–6/boe; maintaining strong regulator relationships is essential for PrimeEnergy to secure permits and incentives.

Geopolitical supply chain stability

Global political tensions have pushed lead times for EOR compressors and subsea controls to 9–14 months and driven price inflation of specialized equipment by 18% Y/Y in 2024, squeezing PrimeEnergy’s project timelines and margins.

Fluctuating tariffs on steel and semiconductors—US import duties varying 5–25% since 2023—can raise capex for rigs and sensor arrays by $30–80 million per major basin project.

PrimeEnergy must embed scenario buffers for 10–20% cost variance and extend procurement windows when planning multi-year developments in its core basins to avoid budget overruns and schedule slippage.

Taxation and subsidy frameworks

Political debates over removing intangible drilling cost deductions and other oilfield tax breaks could increase PrimeEnergy's effective tax rate by 3–7 percentage points, risking $40–120m in after-tax cash flow on 2025 EBITDA estimates.

Conversely, federal incentives—like 45Q carbon sequestration credits up to $85/ton and proposed methane reduction grants—could offset capital costs, with the Inflation Reduction Act and FY2025 budget prioritizing domestic energy independence.

- Tax risk: potential 3–7 ppt higher tax rate; $40–120m impact

- Credit upside: 45Q at up to $85/ton CO2

- Policy driver: FY2025 focus on energy independence

Global energy security initiatives

Political pushes to approve new LNG terminals and export licenses have correlated with Henry Hub-linked price uplifts of ~10–15% in 2024–25 for Gulf/Marcellus producers, aligning PrimeEnergy’s production and capex toward export-grade volumes.

- US LNG exports ~12.5 Bcf/d (2025)

- Price uplift for export-focused producers ~10–15% (2024–25)

- PrimeEnergy aligning Appalachian/Permian capex to export markets

Macro drivers swing US upstream: lease bids, LNG, taxes, inflation → ±20% production, big IRR hits

Federal lease sales ($1.2B bids 2024) and tighter NEPA reviews (2025 memo) drive ±15–25% five-year production variance and 200–400bp IRR hits; state-level incentives reduce breakevens $3–6/boe and cut permitting times up to 30% in TX/OK/WV; supply-chain delays (9–14mo) and 18% Y/Y equipment inflation raise capex $30–80M per basin; tax changes risk +3–7ppt ETR (‑$40–120M 2025), while 45Q ($85/ton) and LNG exports (~12.5 Bcf/d 2025) boost realized prices 10–15%.

| Metric | Value |

|---|---|

| Federal lease bids 2024 | $1.2B |

| US LNG exports 2025 | ~12.5 Bcf/d |

| Equipment inflation 2024 | +18% Y/Y |

| Tax risk | +3–7 ppt ETR |

What is included in the product

Explores how external macro-environmental factors uniquely affect PrimeEnergy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to reveal risks and opportunities specific to its region and industry.

Condenses PrimeEnergy's full PESTLE into a concise, visually segmented brief that teams can drop into presentations, annotate with region- or business-specific notes, and share for rapid alignment on external risks and market positioning.

Economic factors

Commodity price volatility

PrimeEnergy’s profitability tracks global crude and natural gas prices, which fell 18% for Brent and 15% for Henry Hub in 2024-25 during cyclical downturns, directly reducing cash flow from mature fields.

Global industrial slowdown trimmed oil demand growth to 0.6% in 2025, pressuring realized prices and revenues from legacy production.

The company uses hedges covering roughly 60% of projected 12‑month volumes, limiting downside in sharp price drops.

Interest rates and capital access

Rising interest rates in 2025—US Fed funds ~5.25–5.50%—have raised PrimeEnergy’s hurdle rates, increasing WACC estimates by ~150–250 bps versus 2023 and compressing NPV on new wells by roughly 10–20% depending on capex intensity.

Tighter credit conditions and a 2024–25 decline in bank E&P lending have reduced debt availability; equity raises are costlier as investor appetite for fossil fuel assets fell ~15–30% in 2024 ESG-driven allocations.

Operational cost inflation

Rising labor, fuel and raw material costs—US diesel prices up ~12% y/y in 2025 and proppant prices +18% from 2023–25—can erode margins for PrimeEnergy despite strong oil/NGL prices; industry EBITDA margins fell ~3–5 pts in high-cost basins. PrimeEnergy faces localized wage inflation for petroleum engineers/technicians, with basin pay premia of 10–25%. Tight supply chains make cost control critical to sustain enhanced recovery economics.

Regional economic health

Regional economic health in Texas, Oklahoma, and West Virginia directly affects infrastructure and service availability for PrimeEnergy; Texas GDP was about $2.3 trillion in 2024, Oklahoma GDP $225 billion, West Virginia $80 billion, supporting extensive pipelines, rail, and midstream services.

Strong economies keep transport networks and processing facilities maintained—Texas handles roughly 25% of US crude oil production (2024), reducing bottlenecks; downturns risk service consolidation, higher tariffs, and field disruptions.

- Texas GDP $2.3T (2024): robust midstream capacity

- Oklahoma $225B, WV $80B (2024): regional support variance

- Texas ~25% US crude output (2024): lower transport risk

- Downturns → provider consolidation, higher service costs

Global demand for natural gas

- IEA demand growth ~1.3%/yr to 2025

- Global gas = ~23% of electricity (2024)

- West Virginia reserves ~12 Tcf

- Supports exploration capex and price floor

PrimeEnergy hit by falling prices, higher WACC and rising costs; hedges soften impact

PrimeEnergy faces weaker commodity prices (Brent -18%, Henry Hub -15% 2024–25), 60% hedge coverage, higher WACC (+150–250bps) compressing NPV 10–20%, tighter E&P lending and 15–30% lower investor appetite for fossil assets, rising input costs (diesel +12% y/y, proppant +18% 2023–25) and regional GDP supports (TX $2.3T, OK $225B, WV $80B; WV reserves ~12 Tcf).

| Metric | Value |

|---|---|

| Brent change 24–25 | -18% |

| Henry Hub change | -15% |

| Hedge coverage | 60% |

| WACC shift | +150–250bps |

| Diesel y/y | +12% |

| Proppant 23–25 | +18% |

| TX GDP 2024 | $2.3T |

| WV reserves | ~12 Tcf |

Full Version Awaits

PrimeEnergy PESTLE Analysis

The preview shown here is the exact PrimeEnergy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and fast-moving technology trends are reshaping PrimeEnergy’s strategic outlook—our concise PESTLE highlights key risks and opportunities you need to know; purchase the full analysis to access the complete, actionable breakdown and ready-to-use insights for investment or strategy decisions.

Political factors

Federal energy policy shifts

Federal administration stance on domestic oil and gas heavily impacts PrimeEnergy via federal land leasing: 2024 DOI lease sales generated $1.2B in bids, shaping access to acreage and CAPEX plans.

Executive orders altering drilling permits or pipeline approvals—e.g., 2025 executive memo tightening NEPA reviews—can delay projects, raising project IRR hurdles by an estimated 200–400 basis points.

By late 2025 the tradeoff between energy security and transition goals dictates regulatory stability; shifts in policy risk ±15–25% variance in five-year production forecasts for firms like PrimeEnergy.

State level regulatory support

Operations in Texas, Oklahoma, and West Virginia benefit from localized political support where the energy sector contributes respectively about 17%, 14% and 12% of state GDP-related output; these states often streamline permitting—reducing approval times by up to 30% in some basins—and offer incentives (e.g., tax credits and cost-sharing for secondary recovery) that lower project breakevens by an estimated $3–6/boe; maintaining strong regulator relationships is essential for PrimeEnergy to secure permits and incentives.

Geopolitical supply chain stability

Global political tensions have pushed lead times for EOR compressors and subsea controls to 9–14 months and driven price inflation of specialized equipment by 18% Y/Y in 2024, squeezing PrimeEnergy’s project timelines and margins.

Fluctuating tariffs on steel and semiconductors—US import duties varying 5–25% since 2023—can raise capex for rigs and sensor arrays by $30–80 million per major basin project.

PrimeEnergy must embed scenario buffers for 10–20% cost variance and extend procurement windows when planning multi-year developments in its core basins to avoid budget overruns and schedule slippage.

Taxation and subsidy frameworks

Political debates over removing intangible drilling cost deductions and other oilfield tax breaks could increase PrimeEnergy's effective tax rate by 3–7 percentage points, risking $40–120m in after-tax cash flow on 2025 EBITDA estimates.

Conversely, federal incentives—like 45Q carbon sequestration credits up to $85/ton and proposed methane reduction grants—could offset capital costs, with the Inflation Reduction Act and FY2025 budget prioritizing domestic energy independence.

- Tax risk: potential 3–7 ppt higher tax rate; $40–120m impact

- Credit upside: 45Q at up to $85/ton CO2

- Policy driver: FY2025 focus on energy independence

Global energy security initiatives

Political pushes to approve new LNG terminals and export licenses have correlated with Henry Hub-linked price uplifts of ~10–15% in 2024–25 for Gulf/Marcellus producers, aligning PrimeEnergy’s production and capex toward export-grade volumes.

- US LNG exports ~12.5 Bcf/d (2025)

- Price uplift for export-focused producers ~10–15% (2024–25)

- PrimeEnergy aligning Appalachian/Permian capex to export markets

Macro drivers swing US upstream: lease bids, LNG, taxes, inflation → ±20% production, big IRR hits

Federal lease sales ($1.2B bids 2024) and tighter NEPA reviews (2025 memo) drive ±15–25% five-year production variance and 200–400bp IRR hits; state-level incentives reduce breakevens $3–6/boe and cut permitting times up to 30% in TX/OK/WV; supply-chain delays (9–14mo) and 18% Y/Y equipment inflation raise capex $30–80M per basin; tax changes risk +3–7ppt ETR (‑$40–120M 2025), while 45Q ($85/ton) and LNG exports (~12.5 Bcf/d 2025) boost realized prices 10–15%.

| Metric | Value |

|---|---|

| Federal lease bids 2024 | $1.2B |

| US LNG exports 2025 | ~12.5 Bcf/d |

| Equipment inflation 2024 | +18% Y/Y |

| Tax risk | +3–7 ppt ETR |

What is included in the product

Explores how external macro-environmental factors uniquely affect PrimeEnergy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to reveal risks and opportunities specific to its region and industry.

Condenses PrimeEnergy's full PESTLE into a concise, visually segmented brief that teams can drop into presentations, annotate with region- or business-specific notes, and share for rapid alignment on external risks and market positioning.

Economic factors

Commodity price volatility

PrimeEnergy’s profitability tracks global crude and natural gas prices, which fell 18% for Brent and 15% for Henry Hub in 2024-25 during cyclical downturns, directly reducing cash flow from mature fields.

Global industrial slowdown trimmed oil demand growth to 0.6% in 2025, pressuring realized prices and revenues from legacy production.

The company uses hedges covering roughly 60% of projected 12‑month volumes, limiting downside in sharp price drops.

Interest rates and capital access

Rising interest rates in 2025—US Fed funds ~5.25–5.50%—have raised PrimeEnergy’s hurdle rates, increasing WACC estimates by ~150–250 bps versus 2023 and compressing NPV on new wells by roughly 10–20% depending on capex intensity.

Tighter credit conditions and a 2024–25 decline in bank E&P lending have reduced debt availability; equity raises are costlier as investor appetite for fossil fuel assets fell ~15–30% in 2024 ESG-driven allocations.

Operational cost inflation

Rising labor, fuel and raw material costs—US diesel prices up ~12% y/y in 2025 and proppant prices +18% from 2023–25—can erode margins for PrimeEnergy despite strong oil/NGL prices; industry EBITDA margins fell ~3–5 pts in high-cost basins. PrimeEnergy faces localized wage inflation for petroleum engineers/technicians, with basin pay premia of 10–25%. Tight supply chains make cost control critical to sustain enhanced recovery economics.

Regional economic health

Regional economic health in Texas, Oklahoma, and West Virginia directly affects infrastructure and service availability for PrimeEnergy; Texas GDP was about $2.3 trillion in 2024, Oklahoma GDP $225 billion, West Virginia $80 billion, supporting extensive pipelines, rail, and midstream services.

Strong economies keep transport networks and processing facilities maintained—Texas handles roughly 25% of US crude oil production (2024), reducing bottlenecks; downturns risk service consolidation, higher tariffs, and field disruptions.

- Texas GDP $2.3T (2024): robust midstream capacity

- Oklahoma $225B, WV $80B (2024): regional support variance

- Texas ~25% US crude output (2024): lower transport risk

- Downturns → provider consolidation, higher service costs

Global demand for natural gas

- IEA demand growth ~1.3%/yr to 2025

- Global gas = ~23% of electricity (2024)

- West Virginia reserves ~12 Tcf

- Supports exploration capex and price floor

PrimeEnergy hit by falling prices, higher WACC and rising costs; hedges soften impact

PrimeEnergy faces weaker commodity prices (Brent -18%, Henry Hub -15% 2024–25), 60% hedge coverage, higher WACC (+150–250bps) compressing NPV 10–20%, tighter E&P lending and 15–30% lower investor appetite for fossil assets, rising input costs (diesel +12% y/y, proppant +18% 2023–25) and regional GDP supports (TX $2.3T, OK $225B, WV $80B; WV reserves ~12 Tcf).

| Metric | Value |

|---|---|

| Brent change 24–25 | -18% |

| Henry Hub change | -15% |

| Hedge coverage | 60% |

| WACC shift | +150–250bps |

| Diesel y/y | +12% |

| Proppant 23–25 | +18% |

| TX GDP 2024 | $2.3T |

| WV reserves | ~12 Tcf |

Full Version Awaits

PrimeEnergy PESTLE Analysis

The preview shown here is the exact PrimeEnergy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.