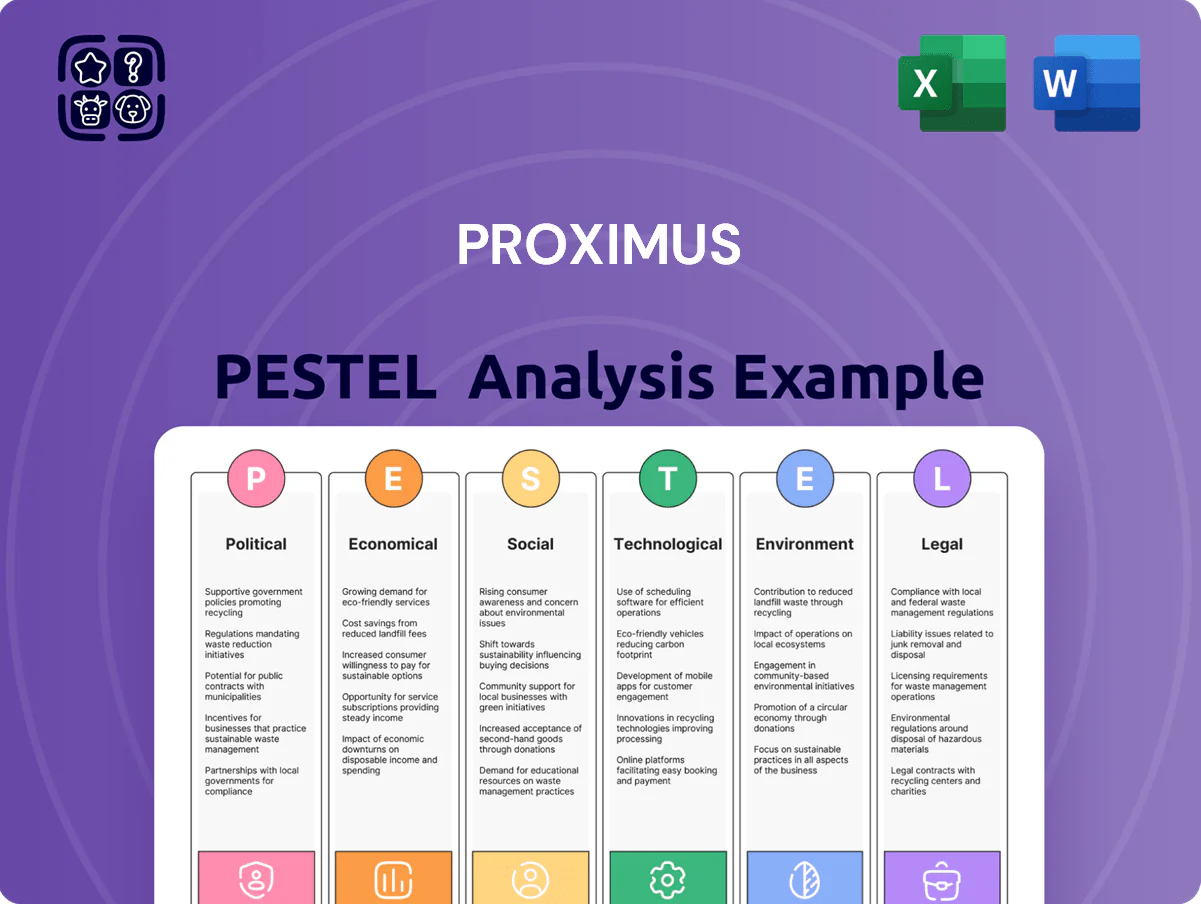

Proximus PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political, economic, and technological forces shape Proximus’s strategy and performance with our concise PESTLE snapshot—crafted for investors, consultants, and strategists; buy the full analysis to access detailed risks, opportunities, and actionable recommendations ready for immediate use.

Political factors

Government majority shareholding

The Belgian State holds 53.1 percent of Proximus, creating a direct link between corporate strategy and national interest and ensuring alignment with public service obligations.

This majority stake supports long-term infrastructure spending—Proximus invested €1.1 billion in 2024 capex—but can prompt political influence over management, dividend policy (€0.72 per share in 2024) and strategic choices.

As of late 2025, state control stabilizes funding for broadband rollout yet may slow rapid market-driven pivots and M&A decisions.

EU digital sovereignty initiatives

The EU’s digital sovereignty drive steers Proximus toward EU-based vendors and stricter data residency, affecting partner selection and data handling amid 2024 rules like the EU Cybersecurity Act and NIS2; compliance adds estimated procurement premium of 5–12% versus non-EU suppliers.

Geopolitical vendor restrictions

Ongoing geopolitical tensions over high-risk vendors have led Proximus to phase out certain international hardware for core networks, triggering reinvestment of about €300–€400 million through 2024–2025 into western-aligned technology to comply with Belgian and EU security mandates; this has increased capex intensity and required reshaping supplier partnerships to safeguard the Belgian communications backbone.

Regional infrastructure coordination

Operating across Flanders, Wallonia and Brussels forces Proximus to navigate three sets of permit regimes; Flanders fast-tracked ~70% of fiber permits in 2024 versus ~45% in Wallonia, impacting rollout speed.

Each region enforces different antenna radiation limits and zoning rules, raising compliance costs—regional regulatory variation contributed to a €60–€120 million annual variance in rollout capex estimates for 2025–2027.

Stable regional politics is critical to hit Proximus’ 2025–2030 coverage targets (aiming for 95% fixed NGA by 2030); political delays could shift timelines and increase costs materially.

- Three authorities — distinct permits and radiation standards

- 2024 permit fast-track: Flanders ~70%, Wallonia ~45%

- Regional variance added €60–€120M/year to rollout capex estimates

- Political stability vital to achieve 95% NGA by 2030

International subsidiary exposure

Through subsidiaries Telesign and BICS, Proximus generates significant international revenue—Telesign reported about USD 480m revenue in 2024 and BICS contributed roughly EUR 440m—exposing Proximus to U.S. digital policy shifts and sanctions in emerging markets.

Changes in trade rules, sanctions or data localization (e.g., U.S. export controls, India’s 2024 digital rules) can reduce EBITDA of these units and impact group guidance.

Management must monitor geopolitical risk, hedge currency and contract exposure, and adjust customer diversification to protect margins.

- 2024 Telesign revenue ~USD 480m; BICS ~EUR 440m

- Risk drivers: U.S. digital policy, sanctions, data localization

- Mitigations: hedging, diversification, contractual clauses

State 53.1% stake, €1.1bn capex, higher procurement costs and regional capex swings

State 53.1% stake ties strategy to public interest; 2024 capex €1.1bn, dividend €0.72/share. EU rules (NIS2, Cybersecurity Act) and vendor bans raised procurement costs ~5–12% and drove €300–400m reinvestment 2024–25. Regional permit variance (Flanders ~70% fast-track, Wallonia ~45%) added €60–120m/year to rollout capex; Telesign revenue ~USD480m, BICS ~€440m in 2024.

| Metric | 2024/25 |

|---|---|

| State stake | 53.1% |

| Capex | €1.1bn |

| Procurement premium | 5–12% |

| Reinvestment | €300–400m |

| Permit fast-track (Flanders) | ~70% |

| Permit fast-track (Wallonia) | ~45% |

| Regional capex variance | €60–120m/yr |

| Telesign rev | USD480m |

| BICS rev | €440m |

What is included in the product

Explores how macro-environmental factors uniquely affect Proximus across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting to support executives, consultants and investors in identifying risks, opportunities and strategic priorities.

A concise, visually segmented Proximus PESTLE summary that eases meeting prep and supports quick alignment across teams by highlighting key regulatory, technological, and market risks.

Economic factors

Automatic wage indexation

The Belgian automatic wage indexation ties salaries to inflation, which rose to 9.5% in 2022 and averaged about 6% in 2023–2024, directly increasing Proximus labor costs; as one of Belgium’s largest employers (≈12,000 staff), this amplified wage bills pressurize EBITDA margins—Proximus reported adjusted EBITDA margin of ~37% in 2023. The company must offset indexation via productivity improvements, network automation, and selective price increases to protect profitability.

High capital expenditure for fiber

Proximus is in the final stages of a multi-year Fiber-to-the-Home rollout that cost roughly EUR 2.7–3.0 billion to date; by end-2025 the remaining capex and related financing keep analysts focused on a reported 2024 net debt/EBITDA around 2.6x and debt-to-equity pressure. The economic payoff hinges on migrating subscribers to higher ARPU fiber plans (fixed broadband ARPU uplift potential 10–20%) and retiring copper to cut OPEX and accelerate ROI.

Entrance of a fourth mobile operator

The entry of Digi in 2024 shifted Belgium from three to four mobile operators, triggering intensified price competition and a 3-5% decline in market-wide ARPU in 2024 according to industry reports.

For Proximus this economic pressure mandates differentiation via quality, fixed-mobile bundling and value-added services rather than price cuts to protect margins.

Management must prioritize premium packages and loyalty programs; Proximus reported a 1.2% fall in consumer mobile ARPU H1 2025, underscoring urgency for retention and upsell strategies.

B2B digital transformation spending

Enterprise spending on cloud, cybersecurity and managed ICT rose across Europe; IDC reported European cloud spending hit about €100bn in 2024, with cybersecurity budgets growing ~9% YoY—Proximus positions as strategic partner offering cloud, security and managed services to capture this demand.

B2B revenue growth (Proximus B2B represented ~45% of service revenue in 2024) helps offset stagnant residential ARPU and intense price competition, stabilizing margins and supporting higher-value service upsells.

- Sustained enterprise demand: cloud, security, managed ICT

- IDC: €100bn EU cloud spend 2024; cybersecurity +9% YoY

- Proximus B2B ≈45% of service revenue in 2024

- B2B growth hedges saturated, price-sensitive residential market

Interest rate volatility

As a capital-intensive telecom with net debt around EUR 4.5bn (2025 guidance) Proximus is highly sensitive to ECB rate moves; a 100bps rise in rates can materially increase annual interest expense and depress enterprise valuation via higher WACC.

Higher borrowing costs could delay or scale back multi-year broadband and 5G investments; management uses interest rate swaps and caps to hedge exposure and protect cash flows.

Hedging supports dividend sustainability—Proximus paid EUR 1.00 per share in 2024—by smoothing financing costs amid rate volatility.

- Net debt ~EUR 4.5bn (2025 guidance)

- 100bps rate rise raises WACC and interest expense materially

- Swaps/caps used to hedge interest-rate risk

- Dividend EUR 1.00 in 2024; hedging preserves payout capacity

Proximus margins steady amid wage inflation and fiber spending; ARPU pressured by Digi

Belgian wage indexation (inflation 9.5% in 2022; ~6% avg 2023–24) raised Proximus labor costs; adjusted EBITDA margin ~37% in 2023. Fiber rollout capex ~EUR 2.7–3.0bn to date; net debt ~EUR 4.5bn (2025 guidance), net debt/EBITDA ~2.6x (2024). Digi entry cut ARPU 3–5% in 2024; Proximus B2B ≈45% service revenue (2024) offsets consumer pressure.

| Metric | Value |

|---|---|

| Adj. EBITDA margin (2023) | ~37% |

| Net debt (2025 guidance) | ~EUR 4.5bn |

| Net debt/EBITDA (2024) | ~2.6x |

| Fiber capex to date | EUR 2.7–3.0bn |

| ARPU decline post-Digi (2024) | 3–5% |

| B2B share (2024) | ~45% |

Same Document Delivered

Proximus PESTLE Analysis

The preview shown here is the exact Proximus PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview match the final file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how political, economic, and technological forces shape Proximus’s strategy and performance with our concise PESTLE snapshot—crafted for investors, consultants, and strategists; buy the full analysis to access detailed risks, opportunities, and actionable recommendations ready for immediate use.

Political factors

Government majority shareholding

The Belgian State holds 53.1 percent of Proximus, creating a direct link between corporate strategy and national interest and ensuring alignment with public service obligations.

This majority stake supports long-term infrastructure spending—Proximus invested €1.1 billion in 2024 capex—but can prompt political influence over management, dividend policy (€0.72 per share in 2024) and strategic choices.

As of late 2025, state control stabilizes funding for broadband rollout yet may slow rapid market-driven pivots and M&A decisions.

EU digital sovereignty initiatives

The EU’s digital sovereignty drive steers Proximus toward EU-based vendors and stricter data residency, affecting partner selection and data handling amid 2024 rules like the EU Cybersecurity Act and NIS2; compliance adds estimated procurement premium of 5–12% versus non-EU suppliers.

Geopolitical vendor restrictions

Ongoing geopolitical tensions over high-risk vendors have led Proximus to phase out certain international hardware for core networks, triggering reinvestment of about €300–€400 million through 2024–2025 into western-aligned technology to comply with Belgian and EU security mandates; this has increased capex intensity and required reshaping supplier partnerships to safeguard the Belgian communications backbone.

Regional infrastructure coordination

Operating across Flanders, Wallonia and Brussels forces Proximus to navigate three sets of permit regimes; Flanders fast-tracked ~70% of fiber permits in 2024 versus ~45% in Wallonia, impacting rollout speed.

Each region enforces different antenna radiation limits and zoning rules, raising compliance costs—regional regulatory variation contributed to a €60–€120 million annual variance in rollout capex estimates for 2025–2027.

Stable regional politics is critical to hit Proximus’ 2025–2030 coverage targets (aiming for 95% fixed NGA by 2030); political delays could shift timelines and increase costs materially.

- Three authorities — distinct permits and radiation standards

- 2024 permit fast-track: Flanders ~70%, Wallonia ~45%

- Regional variance added €60–€120M/year to rollout capex estimates

- Political stability vital to achieve 95% NGA by 2030

International subsidiary exposure

Through subsidiaries Telesign and BICS, Proximus generates significant international revenue—Telesign reported about USD 480m revenue in 2024 and BICS contributed roughly EUR 440m—exposing Proximus to U.S. digital policy shifts and sanctions in emerging markets.

Changes in trade rules, sanctions or data localization (e.g., U.S. export controls, India’s 2024 digital rules) can reduce EBITDA of these units and impact group guidance.

Management must monitor geopolitical risk, hedge currency and contract exposure, and adjust customer diversification to protect margins.

- 2024 Telesign revenue ~USD 480m; BICS ~EUR 440m

- Risk drivers: U.S. digital policy, sanctions, data localization

- Mitigations: hedging, diversification, contractual clauses

State 53.1% stake, €1.1bn capex, higher procurement costs and regional capex swings

State 53.1% stake ties strategy to public interest; 2024 capex €1.1bn, dividend €0.72/share. EU rules (NIS2, Cybersecurity Act) and vendor bans raised procurement costs ~5–12% and drove €300–400m reinvestment 2024–25. Regional permit variance (Flanders ~70% fast-track, Wallonia ~45%) added €60–120m/year to rollout capex; Telesign revenue ~USD480m, BICS ~€440m in 2024.

| Metric | 2024/25 |

|---|---|

| State stake | 53.1% |

| Capex | €1.1bn |

| Procurement premium | 5–12% |

| Reinvestment | €300–400m |

| Permit fast-track (Flanders) | ~70% |

| Permit fast-track (Wallonia) | ~45% |

| Regional capex variance | €60–120m/yr |

| Telesign rev | USD480m |

| BICS rev | €440m |

What is included in the product

Explores how macro-environmental factors uniquely affect Proximus across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, sector-specific examples, forward-looking insights for scenario planning, and clean formatting to support executives, consultants and investors in identifying risks, opportunities and strategic priorities.

A concise, visually segmented Proximus PESTLE summary that eases meeting prep and supports quick alignment across teams by highlighting key regulatory, technological, and market risks.

Economic factors

Automatic wage indexation

The Belgian automatic wage indexation ties salaries to inflation, which rose to 9.5% in 2022 and averaged about 6% in 2023–2024, directly increasing Proximus labor costs; as one of Belgium’s largest employers (≈12,000 staff), this amplified wage bills pressurize EBITDA margins—Proximus reported adjusted EBITDA margin of ~37% in 2023. The company must offset indexation via productivity improvements, network automation, and selective price increases to protect profitability.

High capital expenditure for fiber

Proximus is in the final stages of a multi-year Fiber-to-the-Home rollout that cost roughly EUR 2.7–3.0 billion to date; by end-2025 the remaining capex and related financing keep analysts focused on a reported 2024 net debt/EBITDA around 2.6x and debt-to-equity pressure. The economic payoff hinges on migrating subscribers to higher ARPU fiber plans (fixed broadband ARPU uplift potential 10–20%) and retiring copper to cut OPEX and accelerate ROI.

Entrance of a fourth mobile operator

The entry of Digi in 2024 shifted Belgium from three to four mobile operators, triggering intensified price competition and a 3-5% decline in market-wide ARPU in 2024 according to industry reports.

For Proximus this economic pressure mandates differentiation via quality, fixed-mobile bundling and value-added services rather than price cuts to protect margins.

Management must prioritize premium packages and loyalty programs; Proximus reported a 1.2% fall in consumer mobile ARPU H1 2025, underscoring urgency for retention and upsell strategies.

B2B digital transformation spending

Enterprise spending on cloud, cybersecurity and managed ICT rose across Europe; IDC reported European cloud spending hit about €100bn in 2024, with cybersecurity budgets growing ~9% YoY—Proximus positions as strategic partner offering cloud, security and managed services to capture this demand.

B2B revenue growth (Proximus B2B represented ~45% of service revenue in 2024) helps offset stagnant residential ARPU and intense price competition, stabilizing margins and supporting higher-value service upsells.

- Sustained enterprise demand: cloud, security, managed ICT

- IDC: €100bn EU cloud spend 2024; cybersecurity +9% YoY

- Proximus B2B ≈45% of service revenue in 2024

- B2B growth hedges saturated, price-sensitive residential market

Interest rate volatility

As a capital-intensive telecom with net debt around EUR 4.5bn (2025 guidance) Proximus is highly sensitive to ECB rate moves; a 100bps rise in rates can materially increase annual interest expense and depress enterprise valuation via higher WACC.

Higher borrowing costs could delay or scale back multi-year broadband and 5G investments; management uses interest rate swaps and caps to hedge exposure and protect cash flows.

Hedging supports dividend sustainability—Proximus paid EUR 1.00 per share in 2024—by smoothing financing costs amid rate volatility.

- Net debt ~EUR 4.5bn (2025 guidance)

- 100bps rate rise raises WACC and interest expense materially

- Swaps/caps used to hedge interest-rate risk

- Dividend EUR 1.00 in 2024; hedging preserves payout capacity

Proximus margins steady amid wage inflation and fiber spending; ARPU pressured by Digi

Belgian wage indexation (inflation 9.5% in 2022; ~6% avg 2023–24) raised Proximus labor costs; adjusted EBITDA margin ~37% in 2023. Fiber rollout capex ~EUR 2.7–3.0bn to date; net debt ~EUR 4.5bn (2025 guidance), net debt/EBITDA ~2.6x (2024). Digi entry cut ARPU 3–5% in 2024; Proximus B2B ≈45% service revenue (2024) offsets consumer pressure.

| Metric | Value |

|---|---|

| Adj. EBITDA margin (2023) | ~37% |

| Net debt (2025 guidance) | ~EUR 4.5bn |

| Net debt/EBITDA (2024) | ~2.6x |

| Fiber capex to date | EUR 2.7–3.0bn |

| ARPU decline post-Digi (2024) | 3–5% |

| B2B share (2024) | ~45% |

Same Document Delivered

Proximus PESTLE Analysis

The preview shown here is the exact Proximus PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview match the final file you’ll download immediately after payment.