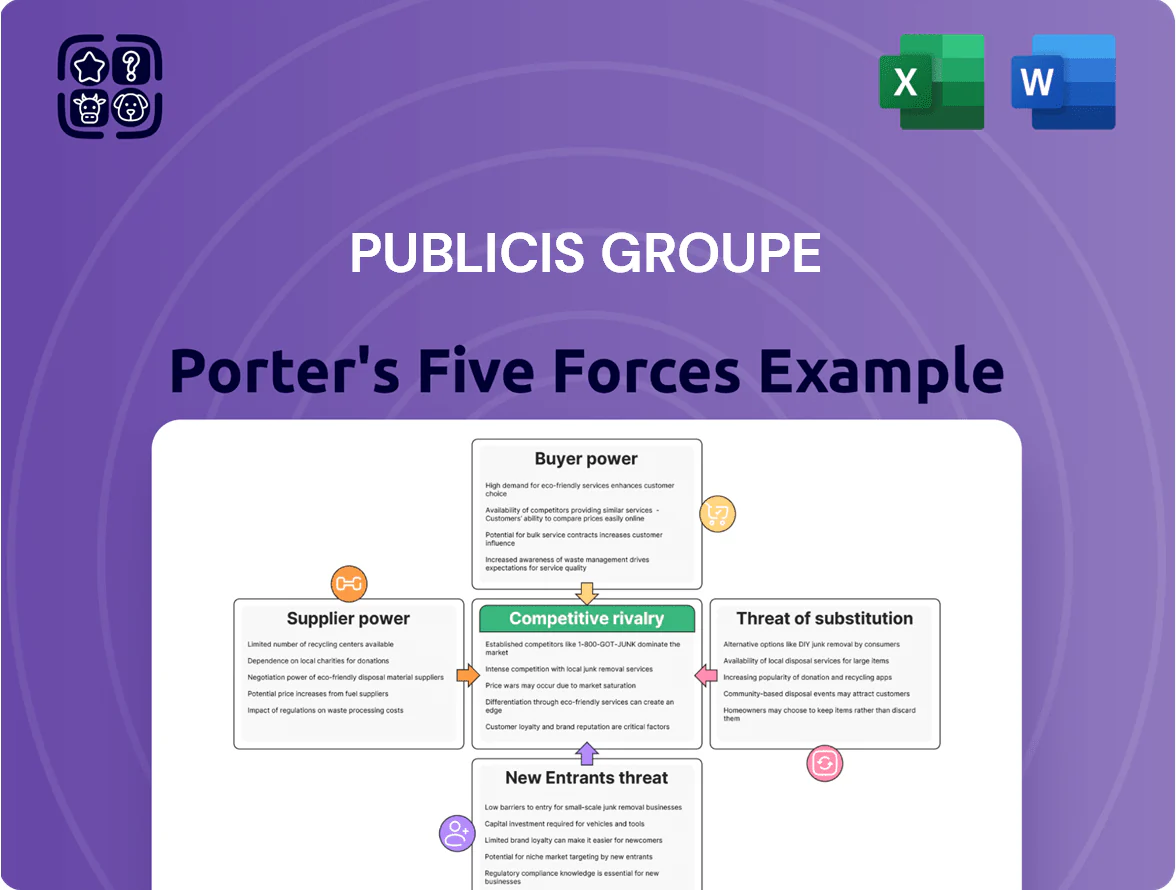

Publicis Groupe Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Publicis Groupe faces moderate buyer power and rising digital substitutes, while its scale and diversified services mitigate supplier and entrant threats, yet competitive intensity among global agencies remains high.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Publicis Groupe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Major Media and Tech Platforms

Global tech giants—Google, Meta, and Amazon—control roughly 70% of global digital ad spend (2024), giving suppliers strong leverage over Publicis Groupe for inventory and user data access. These platforms are essential for client reach and measurement, so Publicis must secure preferred deals and beta access to protect CPMs and campaign performance. In 2024 Publicis reported €11.2bn revenue; losing favored placement would materially raise media costs and hurt margins.

Dependence on Specialized AI and Cloud Infrastructure

As Publicis scales CoreAI, it depends on cloud giants (AWS, Google Cloud, Microsoft) and Nvidia-class GPUs for Sapient and Epsilon; in 2024 cloud capex among top providers exceeded $80bn, concentrating supplier leverage.

These suppliers host and process terabytes of client data and deliver ML acceleration; switching costs include migration, revalidation, and multi-month downtime, often >$10m for enterprise stacks.

High integration and volume pricing mean suppliers can influence fees and SLAs, raising operating risk and margin pressure for Publicis absent long-term contracts or on‑prem offsets.

Competition for High Tier Creative and Technical Talent

Human capital is Publicis Groupe’s core asset, especially data scientists and creative directors; in 2024 demand for data science roles rose ~35% year-over-year and median tech creative salaries climbed 12% in major markets.

These specialists act as labor suppliers who can command premium pay and hybrid/remote terms, raising supplier power and margin pressure.

Publicis must keep investing in employer brand, training, and M&A to retain niche talent; employee attrition above 12% in 2023 correlated with higher client churn.

Data Acquisition and Third Party Information Providers

Publicis, despite owning Epsilon, still buys supplemental data from third-party providers to cover regional gaps; in 2024 Publicis reported Epsilon serving ~70% of its CRM needs but noted external sources fill the rest.

Suppliers can raise prices as privacy rules tighten and first-party data becomes scarce; IAB Europe estimated in 2024 a 12–18% price uplift for premium audience segments after cookie deprecations.

That reliance creates a cost dependency that directly raises media planning expenses and squeezes margins when supplier pricing or compliance costs climb.

- Publicis uses Epsilon for ~70% CRM; 30% from third parties

- 2024 premium data price rise: 12–18% (IAB Europe)

- Higher supplier costs increase media planning spend and margin pressure

Consolidation of Ad Tech Software Vendors

Consolidation in ad-tech leaves fewer, larger software suppliers—by 2024 the top 10 ad-tech firms controlled ~62% of programmatic spend—raising supplier power over attribution, brand-safety, and execution tools used across Publicis workflows.

As these vendors expand through M&A and scale, they push higher licensing fees and proprietary integration standards; Publicis faces rising TCO and lock-in risk to maintain operational efficiency.

- Top-10 control ~62% programmatic spend (2024)

- Fewer vendors → higher licensing and integration demands

- Risk: increased TCO and vendor lock-in

Supply power concentrated: platforms, ad‑tech, cloud & data drive pricing and margin risk

Suppliers hold strong leverage: Google/Meta/Amazon ~70% digital ad spend (2024), top-10 ad-tech ~62% programmatic (2024), cloud capex >€80bn (2024), Epsilon covers ~70% CRM, 30% from third parties, data price uplift 12–18% (IAB Europe 2024); switching costs often >€10m and high talent pay pressures raise margin risk.

| Metric | 2024 |

|---|---|

| Big platforms share | ~70% |

| Top-10 ad-tech | ~62% |

| Cloud capex (top) | €80bn+ |

| Epsilon CRM | ~70% |

| Data price uplift | 12–18% |

What is included in the product

Tailored Porter's Five Forces analysis for Publicis Groupe that uncovers competitive intensity, customer and supplier leverage, entry barriers, and substitute threats, highlighting disruptive trends and strategic implications for market share and profitability.

One-sheet Porter's Five Forces for Publicis Groupe—quickly assess competitive intensity and client bargaining power to streamline strategic choices and relieve decision-making friction.

Customers Bargaining Power

Concentration of Large Multinational Accounts

Publicis serves many of the world’s largest advertisers who account for roughly 35–45% of revenue via multi‑year global contracts (2024 client mix).

These mega‑clients exert strong leverage to push fees down and demand tailored models like Power of One, raising margin pressure.

Loss of a single top account — which can represent 2–5% of annual revenue — can noticeably hit EBITDA and drove stock moves in past account losses.

Shift Toward Performance Based Pricing Models

Clients are shifting from retainers to performance-based pricing, with global marketing contracts tied to KPIs rising ~18% Y/Y in 2024 per WARC, pushing Publicis to bear more revenue risk tied to ROI. This gives buyers leverage to adjust fees based on campaign outcomes, reducing revenue visibility and increasing churn risk. Publicis must therefore share granular data, prove incremental ROI, and tighten creative efficiency to protect margins; digital media CPMs rose ~12% in 2024, squeezing costs.

Threat of In Housing Marketing Operations

Many large clients—about 42% of Global 2000 marketers per a 2024 Forrester survey—have built in‑house creative or media teams to cut agency fees by 10–30% and keep first‑party data control; that creates a real bargaining threat to Publicis.

Clients can shift programmatic buying or content production away quickly, so Publicis must prove external scale and data integration save clients time and lift ROI by measurable margins—Publicis reported 2024 organic growth of 8.3%, showing value but not immunity.

Procurement Led Negotiation Processes

Procurement-led selection has shifted agency deals toward cost and service standarization, pressuring industry margins; global procurement involvement rose to ~62% of marketing sourcing decisions by 2024, driving fee compression of 3–5% annually in pitch-heavy accounts.

Publicis must push its high-value digital transformation work—which delivered 2024 organic growth in Data & Consulting of ~8%—to reframe discussions from price to outcome and protect margin.

- Procurement influence: ~62% of sourcing decisions (2024)

- Fee compression: 3–5% annual pressure

- Publicis strength: Data & Consulting organic growth ~8% in 2024

- Strategy: Sell outcomes, not hourly rates

Low Switching Costs for Project Based Work

While global media mandates remain sticky, about 40% of 2024 global marketing budgets shifted to short-term projects, where switching costs are low.

Clients can trial agencies for digital or creative tasks with minimal disruption, driving churn risk and pressuring margins for Publicis Groupe.

Publicis must continuously re-earn preference via rapid innovation and reliable delivery; its 2024 organic growth of 6.2% helps but isn’t a guarantee.

- ~40% of budgets now short-term (2024)

- Low switching = easy trials, higher churn

- Publicis organic growth 6.2% (2024)

- Requires constant innovation and delivery

Clients Hold the Leverage: Top Accounts, Procurement & In‑House Cuts Squeeze Fees

Customers hold high bargaining power: top global clients drive 35–45% revenue (2024), press for lower fees and outcome‑based pricing (KPIs up ~18% Y/Y), and procurement now influences ~62% of sourcing, causing 3–5% annual fee compression; in‑house teams (≈42% of Global 2000) cut agency fees 10–30% and raise churn risk despite Publicis 2024 organic growth 6.2–8.3% in key units.

| Metric | 2024 |

|---|---|

| Top-client revenue | 35–45% |

| Procurement influence | 62% |

| KPIs tied deals growth | +18% Y/Y |

| Fee compression | 3–5% p.a. |

| In‑house adoption (G2000) | 42% |

| Publicis organic growth | 6.2%–8.3% |

Preview the Actual Deliverable

Publicis Groupe Porter's Five Forces Analysis

This preview shows the exact Publicis Groupe Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or mockups—fully formatted and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Publicis Groupe faces moderate buyer power and rising digital substitutes, while its scale and diversified services mitigate supplier and entrant threats, yet competitive intensity among global agencies remains high.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Publicis Groupe’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Major Media and Tech Platforms

Global tech giants—Google, Meta, and Amazon—control roughly 70% of global digital ad spend (2024), giving suppliers strong leverage over Publicis Groupe for inventory and user data access. These platforms are essential for client reach and measurement, so Publicis must secure preferred deals and beta access to protect CPMs and campaign performance. In 2024 Publicis reported €11.2bn revenue; losing favored placement would materially raise media costs and hurt margins.

Dependence on Specialized AI and Cloud Infrastructure

As Publicis scales CoreAI, it depends on cloud giants (AWS, Google Cloud, Microsoft) and Nvidia-class GPUs for Sapient and Epsilon; in 2024 cloud capex among top providers exceeded $80bn, concentrating supplier leverage.

These suppliers host and process terabytes of client data and deliver ML acceleration; switching costs include migration, revalidation, and multi-month downtime, often >$10m for enterprise stacks.

High integration and volume pricing mean suppliers can influence fees and SLAs, raising operating risk and margin pressure for Publicis absent long-term contracts or on‑prem offsets.

Competition for High Tier Creative and Technical Talent

Human capital is Publicis Groupe’s core asset, especially data scientists and creative directors; in 2024 demand for data science roles rose ~35% year-over-year and median tech creative salaries climbed 12% in major markets.

These specialists act as labor suppliers who can command premium pay and hybrid/remote terms, raising supplier power and margin pressure.

Publicis must keep investing in employer brand, training, and M&A to retain niche talent; employee attrition above 12% in 2023 correlated with higher client churn.

Data Acquisition and Third Party Information Providers

Publicis, despite owning Epsilon, still buys supplemental data from third-party providers to cover regional gaps; in 2024 Publicis reported Epsilon serving ~70% of its CRM needs but noted external sources fill the rest.

Suppliers can raise prices as privacy rules tighten and first-party data becomes scarce; IAB Europe estimated in 2024 a 12–18% price uplift for premium audience segments after cookie deprecations.

That reliance creates a cost dependency that directly raises media planning expenses and squeezes margins when supplier pricing or compliance costs climb.

- Publicis uses Epsilon for ~70% CRM; 30% from third parties

- 2024 premium data price rise: 12–18% (IAB Europe)

- Higher supplier costs increase media planning spend and margin pressure

Consolidation of Ad Tech Software Vendors

Consolidation in ad-tech leaves fewer, larger software suppliers—by 2024 the top 10 ad-tech firms controlled ~62% of programmatic spend—raising supplier power over attribution, brand-safety, and execution tools used across Publicis workflows.

As these vendors expand through M&A and scale, they push higher licensing fees and proprietary integration standards; Publicis faces rising TCO and lock-in risk to maintain operational efficiency.

- Top-10 control ~62% programmatic spend (2024)

- Fewer vendors → higher licensing and integration demands

- Risk: increased TCO and vendor lock-in

Supply power concentrated: platforms, ad‑tech, cloud & data drive pricing and margin risk

Suppliers hold strong leverage: Google/Meta/Amazon ~70% digital ad spend (2024), top-10 ad-tech ~62% programmatic (2024), cloud capex >€80bn (2024), Epsilon covers ~70% CRM, 30% from third parties, data price uplift 12–18% (IAB Europe 2024); switching costs often >€10m and high talent pay pressures raise margin risk.

| Metric | 2024 |

|---|---|

| Big platforms share | ~70% |

| Top-10 ad-tech | ~62% |

| Cloud capex (top) | €80bn+ |

| Epsilon CRM | ~70% |

| Data price uplift | 12–18% |

What is included in the product

Tailored Porter's Five Forces analysis for Publicis Groupe that uncovers competitive intensity, customer and supplier leverage, entry barriers, and substitute threats, highlighting disruptive trends and strategic implications for market share and profitability.

One-sheet Porter's Five Forces for Publicis Groupe—quickly assess competitive intensity and client bargaining power to streamline strategic choices and relieve decision-making friction.

Customers Bargaining Power

Concentration of Large Multinational Accounts

Publicis serves many of the world’s largest advertisers who account for roughly 35–45% of revenue via multi‑year global contracts (2024 client mix).

These mega‑clients exert strong leverage to push fees down and demand tailored models like Power of One, raising margin pressure.

Loss of a single top account — which can represent 2–5% of annual revenue — can noticeably hit EBITDA and drove stock moves in past account losses.

Shift Toward Performance Based Pricing Models

Clients are shifting from retainers to performance-based pricing, with global marketing contracts tied to KPIs rising ~18% Y/Y in 2024 per WARC, pushing Publicis to bear more revenue risk tied to ROI. This gives buyers leverage to adjust fees based on campaign outcomes, reducing revenue visibility and increasing churn risk. Publicis must therefore share granular data, prove incremental ROI, and tighten creative efficiency to protect margins; digital media CPMs rose ~12% in 2024, squeezing costs.

Threat of In Housing Marketing Operations

Many large clients—about 42% of Global 2000 marketers per a 2024 Forrester survey—have built in‑house creative or media teams to cut agency fees by 10–30% and keep first‑party data control; that creates a real bargaining threat to Publicis.

Clients can shift programmatic buying or content production away quickly, so Publicis must prove external scale and data integration save clients time and lift ROI by measurable margins—Publicis reported 2024 organic growth of 8.3%, showing value but not immunity.

Procurement Led Negotiation Processes

Procurement-led selection has shifted agency deals toward cost and service standarization, pressuring industry margins; global procurement involvement rose to ~62% of marketing sourcing decisions by 2024, driving fee compression of 3–5% annually in pitch-heavy accounts.

Publicis must push its high-value digital transformation work—which delivered 2024 organic growth in Data & Consulting of ~8%—to reframe discussions from price to outcome and protect margin.

- Procurement influence: ~62% of sourcing decisions (2024)

- Fee compression: 3–5% annual pressure

- Publicis strength: Data & Consulting organic growth ~8% in 2024

- Strategy: Sell outcomes, not hourly rates

Low Switching Costs for Project Based Work

While global media mandates remain sticky, about 40% of 2024 global marketing budgets shifted to short-term projects, where switching costs are low.

Clients can trial agencies for digital or creative tasks with minimal disruption, driving churn risk and pressuring margins for Publicis Groupe.

Publicis must continuously re-earn preference via rapid innovation and reliable delivery; its 2024 organic growth of 6.2% helps but isn’t a guarantee.

- ~40% of budgets now short-term (2024)

- Low switching = easy trials, higher churn

- Publicis organic growth 6.2% (2024)

- Requires constant innovation and delivery

Clients Hold the Leverage: Top Accounts, Procurement & In‑House Cuts Squeeze Fees

Customers hold high bargaining power: top global clients drive 35–45% revenue (2024), press for lower fees and outcome‑based pricing (KPIs up ~18% Y/Y), and procurement now influences ~62% of sourcing, causing 3–5% annual fee compression; in‑house teams (≈42% of Global 2000) cut agency fees 10–30% and raise churn risk despite Publicis 2024 organic growth 6.2–8.3% in key units.

| Metric | 2024 |

|---|---|

| Top-client revenue | 35–45% |

| Procurement influence | 62% |

| KPIs tied deals growth | +18% Y/Y |

| Fee compression | 3–5% p.a. |

| In‑house adoption (G2000) | 42% |

| Publicis organic growth | 6.2%–8.3% |

Preview the Actual Deliverable

Publicis Groupe Porter's Five Forces Analysis

This preview shows the exact Publicis Groupe Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or mockups—fully formatted and ready for immediate download and use.