Prysmian PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic trends, and technological advances are reshaping Prysmian’s market—our concise PESTLE highlights key external drivers and risks that matter to investors and strategists; purchase the full analysis to access the complete, actionable breakdown and ready-to-use insights for your next decision.

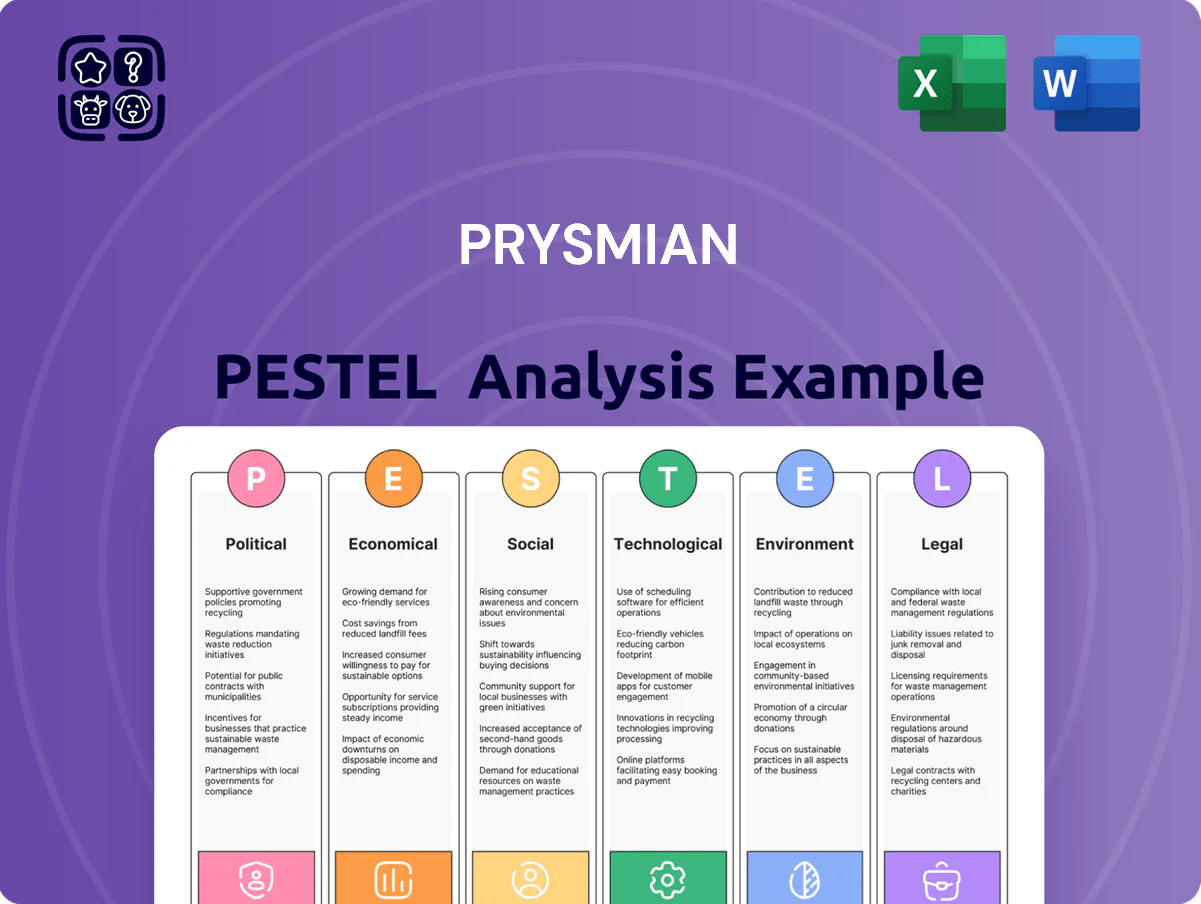

Political factors

Geopolitical focus on energy independence

As of late 2025, EU and US policy drives to cut foreign energy dependence have unlocked roughly €45–55 billion in public funding for grid upgrades and interconnectors; Prysmian, with ~40% share in HV cable tenders, is a primary beneficiary via multimillion-euro contracts across Europe and North America. Governments aim to secure supplies and shift from volatile fossil-fuel imports, boosting long-term demand for Prysmian’s power transmission products and services.

Trade policies and protectionism

Global trade tensions are reshaping Prysmian’s sourcing of copper and aluminum—metals that comprised over 40% of raw-material costs in 2024—forcing the company to manage evolving US and EU tariffs and Buy Local rules that raised import duties by up to 15–25% in some segments in 2023–24. To mitigate duty exposure and preserve margins (2024 EBITDA margin 8.9%), Prysmian is expanding localized manufacturing and supply chains across the US and EU.

Subsidies for renewable energy expansion

Political commitments like the EU Green Deal and national frameworks in Asia are driving €200+ billion investments into offshore wind through 2030, directly boosting Prysmian’s subsea cable demand; Prysmian reported €8.9bn order backlog in FY2024 with renewables as a core driver. Government-led auction schedules heavily influence timing of Prysmian’s contracts, creating revenue visibility tied to policy calendars. Shifts in political leadership can slow subsidy rollouts, compressing long-term project pipelines and impacting multiyear capex and order intake forecasts.

Stability in emerging markets

- 12% of 2024 sales from Latin America — material exposure

- Political shifts can trigger multi-million-euro project delays

- Regulatory changes may force contract renegotiations

- Monitoring South America and Asian markets essential for 2025 growth

Infrastructure stimulus packages

Post-pandemic recovery shifted to long-term infrastructure acts emphasizing digitalization and electrification; EU Recovery and Resilience Facility and US Bipartisan Infrastructure Law channelled over €1.8tn (EU) and $1.2tn respectively toward grid and broadband upgrades through 2024–25, boosting demand for cables and systems.

Prysmian, with 2024 revenues of €15.7bn and ~40% exposure to power and telecom segments, is a primary beneficiary as governments replace aging grids and expand fiber networks to raise national competitiveness.

- €1.8tn EU & $1.2tn US infrastructure funds (2024–25)

- Prysmian 2024 revenue €15.7bn; ~40% power/telecom exposure

- Rising fiber rollout and grid modernization drive long-term demand

Prysmian rides €1.8tn infrastructure wave—HV dominance offsets LatAm political risk

EU/US energy-security funds (€45–55bn) and €1.8tn/$1.2tn infrastructure spending through 2024–25 boost Prysmian (2024 revenue €15.7bn; €8.9bn backlog), with ~40% HV/subsea tender share and 12% sales exposure in Latin America posing political risk; tariffs (up to 25%) and local-content rules drive regional manufacturing expansion to protect 2024 EBITDA margin 8.9%.

| Metric | Value |

|---|---|

| 2024 Revenue | €15.7bn |

| Order backlog FY2024 | €8.9bn |

| HV tender share | ~40% |

| LatAm sales | 12% |

| 2024 EBITDA margin | 8.9% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Prysmian, with data-driven trends and region-specific examples to reveal risks and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Prysmian's external risks and opportunities for quick reference in meetings, easily editable for regional or business-line notes and drop-in ready for presentations or strategy packs.

Economic factors

Raw material price volatility

The costs of copper, aluminum and polymers remain primary drivers of Prysmian’s manufacturing expenses; copper averaged about 9,200 USD/t in 2025 and polymer feedstock rose ~12% y/y, squeezing margins.

By end-2025 global commodity volatility—copper price swings ±15% in 2025—continued to affect pricing strategies and EBITDA variability.

Prysmian uses sophisticated hedging and long-term indexation on large contracts; hedges covered an estimated 60–70% of expected raw material exposure into 2026.

Interest rate environment and CAPEX

Higher interest rates in 2024–25 pushed global policy rates to averages near 4–5%, raising project financing costs and extending payback thresholds for utility and telecom CAPEX, delaying some grid and fiber rollouts.

Despite tighter capital, Prysmian benefits from resilient demand in energy transition projects; offshore wind and HV interconnectors secured multi-year contracts worth billions, cushioning order visibility against higher cost of capital.

Global inflation and labor costs

Persistent global inflation—CPI averaging above 5% in key markets in 2024—has pushed wages up ~6–8% at Prysmian’s production sites, raising input and labor costs and compressing 2024 operating margins reported at ~6.5%. Prysmian is accelerating automation and lean programs, targeting double-digit ROI on capex to improve productivity and offset a €300–400m annualized cost pressure. The firm must balance price increases—average selling price hikes of ~4–7% in 2024—and risk of volume loss to protect market share.

Currency exchange rate fluctuations

Prysmian, operating in over 50 countries, faces material currency translation risk; in FY2024 about 22% of revenue was non-euro denominated, so a 5% euro appreciation vs USD could reduce reported EUR revenue by ~1.1% (~€150–200m range based on 2024 sales ~€14bn).

The group uses natural hedging—local sourcing and invoicing—and derivatives; net exposure management kept 2024 forex losses within low-single-digit millions, per annual report risk disclosures.

- 50+ countries exposure

- ~22% revenue non-euro in 2024

- 5% EUR appreciation ≈ −€150–200m impact

- Mitigation: natural hedges + derivatives; limited 2024 forex losses

Growth in the digital economy

The global data center market was valued at about $233 billion in 2024 and is projected to grow ~6–8% annually to 2028, while worldwide 5G subscriptions reached ~1.4 billion in 2024—both driving sustained demand for high-quality fiber optic cables from Prysmian.

During 2023–2024 downturns in heavy industry, Prysmian’s telecom BU showed resilience, with fiber sales growth offsetting dips in energy projects and contributing to more stable revenue streams.

The telecom segment thus acts as a stabilizer versus cyclical industrial exposure, supporting Prysmian’s overall margin stability and capital allocation for innovation.

- Data center market ~$233B (2024); CAGR ~6–8% to 2028

- 5G subscriptions ~1.4B (2024)

- Telecom BU fiber sales growth offset cyclical energy downturns

Commodity pressure narrows margins but offshore wind, data centers boost revenue visibility

Commodity costs (copper ~9,200 USD/t in 2025; polymers +12% y/y) and ±15% 2025 copper volatility pressured margins; hedges covered ~60–70% into 2026. Higher rates (policy 4–5% in 2024–25) increased capex costs but strong orders in offshore wind/HV interconnectors and telecom fiber (data center market ~$233bn in 2024; 5G subs ~1.4bn) supported revenue visibility.

| Metric | Value |

|---|---|

| Copper (2025) | ~9,200 USD/t |

| Polymers | +12% y/y (2025) |

| Hedge coverage | 60–70% |

| Policy rates | 4–5% (2024–25) |

| Data center market (2024) | ~$233bn |

| 5G subs (2024) | ~1.4bn |

What You See Is What You Get

Prysmian PESTLE Analysis

The preview shown here is the exact Prysmian PESTLE document you’ll receive after purchase—fully formatted and ready to use. This screenshot reflects the real, final file with all analysis, headings, and visuals intact. After checkout you’ll be able to download this exact, professionally structured report with no placeholders or surprises. What you see is what you’ll own and can immediately apply to your strategic work.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic trends, and technological advances are reshaping Prysmian’s market—our concise PESTLE highlights key external drivers and risks that matter to investors and strategists; purchase the full analysis to access the complete, actionable breakdown and ready-to-use insights for your next decision.

Political factors

Geopolitical focus on energy independence

As of late 2025, EU and US policy drives to cut foreign energy dependence have unlocked roughly €45–55 billion in public funding for grid upgrades and interconnectors; Prysmian, with ~40% share in HV cable tenders, is a primary beneficiary via multimillion-euro contracts across Europe and North America. Governments aim to secure supplies and shift from volatile fossil-fuel imports, boosting long-term demand for Prysmian’s power transmission products and services.

Trade policies and protectionism

Global trade tensions are reshaping Prysmian’s sourcing of copper and aluminum—metals that comprised over 40% of raw-material costs in 2024—forcing the company to manage evolving US and EU tariffs and Buy Local rules that raised import duties by up to 15–25% in some segments in 2023–24. To mitigate duty exposure and preserve margins (2024 EBITDA margin 8.9%), Prysmian is expanding localized manufacturing and supply chains across the US and EU.

Subsidies for renewable energy expansion

Political commitments like the EU Green Deal and national frameworks in Asia are driving €200+ billion investments into offshore wind through 2030, directly boosting Prysmian’s subsea cable demand; Prysmian reported €8.9bn order backlog in FY2024 with renewables as a core driver. Government-led auction schedules heavily influence timing of Prysmian’s contracts, creating revenue visibility tied to policy calendars. Shifts in political leadership can slow subsidy rollouts, compressing long-term project pipelines and impacting multiyear capex and order intake forecasts.

Stability in emerging markets

- 12% of 2024 sales from Latin America — material exposure

- Political shifts can trigger multi-million-euro project delays

- Regulatory changes may force contract renegotiations

- Monitoring South America and Asian markets essential for 2025 growth

Infrastructure stimulus packages

Post-pandemic recovery shifted to long-term infrastructure acts emphasizing digitalization and electrification; EU Recovery and Resilience Facility and US Bipartisan Infrastructure Law channelled over €1.8tn (EU) and $1.2tn respectively toward grid and broadband upgrades through 2024–25, boosting demand for cables and systems.

Prysmian, with 2024 revenues of €15.7bn and ~40% exposure to power and telecom segments, is a primary beneficiary as governments replace aging grids and expand fiber networks to raise national competitiveness.

- €1.8tn EU & $1.2tn US infrastructure funds (2024–25)

- Prysmian 2024 revenue €15.7bn; ~40% power/telecom exposure

- Rising fiber rollout and grid modernization drive long-term demand

Prysmian rides €1.8tn infrastructure wave—HV dominance offsets LatAm political risk

EU/US energy-security funds (€45–55bn) and €1.8tn/$1.2tn infrastructure spending through 2024–25 boost Prysmian (2024 revenue €15.7bn; €8.9bn backlog), with ~40% HV/subsea tender share and 12% sales exposure in Latin America posing political risk; tariffs (up to 25%) and local-content rules drive regional manufacturing expansion to protect 2024 EBITDA margin 8.9%.

| Metric | Value |

|---|---|

| 2024 Revenue | €15.7bn |

| Order backlog FY2024 | €8.9bn |

| HV tender share | ~40% |

| LatAm sales | 12% |

| 2024 EBITDA margin | 8.9% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Prysmian, with data-driven trends and region-specific examples to reveal risks and opportunities for executives and investors.

A concise, PESTLE-segmented summary of Prysmian's external risks and opportunities for quick reference in meetings, easily editable for regional or business-line notes and drop-in ready for presentations or strategy packs.

Economic factors

Raw material price volatility

The costs of copper, aluminum and polymers remain primary drivers of Prysmian’s manufacturing expenses; copper averaged about 9,200 USD/t in 2025 and polymer feedstock rose ~12% y/y, squeezing margins.

By end-2025 global commodity volatility—copper price swings ±15% in 2025—continued to affect pricing strategies and EBITDA variability.

Prysmian uses sophisticated hedging and long-term indexation on large contracts; hedges covered an estimated 60–70% of expected raw material exposure into 2026.

Interest rate environment and CAPEX

Higher interest rates in 2024–25 pushed global policy rates to averages near 4–5%, raising project financing costs and extending payback thresholds for utility and telecom CAPEX, delaying some grid and fiber rollouts.

Despite tighter capital, Prysmian benefits from resilient demand in energy transition projects; offshore wind and HV interconnectors secured multi-year contracts worth billions, cushioning order visibility against higher cost of capital.

Global inflation and labor costs

Persistent global inflation—CPI averaging above 5% in key markets in 2024—has pushed wages up ~6–8% at Prysmian’s production sites, raising input and labor costs and compressing 2024 operating margins reported at ~6.5%. Prysmian is accelerating automation and lean programs, targeting double-digit ROI on capex to improve productivity and offset a €300–400m annualized cost pressure. The firm must balance price increases—average selling price hikes of ~4–7% in 2024—and risk of volume loss to protect market share.

Currency exchange rate fluctuations

Prysmian, operating in over 50 countries, faces material currency translation risk; in FY2024 about 22% of revenue was non-euro denominated, so a 5% euro appreciation vs USD could reduce reported EUR revenue by ~1.1% (~€150–200m range based on 2024 sales ~€14bn).

The group uses natural hedging—local sourcing and invoicing—and derivatives; net exposure management kept 2024 forex losses within low-single-digit millions, per annual report risk disclosures.

- 50+ countries exposure

- ~22% revenue non-euro in 2024

- 5% EUR appreciation ≈ −€150–200m impact

- Mitigation: natural hedges + derivatives; limited 2024 forex losses

Growth in the digital economy

The global data center market was valued at about $233 billion in 2024 and is projected to grow ~6–8% annually to 2028, while worldwide 5G subscriptions reached ~1.4 billion in 2024—both driving sustained demand for high-quality fiber optic cables from Prysmian.

During 2023–2024 downturns in heavy industry, Prysmian’s telecom BU showed resilience, with fiber sales growth offsetting dips in energy projects and contributing to more stable revenue streams.

The telecom segment thus acts as a stabilizer versus cyclical industrial exposure, supporting Prysmian’s overall margin stability and capital allocation for innovation.

- Data center market ~$233B (2024); CAGR ~6–8% to 2028

- 5G subscriptions ~1.4B (2024)

- Telecom BU fiber sales growth offset cyclical energy downturns

Commodity pressure narrows margins but offshore wind, data centers boost revenue visibility

Commodity costs (copper ~9,200 USD/t in 2025; polymers +12% y/y) and ±15% 2025 copper volatility pressured margins; hedges covered ~60–70% into 2026. Higher rates (policy 4–5% in 2024–25) increased capex costs but strong orders in offshore wind/HV interconnectors and telecom fiber (data center market ~$233bn in 2024; 5G subs ~1.4bn) supported revenue visibility.

| Metric | Value |

|---|---|

| Copper (2025) | ~9,200 USD/t |

| Polymers | +12% y/y (2025) |

| Hedge coverage | 60–70% |

| Policy rates | 4–5% (2024–25) |

| Data center market (2024) | ~$233bn |

| 5G subs (2024) | ~1.4bn |

What You See Is What You Get

Prysmian PESTLE Analysis

The preview shown here is the exact Prysmian PESTLE document you’ll receive after purchase—fully formatted and ready to use. This screenshot reflects the real, final file with all analysis, headings, and visuals intact. After checkout you’ll be able to download this exact, professionally structured report with no placeholders or surprises. What you see is what you’ll own and can immediately apply to your strategic work.