Progyny Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

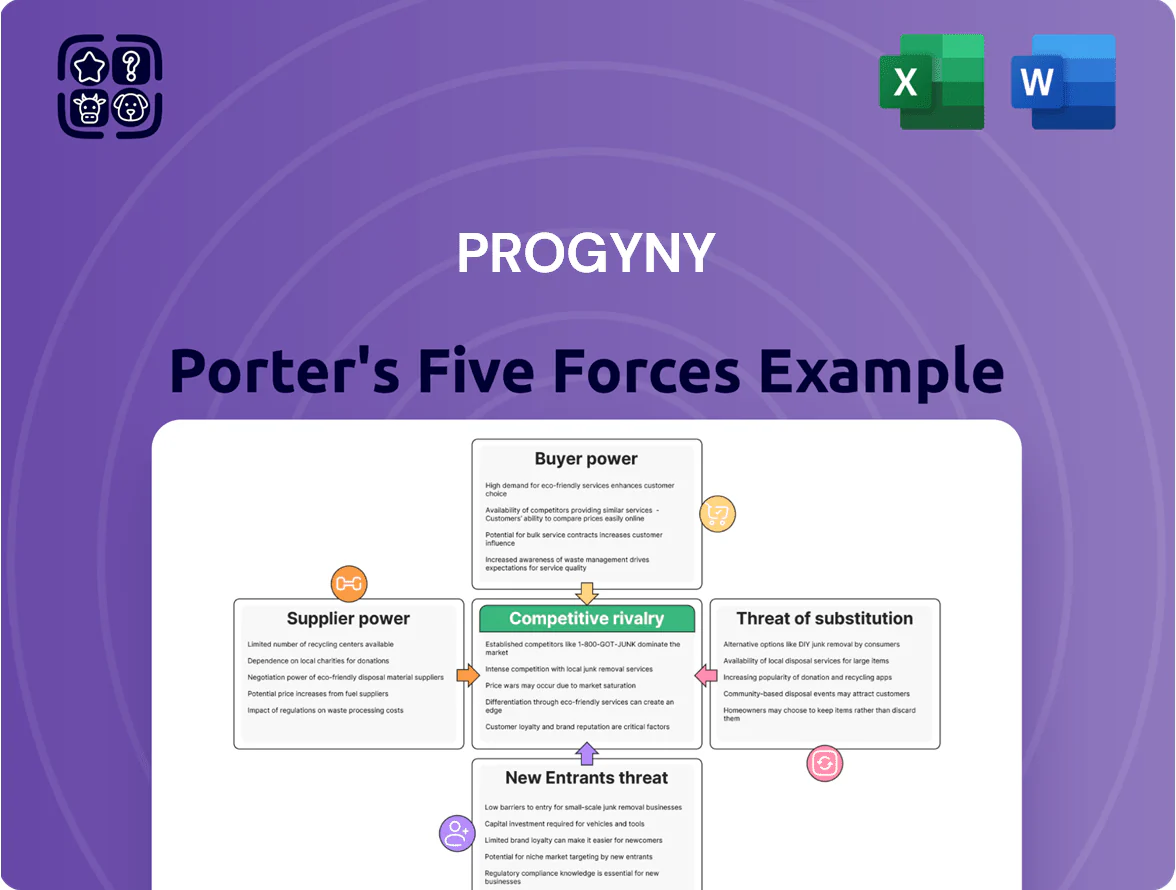

Progyny faces moderate bargaining power from large corporate buyers and payers, high competitive rivalry among fertility benefit managers and clinics, and evolving substitute threats from alternative fertility solutions and telehealth innovations.

Supplier power is tempered by clinic fragmentation but constrained by specialized medical services, while regulatory and technological barriers limit new entrants—yet capital-light digital competitors could disrupt pricing and margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Progyny’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Premier Fertility Clinics

Progyny depends on a curated network of ~150 high-performing fertility clinics that drive >70% of successful outcomes; this concentration gives premier clinics leverage despite Progyny’s referral volume. Top-tier reproductive specialists have limited capacity—average wait times rose to 8–12 weeks in 2024—so clinics can sustain premium pricing. By end-2025, estimated shortfall of 2,500 reproductive endocrinologists in the U.S. keeps supplier bargaining power high. Higher clinic pricing pressures Progyny’s unit economics unless offset by negotiated bundles or volume discounts.

Dependence on Specialized Pharmaceutical Manufacturers

Progyny Rx relies on a handful of specialized pharma firms for biologic fertility drugs, and with biologics making up roughly 70% of IVF drug spend industry-wide (2024 IQVIA), supplier concentration gives makers strong pricing power.

Few generics exist for these high-cost injectables; in 2024 average cycle drug costs exceeded $3,500, so manufacturer price hikes or supply disruptions can compress Progyny’s pharmacy-margin and raise client costs.

Influence of Specialized Medical Professionals

The supply of board-certified reproductive endocrinologists in North America is tight—AAMC data show a <10% annual increase in demand for fertility care vs ~1–2% supply growth—letting specialists and clinic directors push for higher pay and better referral terms; Progyny reported provider network margins pressured in 2024, and as it expands geographically, securing specialists at sustainable cost will be a key bottleneck to scaling operations.

Technological and Data Infrastructure Providers

Progyny relies on advanced analytics and telehealth platforms to track outcomes; in 2024 its platform processed over 120,000 patient interactions, tying clinical success metrics to vendor systems.

Vendors hold leverage via high switching costs, strict HIPAA (HIPAA: Health Insurance Portability and Accountability Act) obligations, and estimated migration costs exceeding $5–10M plus 6–12 months of operational risk.

Any supplier change risks data migration failures, service disruption, and regulatory exposure, making supplier power materially high.

- 120,000+ patient interactions (2024)

- Estimated migration cost $5–10M

- Switch time 6–12 months

- High HIPAA compliance risk

Labor Market Competition for Patient Care Advocates

Progyny’s high-touch Patient Care Advocates are central to its fertility benefit; demand for skilled healthcare coordinators grew 12% in the US healthcare workforce from 2019–2024, giving these workers collective leverage to push wages up.

To keep quality and avoid costly turnover—average replacement cost per clinical staff is 20–30% of annual salary—Progyny must invest in pay, training, and retention, squeezing margins or raising prices.

- Advocate-dependent model increases supplier (labor) power

- US coordinator workforce +12% (2019–2024)

- Replacement cost 20–30% of salary

- Requires higher labour spend, impacts margins

Clinic & biologic concentration, long waits and high migration costs squeeze Progyny margins

Suppliers exert high bargaining power: ~150 clinics drive >70% outcomes, 8–12 week waits (2024), projected shortfall of 2,500 REIs by end-2025, and biologics = ~70% of IVF drug spend (IQVIA 2024); clinic and drug concentration, scarce patient‑care advocates, high switching/migration costs ($5–10M, 6–12 months), and average cycle drug cost >$3,500 compress Progyny’s margins.

| Metric | Value |

|---|---|

| Clinics driving outcomes | ~150 |

| % outcomes from network | >70% |

| REI shortfall (end‑2025) | 2,500 |

| Wait times (2024) | 8–12 weeks |

| Biologics share of drug spend (2024) | ~70% |

| Avg cycle drug cost (2024) | >$3,500 |

| Migration cost / time | $5–10M / 6–12 mo |

| Patient interactions (2024) | 120,000+ |

What is included in the product

Tailored Porter's Five Forces analysis for Progyny that uncovers competitive drivers, supplier and buyer power, threat of entry and substitutes, and identifies disruptive forces and strategic levers to protect and grow market share.

Clear, one-sheet Porter's Five Forces tailored to Progyny—instantly highlight competitive threats and partnership opportunities to streamline strategic decisions.

Customers Bargaining Power

Leverage of Large Self-Insured Employers

Large self-insured employers—Progyny’s primary customers—hold strong leverage, often covering 5,000–100,000 employees and negotiating steep volume discounts and bespoke reporting for utilization and outcomes.

These buyers demand transparent KPIs; in 2024 employer audits of fertility benefits rose ~28%, and clients press for per-member-per-year pricing tied to clinical success and total cost of care.

Consolidation of Health Insurance Carriers

Progyny relies on partnerships with large health plans, but consolidation concentrates distribution power: the top five US carriers (UnitedHealth, Anthem, Aetna/CVS, Cigna, Humana) covered about 70% of employer-based insured lives in 2024, so carriers can demand deeper discounts or exclusivity.

If a major carrier builds an internal fertility program, Progyny’s addressable market to mid-to-large employers could shrink materially; a 2023 Willis Towers Watson survey found 48% of employers prefer carrier-managed benefits, raising churn risk for vendors.

Increased Sensitivity to Benefit Costs

By late 2025, 62% of surveyed HR buyers report tighter budgets and demand transparent pricing for specialized benefits; many threaten switching to lower-cost, digital-only fertility vendors if premiums rise more than 8% year-over-year. This forces Progyny to tie its higher clinical success—reported 35% greater live-birth rates in employer cohorts—to total-cost-of-care savings, often shown as 12–18% lower downstream maternity and infertility spend.

Demand for Global Benefit Parity

Multinational employers now demand uniform fertility benefits across regions, forcing Progyny to scale international operations quickly or risk losing deals to competitors with established global footprints like Carrot and Maven; 62% of Fortune 500 companies reported pushing for global parity in 2024, per Mercer.

Customers leverage global scale to negotiate multi-jurisdictional coverage, driving price pressure and requiring Progyny to meet diverse regulatory, reimbursement, and data‑privacy rules across 30+ target markets to retain contracts.

- 62% of Fortune 500 want global parity (Mercer 2024)

- Competitors with global presence: Carrot, Maven

- Needs compliance across 30+ markets

- Raises price and operational pressure on Progyny

Availability of Alternative Benefit Models

Employers now choose from reimbursement-only accounts, direct-to-clinic deals, and specialty vendors, cutting reliance on managed-care fertility models and raising buyer power.

Unbundling lets employers pick IVF, egg-freezing, or benefits administration separately, boosting leverage at renewals; 2024 surveys show 38% of employers offered at least one alternative model and plan-switching rose 14% year-over-year.

Here’s the quick math: if 40% of renewals face multi-vendor bids, Progyny’s pricing leverage falls accordingly—so retention must hinge on measurable outcomes and integration.

- 38% of employers used alternative models in 2024

- 14% increase in plan-switching YoY

- Multi-vendor bidding in ~40% of renewals

Employers Demand Outcome-Tied Fertility Pricing as Multi-Vendor Bids Rise

Large self-insured employers and consolidated carriers exert high leverage, demanding outcome-tied pricing, audits, and global parity; 2024–25 data: 62% Fortune 500 want global parity (Mercer 2024), 48% prefer carrier-managed benefits (Willis Towers Watson 2023), 38% used alternative models in 2024; multi-vendor bids hit ~40% of renewals, pressuring Progyny to prove 12–18% total-cost savings.

| Metric | Value |

|---|---|

| Fortune 500 demand | 62% |

| Prefer carrier-managed | 48% |

| Alt models used | 38% |

| Multi-vendor renewals | ~40% |

| Claimed TCoC savings | 12–18% |

Full Version Awaits

Progyny Porter's Five Forces Analysis

This preview shows the exact Progyny Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download upon purchase with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Progyny faces moderate bargaining power from large corporate buyers and payers, high competitive rivalry among fertility benefit managers and clinics, and evolving substitute threats from alternative fertility solutions and telehealth innovations.

Supplier power is tempered by clinic fragmentation but constrained by specialized medical services, while regulatory and technological barriers limit new entrants—yet capital-light digital competitors could disrupt pricing and margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Progyny’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Premier Fertility Clinics

Progyny depends on a curated network of ~150 high-performing fertility clinics that drive >70% of successful outcomes; this concentration gives premier clinics leverage despite Progyny’s referral volume. Top-tier reproductive specialists have limited capacity—average wait times rose to 8–12 weeks in 2024—so clinics can sustain premium pricing. By end-2025, estimated shortfall of 2,500 reproductive endocrinologists in the U.S. keeps supplier bargaining power high. Higher clinic pricing pressures Progyny’s unit economics unless offset by negotiated bundles or volume discounts.

Dependence on Specialized Pharmaceutical Manufacturers

Progyny Rx relies on a handful of specialized pharma firms for biologic fertility drugs, and with biologics making up roughly 70% of IVF drug spend industry-wide (2024 IQVIA), supplier concentration gives makers strong pricing power.

Few generics exist for these high-cost injectables; in 2024 average cycle drug costs exceeded $3,500, so manufacturer price hikes or supply disruptions can compress Progyny’s pharmacy-margin and raise client costs.

Influence of Specialized Medical Professionals

The supply of board-certified reproductive endocrinologists in North America is tight—AAMC data show a <10% annual increase in demand for fertility care vs ~1–2% supply growth—letting specialists and clinic directors push for higher pay and better referral terms; Progyny reported provider network margins pressured in 2024, and as it expands geographically, securing specialists at sustainable cost will be a key bottleneck to scaling operations.

Technological and Data Infrastructure Providers

Progyny relies on advanced analytics and telehealth platforms to track outcomes; in 2024 its platform processed over 120,000 patient interactions, tying clinical success metrics to vendor systems.

Vendors hold leverage via high switching costs, strict HIPAA (HIPAA: Health Insurance Portability and Accountability Act) obligations, and estimated migration costs exceeding $5–10M plus 6–12 months of operational risk.

Any supplier change risks data migration failures, service disruption, and regulatory exposure, making supplier power materially high.

- 120,000+ patient interactions (2024)

- Estimated migration cost $5–10M

- Switch time 6–12 months

- High HIPAA compliance risk

Labor Market Competition for Patient Care Advocates

Progyny’s high-touch Patient Care Advocates are central to its fertility benefit; demand for skilled healthcare coordinators grew 12% in the US healthcare workforce from 2019–2024, giving these workers collective leverage to push wages up.

To keep quality and avoid costly turnover—average replacement cost per clinical staff is 20–30% of annual salary—Progyny must invest in pay, training, and retention, squeezing margins or raising prices.

- Advocate-dependent model increases supplier (labor) power

- US coordinator workforce +12% (2019–2024)

- Replacement cost 20–30% of salary

- Requires higher labour spend, impacts margins

Clinic & biologic concentration, long waits and high migration costs squeeze Progyny margins

Suppliers exert high bargaining power: ~150 clinics drive >70% outcomes, 8–12 week waits (2024), projected shortfall of 2,500 REIs by end-2025, and biologics = ~70% of IVF drug spend (IQVIA 2024); clinic and drug concentration, scarce patient‑care advocates, high switching/migration costs ($5–10M, 6–12 months), and average cycle drug cost >$3,500 compress Progyny’s margins.

| Metric | Value |

|---|---|

| Clinics driving outcomes | ~150 |

| % outcomes from network | >70% |

| REI shortfall (end‑2025) | 2,500 |

| Wait times (2024) | 8–12 weeks |

| Biologics share of drug spend (2024) | ~70% |

| Avg cycle drug cost (2024) | >$3,500 |

| Migration cost / time | $5–10M / 6–12 mo |

| Patient interactions (2024) | 120,000+ |

What is included in the product

Tailored Porter's Five Forces analysis for Progyny that uncovers competitive drivers, supplier and buyer power, threat of entry and substitutes, and identifies disruptive forces and strategic levers to protect and grow market share.

Clear, one-sheet Porter's Five Forces tailored to Progyny—instantly highlight competitive threats and partnership opportunities to streamline strategic decisions.

Customers Bargaining Power

Leverage of Large Self-Insured Employers

Large self-insured employers—Progyny’s primary customers—hold strong leverage, often covering 5,000–100,000 employees and negotiating steep volume discounts and bespoke reporting for utilization and outcomes.

These buyers demand transparent KPIs; in 2024 employer audits of fertility benefits rose ~28%, and clients press for per-member-per-year pricing tied to clinical success and total cost of care.

Consolidation of Health Insurance Carriers

Progyny relies on partnerships with large health plans, but consolidation concentrates distribution power: the top five US carriers (UnitedHealth, Anthem, Aetna/CVS, Cigna, Humana) covered about 70% of employer-based insured lives in 2024, so carriers can demand deeper discounts or exclusivity.

If a major carrier builds an internal fertility program, Progyny’s addressable market to mid-to-large employers could shrink materially; a 2023 Willis Towers Watson survey found 48% of employers prefer carrier-managed benefits, raising churn risk for vendors.

Increased Sensitivity to Benefit Costs

By late 2025, 62% of surveyed HR buyers report tighter budgets and demand transparent pricing for specialized benefits; many threaten switching to lower-cost, digital-only fertility vendors if premiums rise more than 8% year-over-year. This forces Progyny to tie its higher clinical success—reported 35% greater live-birth rates in employer cohorts—to total-cost-of-care savings, often shown as 12–18% lower downstream maternity and infertility spend.

Demand for Global Benefit Parity

Multinational employers now demand uniform fertility benefits across regions, forcing Progyny to scale international operations quickly or risk losing deals to competitors with established global footprints like Carrot and Maven; 62% of Fortune 500 companies reported pushing for global parity in 2024, per Mercer.

Customers leverage global scale to negotiate multi-jurisdictional coverage, driving price pressure and requiring Progyny to meet diverse regulatory, reimbursement, and data‑privacy rules across 30+ target markets to retain contracts.

- 62% of Fortune 500 want global parity (Mercer 2024)

- Competitors with global presence: Carrot, Maven

- Needs compliance across 30+ markets

- Raises price and operational pressure on Progyny

Availability of Alternative Benefit Models

Employers now choose from reimbursement-only accounts, direct-to-clinic deals, and specialty vendors, cutting reliance on managed-care fertility models and raising buyer power.

Unbundling lets employers pick IVF, egg-freezing, or benefits administration separately, boosting leverage at renewals; 2024 surveys show 38% of employers offered at least one alternative model and plan-switching rose 14% year-over-year.

Here’s the quick math: if 40% of renewals face multi-vendor bids, Progyny’s pricing leverage falls accordingly—so retention must hinge on measurable outcomes and integration.

- 38% of employers used alternative models in 2024

- 14% increase in plan-switching YoY

- Multi-vendor bidding in ~40% of renewals

Employers Demand Outcome-Tied Fertility Pricing as Multi-Vendor Bids Rise

Large self-insured employers and consolidated carriers exert high leverage, demanding outcome-tied pricing, audits, and global parity; 2024–25 data: 62% Fortune 500 want global parity (Mercer 2024), 48% prefer carrier-managed benefits (Willis Towers Watson 2023), 38% used alternative models in 2024; multi-vendor bids hit ~40% of renewals, pressuring Progyny to prove 12–18% total-cost savings.

| Metric | Value |

|---|---|

| Fortune 500 demand | 62% |

| Prefer carrier-managed | 48% |

| Alt models used | 38% |

| Multi-vendor renewals | ~40% |

| Claimed TCoC savings | 12–18% |

Full Version Awaits

Progyny Porter's Five Forces Analysis

This preview shows the exact Progyny Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download upon purchase with no placeholders or mockups.