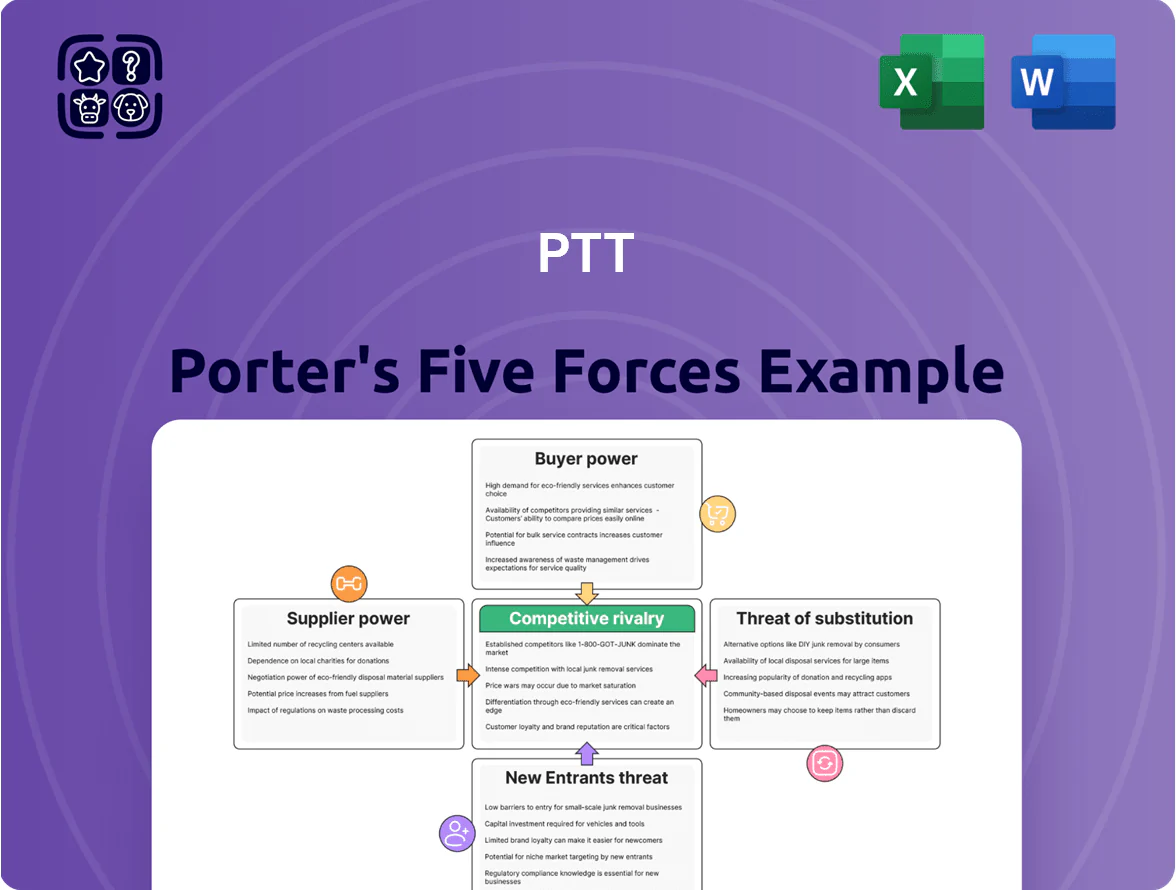

PTT Porter's Five Forces Analysis

Don't Miss the Bigger Picture

PTT faces moderate supplier power, high capital barriers for new entrants, and evolving substitute threats from renewables—while buyer power and intra-industry rivalry shape margins and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PTT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Global Crude Oil Markets

PTT imports roughly 60–70% of Thailand’s crude needs, sourcing mainly from the Middle East and OPEC+; despite PTT Exploration and Production (PTTEP) supplying about 25–30% internally, global market shifts left PTT exposed to 2024–25 Brent swings between $70–95/bbl, raising feedstock cost risk.

This external reliance gives large producers moderate–high bargaining power over prices and volume allocation; supply disruptions in 2022–24 and OPEC+ cuts showed how quickly margins and refining throughput can be impacted.

Vertical Integration through Upstream Subsidiaries

PTT’s ownership of PTTEP (PTT Exploration and Production Public Company Limited) cuts supplier power by supplying about 30–35% of the group’s upstream volumes; PTTEP reported 2024 production of ~235 thousand boe/d, lowering third‑party gas and crude purchases. By owning exploration and production assets across Thailand and abroad, PTT trims dependency on external vendors and shields margins from short-term price swings. This vertical integration improved PTT Group’s gross margin stability in 2024, reducing procurement exposure during 2022–24 volatility.

Specialized Technology and Equipment Vendors

As PTT shifts to high-tech petrochemicals and renewables, dependency on specialized European and North American vendors rises; in 2024 PTT sourced roughly 28% of its advanced process tech from those regions, boosting supplier leverage.

Proprietary carbon capture units and advanced catalysts are niche; vendors can command price premiums of 10–25% and limit spare-part access, raising OPEX and upgrade costs.

PTT must lock multi-year service contracts, localize maintenance, and co-invest in R&D to secure uptime and protect a projected 2030 EBIT margin uplift of ~3 percentage points.

Labor Market Dynamics and Technical Expertise

The supply of highly skilled petroleum and chemical engineers is tightening, raising supplier (labor) bargaining power as firms compete for talent amid digital and decarbonization shifts; Southeast Asian engineering wages rose ~6–8% in 2024, per Mercer, pressuring PTT to pay up.

PTT must boost pay and training—its 2024 LTI (learning & training investment) rose to ~0.9% of operating expenses—to retain specialists for integrated downstream and renewables projects.

- Regional wage growth 6–8% (2024, Mercer)

- PTT training spend ≈0.9% Opex (2024)

- Talent churn raises project delay risk 10–15%

Long-term Natural Gas Procurement Contracts

PTT secures most of Thailand’s gas via long-term deals, including pipelines from Myanmar and LNG contracts; in 2024 PTT imported about 12 bcm of gas, with long-term supplies covering ~70% of demand, which locks volumes but ensures steady feedstock.

These contracts commonly include take-or-pay clauses, limiting PTT’s ability to switch suppliers quickly and reducing short-term bargaining leverage despite price indexation mechanisms that can partially offset risk.

Geopolitics in supplier countries (Myanmar instability, global LNG market tightness) directly affects PTT’s leverage in renegotiations; disruption risk raises re-contracting costs and strengthens suppliers’ position.

- 2024 imports ~12 bcm; ~70% long-term

- Take-or-pay limits flexibility

- Geopolitical risk raises supplier leverage

Moderate‑High Supplier Power: 60–70% imports, PTTEP 25–30%, vendor premiums 10–25%

Supplier power is moderate–high: PTT imports 60–70% crude, PTTEP supplies ~25–30% (PTTEP prod. ~235k boe/d in 2024), LNG imports ~12 bcm with ~70% long‑term; specialized tech/vendor premiums 10–25%; regional engineering wages +6–8% (2024); take‑or‑pay clauses limit flexibility and raise re‑contracting costs.

| Metric | 2024 |

|---|---|

| Crude imported | 60–70% |

| PTTEP supply | 25–30% (235k boe/d) |

| LNG imports | ~12 bcm (70% LT) |

| Vendor premium | 10–25% |

| Wage growth | 6–8% |

What is included in the product

Tailored exclusively for PTT, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics that influence PTT’s pricing, profitability, and strategic positioning.

Clear, one-sheet Porter's Five Forces summary tailored for PTT—quickly spot supply, buyer, and regulatory pressures to streamline strategic decisions.

Customers Bargaining Power

Retail Consumer Price Sensitivity

Individual motorists at PTT stations have low bargaining power, but collective sensitivity to pump prices is high: Thailand’s average petrol price fluctuation of ±3–5 THB/liter in 2024 drove monthly station traffic swings of ~4% per SET-listed petrol retailer reports.

Fuel is a low-differentiation commodity, so price or loyalty perks prompt switching to Bangchak or Shell; PTT’s market share dipped to ~33% in 2024 amid price wars.

PTT reduces churn by boosting non-oil revenue—Café Amazon and convenience stores accounted for ~22% of PTT Oil Retail revenue in 2024—building ecosystem loyalty beyond fuel price alone.

Government Influence and Public Policy

The Thai government, holding ~30.7% direct stake in PTT as of Dec 2025 and acting as the largest domestic fuel buyer, strongly shapes pricing and policy.

Regulators capped diesel subsidies in 2024-25, trimming PTT’s downstream gross margin by an estimated 1.2–1.8 percentage points and limiting retail pricing freedom.

These interventions force PTT to balance profit targets with national energy security obligations, affecting investment timing and tariff strategies.

Industrial and Power Generation Offtakers

Large industrial clients and the Electricity Generating Authority of Thailand (EGAT) buy high volumes—EGAT consumed ~22 bcm of gas in 2023—giving them strong bargaining power to secure long-term, fixed-price deals that pressure margins. PTT must offer competitive pricing; in 2024 PTT’s upstream gas sales accounted for about 45% of domestic supply, so losing one major offtaker would dent volumes and EBITDA. High reliability is critical: Thailand’s peak demand outages in 2022 cost industry an estimated $120m in lost output, so customers can and will seek direct imports or alternative fuels if supply or price falters.

Corporate Shift toward Green Energy Requirements

By end-2025, large B2B customers demand carbon-neutral energy to hit ESG targets; global corporate renewables PPA volume hit ~33 GW in 2024, pressuring PTT to offer certified green power and carbon credits.

If PTT fails, industrial clients can shift procurement to specialist renewables firms—threatening revenue: 2024 industrial electricity sales made up ~40% of Thailand’s commercial demand.

That power forces PTT to speed its move into electricity and renewables to retain its industrial base and protect long-term margins.

- 33 GW corporate PPAs in 2024

- Industrial ~40% of commercial demand (2024)

- Risk: client migration to certified green suppliers

Wholesale Distribution and Export Markets

In petrochemicals and refining, PTT sells into a global wholesale and export market where buyers can choose suppliers from Singapore, China, and GCC hubs; OECD export volumes rose 4% in 2024, intensifying competition.

International customers are highly price-driven and switch on small margin or logistic gains; spot naphtha spreads averaged $45/ton in 2025 YTD, so marginal cost shifts matter.

PTT must use scale and its integrated chain—refining, petrochemicals, shipping—to offer tighter pricing and steadier specs; PTT’s 2024 refining throughput was ~1.1 million bpd, aiding unit-cost leverage.

- Global buyer pool: Singapore/China hubs

- Price sensitivity: spot spreads ~$45/ton (2025 YTD)

- Switching power: low switching costs, high logistics influence

- PTT edge: 1.1 million bpd throughput (2024), integrated chain

PTT: Retail price-sensitive motorists vs powerful B2B buyers—non-oil mix cushions margins

Customers wield mixed power: retail motorists have low individual power but high price sensitivity (±3–5 THB/l swing → ~4% monthly traffic change in 2024), while large B2B buyers and EGAT hold strong leverage via volume and long-term contracts; PTT’s 2024 non-oil mix (Café Amazon + stores ≈22% of oil retail) and 1.1 million bpd refining throughput (2024) blunt price pressure.

| Metric | 2024/25 |

|---|---|

| PTT retail share | ≈33% (2024) |

| Motorist price sensitivity | ±3–5 THB/l → ~4% traffic swing |

| Non-oil retail rev | ≈22% |

| Refining throughput | 1.1 m bpd (2024) |

| Govt stake | ≈30.7% (Dec 2025) |

| Corporate PPAs global | 33 GW (2024) |

What You See Is What You Get

PTT Porter's Five Forces Analysis

This preview shows the exact PTT Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the complete deliverable, and once payment is made you'll gain instant access to this same file. What you see is exactly what you'll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

PTT faces moderate supplier power, high capital barriers for new entrants, and evolving substitute threats from renewables—while buyer power and intra-industry rivalry shape margins and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PTT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Global Crude Oil Markets

PTT imports roughly 60–70% of Thailand’s crude needs, sourcing mainly from the Middle East and OPEC+; despite PTT Exploration and Production (PTTEP) supplying about 25–30% internally, global market shifts left PTT exposed to 2024–25 Brent swings between $70–95/bbl, raising feedstock cost risk.

This external reliance gives large producers moderate–high bargaining power over prices and volume allocation; supply disruptions in 2022–24 and OPEC+ cuts showed how quickly margins and refining throughput can be impacted.

Vertical Integration through Upstream Subsidiaries

PTT’s ownership of PTTEP (PTT Exploration and Production Public Company Limited) cuts supplier power by supplying about 30–35% of the group’s upstream volumes; PTTEP reported 2024 production of ~235 thousand boe/d, lowering third‑party gas and crude purchases. By owning exploration and production assets across Thailand and abroad, PTT trims dependency on external vendors and shields margins from short-term price swings. This vertical integration improved PTT Group’s gross margin stability in 2024, reducing procurement exposure during 2022–24 volatility.

Specialized Technology and Equipment Vendors

As PTT shifts to high-tech petrochemicals and renewables, dependency on specialized European and North American vendors rises; in 2024 PTT sourced roughly 28% of its advanced process tech from those regions, boosting supplier leverage.

Proprietary carbon capture units and advanced catalysts are niche; vendors can command price premiums of 10–25% and limit spare-part access, raising OPEX and upgrade costs.

PTT must lock multi-year service contracts, localize maintenance, and co-invest in R&D to secure uptime and protect a projected 2030 EBIT margin uplift of ~3 percentage points.

Labor Market Dynamics and Technical Expertise

The supply of highly skilled petroleum and chemical engineers is tightening, raising supplier (labor) bargaining power as firms compete for talent amid digital and decarbonization shifts; Southeast Asian engineering wages rose ~6–8% in 2024, per Mercer, pressuring PTT to pay up.

PTT must boost pay and training—its 2024 LTI (learning & training investment) rose to ~0.9% of operating expenses—to retain specialists for integrated downstream and renewables projects.

- Regional wage growth 6–8% (2024, Mercer)

- PTT training spend ≈0.9% Opex (2024)

- Talent churn raises project delay risk 10–15%

Long-term Natural Gas Procurement Contracts

PTT secures most of Thailand’s gas via long-term deals, including pipelines from Myanmar and LNG contracts; in 2024 PTT imported about 12 bcm of gas, with long-term supplies covering ~70% of demand, which locks volumes but ensures steady feedstock.

These contracts commonly include take-or-pay clauses, limiting PTT’s ability to switch suppliers quickly and reducing short-term bargaining leverage despite price indexation mechanisms that can partially offset risk.

Geopolitics in supplier countries (Myanmar instability, global LNG market tightness) directly affects PTT’s leverage in renegotiations; disruption risk raises re-contracting costs and strengthens suppliers’ position.

- 2024 imports ~12 bcm; ~70% long-term

- Take-or-pay limits flexibility

- Geopolitical risk raises supplier leverage

Moderate‑High Supplier Power: 60–70% imports, PTTEP 25–30%, vendor premiums 10–25%

Supplier power is moderate–high: PTT imports 60–70% crude, PTTEP supplies ~25–30% (PTTEP prod. ~235k boe/d in 2024), LNG imports ~12 bcm with ~70% long‑term; specialized tech/vendor premiums 10–25%; regional engineering wages +6–8% (2024); take‑or‑pay clauses limit flexibility and raise re‑contracting costs.

| Metric | 2024 |

|---|---|

| Crude imported | 60–70% |

| PTTEP supply | 25–30% (235k boe/d) |

| LNG imports | ~12 bcm (70% LT) |

| Vendor premium | 10–25% |

| Wage growth | 6–8% |

What is included in the product

Tailored exclusively for PTT, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics that influence PTT’s pricing, profitability, and strategic positioning.

Clear, one-sheet Porter's Five Forces summary tailored for PTT—quickly spot supply, buyer, and regulatory pressures to streamline strategic decisions.

Customers Bargaining Power

Retail Consumer Price Sensitivity

Individual motorists at PTT stations have low bargaining power, but collective sensitivity to pump prices is high: Thailand’s average petrol price fluctuation of ±3–5 THB/liter in 2024 drove monthly station traffic swings of ~4% per SET-listed petrol retailer reports.

Fuel is a low-differentiation commodity, so price or loyalty perks prompt switching to Bangchak or Shell; PTT’s market share dipped to ~33% in 2024 amid price wars.

PTT reduces churn by boosting non-oil revenue—Café Amazon and convenience stores accounted for ~22% of PTT Oil Retail revenue in 2024—building ecosystem loyalty beyond fuel price alone.

Government Influence and Public Policy

The Thai government, holding ~30.7% direct stake in PTT as of Dec 2025 and acting as the largest domestic fuel buyer, strongly shapes pricing and policy.

Regulators capped diesel subsidies in 2024-25, trimming PTT’s downstream gross margin by an estimated 1.2–1.8 percentage points and limiting retail pricing freedom.

These interventions force PTT to balance profit targets with national energy security obligations, affecting investment timing and tariff strategies.

Industrial and Power Generation Offtakers

Large industrial clients and the Electricity Generating Authority of Thailand (EGAT) buy high volumes—EGAT consumed ~22 bcm of gas in 2023—giving them strong bargaining power to secure long-term, fixed-price deals that pressure margins. PTT must offer competitive pricing; in 2024 PTT’s upstream gas sales accounted for about 45% of domestic supply, so losing one major offtaker would dent volumes and EBITDA. High reliability is critical: Thailand’s peak demand outages in 2022 cost industry an estimated $120m in lost output, so customers can and will seek direct imports or alternative fuels if supply or price falters.

Corporate Shift toward Green Energy Requirements

By end-2025, large B2B customers demand carbon-neutral energy to hit ESG targets; global corporate renewables PPA volume hit ~33 GW in 2024, pressuring PTT to offer certified green power and carbon credits.

If PTT fails, industrial clients can shift procurement to specialist renewables firms—threatening revenue: 2024 industrial electricity sales made up ~40% of Thailand’s commercial demand.

That power forces PTT to speed its move into electricity and renewables to retain its industrial base and protect long-term margins.

- 33 GW corporate PPAs in 2024

- Industrial ~40% of commercial demand (2024)

- Risk: client migration to certified green suppliers

Wholesale Distribution and Export Markets

In petrochemicals and refining, PTT sells into a global wholesale and export market where buyers can choose suppliers from Singapore, China, and GCC hubs; OECD export volumes rose 4% in 2024, intensifying competition.

International customers are highly price-driven and switch on small margin or logistic gains; spot naphtha spreads averaged $45/ton in 2025 YTD, so marginal cost shifts matter.

PTT must use scale and its integrated chain—refining, petrochemicals, shipping—to offer tighter pricing and steadier specs; PTT’s 2024 refining throughput was ~1.1 million bpd, aiding unit-cost leverage.

- Global buyer pool: Singapore/China hubs

- Price sensitivity: spot spreads ~$45/ton (2025 YTD)

- Switching power: low switching costs, high logistics influence

- PTT edge: 1.1 million bpd throughput (2024), integrated chain

PTT: Retail price-sensitive motorists vs powerful B2B buyers—non-oil mix cushions margins

Customers wield mixed power: retail motorists have low individual power but high price sensitivity (±3–5 THB/l swing → ~4% monthly traffic change in 2024), while large B2B buyers and EGAT hold strong leverage via volume and long-term contracts; PTT’s 2024 non-oil mix (Café Amazon + stores ≈22% of oil retail) and 1.1 million bpd refining throughput (2024) blunt price pressure.

| Metric | 2024/25 |

|---|---|

| PTT retail share | ≈33% (2024) |

| Motorist price sensitivity | ±3–5 THB/l → ~4% traffic swing |

| Non-oil retail rev | ≈22% |

| Refining throughput | 1.1 m bpd (2024) |

| Govt stake | ≈30.7% (Dec 2025) |

| Corporate PPAs global | 33 GW (2024) |

What You See Is What You Get

PTT Porter's Five Forces Analysis

This preview shows the exact PTT Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the complete deliverable, and once payment is made you'll gain instant access to this same file. What you see is exactly what you'll get.