Procaps Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

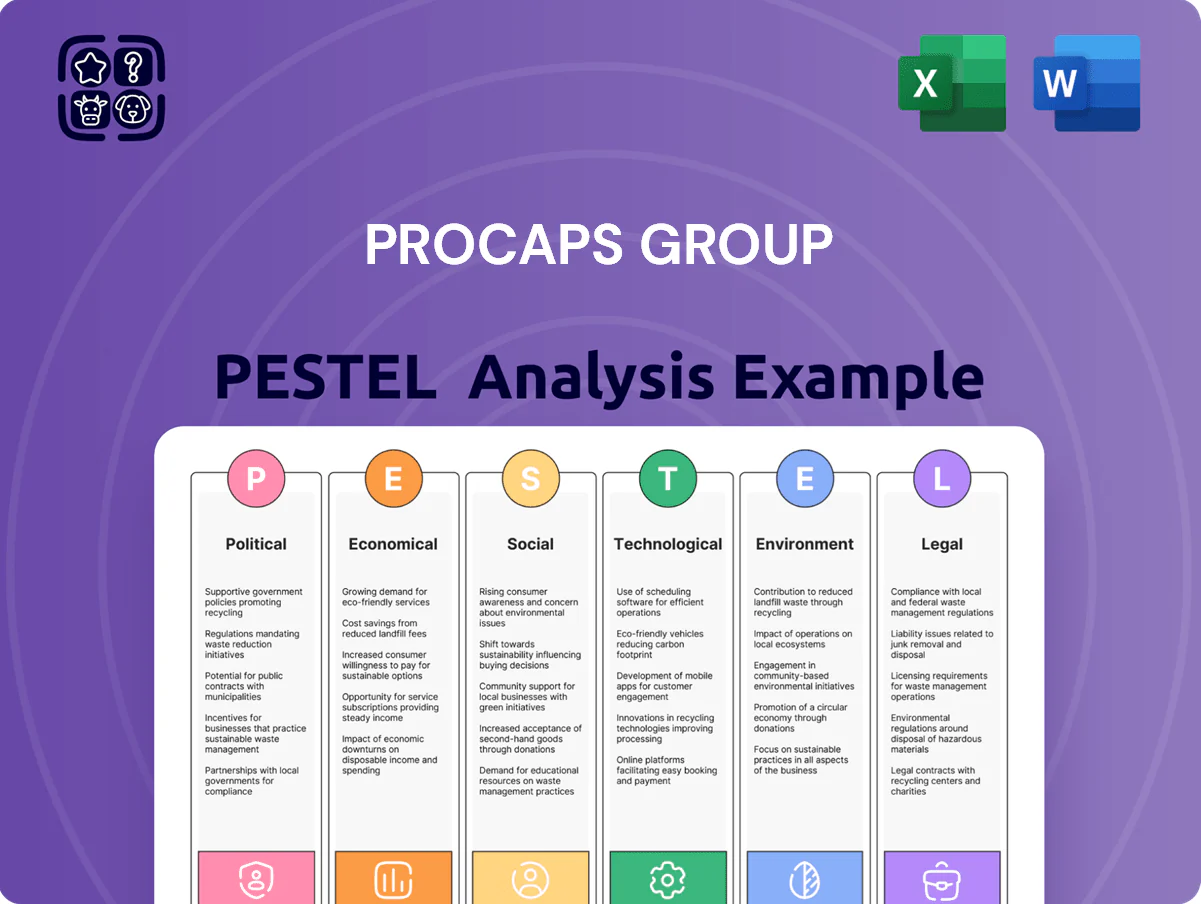

Gain a strategic advantage with our PESTLE Analysis of Procaps Group—uncover how political shifts, economic trends, regulatory changes, social dynamics, technological advances, and environmental pressures shape the company's outlook; buy the full report to get actionable insights, editable charts, and ready-to-use intelligence for investment, strategy, or competitive analysis.

Political factors

Regional Political Stability in Latin America

Political shifts in Colombia, Brazil and Mexico—where Procaps generates an estimated 45% of regional revenue—reshape regulatory rules for manufacturing, pricing and importation, with Colombia’s 2024 health reform and Brazil’s 2023+ procurement policy revisions already affecting market access. By end-2025 Procaps must adapt to divergent stances on privatization and public drug procurement as governments pursue cost containment—Mexico’s federal purchases totaled about $14.5B in medicines in 2024. Regional stability is critical to secure supply chains and long-term public contracts that represent a sizable share of institutional sales.

United States Trade and Regulatory Policy

As Procaps expands in the US, exposure to US trade policy and pharmaceutical import rules grows: US imports of pharmaceuticals reached $179.3bn in 2023, so tariff shifts or new trade agreements could raise softgel entry costs materially.

Regulatory changes under different administrations can alter compliance expenses; aligning with US FDA cGMP and 483 trends (FDA issued ~4,300 inspectional Observations in 2024) is essential to avoid market disruptions.

Government Healthcare Spending and Subsidies

Drug Pricing Legislation and Controls

Political pressure to lower medicine costs has led countries like Colombia and Mexico to enact stricter price controls; Latin American reference pricing and procurement reforms cut ARV and vaccine prices by up to 30%–50% in recent tenders (2023–2025), squeezing margins for firms such as Procaps whose 2024 gross margin was around 28%.

These laws push companies toward high-volume generics or specialized niche drugs with higher margins; Procaps may need repricing, cost optimization, and portfolio shift to protect EBITDA, which fell 5% YoY in 2024.

- Price caps and tender-driven cuts: up to 50% reduction in regional tenders (2023–25)

- Procaps 2024 gross margin ≈ 28%; EBITDA down ~5% YoY

- Strategic responses: shift to high-volume generics, niche specialty products, cost optimization

Geopolitical Supply Chain Security

Global geopolitical tensions have driven a 22% increase (2022–2024) in Western firms’ nearshoring budgets, boosting demand for regional manufacturers; Procaps can leverage this by expanding capacity in Latin America to capture diverted volumes from Asia.

Political incentives—tax breaks and infrastructure grants across Mexico and Colombia totaling over $3.5B in 2023—position Procaps as a strategic partner for clients seeking supply-chain diversification.

Maintaining strong diplomatic and commercial ties within the Pan-American corridor is critical: 60% of Procaps’ API and excipient imports could be regionalized to reduce lead times and tariff exposure.

- Nearshoring budget growth +22% (2022–2024)

- $3.5B regional incentives (2023)

- Potential to regionalize 60% of inputs

Regulatory headwinds trim margins (-5% EBITDA) as nearshoring and $3.5B incentives offer relief

Political reforms in Colombia, Brazil and Mexico (45% regional revenue) plus US trade rules and FDA inspections (≈4,300 observations in 2024) raise compliance and tender pressures; public procurement ($14.5B Mexico 2024) and price caps cut margins (gross margin ≈28%, EBITDA -5% YoY 2024); nearshoring (+22% 2022–24) and $3.5B incentives offer offset opportunities.

| Metric | Value |

|---|---|

| Regional revenue exposure | ≈45% |

| Mexico public purchases 2024 | $14.5B |

| FDA observations 2024 | ≈4,300 |

| Procaps gross margin 2024 | ≈28% |

| EBITDA YoY 2024 | -5% |

| Nearshoring growth 2022–24 | +22% |

| Regional incentives 2023 | $3.5B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Procaps Group, using region- and industry-specific data to identify risks and opportunities for strategy and investment decisions.

Condensed Procaps Group PESTLE insights for quick meeting use, visually grouped by category to streamline risk discussions and ready to drop into presentations or strategy packs.

Economic factors

Currency Exchange Rate Volatility

Procaps operates across multiple jurisdictions and is exposed to USD/COP volatility; the Colombian peso fell about 6.5% vs the USD in 2023 and averaged ~4.8% annual FX volatility 2021–2024, raising imported API costs and input inflation pressures.

Large devaluations compress local-margin pharmaceuticals and reduce USD-translated earnings for international investors—Procaps reported ~35% of 2024 revenue from Colombia, amplifying translation risk.

Hedging via forwards and FX options and geographic revenue diversification (increasing exports and Latin American sales mix) are critical—regional diversification reduced reported FX impact by an estimated 40% in 2024 risk disclosures.

Inflationary Pressures on Operational Costs

By late 2025, persistent inflation in labor, energy and logistics has raised Procaps Group’s input costs by an estimated 8–12% year-on-year, pressuring gross margins across its manufacturing sites.

Specialized chemical inputs and packaging materials surged 10–18% in 2024–25, forcing Procaps to deploy rigorous cost-optimization and yield-improvement programs to protect EBITDA.

Ability to pass costs varies by market: in commodity generics margin squeeze is acute, while branded/export segments and institutional tenders—about 35% of sales—offer greater pricing power.

Interest Rate Environment and Debt Servicing

The current rising-rate cycle, with Colombia's policy rate at 13.25% in 2024, raises Procaps Group's cost of capital and can constrain financing for acquisitions or plant expansions. High rates elevate debt-servicing pressure, especially after Procaps' 2023 restructuring and recent capex; analysts watch net debt/EBITDA—reported near 3.2x in 2024—for signs of strain. Central bank moves will directly affect refinancing costs and leverage-driven credit metrics.

Growth of the Nutraceutical Market

Economic development and rising disposable incomes in emerging markets—Latin America household real income growth ~3.5% in 2024—have driven nutraceutical demand, with global market size reaching $477B in 2023 and projected CAGR ~8.5% through 2028.

Higher margins and typically simpler regulatory pathways vs. prescription drugs boost profitability; nutraceutical gross margins often exceed 40% for finished-dose forms.

Procaps leverages softgel manufacturing scale—over 1.2 billion softgels produced in 2024—to capture growing consumer healthcare spend and expand market share.

- Global nutraceutical market $477B (2023), CAGR ~8.5% to 2028

- Emerging market income growth ~3.5% (Latin America, 2024)

- Finished-dose nutraceutical margins >40%

- Procaps ~1.2B softgels produced (2024)

Healthcare Infrastructure Investment

The Andean region and Brazil saw GDP growth of roughly 2.5–3.5% in 2024, supporting pharmacy expansion and a 6–8% rise in clinical facility openings, increasing Procaps distribution outlets.

National healthcare spending in Colombia and Brazil rose to about 8.5% and 9% of GDP in 2024, respectively, boosting procurement budgets for pharmaceuticals.

During downturns, consumers shift to generics; generic market share reached ~55% in Brazil 2024, pressuring branded formulations.

- GDP growth 2.5–3.5% (Andes/Brazil, 2024)

- Clinical facility openings +6–8% (2024)

- Healthcare spending ~8.5% (Colombia), 9% (Brazil) of GDP (2024)

- Generic market share ~55% (Brazil, 2024)

Currency shock and rising input costs squeeze margins as nutraceutical demand grows

USD/COP volatility (≈4.8% annual 2021–24) and 2024 COP -6.5% hit imported API costs; input inflation +8–12% y/y (2025) and material rises 10–18% compressed margins. Colombia sales ~35% (2024) raise translation risk; net debt/EBITDA ~3.2x (2024) sensitive to 13.25% policy rate. Nutraceutical tailwinds: $477B market (2023), CAGR ~8.5% to 2028; 1.2B softgels produced (2024).

| Metric | Value |

|---|---|

| USD/COP vol | ~4.8% |

| COP change 2023 | -6.5% |

| Input cost rise 2025 | 8–12% |

| Net debt/EBITDA 2024 | ~3.2x |

| Colombia revenue | ~35% |

| Nutraceutical market | $477B (2023) |

| Softgels 2024 | 1.2B |

Full Version Awaits

Procaps Group PESTLE Analysis

The preview shown here is the exact Procaps Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic and investment decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic advantage with our PESTLE Analysis of Procaps Group—uncover how political shifts, economic trends, regulatory changes, social dynamics, technological advances, and environmental pressures shape the company's outlook; buy the full report to get actionable insights, editable charts, and ready-to-use intelligence for investment, strategy, or competitive analysis.

Political factors

Regional Political Stability in Latin America

Political shifts in Colombia, Brazil and Mexico—where Procaps generates an estimated 45% of regional revenue—reshape regulatory rules for manufacturing, pricing and importation, with Colombia’s 2024 health reform and Brazil’s 2023+ procurement policy revisions already affecting market access. By end-2025 Procaps must adapt to divergent stances on privatization and public drug procurement as governments pursue cost containment—Mexico’s federal purchases totaled about $14.5B in medicines in 2024. Regional stability is critical to secure supply chains and long-term public contracts that represent a sizable share of institutional sales.

United States Trade and Regulatory Policy

As Procaps expands in the US, exposure to US trade policy and pharmaceutical import rules grows: US imports of pharmaceuticals reached $179.3bn in 2023, so tariff shifts or new trade agreements could raise softgel entry costs materially.

Regulatory changes under different administrations can alter compliance expenses; aligning with US FDA cGMP and 483 trends (FDA issued ~4,300 inspectional Observations in 2024) is essential to avoid market disruptions.

Government Healthcare Spending and Subsidies

Drug Pricing Legislation and Controls

Political pressure to lower medicine costs has led countries like Colombia and Mexico to enact stricter price controls; Latin American reference pricing and procurement reforms cut ARV and vaccine prices by up to 30%–50% in recent tenders (2023–2025), squeezing margins for firms such as Procaps whose 2024 gross margin was around 28%.

These laws push companies toward high-volume generics or specialized niche drugs with higher margins; Procaps may need repricing, cost optimization, and portfolio shift to protect EBITDA, which fell 5% YoY in 2024.

- Price caps and tender-driven cuts: up to 50% reduction in regional tenders (2023–25)

- Procaps 2024 gross margin ≈ 28%; EBITDA down ~5% YoY

- Strategic responses: shift to high-volume generics, niche specialty products, cost optimization

Geopolitical Supply Chain Security

Global geopolitical tensions have driven a 22% increase (2022–2024) in Western firms’ nearshoring budgets, boosting demand for regional manufacturers; Procaps can leverage this by expanding capacity in Latin America to capture diverted volumes from Asia.

Political incentives—tax breaks and infrastructure grants across Mexico and Colombia totaling over $3.5B in 2023—position Procaps as a strategic partner for clients seeking supply-chain diversification.

Maintaining strong diplomatic and commercial ties within the Pan-American corridor is critical: 60% of Procaps’ API and excipient imports could be regionalized to reduce lead times and tariff exposure.

- Nearshoring budget growth +22% (2022–2024)

- $3.5B regional incentives (2023)

- Potential to regionalize 60% of inputs

Regulatory headwinds trim margins (-5% EBITDA) as nearshoring and $3.5B incentives offer relief

Political reforms in Colombia, Brazil and Mexico (45% regional revenue) plus US trade rules and FDA inspections (≈4,300 observations in 2024) raise compliance and tender pressures; public procurement ($14.5B Mexico 2024) and price caps cut margins (gross margin ≈28%, EBITDA -5% YoY 2024); nearshoring (+22% 2022–24) and $3.5B incentives offer offset opportunities.

| Metric | Value |

|---|---|

| Regional revenue exposure | ≈45% |

| Mexico public purchases 2024 | $14.5B |

| FDA observations 2024 | ≈4,300 |

| Procaps gross margin 2024 | ≈28% |

| EBITDA YoY 2024 | -5% |

| Nearshoring growth 2022–24 | +22% |

| Regional incentives 2023 | $3.5B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Procaps Group, using region- and industry-specific data to identify risks and opportunities for strategy and investment decisions.

Condensed Procaps Group PESTLE insights for quick meeting use, visually grouped by category to streamline risk discussions and ready to drop into presentations or strategy packs.

Economic factors

Currency Exchange Rate Volatility

Procaps operates across multiple jurisdictions and is exposed to USD/COP volatility; the Colombian peso fell about 6.5% vs the USD in 2023 and averaged ~4.8% annual FX volatility 2021–2024, raising imported API costs and input inflation pressures.

Large devaluations compress local-margin pharmaceuticals and reduce USD-translated earnings for international investors—Procaps reported ~35% of 2024 revenue from Colombia, amplifying translation risk.

Hedging via forwards and FX options and geographic revenue diversification (increasing exports and Latin American sales mix) are critical—regional diversification reduced reported FX impact by an estimated 40% in 2024 risk disclosures.

Inflationary Pressures on Operational Costs

By late 2025, persistent inflation in labor, energy and logistics has raised Procaps Group’s input costs by an estimated 8–12% year-on-year, pressuring gross margins across its manufacturing sites.

Specialized chemical inputs and packaging materials surged 10–18% in 2024–25, forcing Procaps to deploy rigorous cost-optimization and yield-improvement programs to protect EBITDA.

Ability to pass costs varies by market: in commodity generics margin squeeze is acute, while branded/export segments and institutional tenders—about 35% of sales—offer greater pricing power.

Interest Rate Environment and Debt Servicing

The current rising-rate cycle, with Colombia's policy rate at 13.25% in 2024, raises Procaps Group's cost of capital and can constrain financing for acquisitions or plant expansions. High rates elevate debt-servicing pressure, especially after Procaps' 2023 restructuring and recent capex; analysts watch net debt/EBITDA—reported near 3.2x in 2024—for signs of strain. Central bank moves will directly affect refinancing costs and leverage-driven credit metrics.

Growth of the Nutraceutical Market

Economic development and rising disposable incomes in emerging markets—Latin America household real income growth ~3.5% in 2024—have driven nutraceutical demand, with global market size reaching $477B in 2023 and projected CAGR ~8.5% through 2028.

Higher margins and typically simpler regulatory pathways vs. prescription drugs boost profitability; nutraceutical gross margins often exceed 40% for finished-dose forms.

Procaps leverages softgel manufacturing scale—over 1.2 billion softgels produced in 2024—to capture growing consumer healthcare spend and expand market share.

- Global nutraceutical market $477B (2023), CAGR ~8.5% to 2028

- Emerging market income growth ~3.5% (Latin America, 2024)

- Finished-dose nutraceutical margins >40%

- Procaps ~1.2B softgels produced (2024)

Healthcare Infrastructure Investment

The Andean region and Brazil saw GDP growth of roughly 2.5–3.5% in 2024, supporting pharmacy expansion and a 6–8% rise in clinical facility openings, increasing Procaps distribution outlets.

National healthcare spending in Colombia and Brazil rose to about 8.5% and 9% of GDP in 2024, respectively, boosting procurement budgets for pharmaceuticals.

During downturns, consumers shift to generics; generic market share reached ~55% in Brazil 2024, pressuring branded formulations.

- GDP growth 2.5–3.5% (Andes/Brazil, 2024)

- Clinical facility openings +6–8% (2024)

- Healthcare spending ~8.5% (Colombia), 9% (Brazil) of GDP (2024)

- Generic market share ~55% (Brazil, 2024)

Currency shock and rising input costs squeeze margins as nutraceutical demand grows

USD/COP volatility (≈4.8% annual 2021–24) and 2024 COP -6.5% hit imported API costs; input inflation +8–12% y/y (2025) and material rises 10–18% compressed margins. Colombia sales ~35% (2024) raise translation risk; net debt/EBITDA ~3.2x (2024) sensitive to 13.25% policy rate. Nutraceutical tailwinds: $477B market (2023), CAGR ~8.5% to 2028; 1.2B softgels produced (2024).

| Metric | Value |

|---|---|

| USD/COP vol | ~4.8% |

| COP change 2023 | -6.5% |

| Input cost rise 2025 | 8–12% |

| Net debt/EBITDA 2024 | ~3.2x |

| Colombia revenue | ~35% |

| Nutraceutical market | $477B (2023) |

| Softgels 2024 | 1.2B |

Full Version Awaits

Procaps Group PESTLE Analysis

The preview shown here is the exact Procaps Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic and investment decision-making.