Progress Software Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Progress Software faces moderate supplier power and evolving buyer demands across cloud and legacy markets, while competition from platform specialists and low-cost entrants raises intensity; technological change and subscription shifts amplify both threat of substitutes and the need for strategic differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Progress Software’s competitive dynamics, market pressures, and strategic advantages in detail.

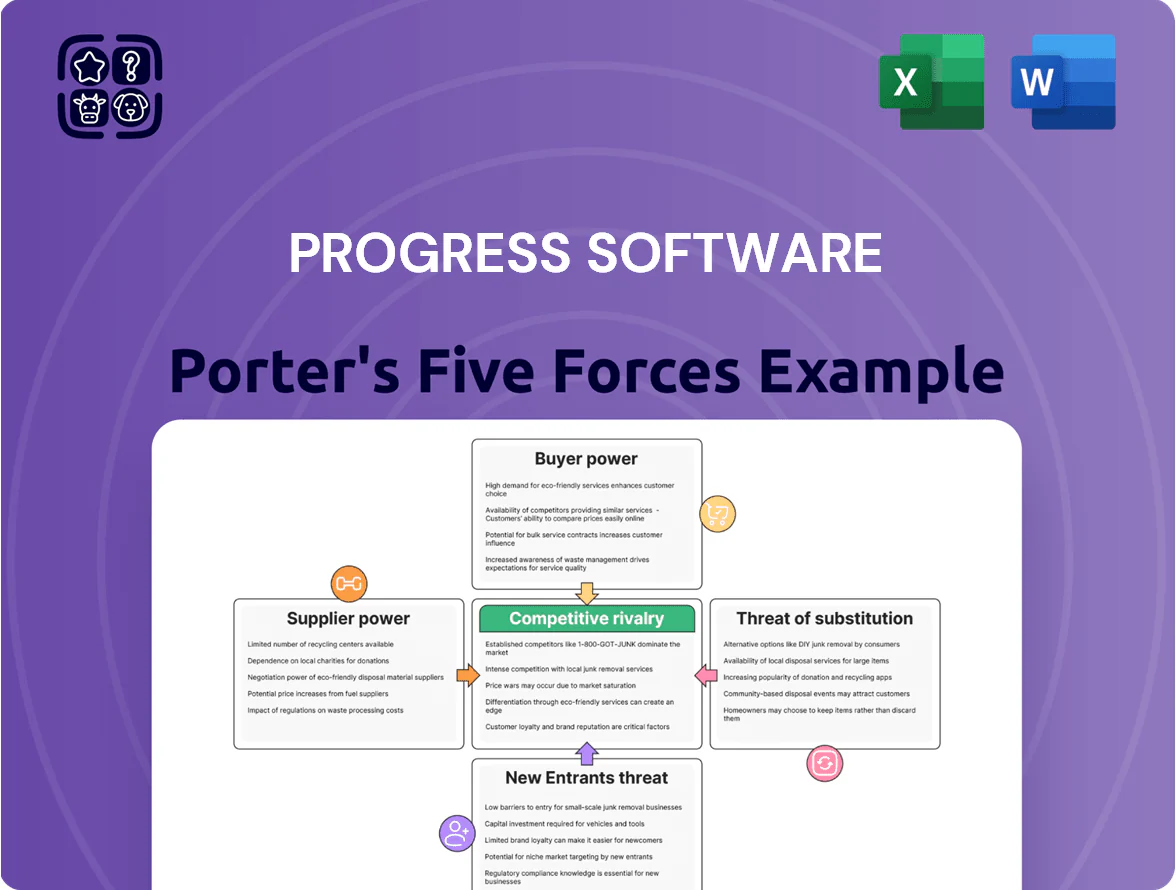

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Progress Software depends on AWS, Microsoft Azure, and Google Cloud for hosting key SaaS and digital-experience products; together these three held about 66% of global cloud IaaS/PaaS market in 2024, giving them strong pricing power.

Their dominance lets them raise fees or change SLAs, which in 2024 pressured software peers’ gross margins by ~2–5 percentage points; similar shifts would cut Progress’s infrastructure margins and raise operating costs.

Scarcity of Specialized Software Engineering Talent

The primary input for Progress Software is senior engineering talent able to support OpenEdge and build low-code/DevOps features; in 2025 demand for dual-skilled devs (legacy proprietary + cloud-native) rose 18% year-over-year, with median US cloud dev salaries at $145k and niche OpenEdge consultants commanding $180k–$250k, giving suppliers strong leverage to demand higher pay and contracting terms, pressuring Progress’s margins and R&D costs.

Dependence on Third-Party Intellectual Property

Progress Software relies on third-party libraries and APIs—many open-source but some proprietary—creating supplier power when niche vendors control key IP; for example, 12% of Progress’s 2024 R&D stack reportedly used licensed components, and a 2023 survey showed 28% of enterprise software vendors faced >15% cost increases after vendor fee hikes; consolidation or higher licensing could raise COGS or force costly rewrites and technical debt.

Influence of Cybersecurity Service Vendors

Progress relies on external cybersecurity firms for audits, threat intelligence, and specialized protection tools; in 2024 global managed security services—valued at about $40.1B—grew 12% YoY, making these vendors both indispensable and scarce.

The rising frequency of sophisticated attacks—global breaches up 15% in 2024—gives vendors leverage, as their services directly affect Progress’s customer trust and compliance, raising switching costs and contract dependency.

- External security spend drives vendor power

- Managed security market ~$40.1B in 2024, +12% YoY

- Global breaches +15% in 2024 increases dependency

- High switching costs and compliance risk strengthen suppliers

Hardware and Semiconductor Supply Chain Impacts

- 2024 semiconductors: $555B revenue (-2.1%)

- ARM server share: ~10% of cloud instances by 2025

- Re-engineering raises R&D/time-to-market risk

- Supplier shifts can dictate roadmap and costs

Supplier dominance hikes cloud, security, talent costs—squeezing margins and roadmaps

Supplier power is high: cloud IaaS/PaaS (AWS, Azure, GCP) held ~66% of market in 2024, pressuring margins; managed security was ~$40.1B (+12% YoY) and breaches rose 15% in 2024, raising dependence; specialized talent demand rose 18% in 2025 with median cloud dev pay ~$145k and OpenEdge consultants $180k–$250k; semiconductors fell to $555B (-2.1%) in 2024, adding re‑engineering costs.

| Supplier | 2024/25 metric | Impact on Progress |

|---|---|---|

| Cloud IaaS/PaaS | 66% market share (2024) | Pricing power, higher infra costs |

| Managed security | $40.1B, +12% YoY (2024) | Critical, scarce, raises spend |

| Talent | Demand +18% (2025); $145k–$250k pay | Rising R&D and salary costs |

| Semiconductors | $555B, -2.1% (2024) | Re‑engineering, roadmap shifts |

What is included in the product

Uncovers competitive pressures facing Progress Software by analyzing rivalry, buyer and supplier power, threat of substitutes, and entry barriers—highlighting disruptive threats, pricing levers, and strategic defenses tailored to its software and services market.

A concise Porter's Five Forces sheet tailored for Progress Software—instantly highlights competitive pressures and strategic risks for faster, board-ready decisions.

Customers Bargaining Power

High Switching Costs for Legacy Ecosystems

A significant share of Progress customers—estimates from Progress' 2024 annual report show ~40% tied to the OpenEdge ecosystem—face high migration costs because mission‑critical apps were customized over decades, so switching requires large replatforming and retraining investments. This entrenched customization limits buyers' price leverage, sustaining Progress' gross margin (2024 gross margin ~68%) and delivering stable recurring revenue—subscription and support made up ~72% of FY2024 revenue—creating a defensive moat against churn.

Availability of Alternative Low-Code Platforms

In 2025’s booming low-code market—projected at $31.6B global revenue for 2025 by Forrester—buyers can choose Mendix, OutSystems, Microsoft Power Apps and others, raising customer bargaining power versus Progress Software.

New or modernizing customers not locked into Progress can demand lower prices or broader integrations; Progress must match competitive pricing and deliver native integrations (APIs, data connectors) to win deals and reduce churn.

Consolidation of Enterprise IT Budgets

Large enterprises are consolidating software vendors to simplify IT and chase discounts; 2024 surveys show 62% of CIOs target vendor reduction within 3 years, strengthening procurement leverage over Progress Software (PRGS).

Procurement now demands bundled pricing and multi-year SLAs; Progress risks margin pressure as customers require demonstrable platform breadth to replace multiple suppliers.

Information Transparency and Market Comparison

By 2025, abundant peer reviews, benchmarks, and transparent pricing mean financial and IT buyers can compare Progress Software directly to rivals and push harder on contract terms, cutting typical enterprise software margins by roughly 150–300 basis points vs. pre-2020 levels.

This transparency shrinks information asymmetry that once let vendors keep opaque pricing, forcing Progress to justify premium features with measurable performance and SLA metrics.

- Peer reviews up ~4x since 2018

- Benchmarks driving 10–25% price concessions

- Buyers demand SLA‑linked fees

Demand for Hybrid and Multi-Cloud Flexibility

Modern enterprise buyers demand hybrid and multi-cloud support to avoid vendor lock-in with AWS, Microsoft Azure, and Google Cloud, and 62% of CIOs cited portability as a top priority in 2024 surveys, pressuring Progress to invest in interoperability.

Meeting this demand requires R&D and partner integrations; Progress’s 2024 R&D spend of $80.6M (13% of revenue) shows scale but customers can still threaten to move workloads, boosting their bargaining power for better support and pricing.

- 62% of CIOs prioritize portability (2024)

- Progress R&D $80.6M in 2024 (13% of revenue)

- Customers can leverage migration to cloud giants

Progress: Strong margins vs rising low-code disruption and CIO-driven vendor cuts

Customers hold moderate-to-high bargaining power: ~40% OpenEdge lock-in limits price pressure, supporting Progress’ ~68% gross margin and 72% recurring revenue (FY2024), but 2025 low-code alternatives ($31.6B market) and CIO-driven vendor consolidation (62% target reduction) plus transparency (peer reviews ↑4x) pressure pricing and SLAs; Progress R&D $80.6M (2024) needed to defend integrations.

| Metric | Value |

|---|---|

| OpenEdge share | ~40% |

| Gross margin FY2024 | ~68% |

| Recurring rev FY2024 | 72% |

| R&D 2024 | $80.6M (13% rev) |

| Low-code 2025 | $31.6B (Forrester) |

| CIOs vendor cut | 62% (2024) |

Same Document Delivered

Progress Software Porter's Five Forces Analysis

This preview shows the exact Progress Software Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Progress Software faces moderate supplier power and evolving buyer demands across cloud and legacy markets, while competition from platform specialists and low-cost entrants raises intensity; technological change and subscription shifts amplify both threat of substitutes and the need for strategic differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Progress Software’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Progress Software depends on AWS, Microsoft Azure, and Google Cloud for hosting key SaaS and digital-experience products; together these three held about 66% of global cloud IaaS/PaaS market in 2024, giving them strong pricing power.

Their dominance lets them raise fees or change SLAs, which in 2024 pressured software peers’ gross margins by ~2–5 percentage points; similar shifts would cut Progress’s infrastructure margins and raise operating costs.

Scarcity of Specialized Software Engineering Talent

The primary input for Progress Software is senior engineering talent able to support OpenEdge and build low-code/DevOps features; in 2025 demand for dual-skilled devs (legacy proprietary + cloud-native) rose 18% year-over-year, with median US cloud dev salaries at $145k and niche OpenEdge consultants commanding $180k–$250k, giving suppliers strong leverage to demand higher pay and contracting terms, pressuring Progress’s margins and R&D costs.

Dependence on Third-Party Intellectual Property

Progress Software relies on third-party libraries and APIs—many open-source but some proprietary—creating supplier power when niche vendors control key IP; for example, 12% of Progress’s 2024 R&D stack reportedly used licensed components, and a 2023 survey showed 28% of enterprise software vendors faced >15% cost increases after vendor fee hikes; consolidation or higher licensing could raise COGS or force costly rewrites and technical debt.

Influence of Cybersecurity Service Vendors

Progress relies on external cybersecurity firms for audits, threat intelligence, and specialized protection tools; in 2024 global managed security services—valued at about $40.1B—grew 12% YoY, making these vendors both indispensable and scarce.

The rising frequency of sophisticated attacks—global breaches up 15% in 2024—gives vendors leverage, as their services directly affect Progress’s customer trust and compliance, raising switching costs and contract dependency.

- External security spend drives vendor power

- Managed security market ~$40.1B in 2024, +12% YoY

- Global breaches +15% in 2024 increases dependency

- High switching costs and compliance risk strengthen suppliers

Hardware and Semiconductor Supply Chain Impacts

- 2024 semiconductors: $555B revenue (-2.1%)

- ARM server share: ~10% of cloud instances by 2025

- Re-engineering raises R&D/time-to-market risk

- Supplier shifts can dictate roadmap and costs

Supplier dominance hikes cloud, security, talent costs—squeezing margins and roadmaps

Supplier power is high: cloud IaaS/PaaS (AWS, Azure, GCP) held ~66% of market in 2024, pressuring margins; managed security was ~$40.1B (+12% YoY) and breaches rose 15% in 2024, raising dependence; specialized talent demand rose 18% in 2025 with median cloud dev pay ~$145k and OpenEdge consultants $180k–$250k; semiconductors fell to $555B (-2.1%) in 2024, adding re‑engineering costs.

| Supplier | 2024/25 metric | Impact on Progress |

|---|---|---|

| Cloud IaaS/PaaS | 66% market share (2024) | Pricing power, higher infra costs |

| Managed security | $40.1B, +12% YoY (2024) | Critical, scarce, raises spend |

| Talent | Demand +18% (2025); $145k–$250k pay | Rising R&D and salary costs |

| Semiconductors | $555B, -2.1% (2024) | Re‑engineering, roadmap shifts |

What is included in the product

Uncovers competitive pressures facing Progress Software by analyzing rivalry, buyer and supplier power, threat of substitutes, and entry barriers—highlighting disruptive threats, pricing levers, and strategic defenses tailored to its software and services market.

A concise Porter's Five Forces sheet tailored for Progress Software—instantly highlights competitive pressures and strategic risks for faster, board-ready decisions.

Customers Bargaining Power

High Switching Costs for Legacy Ecosystems

A significant share of Progress customers—estimates from Progress' 2024 annual report show ~40% tied to the OpenEdge ecosystem—face high migration costs because mission‑critical apps were customized over decades, so switching requires large replatforming and retraining investments. This entrenched customization limits buyers' price leverage, sustaining Progress' gross margin (2024 gross margin ~68%) and delivering stable recurring revenue—subscription and support made up ~72% of FY2024 revenue—creating a defensive moat against churn.

Availability of Alternative Low-Code Platforms

In 2025’s booming low-code market—projected at $31.6B global revenue for 2025 by Forrester—buyers can choose Mendix, OutSystems, Microsoft Power Apps and others, raising customer bargaining power versus Progress Software.

New or modernizing customers not locked into Progress can demand lower prices or broader integrations; Progress must match competitive pricing and deliver native integrations (APIs, data connectors) to win deals and reduce churn.

Consolidation of Enterprise IT Budgets

Large enterprises are consolidating software vendors to simplify IT and chase discounts; 2024 surveys show 62% of CIOs target vendor reduction within 3 years, strengthening procurement leverage over Progress Software (PRGS).

Procurement now demands bundled pricing and multi-year SLAs; Progress risks margin pressure as customers require demonstrable platform breadth to replace multiple suppliers.

Information Transparency and Market Comparison

By 2025, abundant peer reviews, benchmarks, and transparent pricing mean financial and IT buyers can compare Progress Software directly to rivals and push harder on contract terms, cutting typical enterprise software margins by roughly 150–300 basis points vs. pre-2020 levels.

This transparency shrinks information asymmetry that once let vendors keep opaque pricing, forcing Progress to justify premium features with measurable performance and SLA metrics.

- Peer reviews up ~4x since 2018

- Benchmarks driving 10–25% price concessions

- Buyers demand SLA‑linked fees

Demand for Hybrid and Multi-Cloud Flexibility

Modern enterprise buyers demand hybrid and multi-cloud support to avoid vendor lock-in with AWS, Microsoft Azure, and Google Cloud, and 62% of CIOs cited portability as a top priority in 2024 surveys, pressuring Progress to invest in interoperability.

Meeting this demand requires R&D and partner integrations; Progress’s 2024 R&D spend of $80.6M (13% of revenue) shows scale but customers can still threaten to move workloads, boosting their bargaining power for better support and pricing.

- 62% of CIOs prioritize portability (2024)

- Progress R&D $80.6M in 2024 (13% of revenue)

- Customers can leverage migration to cloud giants

Progress: Strong margins vs rising low-code disruption and CIO-driven vendor cuts

Customers hold moderate-to-high bargaining power: ~40% OpenEdge lock-in limits price pressure, supporting Progress’ ~68% gross margin and 72% recurring revenue (FY2024), but 2025 low-code alternatives ($31.6B market) and CIO-driven vendor consolidation (62% target reduction) plus transparency (peer reviews ↑4x) pressure pricing and SLAs; Progress R&D $80.6M (2024) needed to defend integrations.

| Metric | Value |

|---|---|

| OpenEdge share | ~40% |

| Gross margin FY2024 | ~68% |

| Recurring rev FY2024 | 72% |

| R&D 2024 | $80.6M (13% rev) |

| Low-code 2025 | $31.6B (Forrester) |

| CIOs vendor cut | 62% (2024) |

Same Document Delivered

Progress Software Porter's Five Forces Analysis

This preview shows the exact Progress Software Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use the moment you buy.