PS Business Parks Porter's Five Forces Analysis

From Overview to Strategy Blueprint

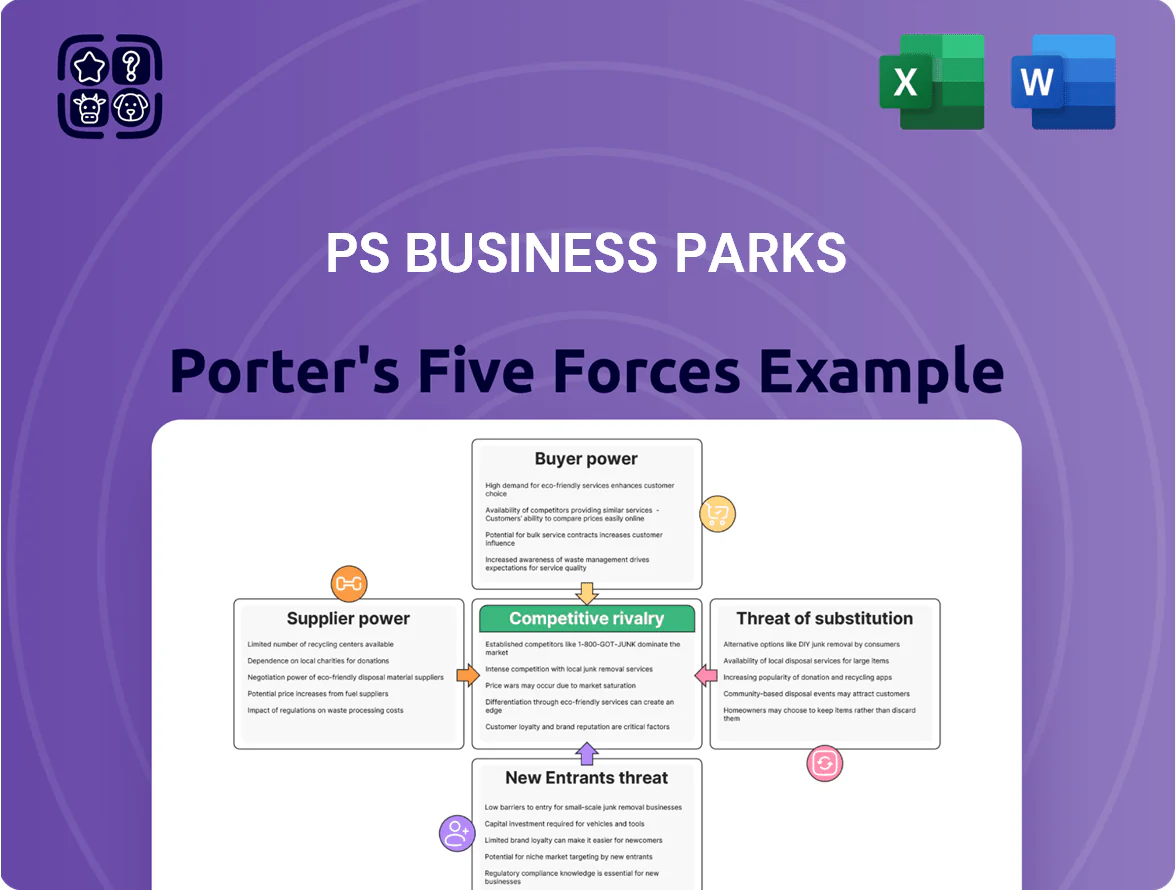

PS Business Parks faces moderate buyer power and substitution risk, balanced by steady demand for flexible commercial space and high capital costs that deter new entrants; suppliers hold limited leverage, while rivalry intensifies across local markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PS Business Parks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction and Maintenance Labor Markets

In 2025 the U.S. skilled trades gap keeps pressure on PS Business Parks: Bureau of Labor Statistics data show 6.5% fewer HVAC/electrical/plumbing entrants vs 2019, letting specialized contractors command 8–12% higher hourly rates and extend timelines by 10–18%, so PS must lock long-term vendor contracts and volume discounts to avoid 5–7% NOI erosion from maintenance overruns.

Energy and Utility Provider Monopolies

Utility firms act as local monopolies, leaving PS Business Parks little ability to push down electricity, water, and waste rates; U.S. commercial electricity prices rose 6.4% in 2023 and averaged about 12.8 cents/kWh in 2024, squeezing margins.

Stronger EPA rules and state clean-energy mandates (California 2045, New York 2040) raise compliance costs, so suppliers press on operating expenses and capital plans.

PSB must invest in efficiency—LED lighting, HVAC upgrades, on-site solar—to cut energy spend; a 20% energy reduction can improve NOI noticeably, since utilities form a material portion of facility OPEX.

Municipal and Regulatory Oversight

Local governments and zoning boards are de facto suppliers for PS Business Parks, granting operating and development rights; in 2024 about 42% of U.S. municipalities tightened zoning rules, raising approval times by an average of 18% per NAIOP data.

They extract value via building permits, impact fees, and property taxes—U.S. commercial property tax rates averaged 1.1% in 2023, affecting NOI directly.

Compliance mandates on sustainability and land use—California’s 2023 climate zoning updates and similar measures in 15 states—can force costly retrofit investments and limit redeployment.

Because owners have limited recourse, statutory changes can drop asset-level returns rapidly; a 100-basis-point effective tax hike can cut cap rates and reduce NAV materially.

Capital and Financing Sources

Being owned by Blackstone gives PS Business Parks strong internal liquidity, but 2025 market-wide cost of debt—corporate bond yields ~5.0% and senior CRE loan spreads ~250–300 bps—still shapes deal economics and redevelopment returns.

Traditional lenders and bond markets set financing terms that affect acquisition IRRs; higher rates in 2025 raise required yields and can delay large projects, so PS must manage capital structure to keep its cost of capital competitive with other institutional owners.

Material Costs for Tenant Improvements

Rising raw-material costs—steel up ~18% and ready-mix concrete up ~12% in 2024 vs 2023—raise PS Business Parks’ tenant-improvement (TI) budgets and limit rapid customization for new tenants.

Suppliers keep leverage due to global supply-chain tightness and strong logistics construction demand; PS often passes costs to tenants, but higher TI prices slowed flex-office leasing velocity by an estimated 6% in 2024.

- Steel +18% (2024 vs 2023)

- Concrete +12% (2024 vs 2023)

- TI cost pass-through common

- Flex-office leasing velocity down ~6% (2024)

Supplier pressure squeezes PSB: skills shortage, material inflation & higher OPEX

Suppliers hold meaningful power over PS Business Parks: skilled-trades shortages (6.5% fewer entrants vs 2019) and 2024 raw-material inflation (steel +18%, concrete +12%) raise maintenance/TI costs and extend timelines, while local utilities (commercial electricity ~12.8¢/kWh in 2024) and stricter regulations (CA 2045, NY 2040) further pressure OPEX and capex, forcing long-term contracts, efficiency investments, and careful capital planning to protect NOI.

| Metric | Value |

|---|---|

| Skilled-trades entrants vs 2019 | -6.5% |

| Steel price change (2024 vs 2023) | +18% |

| Concrete price change (2024 vs 2023) | +12% |

| Commercial electricity (2024) | ~12.8¢/kWh |

| Typical NOI risk from maintenance overruns | 5–7% |

What is included in the product

Tailored exclusively for PS Business Parks, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier leverage, entry barriers, substitutes, and emerging threats shaping its industrial and office REIT profitability.

One-sheet Porter's Five Forces for PS Business Parks—quickly spot competitive pressures and tailor mitigation strategies for leasing, capex, and tenant mix decisions.

Customers Bargaining Power

Tenant Base Fragmentation

This tenant fragmentation supports standardized NNN and modified gross leases across ~4,000 properties, making rent renewal negotiations routine and reducing bespoke discounts.

As a result, revenue predictability improved: same-store NOI grew 2.8% in 2024, reflecting fewer tenant-specific concessions and steadier cash flows.

Demand for Flexible Lease Terms

In 2025 tenants demand shorter leases and flexible layouts—CBRE reports 28% of U.S. industrial leases now under 24 months—forcing PS Business Parks to offer adaptable terms and modular suites, which raises tenant negotiating power on rent and concessions.

PSB that resists flexibility risks churn: JLL found flexible-space providers grew occupancy 6.5% YoY in 2024, so failure to adapt can lead to loss to agile competitors prioritizing short-term, scalable leases.

Switching Costs and Location Dependency

For many industrial and flex tenants, moving specialized equipment and re-establishing local supply chains can cost millions and take months, creating strong lock-in that weakens customer bargaining power at PS Business Parks’ lease renewals.

PSB’s campuses near ports, major highways, and rail hubs—over 70% of its 95.6 million rentable square feet in 2024 sat in top logistics markets—further discourage relocation, letting PSB push modest rent increases with limited churn.

Availability of Market Information

The 2025 rise of digital real estate platforms (LoopNet, CoStar, VTS) gives PS Business Parks tenants clearer rent and vacancy data, enabling sharper comparisons and tougher negotiations based on real-time listings and comps.

Greater transparency shrinks the information gap that once favored institutional landlords during price discovery, pressuring PSB to justify premiums with service or location-based differentiation.

- 2025: national CRE vacancy transparency up ~18% vs 2019 (industry reports)

- Tenants use real-time comps to seek 3–7% lower rents

- Data reduces PSB pricing leverage in commoditized markets

Economic Sensitivity of SMBs

SMBs (small and medium-sized businesses) are more exposed to macro swings than large firms, so PS Business Parks faces higher rent-collection volatility; in 2023 SMBs made up about 60% of U.S. commercial leases, and small-firm bankruptcy filings rose 12% year-over-year in Q2 2024.

In downturns tenants often request deferrals or lower rents to avoid insolvency, forcing PSB to weigh short-term concessions against long-term occupancy—PSB reported 95.4% same-store occupancy in 2024 but noted elevated collection work-outs.

PSB must align pricing with tenant health: selective concessions, flexible lease terms, and credit monitoring can preserve occupancy while limiting revenue loss.

- SMBs = higher default sensitivity

- 2023: ~60% of commercial leases from SMBs

- Q2 2024 small-firm bankruptcies +12%

- PSB 2024 same-store occupancy 95.4%

Rising tenant leverage: shorter leases, SMB risk and greater vacancy transparency

| Metric | Value |

|---|---|

| Largest tenant share (2024) | ≤3% |

| Same-store occupancy (2024) | 95.4% |

| SMB share of leases (2023) | ≈60% |

| Industrial leases <24 months (2025) | 28% |

| Vacancy transparency vs 2019 (2025) | +18% |

Full Version Awaits

PS Business Parks Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for PS Business Parks you'll receive after purchase—fully formatted, professionally written, and ready for immediate download. The document contains competitive rivalry, supplier and buyer power, threat of new entrants, and threat of substitutes tailored to PSB’s market position. No placeholders or samples—what you see is the final deliverable available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

PS Business Parks faces moderate buyer power and substitution risk, balanced by steady demand for flexible commercial space and high capital costs that deter new entrants; suppliers hold limited leverage, while rivalry intensifies across local markets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PS Business Parks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction and Maintenance Labor Markets

In 2025 the U.S. skilled trades gap keeps pressure on PS Business Parks: Bureau of Labor Statistics data show 6.5% fewer HVAC/electrical/plumbing entrants vs 2019, letting specialized contractors command 8–12% higher hourly rates and extend timelines by 10–18%, so PS must lock long-term vendor contracts and volume discounts to avoid 5–7% NOI erosion from maintenance overruns.

Energy and Utility Provider Monopolies

Utility firms act as local monopolies, leaving PS Business Parks little ability to push down electricity, water, and waste rates; U.S. commercial electricity prices rose 6.4% in 2023 and averaged about 12.8 cents/kWh in 2024, squeezing margins.

Stronger EPA rules and state clean-energy mandates (California 2045, New York 2040) raise compliance costs, so suppliers press on operating expenses and capital plans.

PSB must invest in efficiency—LED lighting, HVAC upgrades, on-site solar—to cut energy spend; a 20% energy reduction can improve NOI noticeably, since utilities form a material portion of facility OPEX.

Municipal and Regulatory Oversight

Local governments and zoning boards are de facto suppliers for PS Business Parks, granting operating and development rights; in 2024 about 42% of U.S. municipalities tightened zoning rules, raising approval times by an average of 18% per NAIOP data.

They extract value via building permits, impact fees, and property taxes—U.S. commercial property tax rates averaged 1.1% in 2023, affecting NOI directly.

Compliance mandates on sustainability and land use—California’s 2023 climate zoning updates and similar measures in 15 states—can force costly retrofit investments and limit redeployment.

Because owners have limited recourse, statutory changes can drop asset-level returns rapidly; a 100-basis-point effective tax hike can cut cap rates and reduce NAV materially.

Capital and Financing Sources

Being owned by Blackstone gives PS Business Parks strong internal liquidity, but 2025 market-wide cost of debt—corporate bond yields ~5.0% and senior CRE loan spreads ~250–300 bps—still shapes deal economics and redevelopment returns.

Traditional lenders and bond markets set financing terms that affect acquisition IRRs; higher rates in 2025 raise required yields and can delay large projects, so PS must manage capital structure to keep its cost of capital competitive with other institutional owners.

Material Costs for Tenant Improvements

Rising raw-material costs—steel up ~18% and ready-mix concrete up ~12% in 2024 vs 2023—raise PS Business Parks’ tenant-improvement (TI) budgets and limit rapid customization for new tenants.

Suppliers keep leverage due to global supply-chain tightness and strong logistics construction demand; PS often passes costs to tenants, but higher TI prices slowed flex-office leasing velocity by an estimated 6% in 2024.

- Steel +18% (2024 vs 2023)

- Concrete +12% (2024 vs 2023)

- TI cost pass-through common

- Flex-office leasing velocity down ~6% (2024)

Supplier pressure squeezes PSB: skills shortage, material inflation & higher OPEX

Suppliers hold meaningful power over PS Business Parks: skilled-trades shortages (6.5% fewer entrants vs 2019) and 2024 raw-material inflation (steel +18%, concrete +12%) raise maintenance/TI costs and extend timelines, while local utilities (commercial electricity ~12.8¢/kWh in 2024) and stricter regulations (CA 2045, NY 2040) further pressure OPEX and capex, forcing long-term contracts, efficiency investments, and careful capital planning to protect NOI.

| Metric | Value |

|---|---|

| Skilled-trades entrants vs 2019 | -6.5% |

| Steel price change (2024 vs 2023) | +18% |

| Concrete price change (2024 vs 2023) | +12% |

| Commercial electricity (2024) | ~12.8¢/kWh |

| Typical NOI risk from maintenance overruns | 5–7% |

What is included in the product

Tailored exclusively for PS Business Parks, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier leverage, entry barriers, substitutes, and emerging threats shaping its industrial and office REIT profitability.

One-sheet Porter's Five Forces for PS Business Parks—quickly spot competitive pressures and tailor mitigation strategies for leasing, capex, and tenant mix decisions.

Customers Bargaining Power

Tenant Base Fragmentation

This tenant fragmentation supports standardized NNN and modified gross leases across ~4,000 properties, making rent renewal negotiations routine and reducing bespoke discounts.

As a result, revenue predictability improved: same-store NOI grew 2.8% in 2024, reflecting fewer tenant-specific concessions and steadier cash flows.

Demand for Flexible Lease Terms

In 2025 tenants demand shorter leases and flexible layouts—CBRE reports 28% of U.S. industrial leases now under 24 months—forcing PS Business Parks to offer adaptable terms and modular suites, which raises tenant negotiating power on rent and concessions.

PSB that resists flexibility risks churn: JLL found flexible-space providers grew occupancy 6.5% YoY in 2024, so failure to adapt can lead to loss to agile competitors prioritizing short-term, scalable leases.

Switching Costs and Location Dependency

For many industrial and flex tenants, moving specialized equipment and re-establishing local supply chains can cost millions and take months, creating strong lock-in that weakens customer bargaining power at PS Business Parks’ lease renewals.

PSB’s campuses near ports, major highways, and rail hubs—over 70% of its 95.6 million rentable square feet in 2024 sat in top logistics markets—further discourage relocation, letting PSB push modest rent increases with limited churn.

Availability of Market Information

The 2025 rise of digital real estate platforms (LoopNet, CoStar, VTS) gives PS Business Parks tenants clearer rent and vacancy data, enabling sharper comparisons and tougher negotiations based on real-time listings and comps.

Greater transparency shrinks the information gap that once favored institutional landlords during price discovery, pressuring PSB to justify premiums with service or location-based differentiation.

- 2025: national CRE vacancy transparency up ~18% vs 2019 (industry reports)

- Tenants use real-time comps to seek 3–7% lower rents

- Data reduces PSB pricing leverage in commoditized markets

Economic Sensitivity of SMBs

SMBs (small and medium-sized businesses) are more exposed to macro swings than large firms, so PS Business Parks faces higher rent-collection volatility; in 2023 SMBs made up about 60% of U.S. commercial leases, and small-firm bankruptcy filings rose 12% year-over-year in Q2 2024.

In downturns tenants often request deferrals or lower rents to avoid insolvency, forcing PSB to weigh short-term concessions against long-term occupancy—PSB reported 95.4% same-store occupancy in 2024 but noted elevated collection work-outs.

PSB must align pricing with tenant health: selective concessions, flexible lease terms, and credit monitoring can preserve occupancy while limiting revenue loss.

- SMBs = higher default sensitivity

- 2023: ~60% of commercial leases from SMBs

- Q2 2024 small-firm bankruptcies +12%

- PSB 2024 same-store occupancy 95.4%

Rising tenant leverage: shorter leases, SMB risk and greater vacancy transparency

| Metric | Value |

|---|---|

| Largest tenant share (2024) | ≤3% |

| Same-store occupancy (2024) | 95.4% |

| SMB share of leases (2023) | ≈60% |

| Industrial leases <24 months (2025) | 28% |

| Vacancy transparency vs 2019 (2025) | +18% |

Full Version Awaits

PS Business Parks Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for PS Business Parks you'll receive after purchase—fully formatted, professionally written, and ready for immediate download. The document contains competitive rivalry, supplier and buyer power, threat of new entrants, and threat of substitutes tailored to PSB’s market position. No placeholders or samples—what you see is the final deliverable available instantly upon payment.