PZ Cussons PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and evolving consumer trends are shaping PZ Cussons’ strategic outlook—our concise PESTLE highlights risks and opportunities you can act on. Purchase the full analysis for a complete, editable report packed with data-driven insights ideal for investors, consultants, and strategy teams. Download now to make smarter, faster decisions.

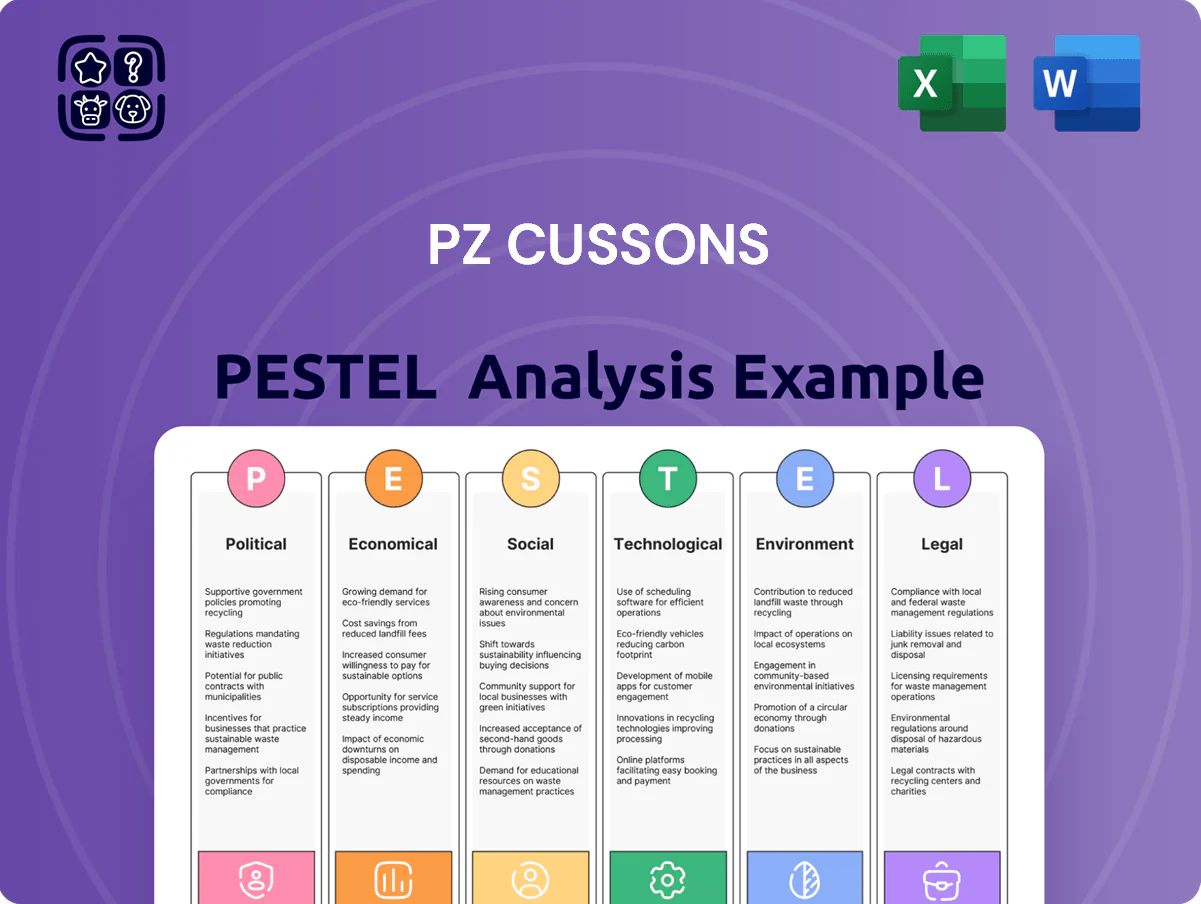

Political factors

Nigerian Regulatory Environment

The Nigerian market accounted for about 18% of PZ Cussons group revenue in FY2024, making regulatory shifts on FX access and profit repatriation material; recent Central Bank FX reforms in 2024 reduced Naira volatility but limited official FX availability, delaying remittances and squeezing margins. Analysts flag that restrictive repatriation policies could cut repatriated profits by an estimated 10–15% annually, raising country risk and operational costs.

Post-Brexit Trade Dynamics

Post-Brexit trade agreements and ongoing UK-EU negotiations affect export competitiveness for UK brands like Carex; UK goods exports to the EU fell 15.8% by value in 2021 vs 2019 and remained 6% below pre-Brexit levels in 2024, increasing pressure on margins. Changes in customs checks and regulatory divergence have raised average export costs by an estimated 4–7% per shipment, impacting unit economics. Strategic planning must price in tariff scenarios and non-tariff barriers to protect gross margins on British-made products.

Geopolitical Stability in West Africa

Regional stability across West African nations affects PZ Cussons supply-chain security and distributor safety; UN OCHA reported 2024 conflict incidents up 12% in the Sahel, increasing transport delays and insurance costs by an estimated 8–10% for FMCG operators.

Political unrest or sudden administration changes cause localized market disruptions that reduce consumer access to essentials—NielsenIQ noted 2024 FMCG out-of-stock spikes of 6–9% in affected West African markets.

PZ Cussons maintains a diversified presence across Nigeria, Ghana and other regional markets, reducing revenue concentration risk; in 2024 West Africa represented roughly 18% of group revenue, helping absorb shocks from nation-specific volatility.

Global Trade Tariffs and Protectionism

The rise of protectionist policies has pushed average global tariffs on consumer goods up; WTO data showed ad-valorem tariffs for manufactured products rose to about 5.8% in 2024, increasing input costs for PZ Cussons and pressuring 2024 gross margins (reported group gross margin 34.1%).

These shifts force reassessment of manufacturing footprint and sourcing—relocating production or nearshoring reduces exposure but may raise capital expenditure and unit costs.

Continuous monitoring of trade relations between the UK, EU, US and major suppliers (China, Turkey, Nigeria) through 2025 is essential to maintain a cost-effective supply chain and protect EBITDA margins.

- Tariff rise: manufactured goods avg 5.8% (WTO 2024)

- PZ Cussons 2024 gross margin: 34.1%

- Risk mitigation: nearshoring/relocation increases capex

- Focus: UK–EU–US–China trade relations through 2025

Government Health and Hygiene Initiatives

Government-led hygiene campaigns boost demand for personal care products; WHO/UNICEF reported global handwashing initiatives reached 2.3 billion people in 2023, supporting sales growth for hygiene brands.

In Indonesia and Nigeria, public–private programs (e.g., Indonesia's 2024 national sanitation plan, Nigeria's 2023 school handwashing rollouts) create distribution and awareness tailwinds for Carex and Cussons Baby.

Aligning CSR with these priorities improved local trust and market access; PZ Cussons' regional CSR spend of ~£12m in 2023–24 helped expand outreach and shelf presence.

- 2.3bn people reached by handwashing initiatives (WHO/UNICEF 2023)

- Indonesia 2024 sanitation plan and Nigeria 2023 school programs

- PZ Cussons regional CSR ~£12m (2023–24) aiding market penetration

2024 Political Risks Hit PZ Cussons: FX Limits, Tariffs & Rising Logistics Compress Margins

Political risks in 2024 concentrated on FX/repatriation limits in Nigeria (c.18% group revenue), UK–EU post-Brexit trade frictions raising export costs ~4–7%, rising regional conflict increasing logistics/insurance costs ~8–10%, and protectionist tariffs averaging 5.8% (WTO 2024) squeezing group gross margin of 34.1%; government hygiene campaigns (2.3bn reached) provide demand support.

| Metric | 2023–24 / 2024 |

|---|---|

| Nigeria revenue share | ~18% |

| UK export cost rise | 4–7% |

| Logistics/insurance rise (Sahel) | 8–10% |

| Avg tariffs (WTO) | 5.8% |

| PZ Cussons gross margin | 34.1% |

| Handwashing reach (WHO/UNICEF) | 2.3bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect PZ Cussons across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to inform strategy and risk management.

A concise, PESTLE-segmented summary of PZ Cussons that’s instantly shareable and presentation-ready, helping teams quickly align on external risks, market drivers, and regulatory impacts during planning or client engagements.

Economic factors

Currency Volatility and Exchange Rate Risk

The devaluation of the Nigerian Naira, which fell about 40% vs the pound between 2020–2024, has materially pressured PZ Cussons’ reported profits as naira-denominated earnings translate into fewer British Pounds. Exchange-rate swings also raise import costs for raw materials, contributing to margin compression—Nigeria accounts for roughly 20–25% of group revenue in recent years. Financial teams increasingly deploy forwards, options and natural hedges; in 2024 management cited active currency hedging to stabilize FX impact on earnings per share.

Inflationary Pressures on Consumer Spending

High inflation in core markets—UK CPI at 4.0% in 2025 Q4 and several African economies above 8–12%—is squeezing household budgets, cutting discretionary spend and slowing FMCG growth.

Consumers are trading down to value brands or reducing purchase frequency; Kantar reported private-label penetration rising 2–4ppt in 2024 in key PZ Cussons markets.

PZ Cussons faces rising input costs (commodities, packaging) and must weigh price hikes against losing price-sensitive customers, balancing margin protection with volume retention.

Commodity Price Fluctuations

Commodity price volatility for inputs like palm oil, tallow and plastic resins hits PZ Cussons' margins directly; palm oil averaged about $850/tonne in 2024, up ~12% year-on-year, while global resin prices rose ~8% in H1 2025, pressuring COGS. Price spikes can cut gross margins within quarters—PZ Cussons reported a 150–200bps margin swing from commodity movements in FY2024. The group leans on strategic sourcing, volume contracts and hedging; long-term supplier agreements covered roughly 40% of key commodity volumes in 2024 to stabilize costs.

Emerging Market Growth Potential

Rapid urbanization in Asia and Africa—urban populations growing ~2% annually and projected to add 1.4 billion people by 2050—fuels demand for consumer goods; middle-class households in emerging markets rose to ~3.8 billion globally by 2025, increasing branded personal care spend.

PZ Cussons’ established footprint in Nigeria, Indonesia and other high-growth markets positions it to capture rising disposable incomes—consumer beauty and personal care segments grew ~6–8% CAGR in sub-Saharan Africa and Southeast Asia in 2023–25.

- Urbanization +1.4B by 2050

- Middle class ~3.8B (2025)

- P&C growth ~6–8% CAGR (2023–25)

- Strong presence: Nigeria, Indonesia

Interest Rate Environments and Debt Servicing

Global central bank tightening since 2022 has pushed benchmark rates: US Fed funds ~5.25–5.50% (2024), ECB ~3.75% and Bank of England ~5.25%, raising corporate borrowing costs and reducing feasibility of large capex for firms like PZ Cussons.

Higher rates lift debt-servicing costs—PZ Cussons held net debt ~£282m at H1 FY25—raising its weighted average cost of capital and hurdle rates for new projects.

Management must enforce strict capital allocation, prioritising low-return divestments and cash flow resilience to preserve liquidity during prolonged restrictive policy.

- Central bank rates up → higher borrowing costs

- PZ Cussons net debt ~£282m (H1 FY25)

- Higher hurdle rates reduce capex feasibility

- Discipline in capital allocation and cash preservation essential

Inflation, FX hit margins: Nigeria exposure, rising costs and tighter balance sheet

Naira devaluation (~40% vs GBP 2020–24) and active hedging; Nigeria ~20–25% revenue. Inflation high (UK CPI 4.0% Q4 2025; key African markets 8–12%), driving downtrading; private-label +2–4ppt (2024). Commodity pressure: palm oil ~$850/t (2024), resin +8% H1 2025; FY24 margin swing 150–200bps. Net debt ~£282m (H1 FY25); higher rates raise WACC, capex discipline needed.

| Metric | Value |

|---|---|

| Nigeria revenue share | 20–25% |

| Naira fall vs GBP (2020–24) | ~40% |

| Palm oil (2024) | $850/t |

| Private-label shift (2024) | +2–4ppt |

| Net debt (H1 FY25) | £282m |

Full Version Awaits

PZ Cussons PESTLE Analysis

The preview shown here is the exact PZ Cussons PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

This real screenshot reflects the final file delivered upon payment, with complete content and no placeholders or surprises.

The layout, analysis, and structure you see are exactly what you’ll be able to download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and evolving consumer trends are shaping PZ Cussons’ strategic outlook—our concise PESTLE highlights risks and opportunities you can act on. Purchase the full analysis for a complete, editable report packed with data-driven insights ideal for investors, consultants, and strategy teams. Download now to make smarter, faster decisions.

Political factors

Nigerian Regulatory Environment

The Nigerian market accounted for about 18% of PZ Cussons group revenue in FY2024, making regulatory shifts on FX access and profit repatriation material; recent Central Bank FX reforms in 2024 reduced Naira volatility but limited official FX availability, delaying remittances and squeezing margins. Analysts flag that restrictive repatriation policies could cut repatriated profits by an estimated 10–15% annually, raising country risk and operational costs.

Post-Brexit Trade Dynamics

Post-Brexit trade agreements and ongoing UK-EU negotiations affect export competitiveness for UK brands like Carex; UK goods exports to the EU fell 15.8% by value in 2021 vs 2019 and remained 6% below pre-Brexit levels in 2024, increasing pressure on margins. Changes in customs checks and regulatory divergence have raised average export costs by an estimated 4–7% per shipment, impacting unit economics. Strategic planning must price in tariff scenarios and non-tariff barriers to protect gross margins on British-made products.

Geopolitical Stability in West Africa

Regional stability across West African nations affects PZ Cussons supply-chain security and distributor safety; UN OCHA reported 2024 conflict incidents up 12% in the Sahel, increasing transport delays and insurance costs by an estimated 8–10% for FMCG operators.

Political unrest or sudden administration changes cause localized market disruptions that reduce consumer access to essentials—NielsenIQ noted 2024 FMCG out-of-stock spikes of 6–9% in affected West African markets.

PZ Cussons maintains a diversified presence across Nigeria, Ghana and other regional markets, reducing revenue concentration risk; in 2024 West Africa represented roughly 18% of group revenue, helping absorb shocks from nation-specific volatility.

Global Trade Tariffs and Protectionism

The rise of protectionist policies has pushed average global tariffs on consumer goods up; WTO data showed ad-valorem tariffs for manufactured products rose to about 5.8% in 2024, increasing input costs for PZ Cussons and pressuring 2024 gross margins (reported group gross margin 34.1%).

These shifts force reassessment of manufacturing footprint and sourcing—relocating production or nearshoring reduces exposure but may raise capital expenditure and unit costs.

Continuous monitoring of trade relations between the UK, EU, US and major suppliers (China, Turkey, Nigeria) through 2025 is essential to maintain a cost-effective supply chain and protect EBITDA margins.

- Tariff rise: manufactured goods avg 5.8% (WTO 2024)

- PZ Cussons 2024 gross margin: 34.1%

- Risk mitigation: nearshoring/relocation increases capex

- Focus: UK–EU–US–China trade relations through 2025

Government Health and Hygiene Initiatives

Government-led hygiene campaigns boost demand for personal care products; WHO/UNICEF reported global handwashing initiatives reached 2.3 billion people in 2023, supporting sales growth for hygiene brands.

In Indonesia and Nigeria, public–private programs (e.g., Indonesia's 2024 national sanitation plan, Nigeria's 2023 school handwashing rollouts) create distribution and awareness tailwinds for Carex and Cussons Baby.

Aligning CSR with these priorities improved local trust and market access; PZ Cussons' regional CSR spend of ~£12m in 2023–24 helped expand outreach and shelf presence.

- 2.3bn people reached by handwashing initiatives (WHO/UNICEF 2023)

- Indonesia 2024 sanitation plan and Nigeria 2023 school programs

- PZ Cussons regional CSR ~£12m (2023–24) aiding market penetration

2024 Political Risks Hit PZ Cussons: FX Limits, Tariffs & Rising Logistics Compress Margins

Political risks in 2024 concentrated on FX/repatriation limits in Nigeria (c.18% group revenue), UK–EU post-Brexit trade frictions raising export costs ~4–7%, rising regional conflict increasing logistics/insurance costs ~8–10%, and protectionist tariffs averaging 5.8% (WTO 2024) squeezing group gross margin of 34.1%; government hygiene campaigns (2.3bn reached) provide demand support.

| Metric | 2023–24 / 2024 |

|---|---|

| Nigeria revenue share | ~18% |

| UK export cost rise | 4–7% |

| Logistics/insurance rise (Sahel) | 8–10% |

| Avg tariffs (WTO) | 5.8% |

| PZ Cussons gross margin | 34.1% |

| Handwashing reach (WHO/UNICEF) | 2.3bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect PZ Cussons across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to inform strategy and risk management.

A concise, PESTLE-segmented summary of PZ Cussons that’s instantly shareable and presentation-ready, helping teams quickly align on external risks, market drivers, and regulatory impacts during planning or client engagements.

Economic factors

Currency Volatility and Exchange Rate Risk

The devaluation of the Nigerian Naira, which fell about 40% vs the pound between 2020–2024, has materially pressured PZ Cussons’ reported profits as naira-denominated earnings translate into fewer British Pounds. Exchange-rate swings also raise import costs for raw materials, contributing to margin compression—Nigeria accounts for roughly 20–25% of group revenue in recent years. Financial teams increasingly deploy forwards, options and natural hedges; in 2024 management cited active currency hedging to stabilize FX impact on earnings per share.

Inflationary Pressures on Consumer Spending

High inflation in core markets—UK CPI at 4.0% in 2025 Q4 and several African economies above 8–12%—is squeezing household budgets, cutting discretionary spend and slowing FMCG growth.

Consumers are trading down to value brands or reducing purchase frequency; Kantar reported private-label penetration rising 2–4ppt in 2024 in key PZ Cussons markets.

PZ Cussons faces rising input costs (commodities, packaging) and must weigh price hikes against losing price-sensitive customers, balancing margin protection with volume retention.

Commodity Price Fluctuations

Commodity price volatility for inputs like palm oil, tallow and plastic resins hits PZ Cussons' margins directly; palm oil averaged about $850/tonne in 2024, up ~12% year-on-year, while global resin prices rose ~8% in H1 2025, pressuring COGS. Price spikes can cut gross margins within quarters—PZ Cussons reported a 150–200bps margin swing from commodity movements in FY2024. The group leans on strategic sourcing, volume contracts and hedging; long-term supplier agreements covered roughly 40% of key commodity volumes in 2024 to stabilize costs.

Emerging Market Growth Potential

Rapid urbanization in Asia and Africa—urban populations growing ~2% annually and projected to add 1.4 billion people by 2050—fuels demand for consumer goods; middle-class households in emerging markets rose to ~3.8 billion globally by 2025, increasing branded personal care spend.

PZ Cussons’ established footprint in Nigeria, Indonesia and other high-growth markets positions it to capture rising disposable incomes—consumer beauty and personal care segments grew ~6–8% CAGR in sub-Saharan Africa and Southeast Asia in 2023–25.

- Urbanization +1.4B by 2050

- Middle class ~3.8B (2025)

- P&C growth ~6–8% CAGR (2023–25)

- Strong presence: Nigeria, Indonesia

Interest Rate Environments and Debt Servicing

Global central bank tightening since 2022 has pushed benchmark rates: US Fed funds ~5.25–5.50% (2024), ECB ~3.75% and Bank of England ~5.25%, raising corporate borrowing costs and reducing feasibility of large capex for firms like PZ Cussons.

Higher rates lift debt-servicing costs—PZ Cussons held net debt ~£282m at H1 FY25—raising its weighted average cost of capital and hurdle rates for new projects.

Management must enforce strict capital allocation, prioritising low-return divestments and cash flow resilience to preserve liquidity during prolonged restrictive policy.

- Central bank rates up → higher borrowing costs

- PZ Cussons net debt ~£282m (H1 FY25)

- Higher hurdle rates reduce capex feasibility

- Discipline in capital allocation and cash preservation essential

Inflation, FX hit margins: Nigeria exposure, rising costs and tighter balance sheet

Naira devaluation (~40% vs GBP 2020–24) and active hedging; Nigeria ~20–25% revenue. Inflation high (UK CPI 4.0% Q4 2025; key African markets 8–12%), driving downtrading; private-label +2–4ppt (2024). Commodity pressure: palm oil ~$850/t (2024), resin +8% H1 2025; FY24 margin swing 150–200bps. Net debt ~£282m (H1 FY25); higher rates raise WACC, capex discipline needed.

| Metric | Value |

|---|---|

| Nigeria revenue share | 20–25% |

| Naira fall vs GBP (2020–24) | ~40% |

| Palm oil (2024) | $850/t |

| Private-label shift (2024) | +2–4ppt |

| Net debt (H1 FY25) | £282m |

Full Version Awaits

PZ Cussons PESTLE Analysis

The preview shown here is the exact PZ Cussons PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

This real screenshot reflects the final file delivered upon payment, with complete content and no placeholders or surprises.

The layout, analysis, and structure you see are exactly what you’ll be able to download immediately after checkout.