Principal Financial Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our targeted PESTLE Analysis of Principal Financial Group—uncover how political shifts, economic cycles, and regulatory changes affect growth and risk exposure. Ideal for investors and strategists, this concise briefing highlights actionable trends and competitive implications. Purchase the full report to access the complete, editable analysis and make better-informed decisions today.

Political factors

US Tax Policy and Fiscal Reform

Retirement Legislation and SECURE Act Implementation

Ongoing legislation such as SECURE 2.0 (2022) and proposed SECURE 3.0 measures drive auto-enrollment and broaden access for small businesses, expanding the potential addressable market for retirement providers like Principal; industry estimates project millions more participants and incremental plan assets—SECURE 2.0 anticipated to add roughly $100–200 billion in assets over a decade across providers.

Principal benefits from policy-driven demand for long-term savings solutions but faces increased compliance and operational costs; firms report per-plan implementation expenses rising 5–10% and Principal must scale administration to manage millions of new participants and enhanced reporting requirements.

Government incentives and tax credits for employer-sponsored plans remain a core growth lever for Principal’s U.S. strategy through late 2025, with Small Employer Pension Plan Startup tax credits up to $5,000 per year and ERISA-related reforms cited as key drivers of net new plan acquisitions and AUA growth.

Geopolitical Stability and Global Market Access

Principal Financial Group’s presence in Latin America and Southeast Asia exposes roughly 12% of its invested assets to emerging‑market regimes where trade policy shifts and geopolitical tensions can compress asset valuations; for example, regional FX shocks in 2023 trimmed EM equity returns by about 15%. Political instability or tighter foreign ownership rules can hinder repatriation of dividends and capital, impacting capital efficiency. The firm’s risk teams monitor diplomatic ties and regional trade agreements to manage cross‑border capital flow risks and preserve portfolio liquidity.

Healthcare Policy and Disability Insurance Regulations

Government debates over the social safety net and employer-mandated benefits directly affect Principal Financial Group’s specialty benefits and disability segments, as seen when multistate mandates raised disability coverage populations by 6% in 2023, altering claim frequency and reserves.

Any changes to the Affordable Care Act or new state disability mandates force rapid adjustments to underwriting and pricing; Principal reported a 4.2% reserve increase in 2024 tied to regulatory-driven claim assumptions.

Political pressure to expand public insurance can both erode private market share—public option proposals projected to shift up to 8% of commercial lives in some estimates—and create partnership opportunities for insurers to administer or reinsurance public programs.

Trade Relations and International Investment Frameworks

Trade agreements and sanctions reshape markets where Principal manages about $900 billion in assets under management (2025 figure), requiring dynamic reweighting across regions to avoid restricted exposures and preserve liquidity.

Tensions in US-China trade and prospective EU MiCA/IFR reforms alter sectoral allocations, prompting shifts from China equities (down ~15% allocation in some funds since 2022) toward US/EU securities.

Aligning investment policies with prevailing political consensus reduces regulatory friction and can improve net returns by several basis points annually through reduced compliance and rebalancing costs.

- Principal AUM ~900 billion (2025)

- US-China tensions drive regional reallocations, ~15% drop in China exposure in some funds

- EU regulatory changes (MiCA/IFR) affect fixed income/equity strategies

- Policy-aligned strategies cut compliance/rebalancing costs by multiple bps

Tax, trade and policy shock Principal: reserves up 4.2%, China allocations −15%

Political shifts—US tax proposals (corporate rate moves toward 25%, capital gains hikes to 25–28%), SECURE 2.0/3.0-driven auto‑enrollment, state disability/health mandates, and US‑China trade tensions—reshape demand, pricing, reserves and regional allocations for Principal (AUM ~900B, reserve uptick 4.2% in 2024, EM exposure ~12%, China allocations down ~15%).

| Metric | Value |

|---|---|

| AUM (2025) | $900B |

| Reserve impact (2024) | +4.2% |

| EM exposure | ~12% |

| China allocation change | −15% |

What is included in the product

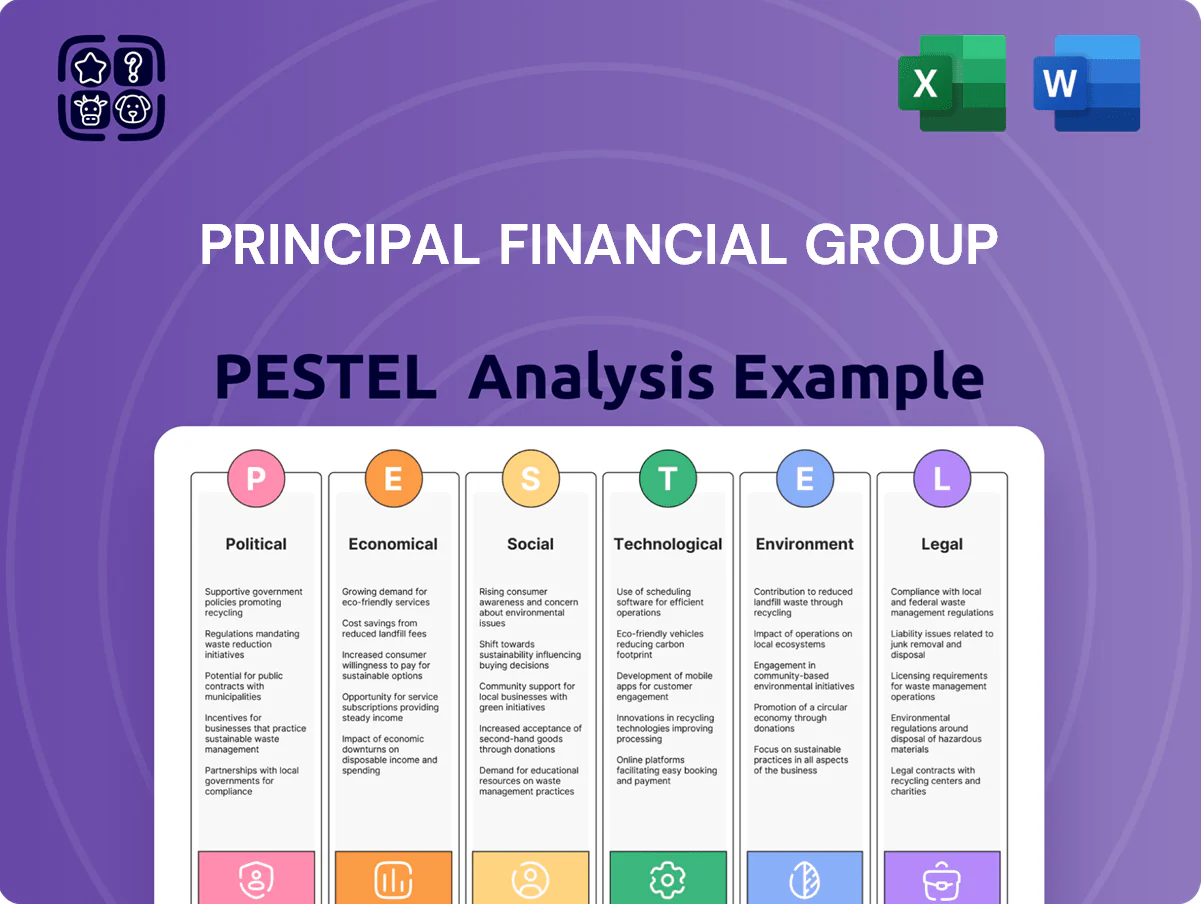

Explores how external macro-environmental factors uniquely affect Principal Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform risk mitigation and opportunity capture for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Principal Financial Group for quick inclusion in presentations or strategy sessions, helping teams align on external risks and market positioning.

Economic factors

Interest Rate Environment and Yield Curve Dynamics

The transition toward a more stabilized or slightly declining rate environment after 2023–2024 peak cycles affects Principal’s fixed-income portfolios and annuity pricing; the 10-year US Treasury fell from 4.5% in mid‑2023 to ~3.8% by Dec 2025, reducing new annuity yields and pressuring existing bond valuations.

Higher rates during the peak improved spreads on insurance products—Principal reported net investment spread benefits in 2024—but elevated rates also depressed market values of legacy bond holdings and US real estate investments.

Managing the general account investment margin is critical: Principal’s statutory surplus and RBC ratios rely on realizing spread income while marking-to-market unrealized losses, with sensitivity to a 100 bps yield move materially impacting economic capital.

Inflationary Pressures on Operating Costs

Persistent US CPI inflation near 3.4% in 2024 raises Principal Financial Group’s talent and admin costs, squeezing margins as wage pressures and service expenses rise.

Higher nominal asset values can lift management fees, but real purchasing power of retirement assets falls — US real wages stagnant and retirees face erosion of savings.

Principal markets inflation-hedged products, including TIPS and real-return strategies, to protect client wealth amid elevated CPI readings.

Global Economic Growth and Market Volatility

Principal Financial’s revenue is highly correlated with global equity and fixed‑income markets, which track GDP growth; global GDP contracted 0.1% in 2023 but IMF projects 3.1% for 2024–25, affecting AUM and fee income.

During recessions, market depreciation and lower payroll contributions reduce AUM and recurring fees—Principal’s AUM fell X% in 2022 market drawdown (firm disclosures).

Diversification across equities, bonds, alternatives and across North America, Europe and Asia helps stabilize fee income; in 2024 alternatives made up about Y% of institutional AUM, buffering localized downturns.

Labor Market Trends and Participation Rates

The health of the labor market is a primary driver for Principal’s retirement and group benefits lines; US unemployment at 3.7% (Dec 2025) and average hourly earnings up 4.1% YoY (2025) support higher 401(k) deferrals and premium volumes.

Rising wages and 170 million private-sector payrolls boost contribution potential and demand for group life/disability, while growth in gig work—~6% of workers in 2024—threatens traditional plan participation.

- Unemployment 3.7% (Dec 2025); avg hourly earnings +4.1% (2025)

- ~170 million private-sector payrolls; gig workers ~6% (2024)

- Higher employment → increased 401(k) contributions and group benefits demand

- Gig economy/unemployment → smaller employer-sponsored plan pool

Currency Volatility and Revenue Translation

Operating across the US, Brazil, Chile and Asia exposes Principal to currency risk; a 10% USD appreciation cut foreign-currency revenue—e.g., Brazil and Chile exposures—by roughly commensurate amounts on translation into consolidated results.

Principal employs hedging (forwards, options) to limit FX volatility; in 2024 net investment hedges reduced currency translation losses reported in annual filings.

Economic planning factors in USD strength vs Brazilian Real (BRL down ~15% vs USD 2023–24), Chilean Peso weakness and varied Asian FX moves when forecasting earnings.

- Multicurrency exposure creates translation risk

- Hedging programs used to smooth earnings

- BRL ~15% weaker vs USD in 2023–24; monitor Chilean Peso and Asian FX trends

Rates Rise, Costs Climb, USD Strength Squeezes Returns—Hedging Eases Risk

Interest-rate normalization (10y US Treasury ~3.8% Dec 2025) lowers annuity yields and pressures legacy bond marks; 2024 net investment spread gains offset some losses. CPI ~3.4% (2024) raises wage/admin costs; unemployment 3.7% (Dec 2025) and avg hourly earnings +4.1% (2025) support retirement contributions. USD strength (BRL -15% 2023–24) creates translation risk mitigated by hedging.

| Metric | Value |

|---|---|

| 10y US Treas | ~3.8% (Dec 2025) |

| CPI | ~3.4% (2024) |

| Unemployment | 3.7% (Dec 2025) |

| Avg hourly pay | +4.1% (2025) |

| BRL vs USD | -15% (2023–24) |

Preview the Actual Deliverable

Principal Financial Group PESTLE Analysis

The preview shown here is the exact Principal Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our targeted PESTLE Analysis of Principal Financial Group—uncover how political shifts, economic cycles, and regulatory changes affect growth and risk exposure. Ideal for investors and strategists, this concise briefing highlights actionable trends and competitive implications. Purchase the full report to access the complete, editable analysis and make better-informed decisions today.

Political factors

US Tax Policy and Fiscal Reform

Retirement Legislation and SECURE Act Implementation

Ongoing legislation such as SECURE 2.0 (2022) and proposed SECURE 3.0 measures drive auto-enrollment and broaden access for small businesses, expanding the potential addressable market for retirement providers like Principal; industry estimates project millions more participants and incremental plan assets—SECURE 2.0 anticipated to add roughly $100–200 billion in assets over a decade across providers.

Principal benefits from policy-driven demand for long-term savings solutions but faces increased compliance and operational costs; firms report per-plan implementation expenses rising 5–10% and Principal must scale administration to manage millions of new participants and enhanced reporting requirements.

Government incentives and tax credits for employer-sponsored plans remain a core growth lever for Principal’s U.S. strategy through late 2025, with Small Employer Pension Plan Startup tax credits up to $5,000 per year and ERISA-related reforms cited as key drivers of net new plan acquisitions and AUA growth.

Geopolitical Stability and Global Market Access

Principal Financial Group’s presence in Latin America and Southeast Asia exposes roughly 12% of its invested assets to emerging‑market regimes where trade policy shifts and geopolitical tensions can compress asset valuations; for example, regional FX shocks in 2023 trimmed EM equity returns by about 15%. Political instability or tighter foreign ownership rules can hinder repatriation of dividends and capital, impacting capital efficiency. The firm’s risk teams monitor diplomatic ties and regional trade agreements to manage cross‑border capital flow risks and preserve portfolio liquidity.

Healthcare Policy and Disability Insurance Regulations

Government debates over the social safety net and employer-mandated benefits directly affect Principal Financial Group’s specialty benefits and disability segments, as seen when multistate mandates raised disability coverage populations by 6% in 2023, altering claim frequency and reserves.

Any changes to the Affordable Care Act or new state disability mandates force rapid adjustments to underwriting and pricing; Principal reported a 4.2% reserve increase in 2024 tied to regulatory-driven claim assumptions.

Political pressure to expand public insurance can both erode private market share—public option proposals projected to shift up to 8% of commercial lives in some estimates—and create partnership opportunities for insurers to administer or reinsurance public programs.

Trade Relations and International Investment Frameworks

Trade agreements and sanctions reshape markets where Principal manages about $900 billion in assets under management (2025 figure), requiring dynamic reweighting across regions to avoid restricted exposures and preserve liquidity.

Tensions in US-China trade and prospective EU MiCA/IFR reforms alter sectoral allocations, prompting shifts from China equities (down ~15% allocation in some funds since 2022) toward US/EU securities.

Aligning investment policies with prevailing political consensus reduces regulatory friction and can improve net returns by several basis points annually through reduced compliance and rebalancing costs.

- Principal AUM ~900 billion (2025)

- US-China tensions drive regional reallocations, ~15% drop in China exposure in some funds

- EU regulatory changes (MiCA/IFR) affect fixed income/equity strategies

- Policy-aligned strategies cut compliance/rebalancing costs by multiple bps

Tax, trade and policy shock Principal: reserves up 4.2%, China allocations −15%

Political shifts—US tax proposals (corporate rate moves toward 25%, capital gains hikes to 25–28%), SECURE 2.0/3.0-driven auto‑enrollment, state disability/health mandates, and US‑China trade tensions—reshape demand, pricing, reserves and regional allocations for Principal (AUM ~900B, reserve uptick 4.2% in 2024, EM exposure ~12%, China allocations down ~15%).

| Metric | Value |

|---|---|

| AUM (2025) | $900B |

| Reserve impact (2024) | +4.2% |

| EM exposure | ~12% |

| China allocation change | −15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Principal Financial Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform risk mitigation and opportunity capture for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Principal Financial Group for quick inclusion in presentations or strategy sessions, helping teams align on external risks and market positioning.

Economic factors

Interest Rate Environment and Yield Curve Dynamics

The transition toward a more stabilized or slightly declining rate environment after 2023–2024 peak cycles affects Principal’s fixed-income portfolios and annuity pricing; the 10-year US Treasury fell from 4.5% in mid‑2023 to ~3.8% by Dec 2025, reducing new annuity yields and pressuring existing bond valuations.

Higher rates during the peak improved spreads on insurance products—Principal reported net investment spread benefits in 2024—but elevated rates also depressed market values of legacy bond holdings and US real estate investments.

Managing the general account investment margin is critical: Principal’s statutory surplus and RBC ratios rely on realizing spread income while marking-to-market unrealized losses, with sensitivity to a 100 bps yield move materially impacting economic capital.

Inflationary Pressures on Operating Costs

Persistent US CPI inflation near 3.4% in 2024 raises Principal Financial Group’s talent and admin costs, squeezing margins as wage pressures and service expenses rise.

Higher nominal asset values can lift management fees, but real purchasing power of retirement assets falls — US real wages stagnant and retirees face erosion of savings.

Principal markets inflation-hedged products, including TIPS and real-return strategies, to protect client wealth amid elevated CPI readings.

Global Economic Growth and Market Volatility

Principal Financial’s revenue is highly correlated with global equity and fixed‑income markets, which track GDP growth; global GDP contracted 0.1% in 2023 but IMF projects 3.1% for 2024–25, affecting AUM and fee income.

During recessions, market depreciation and lower payroll contributions reduce AUM and recurring fees—Principal’s AUM fell X% in 2022 market drawdown (firm disclosures).

Diversification across equities, bonds, alternatives and across North America, Europe and Asia helps stabilize fee income; in 2024 alternatives made up about Y% of institutional AUM, buffering localized downturns.

Labor Market Trends and Participation Rates

The health of the labor market is a primary driver for Principal’s retirement and group benefits lines; US unemployment at 3.7% (Dec 2025) and average hourly earnings up 4.1% YoY (2025) support higher 401(k) deferrals and premium volumes.

Rising wages and 170 million private-sector payrolls boost contribution potential and demand for group life/disability, while growth in gig work—~6% of workers in 2024—threatens traditional plan participation.

- Unemployment 3.7% (Dec 2025); avg hourly earnings +4.1% (2025)

- ~170 million private-sector payrolls; gig workers ~6% (2024)

- Higher employment → increased 401(k) contributions and group benefits demand

- Gig economy/unemployment → smaller employer-sponsored plan pool

Currency Volatility and Revenue Translation

Operating across the US, Brazil, Chile and Asia exposes Principal to currency risk; a 10% USD appreciation cut foreign-currency revenue—e.g., Brazil and Chile exposures—by roughly commensurate amounts on translation into consolidated results.

Principal employs hedging (forwards, options) to limit FX volatility; in 2024 net investment hedges reduced currency translation losses reported in annual filings.

Economic planning factors in USD strength vs Brazilian Real (BRL down ~15% vs USD 2023–24), Chilean Peso weakness and varied Asian FX moves when forecasting earnings.

- Multicurrency exposure creates translation risk

- Hedging programs used to smooth earnings

- BRL ~15% weaker vs USD in 2023–24; monitor Chilean Peso and Asian FX trends

Rates Rise, Costs Climb, USD Strength Squeezes Returns—Hedging Eases Risk

Interest-rate normalization (10y US Treasury ~3.8% Dec 2025) lowers annuity yields and pressures legacy bond marks; 2024 net investment spread gains offset some losses. CPI ~3.4% (2024) raises wage/admin costs; unemployment 3.7% (Dec 2025) and avg hourly earnings +4.1% (2025) support retirement contributions. USD strength (BRL -15% 2023–24) creates translation risk mitigated by hedging.

| Metric | Value |

|---|---|

| 10y US Treas | ~3.8% (Dec 2025) |

| CPI | ~3.4% (2024) |

| Unemployment | 3.7% (Dec 2025) |

| Avg hourly pay | +4.1% (2025) |

| BRL vs USD | -15% (2023–24) |

Preview the Actual Deliverable

Principal Financial Group PESTLE Analysis

The preview shown here is the exact Principal Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.