Prudential Financial Porter's Five Forces Analysis

Don't Miss the Bigger Picture

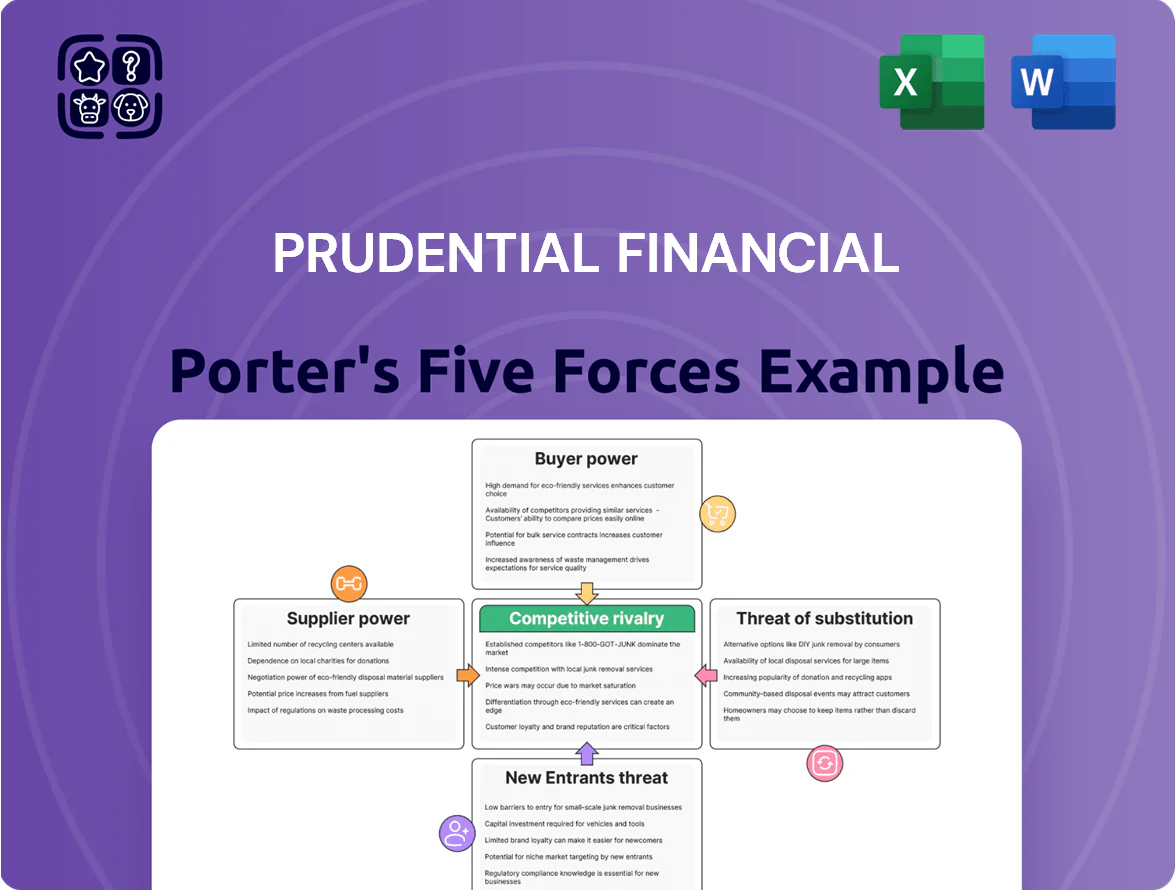

Prudential Financial faces moderate buyer power and regulatory scrutiny, with intense rivalry among large insurers and a manageable threat from new entrants thanks to scale and distribution; supplier influence is limited while technological substitutes and fintech innovations pose growing threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Prudential Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Human Capital and Specialized Talent

The primary suppliers for Prudential are highly skilled professionals—actuaries, investment managers, and data scientists—whose labor market tightened in late 2025 with fintech and quant roles growing 18% year-over-year, boosting bargaining power. Prudential must match market medians—total comp for senior quants around $350k–$500k in 2025—and invest in culture and upskilling to retain the intellectual capital needed for complex risk assessment.

Financial Market Data and Technology Providers

Prudential depends on external vendors for real-time market data, cloud hosting, and cybersecurity; Bloomberg, Amazon Web Services (AWS), and Microsoft Azure dominate these segments and create high switching costs tied to data feeds, APIs, and compliance integrations.

In 2024 Prudential reported ~$1.3B in technology and data expenses (estimate range), so a 10% vendor price rise would add ~130M to operating costs and squeeze margins; a multi-hour outage in 2023 at a major cloud provider disrupted trading and risk systems industry-wide, showing direct operational risk.

Reinsurance Market Dynamics

Reinsurers are critical suppliers for Prudential, ceding portions of life and P/C risk to limit capital strain; in 2024 global reinsurance premiums were about $370bn, concentrated among firms like Munich Re and Swiss Re holding >30% market share, so pricing power is high after catastrophe years.

Prudential’s capital ratios hinge on reinsurance availability and cost—after 2023–24 catastrophe losses, treaty rates rose ~15–25%, squeezing capital relief and raising economic capital needs.

Regulatory and Compliance Bodies

Regulatory bodies provide Prudential Financial the license to operate and set capital rules; Basel III/IV and US risk-based capital standards forced US insurers to hold higher quality capital—Prudential reported a 2024 statutory RBC ratio around 450% (Q4 2024), showing tight capital allocation constraints.

Compliance costs are non-negotiable and limit resource deployment; shifts in IFRS/US GAAP or capital adequacy alter investment, dividends, and buyback capacity, giving regulators near-absolute supplier power.

- Regulators set capital rules

- Prudential Q4 2024 statutory RBC ~450%

- Compliance costs non-negotiable

- Accounting changes reshape capital use

Capital Providers and Debt Markets

Prudential’s main raw material is capital: debt and institutional funding; in 2025 Prudential issued $3.5bn of long-term debt and held $110bn of long-term debt on the balance sheet, so borrowing costs matter materially.

Interest-rate swings and Moody’s/S&P ratings shifts change Prudential’s borrowing spread; a 100bp rate rise in 2022-23 widened funding costs and compressed spreads on fixed-rate products.

High-rate environments boost suppliers’ bargaining power, raising funding costs and squeezing margins on spread-based insurance and annuity lines.

- 2025 long-term debt ~$110bn

- 2025 new issuance $3.5bn

- 100bp rate rise → wider funding spread, lower product margins

Suppliers Hold the Cards: Talent, Tech, Reinsurers & Capital Tighten Leverage

Suppliers (talent, data/cloud vendors, reinsurers, regulators, capital providers) exert high bargaining power: senior quant pay $350k–$500k (2025), tech/data spend ~$1.3B (2024), reinsurance market concentrated (Munich Re/Swiss Re >30%), Prudential long-term debt ~$110B (2025) and $3.5B new issue (2025), statutory RBC ~450% (Q4 2024).

| Supplier | Key metric |

|---|---|

| Talent | Senior quants $350k–$500k (2025) |

| Tech/Data | Spend ~$1.3B (2024) |

| Reinsurance | Top firms >30% share |

| Capital | LT debt ~$110B; issuance $3.5B (2025) |

| Regulation | RBC ~450% (Q4 2024) |

What is included in the product

Comprehensive Porter's Five Forces review of Prudential Financial, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, and substitute threats with industry data and strategic insights to inform investor and management decisions.

A clear, one-sheet Porter’s Five Forces summary for Prudential Financial—speeding strategic decisions by visualizing competitive intensity, regulatory pressure, and bargaining power at a glance.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance

Individual customers now use digital comparison tools—searches for life insurance rate quotes rose 42% in 2024—so Prudential (Prudential Financial, Inc.; ticker PRU) faces high price sensitivity; transparent pricing forces competitive premium adjustments to avoid churn to lower-cost digital insurers like Ladder and Policygenius. Brand loyalty erodes as 58% of consumers cite monthly cost as top buying driver in 2025 surveys.

Institutional Client Negotiation Leverage

Large pension funds and corporate clients account for roughly 45% of Prudential Financial’s $1.2 trillion in assets under management (AUM) as of year-end 2025, giving these buyers scale to demand lower management fees and bespoke service-level agreements.

The ability to redeploy billions quickly means institutional clients extract concessions at renewals; Prudential reported fee compression of ~12 basis points in its institutional segment in 2024, reflecting this leverage.

Low Switching Costs for Asset Management

In mutual fund and investment management, customers face low switching costs; industry surveys show 35% of retail investors moved at least some assets in 2024, and ETF flows hit $800bn in 2024, pressuring Prudential Financial to retain AUM.

The rise of low-cost ETFs and robo-advisors—industry average expense ratios for large US ETFs fell to 0.12% in 2024—gives retail investors easy alternatives if Prudential’s funds underperform.

This ease of movement forces Prudential to deliver consistent alpha or superior service: outflows spike when 3-year relative returns fall below peers, so retention hinges on performance and client experience.

Demand for Digital and Personalized Experiences

Modern customers expect seamless digital interfaces and personalized advice tied to life stages; 2024 surveys show 72% of US consumers prefer digital-first insurers and 58% would switch for better personalization.

If Prudential lags, customers can pivot to neo-insurers and platforms—Insurtech funding hit $11.4B in 2023—shifting bargaining power to consumers who now set service standards.

- 72% prefer digital-first insurers

- 58% would switch for personalization

- Insurtech funding $11.4B (2023)

Information Symmetry and Financial Literacy

The rise of online financial education and tools (Morningstar, Investopedia, robo-advisors) cut information asymmetry: 62% of US adults used online resources for investing in 2023, per FINRA Foundation, so clients now spot fee mispricing and risks in annuities and VULs.

Better literacy means Prudential (NYSE: PRU) faces tougher fee scrutiny—retail net flows fell 2024 Q3 vs. 2023—forcing clearer disclosures and more negotiable terms.

- 62% of US adults used online investing resources (FINRA, 2023)

- Higher client scrutiny on annuity fees after 2022-24 regulatory actions

- Prudential pressured to enhance fee transparency and product education

Digital-savvy customers drive fee cuts as PRU faces 12bps compression amid mass switching

Customers hold strong bargaining power: retail price sensitivity and digital switching (42% rise in life-quote searches, 2024) plus institutional scale (45% of PRU’s $1.2T AUM, 2025) force fee cuts—Prudential saw ~12 bps fee compression in 2024—while 72% prefer digital-first insurers and 58% would switch for personalization (2024–25 surveys).

| Metric | Value |

|---|---|

| PRU AUM (2025) | $1.2T |

| Institutional share | 45% |

| Fee compression (2024) | ~12 bps |

| Life-quote searches ↑ (2024) | 42% |

| Digital-first preference | 72% |

Same Document Delivered

Prudential Financial Porter's Five Forces Analysis

This preview shows the exact Prudential Financial Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups or samples: what you see is the complete, ready-to-use analysis available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Prudential Financial faces moderate buyer power and regulatory scrutiny, with intense rivalry among large insurers and a manageable threat from new entrants thanks to scale and distribution; supplier influence is limited while technological substitutes and fintech innovations pose growing threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Prudential Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Human Capital and Specialized Talent

The primary suppliers for Prudential are highly skilled professionals—actuaries, investment managers, and data scientists—whose labor market tightened in late 2025 with fintech and quant roles growing 18% year-over-year, boosting bargaining power. Prudential must match market medians—total comp for senior quants around $350k–$500k in 2025—and invest in culture and upskilling to retain the intellectual capital needed for complex risk assessment.

Financial Market Data and Technology Providers

Prudential depends on external vendors for real-time market data, cloud hosting, and cybersecurity; Bloomberg, Amazon Web Services (AWS), and Microsoft Azure dominate these segments and create high switching costs tied to data feeds, APIs, and compliance integrations.

In 2024 Prudential reported ~$1.3B in technology and data expenses (estimate range), so a 10% vendor price rise would add ~130M to operating costs and squeeze margins; a multi-hour outage in 2023 at a major cloud provider disrupted trading and risk systems industry-wide, showing direct operational risk.

Reinsurance Market Dynamics

Reinsurers are critical suppliers for Prudential, ceding portions of life and P/C risk to limit capital strain; in 2024 global reinsurance premiums were about $370bn, concentrated among firms like Munich Re and Swiss Re holding >30% market share, so pricing power is high after catastrophe years.

Prudential’s capital ratios hinge on reinsurance availability and cost—after 2023–24 catastrophe losses, treaty rates rose ~15–25%, squeezing capital relief and raising economic capital needs.

Regulatory and Compliance Bodies

Regulatory bodies provide Prudential Financial the license to operate and set capital rules; Basel III/IV and US risk-based capital standards forced US insurers to hold higher quality capital—Prudential reported a 2024 statutory RBC ratio around 450% (Q4 2024), showing tight capital allocation constraints.

Compliance costs are non-negotiable and limit resource deployment; shifts in IFRS/US GAAP or capital adequacy alter investment, dividends, and buyback capacity, giving regulators near-absolute supplier power.

- Regulators set capital rules

- Prudential Q4 2024 statutory RBC ~450%

- Compliance costs non-negotiable

- Accounting changes reshape capital use

Capital Providers and Debt Markets

Prudential’s main raw material is capital: debt and institutional funding; in 2025 Prudential issued $3.5bn of long-term debt and held $110bn of long-term debt on the balance sheet, so borrowing costs matter materially.

Interest-rate swings and Moody’s/S&P ratings shifts change Prudential’s borrowing spread; a 100bp rate rise in 2022-23 widened funding costs and compressed spreads on fixed-rate products.

High-rate environments boost suppliers’ bargaining power, raising funding costs and squeezing margins on spread-based insurance and annuity lines.

- 2025 long-term debt ~$110bn

- 2025 new issuance $3.5bn

- 100bp rate rise → wider funding spread, lower product margins

Suppliers Hold the Cards: Talent, Tech, Reinsurers & Capital Tighten Leverage

Suppliers (talent, data/cloud vendors, reinsurers, regulators, capital providers) exert high bargaining power: senior quant pay $350k–$500k (2025), tech/data spend ~$1.3B (2024), reinsurance market concentrated (Munich Re/Swiss Re >30%), Prudential long-term debt ~$110B (2025) and $3.5B new issue (2025), statutory RBC ~450% (Q4 2024).

| Supplier | Key metric |

|---|---|

| Talent | Senior quants $350k–$500k (2025) |

| Tech/Data | Spend ~$1.3B (2024) |

| Reinsurance | Top firms >30% share |

| Capital | LT debt ~$110B; issuance $3.5B (2025) |

| Regulation | RBC ~450% (Q4 2024) |

What is included in the product

Comprehensive Porter's Five Forces review of Prudential Financial, highlighting competitive rivalry, buyer/supplier leverage, entry barriers, and substitute threats with industry data and strategic insights to inform investor and management decisions.

A clear, one-sheet Porter’s Five Forces summary for Prudential Financial—speeding strategic decisions by visualizing competitive intensity, regulatory pressure, and bargaining power at a glance.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance

Individual customers now use digital comparison tools—searches for life insurance rate quotes rose 42% in 2024—so Prudential (Prudential Financial, Inc.; ticker PRU) faces high price sensitivity; transparent pricing forces competitive premium adjustments to avoid churn to lower-cost digital insurers like Ladder and Policygenius. Brand loyalty erodes as 58% of consumers cite monthly cost as top buying driver in 2025 surveys.

Institutional Client Negotiation Leverage

Large pension funds and corporate clients account for roughly 45% of Prudential Financial’s $1.2 trillion in assets under management (AUM) as of year-end 2025, giving these buyers scale to demand lower management fees and bespoke service-level agreements.

The ability to redeploy billions quickly means institutional clients extract concessions at renewals; Prudential reported fee compression of ~12 basis points in its institutional segment in 2024, reflecting this leverage.

Low Switching Costs for Asset Management

In mutual fund and investment management, customers face low switching costs; industry surveys show 35% of retail investors moved at least some assets in 2024, and ETF flows hit $800bn in 2024, pressuring Prudential Financial to retain AUM.

The rise of low-cost ETFs and robo-advisors—industry average expense ratios for large US ETFs fell to 0.12% in 2024—gives retail investors easy alternatives if Prudential’s funds underperform.

This ease of movement forces Prudential to deliver consistent alpha or superior service: outflows spike when 3-year relative returns fall below peers, so retention hinges on performance and client experience.

Demand for Digital and Personalized Experiences

Modern customers expect seamless digital interfaces and personalized advice tied to life stages; 2024 surveys show 72% of US consumers prefer digital-first insurers and 58% would switch for better personalization.

If Prudential lags, customers can pivot to neo-insurers and platforms—Insurtech funding hit $11.4B in 2023—shifting bargaining power to consumers who now set service standards.

- 72% prefer digital-first insurers

- 58% would switch for personalization

- Insurtech funding $11.4B (2023)

Information Symmetry and Financial Literacy

The rise of online financial education and tools (Morningstar, Investopedia, robo-advisors) cut information asymmetry: 62% of US adults used online resources for investing in 2023, per FINRA Foundation, so clients now spot fee mispricing and risks in annuities and VULs.

Better literacy means Prudential (NYSE: PRU) faces tougher fee scrutiny—retail net flows fell 2024 Q3 vs. 2023—forcing clearer disclosures and more negotiable terms.

- 62% of US adults used online investing resources (FINRA, 2023)

- Higher client scrutiny on annuity fees after 2022-24 regulatory actions

- Prudential pressured to enhance fee transparency and product education

Digital-savvy customers drive fee cuts as PRU faces 12bps compression amid mass switching

Customers hold strong bargaining power: retail price sensitivity and digital switching (42% rise in life-quote searches, 2024) plus institutional scale (45% of PRU’s $1.2T AUM, 2025) force fee cuts—Prudential saw ~12 bps fee compression in 2024—while 72% prefer digital-first insurers and 58% would switch for personalization (2024–25 surveys).

| Metric | Value |

|---|---|

| PRU AUM (2025) | $1.2T |

| Institutional share | 45% |

| Fee compression (2024) | ~12 bps |

| Life-quote searches ↑ (2024) | 42% |

| Digital-first preference | 72% |

Same Document Delivered

Prudential Financial Porter's Five Forces Analysis

This preview shows the exact Prudential Financial Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy.

No mockups or samples: what you see is the complete, ready-to-use analysis available instantly upon payment.