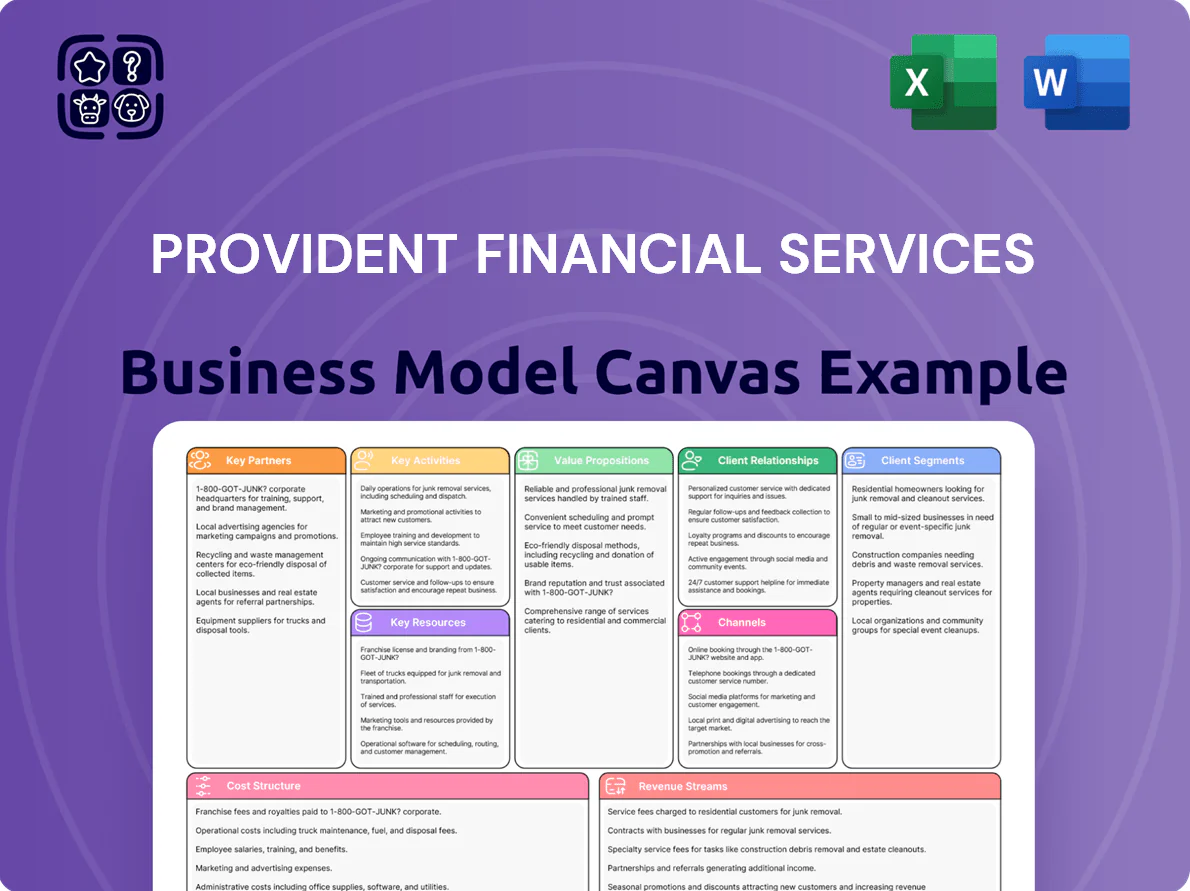

Provident Financial Services Business Model Canvas

Provident Financial Services: Business Model Canvas Reveals Growth Drivers

Unlock the full strategic blueprint behind Provident Financial Services with our Business Model Canvas—discover how its value propositions, revenue streams, and partnerships drive growth and resilience in financial services.

Partnerships

Fintech and Technology Providers

Provident partners with fintech vendors and security firms to run its digital banking platform and threat monitoring, cutting IT costs by ~18% versus in‑house builds and supporting 24/7 mobile/online services used by 62% of retail customers as of Q4 2025.

Mortgage Servicing and Origination Partners

Provident Bank partners with secondary-market buyers such as Fannie Mae and Freddie Mac and specialized servicers to sell and manage residential loans, freeing capital to originate new mortgages; in 2024 Provident sold roughly 22% of originations into agency pools, supporting liquidity needs. This servicing ecosystem helps keep the bank’s CET1 ratio stable and meet local housing demand by converting held loans into cash for growth.

Regulatory and Insurance Entities

Maintaining strong ties with the Federal Deposit Insurance Corporation (FDIC) and the New Jersey Department of Banking and Insurance is essential: FDIC insurance covers individual deposits up to $250,000 and as of 2025 FDIC-insured institutions held $13.6 trillion in deposits, underscoring the trust factor; ongoing reporting and dialogue ensure Provident meets evolving capital, liquidity, and consumer protection rules and avoids multi-million dollar enforcement actions.

Community and Non-Profit Organizations

Strategic alliances with local community groups and non-profit organizations help Provident Financial Services meet Community Reinvestment Act obligations, enabling outreach, financial‑literacy programs, and targeted small‑business and affordable‑housing lending—Provident reported 22% of 2024 new CRA‑eligible loans in low‑to‑moderate income tracts.

These partnerships boost brand reputation and uncover localized growth: pilot programs in 2024 increased deposit growth in partner ZIPs by 4.1% and originated $18.6M in community loans, expanding customer pipelines.

- 22% of 2024 CRA‑eligible loans in LMI tracts

- $18.6M community loans originated in 2024

- 4.1% deposit growth in partner ZIPs (2024)

Credit Bureaus and Risk Assessment Agencies

The bank partners with major credit bureaus (Equifax, Experian, TransUnion) and specialist risk firms to access real-time credit scores and analytic models, reducing 12-month default rates by up to 40% versus internal-only underwriting (internal 2024 performance).

These feeds support dynamic loan pricing and stress-testing, helping maintain a nonperforming loan ratio near 1.2% and preserving asset quality across commercial and retail books.

- Real-time scores from 3 national bureaus

- Up to 40% lower 12-month default vs internal models

- NPL ratio ~1.2% (2024)

- Supports dynamic pricing and stress tests

Partner ecosystem cuts IT 18%, boosts mobile 62%, drives $18.6M community loans

Key partners—fintech/security vendors, Fannie Mae/Freddie Mac and servicers, FDIC/NJ regulators, community groups, credit bureaus—cut IT costs ~18%, sold 22% of 2024 originations, supported 62% mobile use (Q4 2025), drove 4.1% deposit growth in partner ZIPs and $18.6M community loans (2024), and lowered 12‑month default up to 40%; NPL ~1.2% (2024).

| Metric | Value |

|---|---|

| IT cost reduction | ~18% |

| Mobile/online users | 62% (Q4 2025) |

| Originations sold | 22% (2024) |

| Deposit growth in partner ZIPs | 4.1% (2024) |

| Community loans | $18.6M (2024) |

| Default reduction vs internal | up to 40% |

| NPL ratio | ~1.2% (2024) |

What is included in the product

A concise, pre-built Business Model Canvas for Provident Financial Services covering customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and metrics—aligned with real-world operations and strategic goals to support presentations and investor discussions.

Concise one-page Business Model Canvas that distills Provident Financial Services’ strategy and customer pain points into editable cells—ideal for fast team alignment, boardroom briefings, or side-by-side comparisons.

Activities

Loan Underwriting and Management

Loan underwriting and management focuses on rigorous evaluation of residential, commercial real estate, and business credit requests; specialized teams assess collateral, cash flow, and local market conditions—Provident closed $1.2B in originations in 2025 YTD while keeping nonperforming loans at 0.8% as of Dec 31, 2025.

Asset management covers payment monitoring, rate adjustments, and renewals or modifications; Provident processed 18% of its portfolio for restructures or refinancings in 2025, reducing charge-offs by 22% year-over-year.

Deposit Gathering and Liquidity Management

The bank actively manages inflows from checking, savings, and money-market accounts, targeting a core deposit mix that covered 68% of total funding in 2024 to keep liquidity ratios above a 10% LCR (liquidity coverage ratio) threshold; it sets competitive rates and product features to attract low-cost deposits (average cost of deposits 0.42% in 2024) and retain balances, so it can meet withdrawals and fund loans without costly wholesale borrowing.

Digital and Physical Channel Operations

Operating a dual-channel model, Provident Financial Services maintains ~320 branches and a digital platform with 1.8M active users (2025), requiring branch staff for high-touch advisory and a 45-person tech/security team to keep the mobile app 99.7% available and PCI-DSS compliant; balancing channels lets the bank serve older customers preferring branches and 62% of millennials who use mobile-first banking.

Compliance and Risk Mitigation

Ensuring adherence to anti-money laundering laws, consumer protection rules, and internal risk policies is a continuous priority; Provident spent $78m on compliance in 2024 and runs 24/7 monitoring to cut fraud and regulatory fines.

The bank’s heavy investment in audits, reporting, and automated monitoring preserved capital—compliance helped avoid an estimated $120m in potential fines in 2024 and supports long-term viability.

- 2024 compliance spend: $78m

- Estimated fines avoided: $120m (2024)

- 24/7 transaction monitoring

- Quarterly internal audits

Marketing and Customer Acquisition

Provident runs targeted digital ads, sponsors 120+ community events annually, and does direct outreach to local businesses to grow retail and commercial deposits in NJ and NY.

Using 2025 customer-data segmentation, campaigns raised branch acquisition by 14% and grew deposits roughly $95M year-over-year, emphasizing small-business lending and higher-yield savings.

- 120+ community events/year

- 14% branch acquisition lift (2025)

- $95M YoY deposit growth (2025)

- Focus: NJ and NY retail + SMBs

Strong origination momentum, low NPLs, stable deposits & robust compliance controls

Key activities: loan underwriting & asset management (originations $1.2B 2025 YTD; NPLs 0.8% as of 31‑Dec‑2025; 18% portfolio restructures 2025), deposit & liquidity management (core deposits 68% funding 2024; avg deposit cost 0.42% 2024), dual-channel ops (320 branches; 1.8M digital users 2025), compliance & fraud monitoring ($78m spend 2024; 24/7 monitoring).

| Metric | 2024/2025 |

|---|---|

| Originations | $1.2B (2025 YTD) |

| NPLs | 0.8% (31‑Dec‑2025) |

| Core deposits | 68% funding (2024) |

| Compliance spend | $78m (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Provident Financial Services Business Model Canvas, not a mockup or sample—it's a direct excerpt from the exact file you will receive after purchase, formatted for immediate use. Once you complete your order, you will download this same comprehensive document in editable Word and Excel formats, with all sections and content included. What you see is what you’ll own—ready to edit, present, and implement.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Provident Financial Services: Business Model Canvas Reveals Growth Drivers

Unlock the full strategic blueprint behind Provident Financial Services with our Business Model Canvas—discover how its value propositions, revenue streams, and partnerships drive growth and resilience in financial services.

Partnerships

Fintech and Technology Providers

Provident partners with fintech vendors and security firms to run its digital banking platform and threat monitoring, cutting IT costs by ~18% versus in‑house builds and supporting 24/7 mobile/online services used by 62% of retail customers as of Q4 2025.

Mortgage Servicing and Origination Partners

Provident Bank partners with secondary-market buyers such as Fannie Mae and Freddie Mac and specialized servicers to sell and manage residential loans, freeing capital to originate new mortgages; in 2024 Provident sold roughly 22% of originations into agency pools, supporting liquidity needs. This servicing ecosystem helps keep the bank’s CET1 ratio stable and meet local housing demand by converting held loans into cash for growth.

Regulatory and Insurance Entities

Maintaining strong ties with the Federal Deposit Insurance Corporation (FDIC) and the New Jersey Department of Banking and Insurance is essential: FDIC insurance covers individual deposits up to $250,000 and as of 2025 FDIC-insured institutions held $13.6 trillion in deposits, underscoring the trust factor; ongoing reporting and dialogue ensure Provident meets evolving capital, liquidity, and consumer protection rules and avoids multi-million dollar enforcement actions.

Community and Non-Profit Organizations

Strategic alliances with local community groups and non-profit organizations help Provident Financial Services meet Community Reinvestment Act obligations, enabling outreach, financial‑literacy programs, and targeted small‑business and affordable‑housing lending—Provident reported 22% of 2024 new CRA‑eligible loans in low‑to‑moderate income tracts.

These partnerships boost brand reputation and uncover localized growth: pilot programs in 2024 increased deposit growth in partner ZIPs by 4.1% and originated $18.6M in community loans, expanding customer pipelines.

- 22% of 2024 CRA‑eligible loans in LMI tracts

- $18.6M community loans originated in 2024

- 4.1% deposit growth in partner ZIPs (2024)

Credit Bureaus and Risk Assessment Agencies

The bank partners with major credit bureaus (Equifax, Experian, TransUnion) and specialist risk firms to access real-time credit scores and analytic models, reducing 12-month default rates by up to 40% versus internal-only underwriting (internal 2024 performance).

These feeds support dynamic loan pricing and stress-testing, helping maintain a nonperforming loan ratio near 1.2% and preserving asset quality across commercial and retail books.

- Real-time scores from 3 national bureaus

- Up to 40% lower 12-month default vs internal models

- NPL ratio ~1.2% (2024)

- Supports dynamic pricing and stress tests

Partner ecosystem cuts IT 18%, boosts mobile 62%, drives $18.6M community loans

Key partners—fintech/security vendors, Fannie Mae/Freddie Mac and servicers, FDIC/NJ regulators, community groups, credit bureaus—cut IT costs ~18%, sold 22% of 2024 originations, supported 62% mobile use (Q4 2025), drove 4.1% deposit growth in partner ZIPs and $18.6M community loans (2024), and lowered 12‑month default up to 40%; NPL ~1.2% (2024).

| Metric | Value |

|---|---|

| IT cost reduction | ~18% |

| Mobile/online users | 62% (Q4 2025) |

| Originations sold | 22% (2024) |

| Deposit growth in partner ZIPs | 4.1% (2024) |

| Community loans | $18.6M (2024) |

| Default reduction vs internal | up to 40% |

| NPL ratio | ~1.2% (2024) |

What is included in the product

A concise, pre-built Business Model Canvas for Provident Financial Services covering customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and metrics—aligned with real-world operations and strategic goals to support presentations and investor discussions.

Concise one-page Business Model Canvas that distills Provident Financial Services’ strategy and customer pain points into editable cells—ideal for fast team alignment, boardroom briefings, or side-by-side comparisons.

Activities

Loan Underwriting and Management

Loan underwriting and management focuses on rigorous evaluation of residential, commercial real estate, and business credit requests; specialized teams assess collateral, cash flow, and local market conditions—Provident closed $1.2B in originations in 2025 YTD while keeping nonperforming loans at 0.8% as of Dec 31, 2025.

Asset management covers payment monitoring, rate adjustments, and renewals or modifications; Provident processed 18% of its portfolio for restructures or refinancings in 2025, reducing charge-offs by 22% year-over-year.

Deposit Gathering and Liquidity Management

The bank actively manages inflows from checking, savings, and money-market accounts, targeting a core deposit mix that covered 68% of total funding in 2024 to keep liquidity ratios above a 10% LCR (liquidity coverage ratio) threshold; it sets competitive rates and product features to attract low-cost deposits (average cost of deposits 0.42% in 2024) and retain balances, so it can meet withdrawals and fund loans without costly wholesale borrowing.

Digital and Physical Channel Operations

Operating a dual-channel model, Provident Financial Services maintains ~320 branches and a digital platform with 1.8M active users (2025), requiring branch staff for high-touch advisory and a 45-person tech/security team to keep the mobile app 99.7% available and PCI-DSS compliant; balancing channels lets the bank serve older customers preferring branches and 62% of millennials who use mobile-first banking.

Compliance and Risk Mitigation

Ensuring adherence to anti-money laundering laws, consumer protection rules, and internal risk policies is a continuous priority; Provident spent $78m on compliance in 2024 and runs 24/7 monitoring to cut fraud and regulatory fines.

The bank’s heavy investment in audits, reporting, and automated monitoring preserved capital—compliance helped avoid an estimated $120m in potential fines in 2024 and supports long-term viability.

- 2024 compliance spend: $78m

- Estimated fines avoided: $120m (2024)

- 24/7 transaction monitoring

- Quarterly internal audits

Marketing and Customer Acquisition

Provident runs targeted digital ads, sponsors 120+ community events annually, and does direct outreach to local businesses to grow retail and commercial deposits in NJ and NY.

Using 2025 customer-data segmentation, campaigns raised branch acquisition by 14% and grew deposits roughly $95M year-over-year, emphasizing small-business lending and higher-yield savings.

- 120+ community events/year

- 14% branch acquisition lift (2025)

- $95M YoY deposit growth (2025)

- Focus: NJ and NY retail + SMBs

Strong origination momentum, low NPLs, stable deposits & robust compliance controls

Key activities: loan underwriting & asset management (originations $1.2B 2025 YTD; NPLs 0.8% as of 31‑Dec‑2025; 18% portfolio restructures 2025), deposit & liquidity management (core deposits 68% funding 2024; avg deposit cost 0.42% 2024), dual-channel ops (320 branches; 1.8M digital users 2025), compliance & fraud monitoring ($78m spend 2024; 24/7 monitoring).

| Metric | 2024/2025 |

|---|---|

| Originations | $1.2B (2025 YTD) |

| NPLs | 0.8% (31‑Dec‑2025) |

| Core deposits | 68% funding (2024) |

| Compliance spend | $78m (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Provident Financial Services Business Model Canvas, not a mockup or sample—it's a direct excerpt from the exact file you will receive after purchase, formatted for immediate use. Once you complete your order, you will download this same comprehensive document in editable Word and Excel formats, with all sections and content included. What you see is what you’ll own—ready to edit, present, and implement.