PW Medtech Group PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, regulatory pressures, and technological advances are reshaping PW Medtech Group’s prospects—our concise PESTLE highlights the risks and opportunities that matter to investors and strategists; buy the full analysis to access the complete, actionable breakdown and downloadable templates for immediate use.

Political factors

Government healthcare reform policies

The Healthy China 2030 plan and renewed push for universal health coverage are accelerating hospital upgrades and demand for domestic medtech; government R&D subsidies and procurement preferences lifted Chinese medtech investment to RMB 120bn in 2024, benefiting PW Medtech’s interventional devices as hospital procedure volumes grew ~8% YoY, directly supporting the company’s long-term volume and market-penetration strategies.

Geopolitical trade tensions

Ongoing China-West trade friction disrupts access to high-end raw materials and specialized equipment, raising component costs for PW Medtech’s cardiovascular and orthopedic lines—e.g., semiconductor and titanium supply tightness pushed input prices up ~8–12% in 2024 for medical-device suppliers. Export controls and potential tariffs could add 5–15% to bill-of-materials costs, while political instability in target markets risks derailing planned 20–30% revenue growth from overseas expansion.

Centralized procurement expansion

The expansion of China’s Volume-Based Procurement (VBP) since 2023 has driven price cuts up to 60% for selected medical devices, reshaping competition and pressuring margins on high-volume items such as stents and orthopedic implants where PW Medtech earns ~45% of sales.

Guaranteed hospital volumes from VBP force PW Medtech to accept lower unit prices—management reported a 12% gross margin compression in 2024 for VBP-participating SKUs—necessitating tighter cost control.

To retain market share in the >70% hospital procurement channel, PW Medtech must adapt pricing to state bidding cycles, optimize manufacturing scale, and target non-VBP niche products to preserve overall profitability.

Support for domestic substitution

Political mandates promoting Made in China medical devices give PW Medtech a measurable advantage: government procurement policies raised domestic share in public hospital device purchases to 62% in 2024, up from 51% in 2020, favoring local suppliers over multinationals.

Local governments offer subsidies and preferential hospital quotas—some provinces provide up to 15% price subsidies or procurement preference for domestic cardiovascular and orthopedic devices—enabling PW Medtech to reclaim market share from global incumbents.

Regulatory alignment with global standards

The NMPA’s continued alignment with IMDRF frameworks has cut average device approval times by about 20% since 2018, accelerating PW Medtech’s go‑to‑market for exportable devices and easing technology transfers for joint ventures.

Harmonization reduces regulatory duplication and lowers market-entry costs, supporting PW Medtech’s overseas expansion and licensing deals.

Concurrently, heightened political oversight on clinical data integrity has driven a 15–25% rise in compliance and QA spending across Chinese medtech firms, forcing PW Medtech to boost related CAPEX and audit capacity.

- Approval times down ~20% since 2018

- Compliance/QA costs up 15–25%

- Improved ease for overseas entry and tech transfers

China policy reshapes device market: 62% local share, margins squeezed ~12%

Political drivers—Healthy China 2030, VBP expansion, Made-in-China procurement and NMPA-IMDRF alignment—raised domestic hospital device share to 62% in 2024, cut approvals ~20% since 2018, but pushed compliance costs up 15–25% and drove 8–12% input price inflation from trade frictions, compressing VBP SKU gross margins ~12% in 2024.

| Metric | 2024 |

|---|---|

| Domestic procurement share | 62% |

| Approval time change since 2018 | -20% |

| Compliance/QA cost rise | 15–25% |

| Input price inflation | 8–12% |

| VBP SKU margin compression | ~12% |

What is included in the product

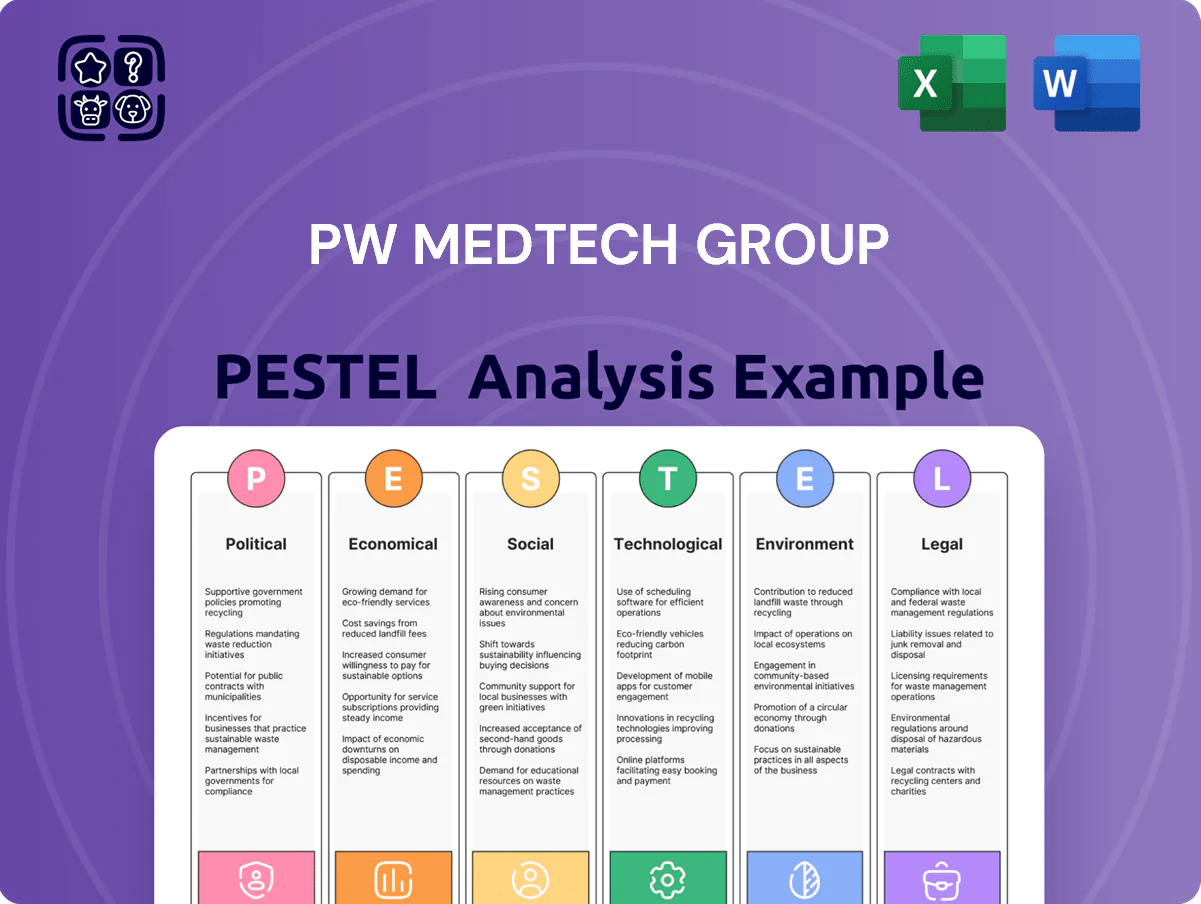

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact PW Medtech Group, with each section drawing on current market data and regional regulatory dynamics to identify risks and growth opportunities.

A concise, PESTLE-segmented brief that highlights external risks and opportunities for PW Medtech Group, enabling quick inclusion in presentations, collaborative planning, or consultant reports while allowing users to add region- or product-specific notes.

Economic factors

Healthcare spending growth

Rising GDP and a 2024 per capita disposable income of about CNY 36,000 in China support higher healthcare spending, driving demand for PW Medtech’s cardiovascular and orthopedic devices as elective procedures grow. Affluent patients increasingly opt for advanced interventions, with China’s healthcare expenditure rising to ~7.1% of GDP in 2023, expanding market opportunities. Economic growth in lower-tier cities—where disposable income rose faster than national average in 2023—fuels demand as infrastructure and hospital upgrades reach underserved regions.

Cost pressure from VBP

The economic reality of Volume-Based Procurement has driven price erosion up to 40-60% for mature device categories in China by 2024, pressuring PW Medtech’s margins.

To remain profitable under lower tender prices the company must cut manufacturing costs and boost supply-chain efficiency; industry targets show 10-15% cost-to-serve reductions achievable via automation and local sourcing.

Diversification into non-VBP high-margin innovative products—where gross margins often exceed 60%—is critical for economic survival given VBP-driven revenue squeezes.

Currency exchange rate volatility

PW Medtech’s international exposure makes Renminbi volatility versus the US dollar and euro material: a 5% RMB depreciation in 2024 would raise imported component costs by roughly the same magnitude, squeezing gross margins, while a 3–7% RMB appreciation in 2023–24 periods improved export competitiveness for select product lines; FX swings also produced non-operating FX losses of $4–7 million across comparable peers during 2023–24, a risk to net income.

Interest rates and capital access

The prevailing interest rate environment in 2025–2026 raises PW Medtech’s average borrowing cost; global policy rates rose to about 4.5% (Fed funds) in 2024–25, lifting corporate yields and increasing project debt service burdens for R&D and facility expansion.

Access to low-cost capital remains critical: recent medtech deals saw leverage at 4–6x EBITDA, and higher rates could derail acquisitions or delay a planned €80–120m manufacturing buildout, while easing monetary policy would restore capacity for leveraged buyouts and capex.

- 2024–25 policy rates ~4–4.5% impacting borrowing costs

- Typical sector leverage 4–6x EBITDA for acquisitions

- Planned capex range €80–120m sensitive to rate shifts

- Monetary easing would enable renewed M&A and capex

Inflationary impact on production

PW Medtech faces rising labor and input costs—global manufacturing wages grew ~6% in 2024 and metal/plastic prices rose ~8–12% year-on-year—pushing up COGS while government tender pricing remains constrained.

To protect margins, the company must scale automation and lean manufacturing; capital expenditure on robotics can cut labor needs by 20–30% and improve unit costs amid 4–6% CPI-driven inflation.

- Labor inflation ~6% (2024); raw material +8–12% YoY

- Government procurement exerts downward pricing pressure

- Automation/lean can reduce labor costs 20–30%

- Target efficiency to offset 4–6% CPI impact

China medtech: demand rises but VBP cuts, cost inflation & FX/rate risks squeeze margins

Economic growth (China GDP +5.2% in 2024) and CNY36,000 per-capita disposable income boost elective procedure demand, while VBP-driven price erosion (40–60%) and input inflation (labor +6%, materials +8–12% in 2024) squeeze margins; RMB volatility (±5% in 2024) and higher rates (~4–4.5% 2024–25) raise FX and financing risks, making automation, local sourcing and high-margin product diversification essential.

| Metric | 2024–25 |

|---|---|

| China GDP growth | +5.2% |

| Disposable income | CNY 36,000 |

| VBP price erosion | 40–60% |

| Labor inflation | +6% |

| Materials | +8–12% |

| Policy rates | 4–4.5% |

| RMB swing | ±5% |

Preview the Actual Deliverable

PW Medtech Group PESTLE Analysis

The preview shown here is the exact PW Medtech Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, regulatory pressures, and technological advances are reshaping PW Medtech Group’s prospects—our concise PESTLE highlights the risks and opportunities that matter to investors and strategists; buy the full analysis to access the complete, actionable breakdown and downloadable templates for immediate use.

Political factors

Government healthcare reform policies

The Healthy China 2030 plan and renewed push for universal health coverage are accelerating hospital upgrades and demand for domestic medtech; government R&D subsidies and procurement preferences lifted Chinese medtech investment to RMB 120bn in 2024, benefiting PW Medtech’s interventional devices as hospital procedure volumes grew ~8% YoY, directly supporting the company’s long-term volume and market-penetration strategies.

Geopolitical trade tensions

Ongoing China-West trade friction disrupts access to high-end raw materials and specialized equipment, raising component costs for PW Medtech’s cardiovascular and orthopedic lines—e.g., semiconductor and titanium supply tightness pushed input prices up ~8–12% in 2024 for medical-device suppliers. Export controls and potential tariffs could add 5–15% to bill-of-materials costs, while political instability in target markets risks derailing planned 20–30% revenue growth from overseas expansion.

Centralized procurement expansion

The expansion of China’s Volume-Based Procurement (VBP) since 2023 has driven price cuts up to 60% for selected medical devices, reshaping competition and pressuring margins on high-volume items such as stents and orthopedic implants where PW Medtech earns ~45% of sales.

Guaranteed hospital volumes from VBP force PW Medtech to accept lower unit prices—management reported a 12% gross margin compression in 2024 for VBP-participating SKUs—necessitating tighter cost control.

To retain market share in the >70% hospital procurement channel, PW Medtech must adapt pricing to state bidding cycles, optimize manufacturing scale, and target non-VBP niche products to preserve overall profitability.

Support for domestic substitution

Political mandates promoting Made in China medical devices give PW Medtech a measurable advantage: government procurement policies raised domestic share in public hospital device purchases to 62% in 2024, up from 51% in 2020, favoring local suppliers over multinationals.

Local governments offer subsidies and preferential hospital quotas—some provinces provide up to 15% price subsidies or procurement preference for domestic cardiovascular and orthopedic devices—enabling PW Medtech to reclaim market share from global incumbents.

Regulatory alignment with global standards

The NMPA’s continued alignment with IMDRF frameworks has cut average device approval times by about 20% since 2018, accelerating PW Medtech’s go‑to‑market for exportable devices and easing technology transfers for joint ventures.

Harmonization reduces regulatory duplication and lowers market-entry costs, supporting PW Medtech’s overseas expansion and licensing deals.

Concurrently, heightened political oversight on clinical data integrity has driven a 15–25% rise in compliance and QA spending across Chinese medtech firms, forcing PW Medtech to boost related CAPEX and audit capacity.

- Approval times down ~20% since 2018

- Compliance/QA costs up 15–25%

- Improved ease for overseas entry and tech transfers

China policy reshapes device market: 62% local share, margins squeezed ~12%

Political drivers—Healthy China 2030, VBP expansion, Made-in-China procurement and NMPA-IMDRF alignment—raised domestic hospital device share to 62% in 2024, cut approvals ~20% since 2018, but pushed compliance costs up 15–25% and drove 8–12% input price inflation from trade frictions, compressing VBP SKU gross margins ~12% in 2024.

| Metric | 2024 |

|---|---|

| Domestic procurement share | 62% |

| Approval time change since 2018 | -20% |

| Compliance/QA cost rise | 15–25% |

| Input price inflation | 8–12% |

| VBP SKU margin compression | ~12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact PW Medtech Group, with each section drawing on current market data and regional regulatory dynamics to identify risks and growth opportunities.

A concise, PESTLE-segmented brief that highlights external risks and opportunities for PW Medtech Group, enabling quick inclusion in presentations, collaborative planning, or consultant reports while allowing users to add region- or product-specific notes.

Economic factors

Healthcare spending growth

Rising GDP and a 2024 per capita disposable income of about CNY 36,000 in China support higher healthcare spending, driving demand for PW Medtech’s cardiovascular and orthopedic devices as elective procedures grow. Affluent patients increasingly opt for advanced interventions, with China’s healthcare expenditure rising to ~7.1% of GDP in 2023, expanding market opportunities. Economic growth in lower-tier cities—where disposable income rose faster than national average in 2023—fuels demand as infrastructure and hospital upgrades reach underserved regions.

Cost pressure from VBP

The economic reality of Volume-Based Procurement has driven price erosion up to 40-60% for mature device categories in China by 2024, pressuring PW Medtech’s margins.

To remain profitable under lower tender prices the company must cut manufacturing costs and boost supply-chain efficiency; industry targets show 10-15% cost-to-serve reductions achievable via automation and local sourcing.

Diversification into non-VBP high-margin innovative products—where gross margins often exceed 60%—is critical for economic survival given VBP-driven revenue squeezes.

Currency exchange rate volatility

PW Medtech’s international exposure makes Renminbi volatility versus the US dollar and euro material: a 5% RMB depreciation in 2024 would raise imported component costs by roughly the same magnitude, squeezing gross margins, while a 3–7% RMB appreciation in 2023–24 periods improved export competitiveness for select product lines; FX swings also produced non-operating FX losses of $4–7 million across comparable peers during 2023–24, a risk to net income.

Interest rates and capital access

The prevailing interest rate environment in 2025–2026 raises PW Medtech’s average borrowing cost; global policy rates rose to about 4.5% (Fed funds) in 2024–25, lifting corporate yields and increasing project debt service burdens for R&D and facility expansion.

Access to low-cost capital remains critical: recent medtech deals saw leverage at 4–6x EBITDA, and higher rates could derail acquisitions or delay a planned €80–120m manufacturing buildout, while easing monetary policy would restore capacity for leveraged buyouts and capex.

- 2024–25 policy rates ~4–4.5% impacting borrowing costs

- Typical sector leverage 4–6x EBITDA for acquisitions

- Planned capex range €80–120m sensitive to rate shifts

- Monetary easing would enable renewed M&A and capex

Inflationary impact on production

PW Medtech faces rising labor and input costs—global manufacturing wages grew ~6% in 2024 and metal/plastic prices rose ~8–12% year-on-year—pushing up COGS while government tender pricing remains constrained.

To protect margins, the company must scale automation and lean manufacturing; capital expenditure on robotics can cut labor needs by 20–30% and improve unit costs amid 4–6% CPI-driven inflation.

- Labor inflation ~6% (2024); raw material +8–12% YoY

- Government procurement exerts downward pricing pressure

- Automation/lean can reduce labor costs 20–30%

- Target efficiency to offset 4–6% CPI impact

China medtech: demand rises but VBP cuts, cost inflation & FX/rate risks squeeze margins

Economic growth (China GDP +5.2% in 2024) and CNY36,000 per-capita disposable income boost elective procedure demand, while VBP-driven price erosion (40–60%) and input inflation (labor +6%, materials +8–12% in 2024) squeeze margins; RMB volatility (±5% in 2024) and higher rates (~4–4.5% 2024–25) raise FX and financing risks, making automation, local sourcing and high-margin product diversification essential.

| Metric | 2024–25 |

|---|---|

| China GDP growth | +5.2% |

| Disposable income | CNY 36,000 |

| VBP price erosion | 40–60% |

| Labor inflation | +6% |

| Materials | +8–12% |

| Policy rates | 4–4.5% |

| RMB swing | ±5% |

Preview the Actual Deliverable

PW Medtech Group PESTLE Analysis

The preview shown here is the exact PW Medtech Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.