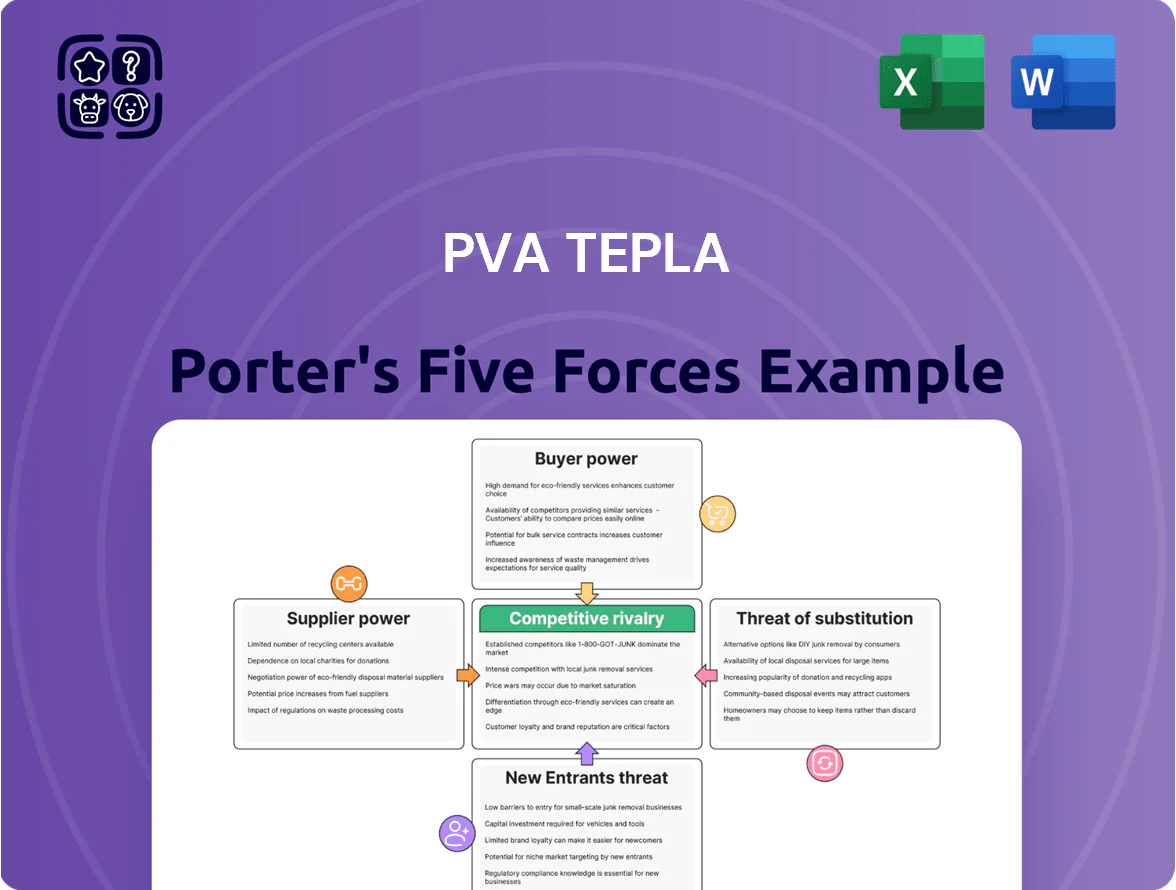

PVA TePla Porter's Five Forces Analysis

From Overview to Strategy Blueprint

PVA TePla operates in a niche high-tech equipment market where supplier specialization and moderate buyer concentration shape competitive dynamics, while capital intensity and IP barriers limit new entrants and substitute threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PVA TePla’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Specialized Component Manufacturers

PVA TePla depends on a small pool of specialized suppliers for vacuum pumps, electronic control units, and advanced sensors, many certified to ISO 9001 and SEMI standards; fewer than 10 global vendors can meet these specs.

Because components must pass strict qualification for semiconductor and crystal-growth tools, supplier concentration gives moderate leverage—switching often takes 6–12+ months of testing and re-qualification.

In 2024 PVA TePla reported ~28% of COGS tied to bought-in precision parts, so supplier delays or price hikes can meaningfully hit margins.

Impact of Raw Material Price Volatility

The production of high-temperature furnaces and plasma systems needs large volumes of specialty metals and high-grade graphite, and global price swings—graphite up ~45% in 2021–2022 and nickel +30% in 2023—can lift PVA TePla’s BOM costs materially.

PVA TePla uses long-term supply contracts to smooth volatility, but suppliers keep leverage via scarcity-driven price resets and energy-cost pass-throughs; a 10% raw-material price rise could cut gross margin by ~3–5 percentage points based on 2024 product mix.

Technological Integration and Intellectual Property

Certain suppliers deliver proprietary sub-systems that are tightly embedded in PVA TePla’s high-vacuum and thermal systems, creating technical dependency; about 30–40% of system value can stem from these modules (company parts-cost estimates, 2024).

If a key tech vendor shifts its roadmap or hikes licensing by 10–25%, PVA TePla could face production delays for specific product lines and margin pressure; dual-sourcing is costly and slow.

Therefore PVA TePla favors collaborative partnerships, joint roadmaps, and multi-year contracts, which raises supplier influence over timelines and contingency planning.

Limited Threat of Forward Integration

Most suppliers to PVA TePla provide niche components or raw materials and lack system-level engineering to produce full crystal-growing or plasma systems, so forward integration risk is low and supplier bargaining power is limited.

Still, because components are specialized, suppliers exert leverage over delivery timing and specs; delays or spec changes can impact PVA TePla’s production cadence and margins—supplier-related delays rose ~12% in semiconductor-equipment supply chains in 2023.

- Low forward integration risk due to missing system engineering

- Supplier power limited vs. commoditized industries

- High influence on delivery schedules and technical specs

- Supply-chain delays up ~12% in 2023 for related equipment

Geographic Concentration of Supply Chains

A significant share of PVA TePla’s specialized suppliers sit in Europe and Asia, exposing the firm to regional slowdowns and port/backlog risks; 2024 trade data showed 62% of critical components sourced from these regions.

By 2025 the company raised strategic inventory by ~18% and added secondary vendors, cutting single‑supplier spend from 47% to 31% to lower leverage.

Still, scarcity of high‑end engineering at supplier firms keeps supplier power elevated—senior supplier engineers remain a choke point for complex modules.

- 62% critical parts from EU/Asia

- Inventory +18% by 2025

- Single‑supplier spend fell 47% → 31%

- Engineering talent shortage sustains supplier leverage

PVA TePla: Tight certified supply raises margins risk despite improving supplier diversification

Specialized suppliers give PVA TePla moderate bargaining power:

certified vendors <10, long re‑qualification 6–12+ months, 2024 bought‑in parts ≈28% COGS; raw‑material swings (graphite +45% ’21–’22, nickel +30% ’23) can cut gross margin ~3–5 ppt on a 10% price rise. By 2025 inventory +18%, single‑supplier spend 47%→31%, but engineering scarcity keeps delivery/spec leverage high.

| Metric | Value |

|---|---|

| Vendors meeting specs | <10 |

| Bought‑in parts (% COGS, 2024) | ≈28% |

| Inventory change (2025) | +18% |

| Single‑supplier spend | 47% → 31% |

| Material price moves | Graphite +45% (’21–’22), Nickel +30% (’23) |

| Supply delays rise (2023) | +12% |

| Re‑qualification | 6–12+ months |

What is included in the product

Tailored Porter's Five Forces analysis for PVA TePla that uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and identifies disruptive forces and strategic levers to protect margin and market position.

A concise Porter's Five Forces one-sheet tailored to PVA TePla—instantly highlights competitive pressures and strategic levers for faster, clearer decision-making.

Customers Bargaining Power

Concentration of Large Scale Industrial Buyers

The customer base for PVA TePla is concentrated among major semiconductor manufacturers, power-electronics producers, and hard-metal specialists, with the top 10 customers accounting for roughly 55% of 2024 equipment revenue.

Those large buyers place high-volume orders for entire production lines, giving them strong leverage to push for price discounts and extended service terms; single-contract discounts can exceed 10% on multi‑year deals.

Loss of a single top-tier semiconductor contract can cut annual revenue forecasts by an estimated 8–12%, based on PVA TePla’s 2024 order book and typical line-item values.

High Switching Costs and System Integration

Once a customer integrates a PVA TePla crystal-growing furnace or metrology system into production, switching costs are very high; industry reports show tool redeployment and validation can cost 0.5–2.0 million euros and take 3–9 months per line.

Systems are often customized to material specs, so vendor change requires massive reinvestment in process calibration, spare parts and employee retraining, raising total migration costs by an estimated 30–60%.

This technical lock-in after purchase sharply reduces customer bargaining power, so price concessions and service pressures are strongest pre-sale and drop materially post-installation.

Demand for Cutting Edge Performance and Precision

Customers in semiconductors and renewables value cutting-edge performance, reliability, and yield over lowest price, and PVA TePla’s equipment for Silicon Carbide (SiC) wafers commands premiums—SiC wafer market revenue grew ~28% in 2024 to $1.9bn, showing willingness to pay for proven tech.

Because these systems are mission-critical, customers accept higher CAPEX to secure uptime and yield, reducing bargaining leverage; PVA TePla’s 2024 service and spare-parts revenue of €45m underlines this premium mix.

Project Based Procurement Cycles

Customers hold strong leverage in early bidding for capital-heavy high-tech tools, often driving down prices and winning favorable financing or multi-year service contracts; bids for SiC fabs in 2024–25 showed suppliers offering payment terms up to 24 months and service discounts of 5–12% on €50–200m systems.

Yet by 2026 urgent SiC capacity needs (industry forecasts: global SiC wafer demand CAGR ~28% 2023–26) have tightened supplier schedules, shifting bargaining power toward equipment makers as lead times extend and delivery slots become scarce.

- High buyer leverage in tenders; 24-month payment terms common

- Service/finance used as negotiation levers; discounts 5–12%

- SiC demand CAGR ~28% (2023–26) tightens supply

- By 2026 supplier lead-times and scarce slots restore provider power

Backward Integration Potential of Tech Giants

Large semiconductor firms like TSMC and Intel could theoretically backward-integrate into crystal growth/inspection to cut costs, but that needs R&D often >$500m and niche physics hires; Apple and Samsung have shown partial vertical moves, and Intel spent $20bn+ on fabs in 2023–25.

This long-term threat forces PVA TePla to push efficiency—patent-led modules, faster cycle times, and service contracts—to keep third-party systems cheaper than in-house builds.

- R&D bar: ≥$100–500m per tech line

- Capex examples: Intel $20bn+ (2023–25)

- Mitigation: patents, SLAs, speed gains

Customer leverage now—but high post‑install lock‑in and booming SiC demand flip power by 2026

Customers wield strong pre-sale leverage—top 10 clients ≈55% of 2024 revenue; discounts 5–12%, payment terms up to 24 months—but post-installation lock-in is high (switch costs €0.5–2.0m; migration +30–60%), and rising SiC demand (CAGR ~28% 2023–26) has tightened supply, shifting some power back to PVA TePla by 2026.

| Metric | Value |

|---|---|

| Top-10 share | ≈55% (2024) |

| Discounts | 5–12% |

| Switch cost | €0.5–2.0m |

| SiC CAGR | ~28% (2023–26) |

Preview Before You Purchase

PVA TePla Porter's Five Forces Analysis

This preview shows the exact PVA TePla Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

PVA TePla operates in a niche high-tech equipment market where supplier specialization and moderate buyer concentration shape competitive dynamics, while capital intensity and IP barriers limit new entrants and substitute threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore PVA TePla’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Specialized Component Manufacturers

PVA TePla depends on a small pool of specialized suppliers for vacuum pumps, electronic control units, and advanced sensors, many certified to ISO 9001 and SEMI standards; fewer than 10 global vendors can meet these specs.

Because components must pass strict qualification for semiconductor and crystal-growth tools, supplier concentration gives moderate leverage—switching often takes 6–12+ months of testing and re-qualification.

In 2024 PVA TePla reported ~28% of COGS tied to bought-in precision parts, so supplier delays or price hikes can meaningfully hit margins.

Impact of Raw Material Price Volatility

The production of high-temperature furnaces and plasma systems needs large volumes of specialty metals and high-grade graphite, and global price swings—graphite up ~45% in 2021–2022 and nickel +30% in 2023—can lift PVA TePla’s BOM costs materially.

PVA TePla uses long-term supply contracts to smooth volatility, but suppliers keep leverage via scarcity-driven price resets and energy-cost pass-throughs; a 10% raw-material price rise could cut gross margin by ~3–5 percentage points based on 2024 product mix.

Technological Integration and Intellectual Property

Certain suppliers deliver proprietary sub-systems that are tightly embedded in PVA TePla’s high-vacuum and thermal systems, creating technical dependency; about 30–40% of system value can stem from these modules (company parts-cost estimates, 2024).

If a key tech vendor shifts its roadmap or hikes licensing by 10–25%, PVA TePla could face production delays for specific product lines and margin pressure; dual-sourcing is costly and slow.

Therefore PVA TePla favors collaborative partnerships, joint roadmaps, and multi-year contracts, which raises supplier influence over timelines and contingency planning.

Limited Threat of Forward Integration

Most suppliers to PVA TePla provide niche components or raw materials and lack system-level engineering to produce full crystal-growing or plasma systems, so forward integration risk is low and supplier bargaining power is limited.

Still, because components are specialized, suppliers exert leverage over delivery timing and specs; delays or spec changes can impact PVA TePla’s production cadence and margins—supplier-related delays rose ~12% in semiconductor-equipment supply chains in 2023.

- Low forward integration risk due to missing system engineering

- Supplier power limited vs. commoditized industries

- High influence on delivery schedules and technical specs

- Supply-chain delays up ~12% in 2023 for related equipment

Geographic Concentration of Supply Chains

A significant share of PVA TePla’s specialized suppliers sit in Europe and Asia, exposing the firm to regional slowdowns and port/backlog risks; 2024 trade data showed 62% of critical components sourced from these regions.

By 2025 the company raised strategic inventory by ~18% and added secondary vendors, cutting single‑supplier spend from 47% to 31% to lower leverage.

Still, scarcity of high‑end engineering at supplier firms keeps supplier power elevated—senior supplier engineers remain a choke point for complex modules.

- 62% critical parts from EU/Asia

- Inventory +18% by 2025

- Single‑supplier spend fell 47% → 31%

- Engineering talent shortage sustains supplier leverage

PVA TePla: Tight certified supply raises margins risk despite improving supplier diversification

Specialized suppliers give PVA TePla moderate bargaining power:

certified vendors <10, long re‑qualification 6–12+ months, 2024 bought‑in parts ≈28% COGS; raw‑material swings (graphite +45% ’21–’22, nickel +30% ’23) can cut gross margin ~3–5 ppt on a 10% price rise. By 2025 inventory +18%, single‑supplier spend 47%→31%, but engineering scarcity keeps delivery/spec leverage high.

| Metric | Value |

|---|---|

| Vendors meeting specs | <10 |

| Bought‑in parts (% COGS, 2024) | ≈28% |

| Inventory change (2025) | +18% |

| Single‑supplier spend | 47% → 31% |

| Material price moves | Graphite +45% (’21–’22), Nickel +30% (’23) |

| Supply delays rise (2023) | +12% |

| Re‑qualification | 6–12+ months |

What is included in the product

Tailored Porter's Five Forces analysis for PVA TePla that uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and identifies disruptive forces and strategic levers to protect margin and market position.

A concise Porter's Five Forces one-sheet tailored to PVA TePla—instantly highlights competitive pressures and strategic levers for faster, clearer decision-making.

Customers Bargaining Power

Concentration of Large Scale Industrial Buyers

The customer base for PVA TePla is concentrated among major semiconductor manufacturers, power-electronics producers, and hard-metal specialists, with the top 10 customers accounting for roughly 55% of 2024 equipment revenue.

Those large buyers place high-volume orders for entire production lines, giving them strong leverage to push for price discounts and extended service terms; single-contract discounts can exceed 10% on multi‑year deals.

Loss of a single top-tier semiconductor contract can cut annual revenue forecasts by an estimated 8–12%, based on PVA TePla’s 2024 order book and typical line-item values.

High Switching Costs and System Integration

Once a customer integrates a PVA TePla crystal-growing furnace or metrology system into production, switching costs are very high; industry reports show tool redeployment and validation can cost 0.5–2.0 million euros and take 3–9 months per line.

Systems are often customized to material specs, so vendor change requires massive reinvestment in process calibration, spare parts and employee retraining, raising total migration costs by an estimated 30–60%.

This technical lock-in after purchase sharply reduces customer bargaining power, so price concessions and service pressures are strongest pre-sale and drop materially post-installation.

Demand for Cutting Edge Performance and Precision

Customers in semiconductors and renewables value cutting-edge performance, reliability, and yield over lowest price, and PVA TePla’s equipment for Silicon Carbide (SiC) wafers commands premiums—SiC wafer market revenue grew ~28% in 2024 to $1.9bn, showing willingness to pay for proven tech.

Because these systems are mission-critical, customers accept higher CAPEX to secure uptime and yield, reducing bargaining leverage; PVA TePla’s 2024 service and spare-parts revenue of €45m underlines this premium mix.

Project Based Procurement Cycles

Customers hold strong leverage in early bidding for capital-heavy high-tech tools, often driving down prices and winning favorable financing or multi-year service contracts; bids for SiC fabs in 2024–25 showed suppliers offering payment terms up to 24 months and service discounts of 5–12% on €50–200m systems.

Yet by 2026 urgent SiC capacity needs (industry forecasts: global SiC wafer demand CAGR ~28% 2023–26) have tightened supplier schedules, shifting bargaining power toward equipment makers as lead times extend and delivery slots become scarce.

- High buyer leverage in tenders; 24-month payment terms common

- Service/finance used as negotiation levers; discounts 5–12%

- SiC demand CAGR ~28% (2023–26) tightens supply

- By 2026 supplier lead-times and scarce slots restore provider power

Backward Integration Potential of Tech Giants

Large semiconductor firms like TSMC and Intel could theoretically backward-integrate into crystal growth/inspection to cut costs, but that needs R&D often >$500m and niche physics hires; Apple and Samsung have shown partial vertical moves, and Intel spent $20bn+ on fabs in 2023–25.

This long-term threat forces PVA TePla to push efficiency—patent-led modules, faster cycle times, and service contracts—to keep third-party systems cheaper than in-house builds.

- R&D bar: ≥$100–500m per tech line

- Capex examples: Intel $20bn+ (2023–25)

- Mitigation: patents, SLAs, speed gains

Customer leverage now—but high post‑install lock‑in and booming SiC demand flip power by 2026

Customers wield strong pre-sale leverage—top 10 clients ≈55% of 2024 revenue; discounts 5–12%, payment terms up to 24 months—but post-installation lock-in is high (switch costs €0.5–2.0m; migration +30–60%), and rising SiC demand (CAGR ~28% 2023–26) has tightened supply, shifting some power back to PVA TePla by 2026.

| Metric | Value |

|---|---|

| Top-10 share | ≈55% (2024) |

| Discounts | 5–12% |

| Switch cost | €0.5–2.0m |

| SiC CAGR | ~28% (2023–26) |

Preview Before You Purchase

PVA TePla Porter's Five Forces Analysis

This preview shows the exact PVA TePla Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.