Procore Porter's Five Forces Analysis

Don't Miss the Bigger Picture

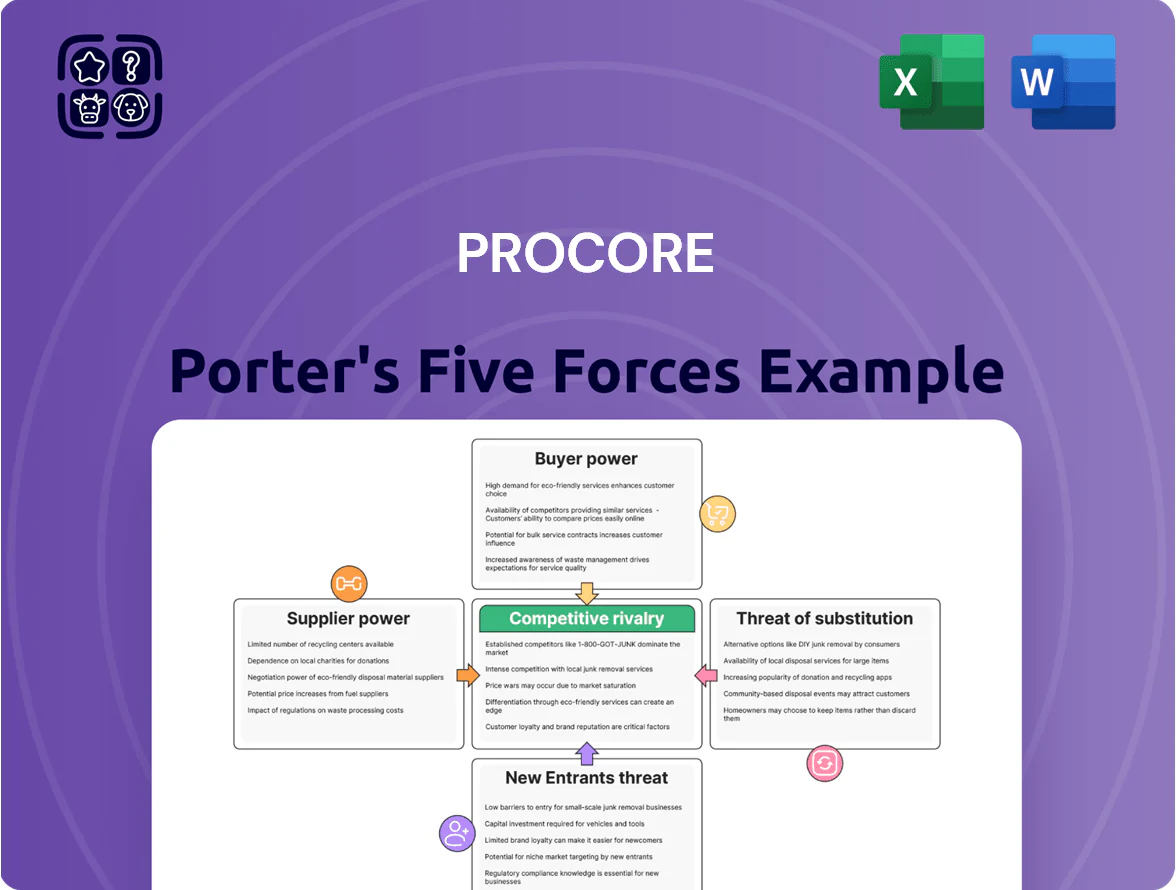

Procore faces moderate rivalry from established construction software vendors, rising buyer power as customers demand integrated workflows, and supplier/partner dynamics that shape platform expansion; barriers to entry remain significant but evolving with cloud-native tools and niche vertical entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Procore’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Hyperscale Cloud Infrastructure Providers

Procore relies heavily on hyperscale clouds—primarily Amazon Web Services—for hosting its platform and data; AWS held ~32% global IaaS market share in 2025, concentrating supplier power.

This concentration lets providers influence pricing and SLAs; cloud costs can be 15–25% of SaaS COGS for large platforms, squeezing margins if rates rise.

Although Procore can refactor to optimize usage, estimated migration costs and technical debt—likely $50–150M for large-scale rehost—limit its bargaining leverage.

Scarcity of Specialized Software Engineering Talent

The market for senior cloud, AI and construction-domain engineers remained tight through 2025, with US median total pay for senior AI/cloud engineers ~$220k–$300k and specialized construction-software roles commanding 10–25% premiums; Procore must match premium compensation and equity to hire at scale.

This dependence on a scarce talent pool gives suppliers (workers) real leverage, pushing Procore’s R&D and operating costs up—salary inflation of 8–12% annualized in 2023–25 squeezed gross margins and raised product development spend per engineer.

Integration Dependency on Third-Party App Developers

The Procore App Marketplace hosts over 500 third-party integrations, supplying niche features like accounting connectors and drone mapping that Procore does not build natively; these developers act as specialized suppliers whose tools increase platform stickiness and contributed an estimated 8–12% of Procore-related transaction value in 2024. If major partners representing, say, the top 20% of app usage migrated exclusively to a rival, Procore’s utility and customer retention could fall noticeably, granting those niche developers moderate bargaining power.

Rising Costs of Cybersecurity and Compliance Services

As construction data becomes a high-value target, Procore depends on specialized cybersecurity vendors and compliance auditors to keep SOC 2 and ISO certifications current; enterprise buyers often require these, so suppliers are effectively must-haves.

These services are costly and failure is expensive—IDC reported average breach costs in 2024 at $4.45M—so security vendors command leverage over Procore’s risk budget and renewal terms.

- Must-have services: SOC 2, ISO audits

- High stakes: avg breach cost $4.45M (2024, IDC)

- Specialized vendors = pricing and timing power

- Impacts: larger share of risk-management spend

Data Acquisition for AI and Machine Learning Training

Procore needs vast, labeled construction data to keep its lead in predictive analytics by 2025; internal telemetry covers much, but external providers and specialist labelers fill gaps in niche datasets.

Only a handful of vendors offer high-fidelity, industry-specific datasets, creating a supplier bottleneck that can slow feature rollout and raise costs—enterprise labeling rates hit $0.10–$0.50 per label in 2024.

Reliance on external data raises concentration risk: a 2023 survey found 62% of construction-tech firms depended on three or fewer data partners for ML-ready datasets.

- High-quality labels cost $0.10–$0.50/label (2024)

- 62% rely on ≤3 data partners (2023)

- Supplier concentration limits speed of advanced feature launches

Hyperscalers, talent & security drive SaaS costs—rehost $50–150M, labels $0.10–0.50

Supplier power is moderate‑to‑high: AWS (≈32% IaaS, 2025) and hyperscalers concentrate hosting leverage; cloud costs = 15–25% SaaS COGS and rehost could cost $50–150M. Talent scarcity (senior AI/cloud pay $220–300k; 10–25% premiums) and security/data vendors (avg breach $4.45M, 2024) raise operating spend; 62% of firms rely on ≤3 data partners, labels $0.10–0.50 each.

| Supplier | Key stat | Impact |

|---|---|---|

| AWS/hyperscalers | ≈32% IaaS (2025) | Pricing/SLA leverage |

| Cloud costs | 15–25% SaaS COGS | Margin pressure |

| Rehost cost | $50–150M | Switch barrier |

| Senior engineers | $220–300k pay | Higher R&D spend |

| Data labels | $0.10–0.50/label (2024) | Feature speed/cost |

| Security | Avg breach $4.45M (2024) | Risk vendor leverage |

What is included in the product

Tailored Porter's Five Forces analysis of Procore that uncovers competitive intensity, buyer and supplier leverage, entry barriers, and substitution risks to inform strategic positioning and valuation.

Clear, one-sheet Porter's Five Forces for Procore—instantly visualize supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions and investor pitches.

Customers Bargaining Power

High Switching Costs for Enterprise-Level Clients

Once a large general contractor or owner embeds Procore into ERP and financial systems, switching costs skyrocket—migrating 10+ years of project records, retraining thousands of staff, and re-linking 100s of subcontractor workflows can exceed millions; Procore reported 2024 ARR growth to $719M, indicating deep enterprise adoption, so despite high service expectations, customers’ ability to leave abruptly is limited, lowering short-term bargaining power.

Industry Fragmentation and the Long Tail of SMBs

The construction sector has ~3.1 million small and mid-sized specialty contractors in the US (US Census, 2023), so individual bargaining power is weak; most are price-takers.

SMBs often adopt Procore because general contractors mandate it—Procore reported 15,000+ customers and platform ubiquity in 2024—creating top-down demand.

That mandate lets Procore preserve list pricing despite cheaper niche tools; switch costs and network effects keep price elasticity low.

Consolidation of Large General Contractors

Demand for Measurable Return on Investment

In the 2025 high-rate environment, customers push Procore for measurable ROI—CFOs demand evidence of productivity gains and risk reduction before renewing amid rising capital costs (US prime ~8.5% in 2025).

Clients press for transparent pricing and proof that Procore cuts project overruns or lowers insurance costs; case studies showing >5–10% schedule or cost savings are common benchmarks.

If Procore cannot show clear ROI versus cheaper point tools, buyers may unbundle the stack to cut software spend and reduce TCO.

- 2025 prime ~8.5% raises ROI hurdle rates

- Buyers expect 5–10% measurable project savings

- Demand for transparent pricing and outcome metrics

- Risk of unbundling if ROI unclear vs point solutions

Influence of Project Owners on Tech Selection

Project owners—real estate developers and government agencies—are increasingly mandating specific construction software to ensure data transparency; by 2024 roughly 25% of large US public owners required standardized digital reporting, pushing platforms like Procore into de facto standards.

These mandates give owners indirect power over Procore’s market share because contractors must adopt the owner-designated platform to win work; Procore reported 16% YoY revenue growth in 2024, partly driven by enterprise mandates.

To stay a mandated solution, Procore must tailor features to owners’ reporting, compliance, and oversight needs—failing which owners may switch mandates and shift market share rapidly.

- Owner mandates drive platform adoption

- 25% large public owners required standard reporting (2024)

- Procore revenue +16% YoY (2024)

- Meeting owner compliance is critical to retain share

Mixed customer leverage: high switching costs vs. big-firm discount power and ROI pressure

Customers’ bargaining power is mixed: high switching costs and owner/GC mandates limit churn and keep price elasticity low, but consolidation of large global firms (25–35% of ARR by 2025) gives them strong volume leverage for discounts and product influence; rising 2025 prime (~8.5%) and demand for 5–10% measurable ROI increase pressure for transparent pricing and unbundling risk.

| Metric | Value |

|---|---|

| Procore ARR growth (2024) | $719M |

| Large firms share (2025) | 25–35% ARR |

| 2025 US prime | ~8.5% |

| Expected ROI benchmark | 5–10% |

Same Document Delivered

Procore Porter's Five Forces Analysis

This preview shows the exact Procore Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy.

No samples or edits—what you see here is the complete file you'll get instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Procore faces moderate rivalry from established construction software vendors, rising buyer power as customers demand integrated workflows, and supplier/partner dynamics that shape platform expansion; barriers to entry remain significant but evolving with cloud-native tools and niche vertical entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Procore’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Hyperscale Cloud Infrastructure Providers

Procore relies heavily on hyperscale clouds—primarily Amazon Web Services—for hosting its platform and data; AWS held ~32% global IaaS market share in 2025, concentrating supplier power.

This concentration lets providers influence pricing and SLAs; cloud costs can be 15–25% of SaaS COGS for large platforms, squeezing margins if rates rise.

Although Procore can refactor to optimize usage, estimated migration costs and technical debt—likely $50–150M for large-scale rehost—limit its bargaining leverage.

Scarcity of Specialized Software Engineering Talent

The market for senior cloud, AI and construction-domain engineers remained tight through 2025, with US median total pay for senior AI/cloud engineers ~$220k–$300k and specialized construction-software roles commanding 10–25% premiums; Procore must match premium compensation and equity to hire at scale.

This dependence on a scarce talent pool gives suppliers (workers) real leverage, pushing Procore’s R&D and operating costs up—salary inflation of 8–12% annualized in 2023–25 squeezed gross margins and raised product development spend per engineer.

Integration Dependency on Third-Party App Developers

The Procore App Marketplace hosts over 500 third-party integrations, supplying niche features like accounting connectors and drone mapping that Procore does not build natively; these developers act as specialized suppliers whose tools increase platform stickiness and contributed an estimated 8–12% of Procore-related transaction value in 2024. If major partners representing, say, the top 20% of app usage migrated exclusively to a rival, Procore’s utility and customer retention could fall noticeably, granting those niche developers moderate bargaining power.

Rising Costs of Cybersecurity and Compliance Services

As construction data becomes a high-value target, Procore depends on specialized cybersecurity vendors and compliance auditors to keep SOC 2 and ISO certifications current; enterprise buyers often require these, so suppliers are effectively must-haves.

These services are costly and failure is expensive—IDC reported average breach costs in 2024 at $4.45M—so security vendors command leverage over Procore’s risk budget and renewal terms.

- Must-have services: SOC 2, ISO audits

- High stakes: avg breach cost $4.45M (2024, IDC)

- Specialized vendors = pricing and timing power

- Impacts: larger share of risk-management spend

Data Acquisition for AI and Machine Learning Training

Procore needs vast, labeled construction data to keep its lead in predictive analytics by 2025; internal telemetry covers much, but external providers and specialist labelers fill gaps in niche datasets.

Only a handful of vendors offer high-fidelity, industry-specific datasets, creating a supplier bottleneck that can slow feature rollout and raise costs—enterprise labeling rates hit $0.10–$0.50 per label in 2024.

Reliance on external data raises concentration risk: a 2023 survey found 62% of construction-tech firms depended on three or fewer data partners for ML-ready datasets.

- High-quality labels cost $0.10–$0.50/label (2024)

- 62% rely on ≤3 data partners (2023)

- Supplier concentration limits speed of advanced feature launches

Hyperscalers, talent & security drive SaaS costs—rehost $50–150M, labels $0.10–0.50

Supplier power is moderate‑to‑high: AWS (≈32% IaaS, 2025) and hyperscalers concentrate hosting leverage; cloud costs = 15–25% SaaS COGS and rehost could cost $50–150M. Talent scarcity (senior AI/cloud pay $220–300k; 10–25% premiums) and security/data vendors (avg breach $4.45M, 2024) raise operating spend; 62% of firms rely on ≤3 data partners, labels $0.10–0.50 each.

| Supplier | Key stat | Impact |

|---|---|---|

| AWS/hyperscalers | ≈32% IaaS (2025) | Pricing/SLA leverage |

| Cloud costs | 15–25% SaaS COGS | Margin pressure |

| Rehost cost | $50–150M | Switch barrier |

| Senior engineers | $220–300k pay | Higher R&D spend |

| Data labels | $0.10–0.50/label (2024) | Feature speed/cost |

| Security | Avg breach $4.45M (2024) | Risk vendor leverage |

What is included in the product

Tailored Porter's Five Forces analysis of Procore that uncovers competitive intensity, buyer and supplier leverage, entry barriers, and substitution risks to inform strategic positioning and valuation.

Clear, one-sheet Porter's Five Forces for Procore—instantly visualize supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions and investor pitches.

Customers Bargaining Power

High Switching Costs for Enterprise-Level Clients

Once a large general contractor or owner embeds Procore into ERP and financial systems, switching costs skyrocket—migrating 10+ years of project records, retraining thousands of staff, and re-linking 100s of subcontractor workflows can exceed millions; Procore reported 2024 ARR growth to $719M, indicating deep enterprise adoption, so despite high service expectations, customers’ ability to leave abruptly is limited, lowering short-term bargaining power.

Industry Fragmentation and the Long Tail of SMBs

The construction sector has ~3.1 million small and mid-sized specialty contractors in the US (US Census, 2023), so individual bargaining power is weak; most are price-takers.

SMBs often adopt Procore because general contractors mandate it—Procore reported 15,000+ customers and platform ubiquity in 2024—creating top-down demand.

That mandate lets Procore preserve list pricing despite cheaper niche tools; switch costs and network effects keep price elasticity low.

Consolidation of Large General Contractors

Demand for Measurable Return on Investment

In the 2025 high-rate environment, customers push Procore for measurable ROI—CFOs demand evidence of productivity gains and risk reduction before renewing amid rising capital costs (US prime ~8.5% in 2025).

Clients press for transparent pricing and proof that Procore cuts project overruns or lowers insurance costs; case studies showing >5–10% schedule or cost savings are common benchmarks.

If Procore cannot show clear ROI versus cheaper point tools, buyers may unbundle the stack to cut software spend and reduce TCO.

- 2025 prime ~8.5% raises ROI hurdle rates

- Buyers expect 5–10% measurable project savings

- Demand for transparent pricing and outcome metrics

- Risk of unbundling if ROI unclear vs point solutions

Influence of Project Owners on Tech Selection

Project owners—real estate developers and government agencies—are increasingly mandating specific construction software to ensure data transparency; by 2024 roughly 25% of large US public owners required standardized digital reporting, pushing platforms like Procore into de facto standards.

These mandates give owners indirect power over Procore’s market share because contractors must adopt the owner-designated platform to win work; Procore reported 16% YoY revenue growth in 2024, partly driven by enterprise mandates.

To stay a mandated solution, Procore must tailor features to owners’ reporting, compliance, and oversight needs—failing which owners may switch mandates and shift market share rapidly.

- Owner mandates drive platform adoption

- 25% large public owners required standard reporting (2024)

- Procore revenue +16% YoY (2024)

- Meeting owner compliance is critical to retain share

Mixed customer leverage: high switching costs vs. big-firm discount power and ROI pressure

Customers’ bargaining power is mixed: high switching costs and owner/GC mandates limit churn and keep price elasticity low, but consolidation of large global firms (25–35% of ARR by 2025) gives them strong volume leverage for discounts and product influence; rising 2025 prime (~8.5%) and demand for 5–10% measurable ROI increase pressure for transparent pricing and unbundling risk.

| Metric | Value |

|---|---|

| Procore ARR growth (2024) | $719M |

| Large firms share (2025) | 25–35% ARR |

| 2025 US prime | ~8.5% |

| Expected ROI benchmark | 5–10% |

Same Document Delivered

Procore Porter's Five Forces Analysis

This preview shows the exact Procore Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy.

No samples or edits—what you see here is the complete file you'll get instantly after payment.