Primoris Services PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping Primoris Services’ strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full PESTLE for a complete, actionable briefing you can use immediately.

Political factors

Infrastructure Investment and Jobs Act (IIJA) Implementation

The IIJA’s remaining $550 billion in directed infrastructure funds, with significant disbursements continuing through 2025, sustains a project pipeline for Primoris in grid modernization and water works; Primoris reported $2.1 billion backlog at end-2024, tied partly to IIJA-related awards.

Energy Policy and Permitting Reform

Political debates over accelerating federal permitting affect Primoris Services’ ability to start large-scale pipeline and renewable projects; faster permitting could shorten project lead times from years to months, impacting revenue recognition—Primoris reported $2.1B revenue in 2024, so timing shifts materially affect cash flow.

Legislative moves to streamline NEPA remain critical; proposed reforms in 2024 aimed to cut review times by up to 50%, directly influencing Primoris’s project schedules and margin realization.

Post-2024 election shifts could reprioritize fossil fuel versus renewable permits, altering backlog composition—Primoris’s backlog and bidding strategy face policy-driven demand risk and opportunity depending on permit allocations.

Geopolitical Influence on Energy Security

Global instability has driven a political mandate for North American energy independence, boosting demand for Primoris’s oil and gas construction services; US oil production averaged 12.4 million b/d in 2024, underpinning pipeline projects.

Political backing for LNG export terminals remains strong—US LNG exports hit 14.6 Bcf/d in 2024—supporting long-term pipeline and terminal construction revenue streams for Primoris.

Security-focused policies ensure conventional infrastructure stays a priority during transition, preserving multi-year contracts and capital spending in midstream and terminal projects.

Federal Incentives for Renewable Energy

The longevity of IRA tax credits is crucial for Primoris Services’ solar and renewables backlog; the IRA extended investment and production tax credits through 2024–2032 tiers, supporting a US utility-scale solar pipeline expected to grow ~15% CAGR to 2026 per sector forecasts.

Political shifts risking repeal or phase-down of credits could cut project starts materially: recent analyses show a 20–35% drop in IRR for many projects if credits are reduced, slowing segment revenue growth.

Decision-makers should stress-test 2024–2026 growth scenarios assuming full, partial, or no credit availability and incorporate policy risk into cashflow and bid strategies.

- IRA credits underpin revenue visibility for Energy/Renewables through 2026

- Policy rollback could reduce project IRRs by 20–35%

- Forecasts should model multiple credit-stability scenarios

Governmental Labor and Trade Regulations

Political decisions on tariffs—tariffs on solar modules rose 10–25% in recent years—can raise Primoris’s project material costs and disrupt timelines tied to imported steel and PV components, affecting margins on contracts typically 5–12% EBITDA for construction segments.

Unionization pressure on federally funded projects shifts bidding strategy toward higher labor-cost offers; Davis-Bacon prevailing wage enforcement increases labor line items by an estimated 8–15% on large infrastructure jobs.

Changes in Department of Labor rules from 2021–2025 tightening overtime and classification have increased labor-related expenses, with some contractors reporting 3–7% rises in total project costs.

- Tariff volatility: +10–25% impacts on imported components

- Union/Davis-Bacon: +8–15% labor cost pressure

- DOL policy shifts: +3–7% overall project cost increases

Primoris rides $550B IIJA into 2025; permitting reform and IRA boost renewables

IIJA funds ($550B) sustain Primoris’s $2.1B backlog into 2025; NEPA/permitting reforms (2024) could cut review times ~50% altering revenue timing; IRA tax-credit stability through 2026 supports renewables (~15% CAGR to 2026); tariffs (+10–25%) and Davis‑Bacon (+8–15% labor) pressure margins (construction EBITDA 5–12%).

| Metric | Value/Impact |

|---|---|

| Backlog | $2.1B |

| IIJA funds | $550B |

| US oil prod. 2024 | 12.4M b/d |

| US LNG exports 2024 | 14.6 Bcf/d |

What is included in the product

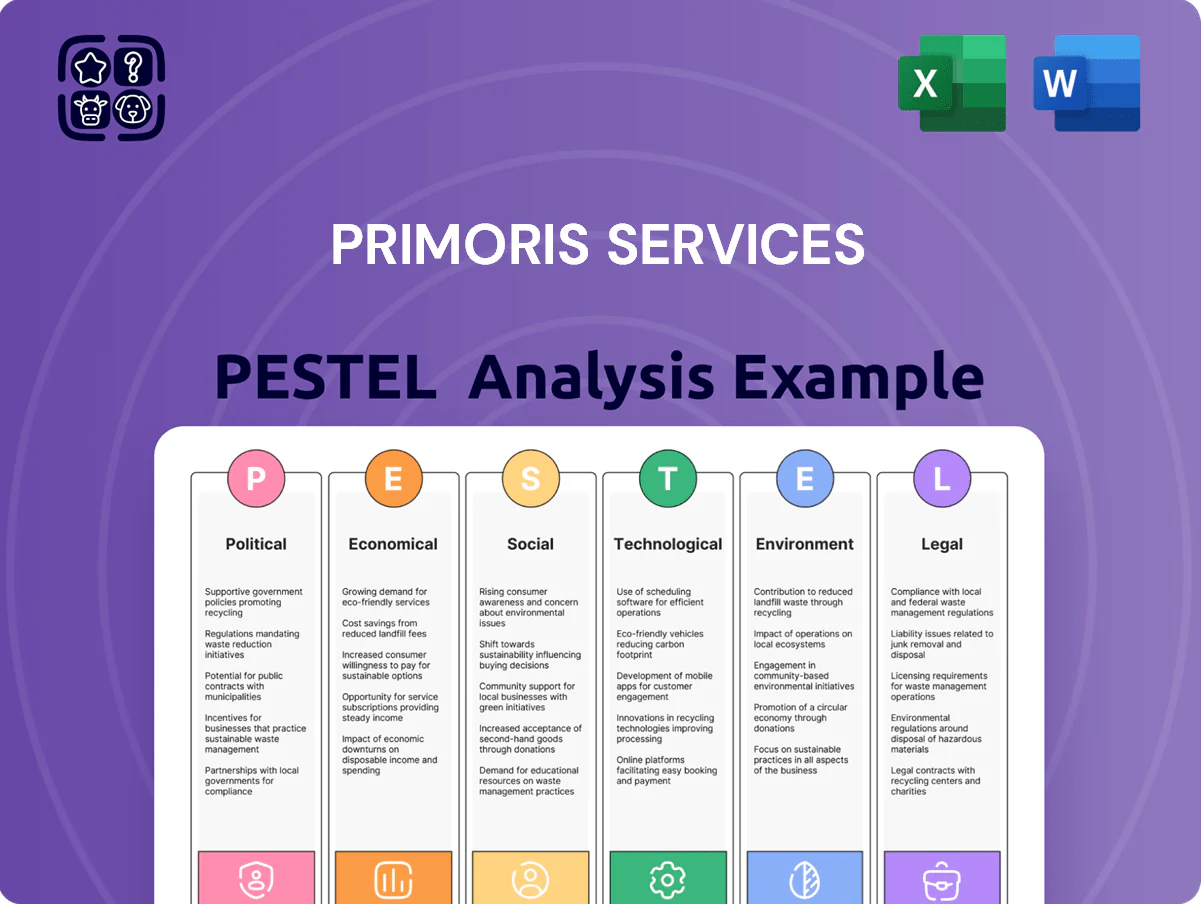

Explores how macro-environmental factors uniquely affect Primoris Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities.

Condenses Primoris Services' PESTLE into a clear, shareable brief—visually segmented by category for quick risk assessment, easy insertion into presentations, and editable notes to tailor insights to region, business line, or client needs.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, the Fed funds rate path remains pivotal for Primoris, as a 2024–25 average effective fed funds rate near 5.0–5.5% raises weighted average borrowing costs for capital projects, prompting some utilities to defer spend and pressuring Primoris’ book-to-bill; Moody’s recent data shows US utility capex growth slowed to ~1% in 2024. A sustained easing to ~4% would likely unlock deferred maintenance and new starts, boosting revenue visibility.

Inflationary Pressures on Material Costs

Fluctuations in steel and copper—steel up ~18% and copper ~23% in 2021–2023 volatility—directly pressure Primoris Services project margins via higher input costs for pipelines and power-grid components.

Primoris uses cost-plus and escalation clauses to mitigate risk, but persistent inflation through 2024–2025 erodes margins on fixed-price contracts, with gross margin variability seen in FY2024 quarterly reports.

Investors should assess Primoris’s pass-through ability; backlog composition and contract mix determine exposure, and management reported ~60% of 2024 revenue from contracts with some inflation protection.

Labor Market Tightness and Wage Growth

Labor market tightness in construction and engineering persists, with 2024 U.S. BLS data showing construction employment vacancies near record levels and median hourly wages up about 4.5% year-over-year; the skilled trades shortage raises recruiting and retention costs, contributing to margin pressure for Primoris Services. In 2024 Primoris reported rising labor costs impacting gross margins, so controlling labor productivity and personnel expenses is critical to preserve competitiveness.

North American Energy Demand Trends

North American GDP growth of ~2.1% in 2024 supports rising electricity and natural gas demand, directly increasing need for Primoris’s utility and pipeline services; US electric demand rose 0.8% in 2023 while natural gas consumption reached ~86 Bcf/day in 2024.

Data center capacity additions—hyperscale growth ~20% CAGR 2022–2025—plus electrification (EVs projected to hit 30 million US registrations by 2026) create localized grid-upgrade demand that benefits Primoris.

Expansion in high-tech manufacturing (reshoring incentives and >$200B in US semiconductor investments through 2026) generates specialized infrastructure projects aligned with Primoris’s capabilities.

- GDP ~2.1% (2024) → higher utility demand

- Electric demand +0.8% (2023); gas ~86 Bcf/day (2024)

- Hyperscale data center CAGR ~20% (2022–25)

- EVs ~30M US registrations by 2026

- Semiconductor investments >$200B through 2026

Currency Fluctuations and International Exposure

Currency swings between the Canadian dollar and US dollar materially affect Primoris valuation of Canadian operations; CAD fell about 6% vs USD in 2024, reducing translated revenues for US-centric reporting.

Regional US economic health—Gulf Coast energy investment and Southwest construction—drives localized infrastructure demand; Texas nonresidential construction rose ~4% YoY in 2024.

Diversification across North American regions helps mitigate localized downturns; Primoris's multi-region footprint reduced revenue volatility during 2023–2025 energy-cycle swings.

- CAD vs USD: −6% in 2024 impacting translated revenues

- Texas nonresidential construction: +4% YoY 2024

- Multi-region diversification reduces localized risk

High rates, input inflation and labor squeeze Primoris; easing rates could unlock projects

Higher 2024–25 fed funds (~5–5.5%) raised borrowing costs, slowing utility capex (~1% growth 2024) and pressuring Primoris’s book-to-bill; easing to ~4% would unlock deferred projects. Input-cost inflation (steel +18%, copper +23% through 2023) and tight labor (construction vacancies high; wages +4.5% YoY 2024) squeeze margins; ~60% 2024 revenue had inflation protection; CAD −6% vs USD 2024 reduced translated revenues.

| Metric | Value |

|---|---|

| Fed funds (avg 2024–25) | ~5–5.5% |

| US utility capex growth 2024 | ~1% |

| Steel / Copper change (2021–23) | +18% / +23% |

| Construction wages YoY 2024 | +4.5% |

| Primoris revenue w/ inflation protection 2024 | ~60% |

| CAD vs USD 2024 | −6% |

What You See Is What You Get

Primoris Services PESTLE Analysis

The preview shown here is the exact Primoris Services PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and environmental regulations are reshaping Primoris Services’ strategic outlook—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter decisions; purchase the full PESTLE for a complete, actionable briefing you can use immediately.

Political factors

Infrastructure Investment and Jobs Act (IIJA) Implementation

The IIJA’s remaining $550 billion in directed infrastructure funds, with significant disbursements continuing through 2025, sustains a project pipeline for Primoris in grid modernization and water works; Primoris reported $2.1 billion backlog at end-2024, tied partly to IIJA-related awards.

Energy Policy and Permitting Reform

Political debates over accelerating federal permitting affect Primoris Services’ ability to start large-scale pipeline and renewable projects; faster permitting could shorten project lead times from years to months, impacting revenue recognition—Primoris reported $2.1B revenue in 2024, so timing shifts materially affect cash flow.

Legislative moves to streamline NEPA remain critical; proposed reforms in 2024 aimed to cut review times by up to 50%, directly influencing Primoris’s project schedules and margin realization.

Post-2024 election shifts could reprioritize fossil fuel versus renewable permits, altering backlog composition—Primoris’s backlog and bidding strategy face policy-driven demand risk and opportunity depending on permit allocations.

Geopolitical Influence on Energy Security

Global instability has driven a political mandate for North American energy independence, boosting demand for Primoris’s oil and gas construction services; US oil production averaged 12.4 million b/d in 2024, underpinning pipeline projects.

Political backing for LNG export terminals remains strong—US LNG exports hit 14.6 Bcf/d in 2024—supporting long-term pipeline and terminal construction revenue streams for Primoris.

Security-focused policies ensure conventional infrastructure stays a priority during transition, preserving multi-year contracts and capital spending in midstream and terminal projects.

Federal Incentives for Renewable Energy

The longevity of IRA tax credits is crucial for Primoris Services’ solar and renewables backlog; the IRA extended investment and production tax credits through 2024–2032 tiers, supporting a US utility-scale solar pipeline expected to grow ~15% CAGR to 2026 per sector forecasts.

Political shifts risking repeal or phase-down of credits could cut project starts materially: recent analyses show a 20–35% drop in IRR for many projects if credits are reduced, slowing segment revenue growth.

Decision-makers should stress-test 2024–2026 growth scenarios assuming full, partial, or no credit availability and incorporate policy risk into cashflow and bid strategies.

- IRA credits underpin revenue visibility for Energy/Renewables through 2026

- Policy rollback could reduce project IRRs by 20–35%

- Forecasts should model multiple credit-stability scenarios

Governmental Labor and Trade Regulations

Political decisions on tariffs—tariffs on solar modules rose 10–25% in recent years—can raise Primoris’s project material costs and disrupt timelines tied to imported steel and PV components, affecting margins on contracts typically 5–12% EBITDA for construction segments.

Unionization pressure on federally funded projects shifts bidding strategy toward higher labor-cost offers; Davis-Bacon prevailing wage enforcement increases labor line items by an estimated 8–15% on large infrastructure jobs.

Changes in Department of Labor rules from 2021–2025 tightening overtime and classification have increased labor-related expenses, with some contractors reporting 3–7% rises in total project costs.

- Tariff volatility: +10–25% impacts on imported components

- Union/Davis-Bacon: +8–15% labor cost pressure

- DOL policy shifts: +3–7% overall project cost increases

Primoris rides $550B IIJA into 2025; permitting reform and IRA boost renewables

IIJA funds ($550B) sustain Primoris’s $2.1B backlog into 2025; NEPA/permitting reforms (2024) could cut review times ~50% altering revenue timing; IRA tax-credit stability through 2026 supports renewables (~15% CAGR to 2026); tariffs (+10–25%) and Davis‑Bacon (+8–15% labor) pressure margins (construction EBITDA 5–12%).

| Metric | Value/Impact |

|---|---|

| Backlog | $2.1B |

| IIJA funds | $550B |

| US oil prod. 2024 | 12.4M b/d |

| US LNG exports 2024 | 14.6 Bcf/d |

What is included in the product

Explores how macro-environmental factors uniquely affect Primoris Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify threats and opportunities.

Condenses Primoris Services' PESTLE into a clear, shareable brief—visually segmented by category for quick risk assessment, easy insertion into presentations, and editable notes to tailor insights to region, business line, or client needs.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, the Fed funds rate path remains pivotal for Primoris, as a 2024–25 average effective fed funds rate near 5.0–5.5% raises weighted average borrowing costs for capital projects, prompting some utilities to defer spend and pressuring Primoris’ book-to-bill; Moody’s recent data shows US utility capex growth slowed to ~1% in 2024. A sustained easing to ~4% would likely unlock deferred maintenance and new starts, boosting revenue visibility.

Inflationary Pressures on Material Costs

Fluctuations in steel and copper—steel up ~18% and copper ~23% in 2021–2023 volatility—directly pressure Primoris Services project margins via higher input costs for pipelines and power-grid components.

Primoris uses cost-plus and escalation clauses to mitigate risk, but persistent inflation through 2024–2025 erodes margins on fixed-price contracts, with gross margin variability seen in FY2024 quarterly reports.

Investors should assess Primoris’s pass-through ability; backlog composition and contract mix determine exposure, and management reported ~60% of 2024 revenue from contracts with some inflation protection.

Labor Market Tightness and Wage Growth

Labor market tightness in construction and engineering persists, with 2024 U.S. BLS data showing construction employment vacancies near record levels and median hourly wages up about 4.5% year-over-year; the skilled trades shortage raises recruiting and retention costs, contributing to margin pressure for Primoris Services. In 2024 Primoris reported rising labor costs impacting gross margins, so controlling labor productivity and personnel expenses is critical to preserve competitiveness.

North American Energy Demand Trends

North American GDP growth of ~2.1% in 2024 supports rising electricity and natural gas demand, directly increasing need for Primoris’s utility and pipeline services; US electric demand rose 0.8% in 2023 while natural gas consumption reached ~86 Bcf/day in 2024.

Data center capacity additions—hyperscale growth ~20% CAGR 2022–2025—plus electrification (EVs projected to hit 30 million US registrations by 2026) create localized grid-upgrade demand that benefits Primoris.

Expansion in high-tech manufacturing (reshoring incentives and >$200B in US semiconductor investments through 2026) generates specialized infrastructure projects aligned with Primoris’s capabilities.

- GDP ~2.1% (2024) → higher utility demand

- Electric demand +0.8% (2023); gas ~86 Bcf/day (2024)

- Hyperscale data center CAGR ~20% (2022–25)

- EVs ~30M US registrations by 2026

- Semiconductor investments >$200B through 2026

Currency Fluctuations and International Exposure

Currency swings between the Canadian dollar and US dollar materially affect Primoris valuation of Canadian operations; CAD fell about 6% vs USD in 2024, reducing translated revenues for US-centric reporting.

Regional US economic health—Gulf Coast energy investment and Southwest construction—drives localized infrastructure demand; Texas nonresidential construction rose ~4% YoY in 2024.

Diversification across North American regions helps mitigate localized downturns; Primoris's multi-region footprint reduced revenue volatility during 2023–2025 energy-cycle swings.

- CAD vs USD: −6% in 2024 impacting translated revenues

- Texas nonresidential construction: +4% YoY 2024

- Multi-region diversification reduces localized risk

High rates, input inflation and labor squeeze Primoris; easing rates could unlock projects

Higher 2024–25 fed funds (~5–5.5%) raised borrowing costs, slowing utility capex (~1% growth 2024) and pressuring Primoris’s book-to-bill; easing to ~4% would unlock deferred projects. Input-cost inflation (steel +18%, copper +23% through 2023) and tight labor (construction vacancies high; wages +4.5% YoY 2024) squeeze margins; ~60% 2024 revenue had inflation protection; CAD −6% vs USD 2024 reduced translated revenues.

| Metric | Value |

|---|---|

| Fed funds (avg 2024–25) | ~5–5.5% |

| US utility capex growth 2024 | ~1% |

| Steel / Copper change (2021–23) | +18% / +23% |

| Construction wages YoY 2024 | +4.5% |

| Primoris revenue w/ inflation protection 2024 | ~60% |

| CAD vs USD 2024 | −6% |

What You See Is What You Get

Primoris Services PESTLE Analysis

The preview shown here is the exact Primoris Services PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.