Grupa PZU Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Grupa PZU faces moderate buyer power and concentrated competition, while regulatory scrutiny and capital-intensive scale limit new entrants—yet strong brand and distribution give it defensive advantages; supplier leverage and substitute threats remain manageable but evolving.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupa PZU’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Human Capital and Specialized Labor

The concentration of actuaries, data scientists, and IT specialists gives suppliers of human capital high bargaining power in 2025, with median CEE data scientist salaries up ~18% above 2021 levels and top actuarial hires commanding €70–120k annual packages. Grupa PZU must match regional tech salaries and stock/bonus incentives to retain talent, raising HR costs by an estimated 6–9% of tech operating spend. This labor constraint is a key driver of operating efficiency and risk-modeling capacity.

Dependence on Healthcare Service Providers

PZU Zdrowie is a major purchaser of medical services, buying services for over 1.2m insured lives in 2024, yet depends on private clinics and scarce specialists, which limits bargaining leverage.

PZU’s scale secures volume discounts—PZU Group bought medical services worth ~PLN 1.8bn in 2024—but rising equipment costs (global medical device inflation ~6% in 2023–24) and wage growth (Polish healthcare salaries up ~8% in 2024) strengthen suppliers’ bargaining power.

That supplier pressure compresses margins: PZU Zdrowie reported a health segment margin decline of ~90 bps in 2024, reflecting higher unit costs and constrained price pass-through.

Reinsurance Market Volatility

Global reinsurers supply critical risk capacity and, after 2023–25 climate losses (insured losses ~USD 210bn in 2023 and 2024 combined), have tightened capacity, raising catastrophe reinsurance rates by ~25–40% in 2025; this hard market gives reinsurers pricing power over PZU for peak perils.

PZU’s 2024 combined ratio was ~96%; with 2025 reinsurance cost inflation, PZU must either absorb higher ceding costs—hitting underwriting margin—or pass ~€50–€120m extra premiums to customers, affecting retention and pricing competitiveness.

Technology and Cloud Infrastructure Providers

- High lock-in: migration >20–30% of annual cloud spend

- 2024 IT spend: ~€120m at PZU

- Supplier price pressure: 10–15% annual fee rises (2023–24)

- Dependence for AI-driven distribution and analytics

Financial Market Intermediaries and Asset Managers

PZU, as Poland’s largest insurer with about PLN 234 billion assets under management (AUM) at end-2024, leverages scale when negotiating with global investment banks and specialist fund managers, but still depends on their niche expertise for ESG-compliant and alternative assets.

These financial intermediaries set fees, reporting terms, and access to private markets; a 50–150 bps fee range on alternatives can cut net portfolio returns materially, so supplier bargaining power remains medium-high.

- PLN 234bn AUM (2024)

- ESG/alternatives need niche managers

- Fees 50–150 bps impact net returns

- Scale helps, but expertise drives influence

Rising supplier costs squeeze margins: HR, reinsurers, medicals and cloud drive higher fees

Suppliers exert medium-high power: talent shortages raise tech/actuarial HR costs ~6–9% of tech spend; medical providers limit PZU Zdrowie’s leverage despite PLN 1.8bn bought (2024); reinsurers hiked catastrophe rates ~25–40% (2025) adding €50–€120m ceding cost; cloud/AI lock-in risks +10–15% fee rises after €120m IT spend (2024); AUM PLN 234bn (2024) limits but does not remove manager fee pressure.

| Metric | Value |

|---|---|

| Tech HR uplift | +6–9% of tech opex |

| PZU medical spend | PLN 1.8bn (2024) |

| Reinsurance rate rise | +25–40% (2025) |

| Extra ceding cost | €50–€120m |

| IT spend | €120m (2024) |

| AUM | PLN 234bn (2024) |

What is included in the product

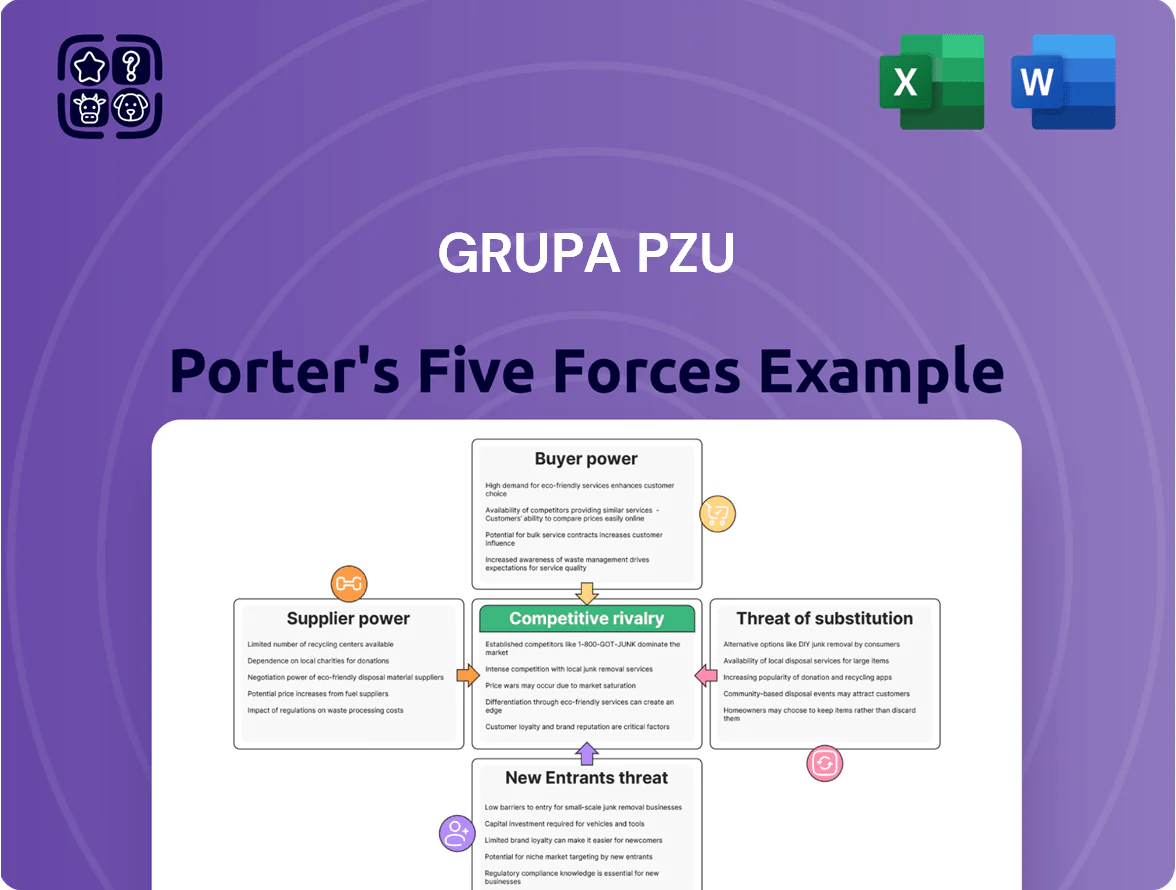

Tailored exclusively for Grupa PZU, this Porter’s Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping the insurer’s pricing power and profitability.

Clear, one-sheet Porter's Five Forces for Grupa PZU—quickly identify competitive pressures and prioritize strategic moves.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance

Individual Polish customers remain highly price-sensitive for motor TPL; 2024 KNF data shows average annual TPL premiums fell 6% y/y to ~PLN 720 as shoppers chased savings.

Price comparison sites reached ~4.2m unique users in 2025, per Gemius, letting buyers switch in minutes and eroding PZU brand loyalty.

That transparency forces PZU to keep below-market or matching rates despite rising claims costs—PZU reported combined ratio 101.3% in 2024—squeezing margins.

Consolidation of Corporate Clients

Growth of Digital-Native Consumer Expectations

Regulatory Protection of Consumer Rights

Strict EU rules and Polish regulators KNF (Polish Financial Supervision Authority) and UOKiK (Office of Competition and Consumer Protection) strengthen individual policyholders’ bargaining power vs Grupa PZU by mandating clear terms and easier complaint/switching processes; EU IDD (Insurance Distribution Directive) and 2024 KNF guidance cut obscure fees and doubled transparency requirements for policy documentation.

These rules limit PZU’s ability to add restrictive clauses or hidden charges, shifting balance toward consumers; in 2024 Poland recorded a 12% rise in insurer complaints resolved in favour of policyholders, increasing switching rates to 7.4% in retail non-life segments.

- EU IDD and 2024 KNF guidance enforce clearer terms

- UOKiK powers speed complaint resolution

- 2024: +12% favourable complaint outcomes

- 2024 retail non-life switching: 7.4%

Influence of Multi-Agency Distribution Channels

Independent agents and brokers act for customers and wield strong influence by recommending insurers; in Poland brokers handled about 28% of non-life premiums in 2024, so their channel power is material for PZU.

If PZU’s commission rates or turnaround and claims service lag, brokers can redirect large volumes to rivals—a 5 percentage-point commission gap can shift millions of PLN in annual premiums.

PZU must keep commissions competitive and invest in distributor portals and SLAs; in 2025 PZU budgeted ~PLN 120m for channel incentives and IT to retain broker flow.

- Brokers represent client choice and drive ~28% non-life premiums

- Commission gaps (≈5pp) risk premium loss

- PZU allocated ~PLN 120m in 2025 for incentives/IT

Price-sensitive customers squeeze insurers: switching, brokers & digital gaps bite margins

Customers have strong bargaining power: retail price sensitivity cut average TPL to ~PLN 720 in 2024 (-6% y/y), switching rose to 7.4% in retail non-life, and 31% cited digital gaps when churning; brokers handled ~28% of non-life premiums in 2024 and corporate clients made ~45% of corporate premium income, pressing for double-digit discounts; PZU’s 2024 combined ratio 101.3% limits rate flexibility.

| Metric | Value (Year) |

|---|---|

| Avg motor TPL premium | ~PLN 720 (2024) |

| Retail switching rate | 7.4% (2024) |

| Churn citing digital issues | 31% (2023) |

| Brokers’ share non-life | 28% (2024) |

| Corporate premium share | ~45% (2024) |

| PZU combined ratio | 101.3% (2024) |

Same Document Delivered

Grupa PZU Porter's Five Forces Analysis

This preview shows the exact Grupa PZU Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it covers competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise insights and strategic implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Grupa PZU faces moderate buyer power and concentrated competition, while regulatory scrutiny and capital-intensive scale limit new entrants—yet strong brand and distribution give it defensive advantages; supplier leverage and substitute threats remain manageable but evolving.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupa PZU’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Human Capital and Specialized Labor

The concentration of actuaries, data scientists, and IT specialists gives suppliers of human capital high bargaining power in 2025, with median CEE data scientist salaries up ~18% above 2021 levels and top actuarial hires commanding €70–120k annual packages. Grupa PZU must match regional tech salaries and stock/bonus incentives to retain talent, raising HR costs by an estimated 6–9% of tech operating spend. This labor constraint is a key driver of operating efficiency and risk-modeling capacity.

Dependence on Healthcare Service Providers

PZU Zdrowie is a major purchaser of medical services, buying services for over 1.2m insured lives in 2024, yet depends on private clinics and scarce specialists, which limits bargaining leverage.

PZU’s scale secures volume discounts—PZU Group bought medical services worth ~PLN 1.8bn in 2024—but rising equipment costs (global medical device inflation ~6% in 2023–24) and wage growth (Polish healthcare salaries up ~8% in 2024) strengthen suppliers’ bargaining power.

That supplier pressure compresses margins: PZU Zdrowie reported a health segment margin decline of ~90 bps in 2024, reflecting higher unit costs and constrained price pass-through.

Reinsurance Market Volatility

Global reinsurers supply critical risk capacity and, after 2023–25 climate losses (insured losses ~USD 210bn in 2023 and 2024 combined), have tightened capacity, raising catastrophe reinsurance rates by ~25–40% in 2025; this hard market gives reinsurers pricing power over PZU for peak perils.

PZU’s 2024 combined ratio was ~96%; with 2025 reinsurance cost inflation, PZU must either absorb higher ceding costs—hitting underwriting margin—or pass ~€50–€120m extra premiums to customers, affecting retention and pricing competitiveness.

Technology and Cloud Infrastructure Providers

- High lock-in: migration >20–30% of annual cloud spend

- 2024 IT spend: ~€120m at PZU

- Supplier price pressure: 10–15% annual fee rises (2023–24)

- Dependence for AI-driven distribution and analytics

Financial Market Intermediaries and Asset Managers

PZU, as Poland’s largest insurer with about PLN 234 billion assets under management (AUM) at end-2024, leverages scale when negotiating with global investment banks and specialist fund managers, but still depends on their niche expertise for ESG-compliant and alternative assets.

These financial intermediaries set fees, reporting terms, and access to private markets; a 50–150 bps fee range on alternatives can cut net portfolio returns materially, so supplier bargaining power remains medium-high.

- PLN 234bn AUM (2024)

- ESG/alternatives need niche managers

- Fees 50–150 bps impact net returns

- Scale helps, but expertise drives influence

Rising supplier costs squeeze margins: HR, reinsurers, medicals and cloud drive higher fees

Suppliers exert medium-high power: talent shortages raise tech/actuarial HR costs ~6–9% of tech spend; medical providers limit PZU Zdrowie’s leverage despite PLN 1.8bn bought (2024); reinsurers hiked catastrophe rates ~25–40% (2025) adding €50–€120m ceding cost; cloud/AI lock-in risks +10–15% fee rises after €120m IT spend (2024); AUM PLN 234bn (2024) limits but does not remove manager fee pressure.

| Metric | Value |

|---|---|

| Tech HR uplift | +6–9% of tech opex |

| PZU medical spend | PLN 1.8bn (2024) |

| Reinsurance rate rise | +25–40% (2025) |

| Extra ceding cost | €50–€120m |

| IT spend | €120m (2024) |

| AUM | PLN 234bn (2024) |

What is included in the product

Tailored exclusively for Grupa PZU, this Porter’s Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping the insurer’s pricing power and profitability.

Clear, one-sheet Porter's Five Forces for Grupa PZU—quickly identify competitive pressures and prioritize strategic moves.

Customers Bargaining Power

High Price Sensitivity in Retail Insurance

Individual Polish customers remain highly price-sensitive for motor TPL; 2024 KNF data shows average annual TPL premiums fell 6% y/y to ~PLN 720 as shoppers chased savings.

Price comparison sites reached ~4.2m unique users in 2025, per Gemius, letting buyers switch in minutes and eroding PZU brand loyalty.

That transparency forces PZU to keep below-market or matching rates despite rising claims costs—PZU reported combined ratio 101.3% in 2024—squeezing margins.

Consolidation of Corporate Clients

Growth of Digital-Native Consumer Expectations

Regulatory Protection of Consumer Rights

Strict EU rules and Polish regulators KNF (Polish Financial Supervision Authority) and UOKiK (Office of Competition and Consumer Protection) strengthen individual policyholders’ bargaining power vs Grupa PZU by mandating clear terms and easier complaint/switching processes; EU IDD (Insurance Distribution Directive) and 2024 KNF guidance cut obscure fees and doubled transparency requirements for policy documentation.

These rules limit PZU’s ability to add restrictive clauses or hidden charges, shifting balance toward consumers; in 2024 Poland recorded a 12% rise in insurer complaints resolved in favour of policyholders, increasing switching rates to 7.4% in retail non-life segments.

- EU IDD and 2024 KNF guidance enforce clearer terms

- UOKiK powers speed complaint resolution

- 2024: +12% favourable complaint outcomes

- 2024 retail non-life switching: 7.4%

Influence of Multi-Agency Distribution Channels

Independent agents and brokers act for customers and wield strong influence by recommending insurers; in Poland brokers handled about 28% of non-life premiums in 2024, so their channel power is material for PZU.

If PZU’s commission rates or turnaround and claims service lag, brokers can redirect large volumes to rivals—a 5 percentage-point commission gap can shift millions of PLN in annual premiums.

PZU must keep commissions competitive and invest in distributor portals and SLAs; in 2025 PZU budgeted ~PLN 120m for channel incentives and IT to retain broker flow.

- Brokers represent client choice and drive ~28% non-life premiums

- Commission gaps (≈5pp) risk premium loss

- PZU allocated ~PLN 120m in 2025 for incentives/IT

Price-sensitive customers squeeze insurers: switching, brokers & digital gaps bite margins

Customers have strong bargaining power: retail price sensitivity cut average TPL to ~PLN 720 in 2024 (-6% y/y), switching rose to 7.4% in retail non-life, and 31% cited digital gaps when churning; brokers handled ~28% of non-life premiums in 2024 and corporate clients made ~45% of corporate premium income, pressing for double-digit discounts; PZU’s 2024 combined ratio 101.3% limits rate flexibility.

| Metric | Value (Year) |

|---|---|

| Avg motor TPL premium | ~PLN 720 (2024) |

| Retail switching rate | 7.4% (2024) |

| Churn citing digital issues | 31% (2023) |

| Brokers’ share non-life | 28% (2024) |

| Corporate premium share | ~45% (2024) |

| PZU combined ratio | 101.3% (2024) |

Same Document Delivered

Grupa PZU Porter's Five Forces Analysis

This preview shows the exact Grupa PZU Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it covers competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise insights and strategic implications.