Prudential Financial PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Prudential Financial faces a shifting external landscape—from regulatory scrutiny and interest-rate volatility to digital disruption and climate-related liabilities—and our PESTLE distills these forces into clear strategic implications; buy the full analysis to unlock actionable insights, ready-made slides, and editable data to inform investment decisions and strategic plans.

Political factors

Geopolitical instability and global trade tensions

Increased geopolitical fragmentation as of late 2025 has hit Prudential’s international operations, with Asia exposures—Japan and Southeast Asia—accounting for roughly 28% of non-US revenue in FY2024 and facing heightened regulatory risk. Shifts in trade alliances and diplomatic friction have led to sudden changes in foreign investment rules and currency repatriation, contributing to FX volatility that trimmed group net income by an estimated $150–200m in 2024. Prudential must continuously adjust capital allocation and hedging across its global insurance and asset management portfolios to preserve solvency and maintain target return on equity near its 10–12% goal.

U.S. fiscal policy and tax reform shifts

Following political shifts in late 2024–2025, potential corporate tax rate changes (e.g., proposals to raise rates from 21% toward 25%–28%) and capital gains adjustments could materially affect Prudential’s net margins and ROE, altering product pricing and competitiveness.

Legislative focus on social safety nets may change demand for tax-advantaged retirement products; for example, a 2025 proposal to expand Social Security-related benefits could reduce individual annuity uptake by several percentage points.

Prudential must stay agile to restructure products and reserves as federal budget decisions and tax code revisions—potentially shifting effective tax rate by 2–4 percentage points—impact actuarial assumptions and capital planning.

Regulatory oversight on systemic importance

Prudential remains monitored by domestic and international regulators as a systemically important financial institution, with the U.S. Financial Stability Oversight Council and equivalents abroad intensifying scrutiny after 2023 stress tests; in 2024 Prudential reported a CET1-like capital buffer equivalent of about 12.6% for its insurance group-level solvency metrics, leaving limited room if political shifts impose stricter capital or enhanced reporting mandates.

Government-sponsored retirement initiatives

Political moves to close the retirement savings gap have led to mandates and incentives for employer plans; in 2024 auto-enrollment laws and state-run programs expanded coverage to over 25 million private-sector workers, creating growth opportunities for Prudential’s recordkeeping and advisory services.

Government-led retirement offerings raise competitive risk: public programs and state plans managing ~$20–40 billion each could pressure fees and margins for Prudential’s retirement segment.

Policy shifts on Social Security adjustments or 401(k) enhancements—such as proposed 2025 legislation increasing catch-up contribution limits by up to 50%—would materially affect Prudential’s asset base and fee revenue.

- Auto-enrollment/state programs: +25M workers (2024)

- State program asset pools: commonly $20–40B

- Potential 2025 401(k) policy: +50% catch-up change impacts AUM/fees

Political influence on ESG mandates

- 17 US states with ESG restrictions (2024)

- $6.7T global sustainable AUM (2023)

- 5–15% higher compliance/reporting costs estimated

Regulatory shocks, FX hits trim profits as auto‑enrollment boosts assets amid ESG constraints

Geopolitical fragmentation and regulatory shifts (Asia = 28% non-US revenue FY2024) raised FX/regulatory risk, trimming ~ $150–200m net income in 2024; potential US tax hikes (21%→25–28%) and 2–4ppt ETR swings threaten margins; auto-enrollment added 25M workers (2024) boosting retirement flows but public plans ($20–40B each) pressure fees; 17 states ESG limits (2024) complicate $1.4T AUM stewardship.

| Metric | Value |

|---|---|

| Asia revenue share (non‑US) | 28% (FY2024) |

| FX/Regulatory hit | $150–200m (2024) |

| Prudential AUM | $1.4T (2024) |

| Auto-enrolled workers | +25M (2024) |

| States with ESG limits | 17 (2024) |

What is included in the product

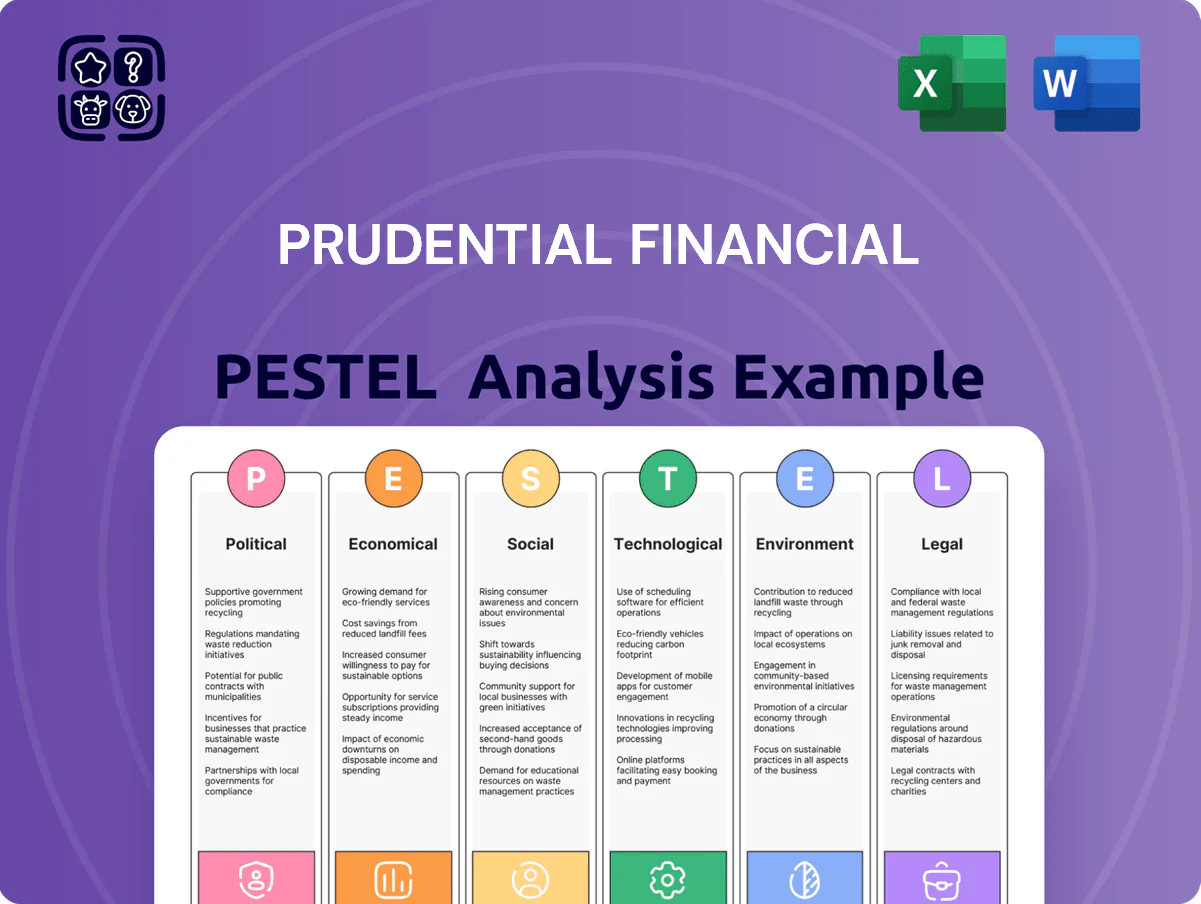

Explores how external macro-environmental factors uniquely affect Prudential Financial across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Prudential Financial for quick inclusion in presentations or planning sessions, easing alignment across teams and stakeholder discussions on external risks and market positioning.

Economic factors

Interest rate environment and yield curve shifts

By end-2025, Fed funds near 5.25% and 10y Treasury ~4.2% shape Prudential’s investment income and pricing; higher coupon reinvestment lifts yields but recent stabilization limits upside to net investment yield (~3.8%–4.2% industry range).

A flattened/inverted curve (10y–2y spread ~-0.1% in 2024–25 episodes) compresses margins on long-duration life and annuity blocks, increasing reserve strain.

Prudential’s spread-based profitability is tightly tied to central bank policy; sustained restrictive stance risks margin squeeze, while cuts could restore spread over time.

Global inflationary pressures and cost of living

Persistent global inflation—consumer prices up ~6.8% YoY in 2023 and still elevated at ~4–5% across key markets in 2024—erodes purchasing power, likely shrinking discretionary budgets for life insurance premiums and investments; simultaneously, Prudential faces higher operating costs (US wage growth ~4.2% in 2024) that can compress margins unless offset by efficiency; the firm must adjust pricing, product features and distribution to keep middle-market offerings affordable.

Equity market volatility and AUM fluctuations

As a major asset manager via PGIM, Prudential’s fee income is highly sensitive to equity and bond market moves; AUM fell 8% in 2022 during market stress and was $1.5 trillion at end-2025, per company reports, making revenues volatile.

Market downturns shrink AUM and can trigger minimum guarantee payouts on variable annuities—Prudential disclosed $1.1 billion of VA hedging losses in 2022 linked to rates and equities.

Diversification across equities, fixed income, alternatives and increased hedging remains the primary strategy to mitigate periodic corrections and support fee stability.

Currency exchange rate fluctuations

With a large footprint in Japan (about 22% of 2024 revenue), Prudential faces translation risk as yen-dollar moves: a 10% yen depreciation could reduce reported net income by an estimated $300–450 million due to non-economic accounting swings.

Prudential employs hedging—cross-currency swaps and FX forwards covering a substantial portion of net foreign exposures—but extreme volatility (e.g., 2024 JPYUSD moves of ±8%) can still strain capital adequacy ratios and regulatory capital buffers.

- ~22% revenue from Japan (2024)

- 10% JPY depreciation ≈ $300–450M hit to reported net income

- Hedging covers large exposures but not tail events

- ±8% JPYUSD 2024 volatility risks capital ratios

Credit market stability and default rates

The health of the corporate bond market is critical for Prudential’s general account, which held about $236 billion in fixed-income securities at year-end 2024; an economic slowdown in late 2025 could push corporate default rates above the 2024 US speculative-grade average of 2.4%, increasing impairments and pressure on capital ratios.

Maintaining a high-quality credit profile—measured by exposure to investment-grade bonds (over 80% of holdings in 2024)—is essential to meet long-term policyholder obligations and avoid downgrades that would raise funding costs.

- General account fixed income: ~$236bn (2024)

- Speculative-grade default rate US 2024: 2.4%

- Investment-grade exposure: >80% of holdings (2024)

Higher rates boost reinvestment but curve, FX & fee swings squeeze PGIM margins

Higher rates (Fed ~5.25% end-2025; 10y ~4.2%) lift reinvestment yields but flattening curve compresses long-duration margins; PGIM AUM ~$1.5T (end-2025) drives fee volatility; general account fixed income ~$236B (2024) with >80% IG mitigates credit stress though rising defaults (spec-grade 2.4% in 2024) and FX (Japan ~22% revenue; 10% JPY move ≈ $300–450M) pose capital risks.

| Metric | Value |

|---|---|

| Fed funds (end-2025) | ~5.25% |

| 10y Treasury | ~4.2% |

| PGIM AUM | $1.5T |

| Fixed income (GA, 2024) | $236B |

| IG exposure | >80% |

| Japan revenue (2024) | ~22% |

What You See Is What You Get

Prudential Financial PESTLE Analysis

The preview shown here is the exact Prudential Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the complete file available for immediate download upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Prudential Financial faces a shifting external landscape—from regulatory scrutiny and interest-rate volatility to digital disruption and climate-related liabilities—and our PESTLE distills these forces into clear strategic implications; buy the full analysis to unlock actionable insights, ready-made slides, and editable data to inform investment decisions and strategic plans.

Political factors

Geopolitical instability and global trade tensions

Increased geopolitical fragmentation as of late 2025 has hit Prudential’s international operations, with Asia exposures—Japan and Southeast Asia—accounting for roughly 28% of non-US revenue in FY2024 and facing heightened regulatory risk. Shifts in trade alliances and diplomatic friction have led to sudden changes in foreign investment rules and currency repatriation, contributing to FX volatility that trimmed group net income by an estimated $150–200m in 2024. Prudential must continuously adjust capital allocation and hedging across its global insurance and asset management portfolios to preserve solvency and maintain target return on equity near its 10–12% goal.

U.S. fiscal policy and tax reform shifts

Following political shifts in late 2024–2025, potential corporate tax rate changes (e.g., proposals to raise rates from 21% toward 25%–28%) and capital gains adjustments could materially affect Prudential’s net margins and ROE, altering product pricing and competitiveness.

Legislative focus on social safety nets may change demand for tax-advantaged retirement products; for example, a 2025 proposal to expand Social Security-related benefits could reduce individual annuity uptake by several percentage points.

Prudential must stay agile to restructure products and reserves as federal budget decisions and tax code revisions—potentially shifting effective tax rate by 2–4 percentage points—impact actuarial assumptions and capital planning.

Regulatory oversight on systemic importance

Prudential remains monitored by domestic and international regulators as a systemically important financial institution, with the U.S. Financial Stability Oversight Council and equivalents abroad intensifying scrutiny after 2023 stress tests; in 2024 Prudential reported a CET1-like capital buffer equivalent of about 12.6% for its insurance group-level solvency metrics, leaving limited room if political shifts impose stricter capital or enhanced reporting mandates.

Government-sponsored retirement initiatives

Political moves to close the retirement savings gap have led to mandates and incentives for employer plans; in 2024 auto-enrollment laws and state-run programs expanded coverage to over 25 million private-sector workers, creating growth opportunities for Prudential’s recordkeeping and advisory services.

Government-led retirement offerings raise competitive risk: public programs and state plans managing ~$20–40 billion each could pressure fees and margins for Prudential’s retirement segment.

Policy shifts on Social Security adjustments or 401(k) enhancements—such as proposed 2025 legislation increasing catch-up contribution limits by up to 50%—would materially affect Prudential’s asset base and fee revenue.

- Auto-enrollment/state programs: +25M workers (2024)

- State program asset pools: commonly $20–40B

- Potential 2025 401(k) policy: +50% catch-up change impacts AUM/fees

Political influence on ESG mandates

- 17 US states with ESG restrictions (2024)

- $6.7T global sustainable AUM (2023)

- 5–15% higher compliance/reporting costs estimated

Regulatory shocks, FX hits trim profits as auto‑enrollment boosts assets amid ESG constraints

Geopolitical fragmentation and regulatory shifts (Asia = 28% non-US revenue FY2024) raised FX/regulatory risk, trimming ~ $150–200m net income in 2024; potential US tax hikes (21%→25–28%) and 2–4ppt ETR swings threaten margins; auto-enrollment added 25M workers (2024) boosting retirement flows but public plans ($20–40B each) pressure fees; 17 states ESG limits (2024) complicate $1.4T AUM stewardship.

| Metric | Value |

|---|---|

| Asia revenue share (non‑US) | 28% (FY2024) |

| FX/Regulatory hit | $150–200m (2024) |

| Prudential AUM | $1.4T (2024) |

| Auto-enrolled workers | +25M (2024) |

| States with ESG limits | 17 (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Prudential Financial across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary of Prudential Financial for quick inclusion in presentations or planning sessions, easing alignment across teams and stakeholder discussions on external risks and market positioning.

Economic factors

Interest rate environment and yield curve shifts

By end-2025, Fed funds near 5.25% and 10y Treasury ~4.2% shape Prudential’s investment income and pricing; higher coupon reinvestment lifts yields but recent stabilization limits upside to net investment yield (~3.8%–4.2% industry range).

A flattened/inverted curve (10y–2y spread ~-0.1% in 2024–25 episodes) compresses margins on long-duration life and annuity blocks, increasing reserve strain.

Prudential’s spread-based profitability is tightly tied to central bank policy; sustained restrictive stance risks margin squeeze, while cuts could restore spread over time.

Global inflationary pressures and cost of living

Persistent global inflation—consumer prices up ~6.8% YoY in 2023 and still elevated at ~4–5% across key markets in 2024—erodes purchasing power, likely shrinking discretionary budgets for life insurance premiums and investments; simultaneously, Prudential faces higher operating costs (US wage growth ~4.2% in 2024) that can compress margins unless offset by efficiency; the firm must adjust pricing, product features and distribution to keep middle-market offerings affordable.

Equity market volatility and AUM fluctuations

As a major asset manager via PGIM, Prudential’s fee income is highly sensitive to equity and bond market moves; AUM fell 8% in 2022 during market stress and was $1.5 trillion at end-2025, per company reports, making revenues volatile.

Market downturns shrink AUM and can trigger minimum guarantee payouts on variable annuities—Prudential disclosed $1.1 billion of VA hedging losses in 2022 linked to rates and equities.

Diversification across equities, fixed income, alternatives and increased hedging remains the primary strategy to mitigate periodic corrections and support fee stability.

Currency exchange rate fluctuations

With a large footprint in Japan (about 22% of 2024 revenue), Prudential faces translation risk as yen-dollar moves: a 10% yen depreciation could reduce reported net income by an estimated $300–450 million due to non-economic accounting swings.

Prudential employs hedging—cross-currency swaps and FX forwards covering a substantial portion of net foreign exposures—but extreme volatility (e.g., 2024 JPYUSD moves of ±8%) can still strain capital adequacy ratios and regulatory capital buffers.

- ~22% revenue from Japan (2024)

- 10% JPY depreciation ≈ $300–450M hit to reported net income

- Hedging covers large exposures but not tail events

- ±8% JPYUSD 2024 volatility risks capital ratios

Credit market stability and default rates

The health of the corporate bond market is critical for Prudential’s general account, which held about $236 billion in fixed-income securities at year-end 2024; an economic slowdown in late 2025 could push corporate default rates above the 2024 US speculative-grade average of 2.4%, increasing impairments and pressure on capital ratios.

Maintaining a high-quality credit profile—measured by exposure to investment-grade bonds (over 80% of holdings in 2024)—is essential to meet long-term policyholder obligations and avoid downgrades that would raise funding costs.

- General account fixed income: ~$236bn (2024)

- Speculative-grade default rate US 2024: 2.4%

- Investment-grade exposure: >80% of holdings (2024)

Higher rates boost reinvestment but curve, FX & fee swings squeeze PGIM margins

Higher rates (Fed ~5.25% end-2025; 10y ~4.2%) lift reinvestment yields but flattening curve compresses long-duration margins; PGIM AUM ~$1.5T (end-2025) drives fee volatility; general account fixed income ~$236B (2024) with >80% IG mitigates credit stress though rising defaults (spec-grade 2.4% in 2024) and FX (Japan ~22% revenue; 10% JPY move ≈ $300–450M) pose capital risks.

| Metric | Value |

|---|---|

| Fed funds (end-2025) | ~5.25% |

| 10y Treasury | ~4.2% |

| PGIM AUM | $1.5T |

| Fixed income (GA, 2024) | $236B |

| IG exposure | >80% |

| Japan revenue (2024) | ~22% |

What You See Is What You Get

Prudential Financial PESTLE Analysis

The preview shown here is the exact Prudential Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the complete file available for immediate download upon payment.