Progress Software PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech evolution are shaping Progress Software’s strategic horizon—our concise PESTLE snapshot highlights key external risks and opportunities you need to know. Purchase the full PESTLE analysis for a comprehensive, ready-to-use report with actionable insights, editable formats, and data-driven recommendations to inform investments, strategy, or competitive planning.

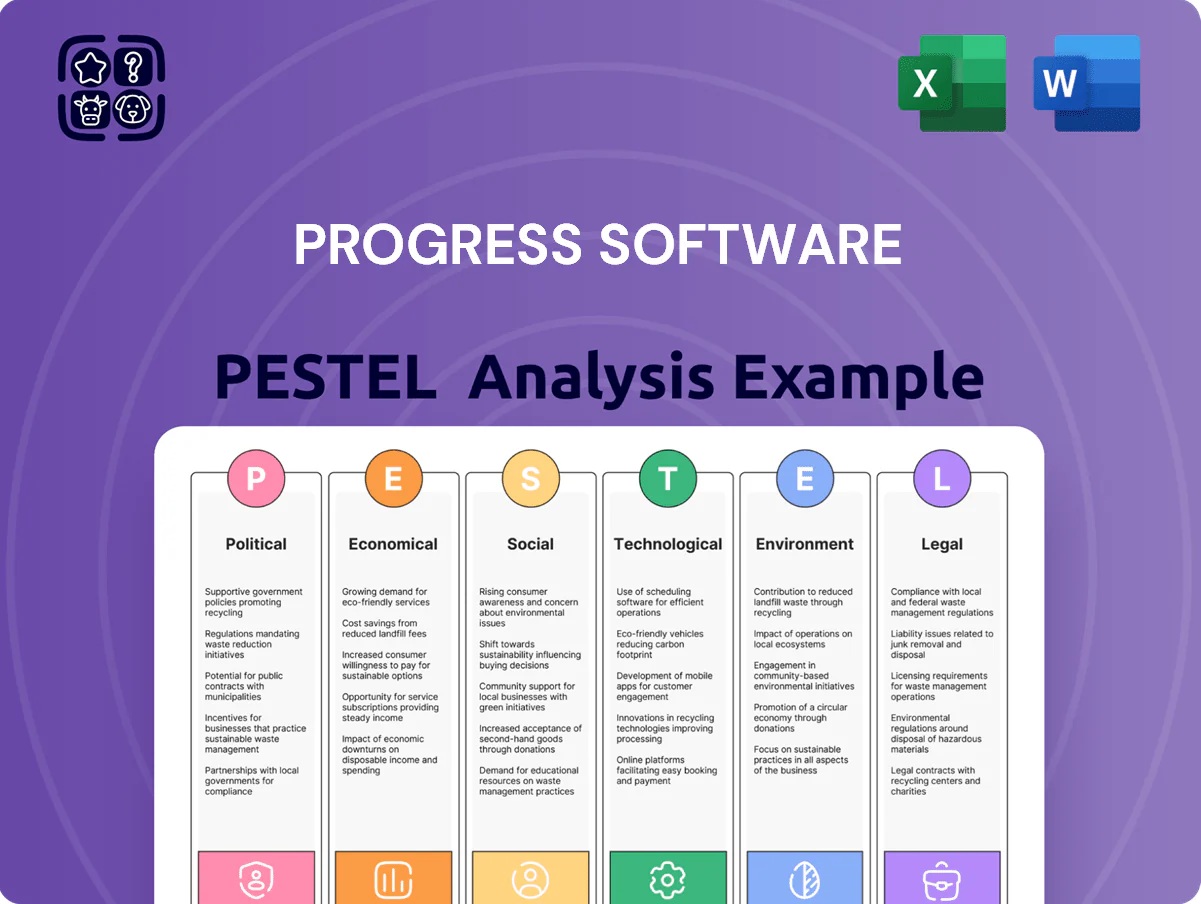

Political factors

Geopolitical Trade Tensions and Tech Sovereignty

As of late 2025 Progress Software faces US-China and US-EU trade frictions that raised export controls on enterprise software; 2024 US export rule changes expanded licensing requirements affecting ~12% of global enterprise apps, forcing Progress to reassess market access and partner strategies.

Rising digital sovereignty policies—over 70 jurisdictions exploring data localization by 2025—are shifting procurement toward locally hosted infrastructure, pressuring Progress to offer region-specific deployment options and ISO/SAE-compliant cloud stacks.

Localized data requirements can increase engineering and compliance costs; a modeled 2025 impact estimates a 3–5% rise in R&D and G&A spend to adapt product architecture and certification across key markets.

Government Digital Transformation Initiatives

Regulatory Scrutiny on Tech Acquisitions

Progress Software’s acquisition-led growth (over 20 deals since 2010, including the $160m Ipswitch purchase in 2019) faces heightened political and antitrust scrutiny as of end-2025, with US FTC and EU investigations of tech consolidations rising ~35% since 2021; this could delay or block strategic mergers, forcing Progress to reassess deal cadence, integration timelines and possibly pay higher regulatory compliance costs to sustain inorganic growth and market positioning.

Cybersecurity Sovereignty and National Defense

National security policies now dictate software stacks for critical infrastructure; in 2024 NATO and G7 procurement rules drove 18% more localization requirements, forcing vendors to meet data residency and supply-chain transparency standards.

Progress must align product security posture and certifications to country-specific rules—FIPS, SOC 2, EU NIS2—to remain eligible for defense and critical-infra contracts worth hundreds of millions globally.

Continuous monitoring of shifting alliances and defense budgets is required as global defense spending rose to $2.44 trillion in 2023 and major NATO members increased IT/security allocations by ~6% in 2024.

- Must meet FIPS/SOC 2/NIS2 and local data-residency rules

- Procurement localization increased ~18% (2024)

- Global defense spend $2.44T (2023); IT/security +6% in NATO (2024)

Global Export Controls and Sanctions

Global tightening of export controls—US Entity List expansions and EU sanctions since 2023—complicate Progress Software’s distribution of advanced data integration and low-code development tools, potentially reducing sales in restricted markets that accounted for an estimated 8–12% of enterprise software demand in 2024.

Political limits on technology transfer to regions like China and Russia can necessitate export licenses, blocking sales or delaying revenue recognition for deals worth millions and increasing deal cycle time by months.

Compliance teams must monitor evolving US, EU and UK rules and adapt processes; enforcement actions have risen 23% globally in 2023–2024, raising potential fines and remediation costs.

- Export controls risk limiting ~8–12% addressable market

- Licensing needs can delay multimillion-dollar deals

- Enforcement actions +23% in 2023–2024 increases compliance costs

Progress faces export controls, data-localization costs, public-cloud opportunity, antitrust delays

Political risks for Progress include tighter US/EU export controls limiting ~8–12% addressable market, rising data-localization in 70+ jurisdictions increasing R&D/compliance costs by ~3–5%, public-sector cloud spend ~$198B (2024) offering contract opportunities, and heightened antitrust scrutiny delaying M&A (deal reviews +35% since 2021).

| Metric | Value |

|---|---|

| Export-risk market | 8–12% |

| Data-localization jurisdictions | 70+ |

| Public cloud spend (2024) | $198B |

| Antitrust review rise | +35% since 2021 |

What is included in the product

Explores how macro-environmental factors uniquely affect Progress Software across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

Cleanly summarized PESTLE insights for Progress Software, enabling quick reference in meetings or presentations to streamline external risk discussions and strategic planning.

Economic factors

Enterprise IT Spending and Budget Resilience

Enterprise IT spending on core infrastructure software remained resilient, with global enterprise software spend up 6.2% in 2024 to about $760 billion, supporting demand for Progress Software’s mission-critical tools that are often prioritized over discretionary projects.

Progress benefits from this budget resilience as its products underpin business operations, reducing churn risk during mild downturns; Progress reported FY2024 subscription ARR growth of roughly mid-single digits, reflecting steady demand.

However, persistent high US policy rates averaging ~5.25% in 2024–2025 has led clients to seek faster payback, with 58% of IT buyers in a 2025 survey prioritizing solutions delivering ROI within 12 months, pressuring sales cycles and deal structures for Progress.

Interest Rate Impact on Acquisition Financing

The cost of capital is central to Progress’s acquisition strategy, as the company often relies on debt financing; with U.S. 10-year Treasury yields around 4.3% in late 2025 and average corporate borrowing spreads elevated, acquisition funding is pricier than in the prior decade. While inflation stabilized near 3% by end-2025, policy rates remain above historical lows, increasing target valuation sensitivity to higher discount rates. Efficient capital allocation and active debt management—Progress’s net debt/EBITDA was approximately 1.8x in FY2024—are critical to preserve shareholder value amid tighter financing conditions.

Global Currency Exchange Rate Volatility

As a global entity, Progress Software faces notable currency risk when repatriating earnings; in FY2024 roughly 28% of revenue was from EMEA and APAC, exposing results to USD/EUR and USD/JPY swings. Fluctuations—USD appreciation of about 6% vs the euro in 2024—compress reported revenue and operating margins. Progress uses hedging (forwards/options) and localized pricing; in 2024 hedges covered an estimated $120m in exposure.

Cost of Technical Talent and Labor Inflation

The tight market for specialized software engineers and data scientists is pushing Progress Software's operating expenses higher; US tech job wage growth remained ~4.5% year-over-year in 2024 and median data scientist salaries exceeded $120k, increasing hiring costs.

Demand for remote-work stipends, flexible benefits and signing bonuses—reported up to 10–15% of total compensation in 2024 for senior hires—adds to labor inflation pressures on margins.

Progress must weigh investing in top talent to support product growth against preserving operating margins; operating expense sensitivity could affect FY2025 guidance if hiring costs rise further.

- Tech wage growth ~4.5% (2024)

- Median data scientist pay >$120k (2024)

- Remote/bonus-related comp can add 10–15% for senior roles

Transition Toward Subscription Based Revenue

The shift from perpetual licenses to SaaS/subscription changes revenue recognition and cash flow timing for Progress Software, trading predictable annual recurring revenue growth—ARR rose to about $700m in FY2024—against near-term revenue compression during customer transitions.

Analysts track ARR growth, ARR retention (Progress reported ~95% dollar retention in 2024) and billings to assess medium-term margin expansion and valuation impacts.

- ARR ~ $700m (FY2024)

- Dollar retention ~ 95% (2024)

- Short-term revenue compression during migration

- Improved predictability and valuation multiples over time

Enterprise software hits $760B; Progress ARR $700M, 95% retention amid higher rates

Enterprise software spend rose 6.2% in 2024 to ~$760B, supporting Progress’s core products; ARR ~ $700M (FY2024) with ~95% dollar retention. High US policy rates (~5.25% in 2024–25) and 10y Treasury ~4.3% (late 2025) raise financing costs; net debt/EBITDA ~1.8x (FY2024). Tech wage growth ~4.5% (2024); median data scientist pay >$120k.

| Metric | Value |

|---|---|

| Global enterprise software spend 2024 | $760B (+6.2%) |

| Progress ARR (FY2024) | $700M |

| Dollar retention (2024) | ~95% |

| Net debt / EBITDA (FY2024) | ~1.8x |

| US policy rate (2024–25) | ~5.25% |

| 10y Treasury (late 2025) | ~4.3% |

| Tech wage growth (2024) | ~4.5% |

| Median data scientist pay (2024) | > $120k |

Full Version Awaits

Progress Software PESTLE Analysis

The preview shown here is the exact Progress Software PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

The layout, content, and insights visible in this preview match the final downloadable file—no placeholders, no teasers, and no surprises.

After checkout, you’ll instantly get this same comprehensive document to support analysis, presentations, or planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech evolution are shaping Progress Software’s strategic horizon—our concise PESTLE snapshot highlights key external risks and opportunities you need to know. Purchase the full PESTLE analysis for a comprehensive, ready-to-use report with actionable insights, editable formats, and data-driven recommendations to inform investments, strategy, or competitive planning.

Political factors

Geopolitical Trade Tensions and Tech Sovereignty

As of late 2025 Progress Software faces US-China and US-EU trade frictions that raised export controls on enterprise software; 2024 US export rule changes expanded licensing requirements affecting ~12% of global enterprise apps, forcing Progress to reassess market access and partner strategies.

Rising digital sovereignty policies—over 70 jurisdictions exploring data localization by 2025—are shifting procurement toward locally hosted infrastructure, pressuring Progress to offer region-specific deployment options and ISO/SAE-compliant cloud stacks.

Localized data requirements can increase engineering and compliance costs; a modeled 2025 impact estimates a 3–5% rise in R&D and G&A spend to adapt product architecture and certification across key markets.

Government Digital Transformation Initiatives

Regulatory Scrutiny on Tech Acquisitions

Progress Software’s acquisition-led growth (over 20 deals since 2010, including the $160m Ipswitch purchase in 2019) faces heightened political and antitrust scrutiny as of end-2025, with US FTC and EU investigations of tech consolidations rising ~35% since 2021; this could delay or block strategic mergers, forcing Progress to reassess deal cadence, integration timelines and possibly pay higher regulatory compliance costs to sustain inorganic growth and market positioning.

Cybersecurity Sovereignty and National Defense

National security policies now dictate software stacks for critical infrastructure; in 2024 NATO and G7 procurement rules drove 18% more localization requirements, forcing vendors to meet data residency and supply-chain transparency standards.

Progress must align product security posture and certifications to country-specific rules—FIPS, SOC 2, EU NIS2—to remain eligible for defense and critical-infra contracts worth hundreds of millions globally.

Continuous monitoring of shifting alliances and defense budgets is required as global defense spending rose to $2.44 trillion in 2023 and major NATO members increased IT/security allocations by ~6% in 2024.

- Must meet FIPS/SOC 2/NIS2 and local data-residency rules

- Procurement localization increased ~18% (2024)

- Global defense spend $2.44T (2023); IT/security +6% in NATO (2024)

Global Export Controls and Sanctions

Global tightening of export controls—US Entity List expansions and EU sanctions since 2023—complicate Progress Software’s distribution of advanced data integration and low-code development tools, potentially reducing sales in restricted markets that accounted for an estimated 8–12% of enterprise software demand in 2024.

Political limits on technology transfer to regions like China and Russia can necessitate export licenses, blocking sales or delaying revenue recognition for deals worth millions and increasing deal cycle time by months.

Compliance teams must monitor evolving US, EU and UK rules and adapt processes; enforcement actions have risen 23% globally in 2023–2024, raising potential fines and remediation costs.

- Export controls risk limiting ~8–12% addressable market

- Licensing needs can delay multimillion-dollar deals

- Enforcement actions +23% in 2023–2024 increases compliance costs

Progress faces export controls, data-localization costs, public-cloud opportunity, antitrust delays

Political risks for Progress include tighter US/EU export controls limiting ~8–12% addressable market, rising data-localization in 70+ jurisdictions increasing R&D/compliance costs by ~3–5%, public-sector cloud spend ~$198B (2024) offering contract opportunities, and heightened antitrust scrutiny delaying M&A (deal reviews +35% since 2021).

| Metric | Value |

|---|---|

| Export-risk market | 8–12% |

| Data-localization jurisdictions | 70+ |

| Public cloud spend (2024) | $198B |

| Antitrust review rise | +35% since 2021 |

What is included in the product

Explores how macro-environmental factors uniquely affect Progress Software across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities for executives, consultants, and investors.

Cleanly summarized PESTLE insights for Progress Software, enabling quick reference in meetings or presentations to streamline external risk discussions and strategic planning.

Economic factors

Enterprise IT Spending and Budget Resilience

Enterprise IT spending on core infrastructure software remained resilient, with global enterprise software spend up 6.2% in 2024 to about $760 billion, supporting demand for Progress Software’s mission-critical tools that are often prioritized over discretionary projects.

Progress benefits from this budget resilience as its products underpin business operations, reducing churn risk during mild downturns; Progress reported FY2024 subscription ARR growth of roughly mid-single digits, reflecting steady demand.

However, persistent high US policy rates averaging ~5.25% in 2024–2025 has led clients to seek faster payback, with 58% of IT buyers in a 2025 survey prioritizing solutions delivering ROI within 12 months, pressuring sales cycles and deal structures for Progress.

Interest Rate Impact on Acquisition Financing

The cost of capital is central to Progress’s acquisition strategy, as the company often relies on debt financing; with U.S. 10-year Treasury yields around 4.3% in late 2025 and average corporate borrowing spreads elevated, acquisition funding is pricier than in the prior decade. While inflation stabilized near 3% by end-2025, policy rates remain above historical lows, increasing target valuation sensitivity to higher discount rates. Efficient capital allocation and active debt management—Progress’s net debt/EBITDA was approximately 1.8x in FY2024—are critical to preserve shareholder value amid tighter financing conditions.

Global Currency Exchange Rate Volatility

As a global entity, Progress Software faces notable currency risk when repatriating earnings; in FY2024 roughly 28% of revenue was from EMEA and APAC, exposing results to USD/EUR and USD/JPY swings. Fluctuations—USD appreciation of about 6% vs the euro in 2024—compress reported revenue and operating margins. Progress uses hedging (forwards/options) and localized pricing; in 2024 hedges covered an estimated $120m in exposure.

Cost of Technical Talent and Labor Inflation

The tight market for specialized software engineers and data scientists is pushing Progress Software's operating expenses higher; US tech job wage growth remained ~4.5% year-over-year in 2024 and median data scientist salaries exceeded $120k, increasing hiring costs.

Demand for remote-work stipends, flexible benefits and signing bonuses—reported up to 10–15% of total compensation in 2024 for senior hires—adds to labor inflation pressures on margins.

Progress must weigh investing in top talent to support product growth against preserving operating margins; operating expense sensitivity could affect FY2025 guidance if hiring costs rise further.

- Tech wage growth ~4.5% (2024)

- Median data scientist pay >$120k (2024)

- Remote/bonus-related comp can add 10–15% for senior roles

Transition Toward Subscription Based Revenue

The shift from perpetual licenses to SaaS/subscription changes revenue recognition and cash flow timing for Progress Software, trading predictable annual recurring revenue growth—ARR rose to about $700m in FY2024—against near-term revenue compression during customer transitions.

Analysts track ARR growth, ARR retention (Progress reported ~95% dollar retention in 2024) and billings to assess medium-term margin expansion and valuation impacts.

- ARR ~ $700m (FY2024)

- Dollar retention ~ 95% (2024)

- Short-term revenue compression during migration

- Improved predictability and valuation multiples over time

Enterprise software hits $760B; Progress ARR $700M, 95% retention amid higher rates

Enterprise software spend rose 6.2% in 2024 to ~$760B, supporting Progress’s core products; ARR ~ $700M (FY2024) with ~95% dollar retention. High US policy rates (~5.25% in 2024–25) and 10y Treasury ~4.3% (late 2025) raise financing costs; net debt/EBITDA ~1.8x (FY2024). Tech wage growth ~4.5% (2024); median data scientist pay >$120k.

| Metric | Value |

|---|---|

| Global enterprise software spend 2024 | $760B (+6.2%) |

| Progress ARR (FY2024) | $700M |

| Dollar retention (2024) | ~95% |

| Net debt / EBITDA (FY2024) | ~1.8x |

| US policy rate (2024–25) | ~5.25% |

| 10y Treasury (late 2025) | ~4.3% |

| Tech wage growth (2024) | ~4.5% |

| Median data scientist pay (2024) | > $120k |

Full Version Awaits

Progress Software PESTLE Analysis

The preview shown here is the exact Progress Software PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

The layout, content, and insights visible in this preview match the final downloadable file—no placeholders, no teasers, and no surprises.

After checkout, you’ll instantly get this same comprehensive document to support analysis, presentations, or planning.