Qantas Airways Boston Consulting Group Matrix

Download Your Competitive Advantage

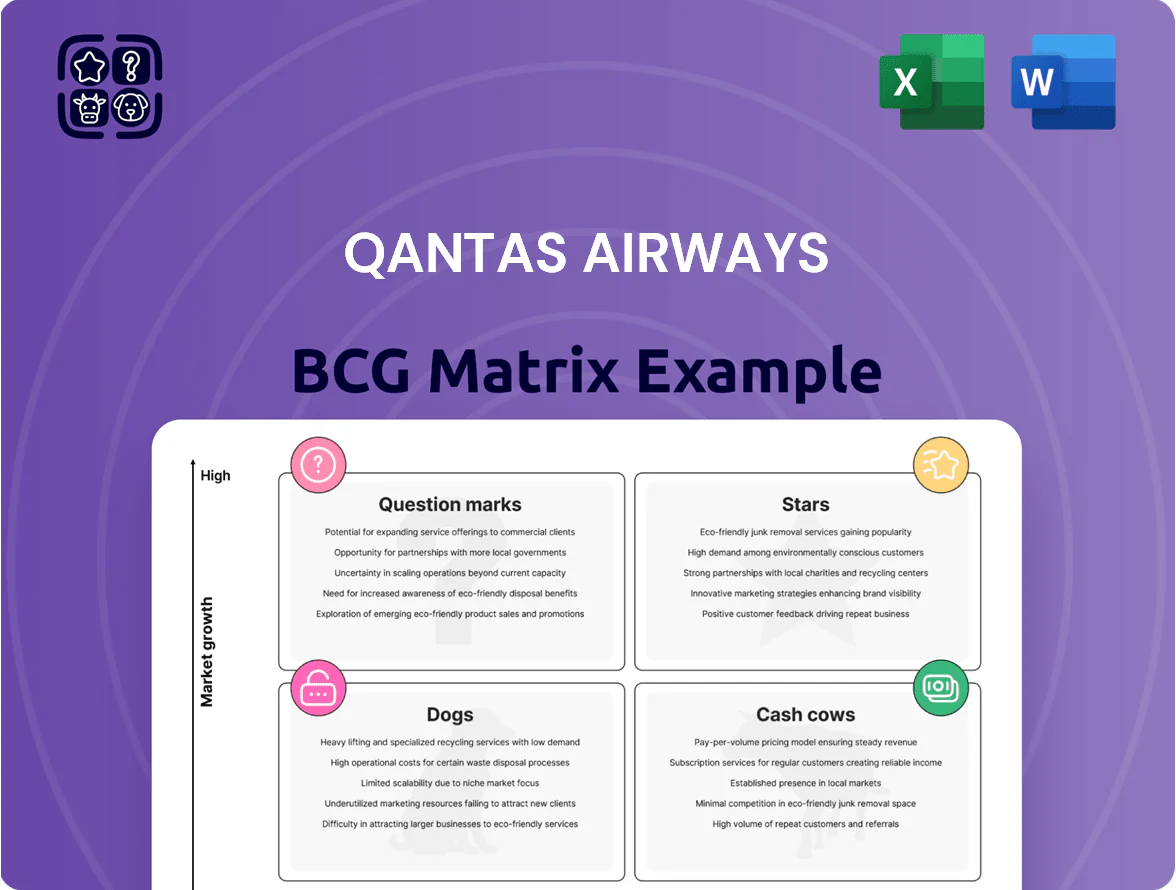

Qantas Airways sits at the intersection of legacy strength and emerging challenges—its domestic network and loyalty program act like Cash Cows while international recovery and low-cost ventures show Question Mark potential; fuel volatility and competitive LCC pressure are persistent threats. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Project Sunrise Ultra-Long-Haul Routes

Project Sunrise launches direct Sydney/Melbourne–London and –New York services with Airbus A350-1000s starting late 2025–early 2026, targeting premium non-stop travel and positioning as Stars in Qantas’s BCG matrix.

These ultra-long-haul routes require ~A$2–2.5bn fleet-related capex (10–12 A350-1000s), but Qantas expects >30% yield premium versus one-stop competitors and aiming for >40% share of premium nonstop demand on these city pairs.

Qantas Loyalty Program Expansion

Qantas Loyalty, the Stars quadrant performer, grew revenue 12% to A$1.1bn in FY2024 and now counts over 13 million active members, keeping a dominant share of Australia’s loyalty market.

It has diversified into credit cards, insurance, and retail partnerships, with non-air redemption now 55% of earnings and higher margin contribution.

Qantas is investing A$150m through 2025 in new tech and analytics platforms to boost personalization and lifetime value, supporting continued growth.

Western Sydney International Airport Operations

The new 24-hour Western Sydney International Airport, due late 2026, is a major growth lever for Qantas as it plans to be a primary anchor tenant, unlocking capacity for ~10m passengers annually in initial phases and reducing Sydney CBD congestion by ~15% per NSW Transport forecasts.

Positioning there expands Qantas’s domestic and international slots in a high-demand catchment that was previously underserved, supporting network growth and potential incremental revenue of A$200–350m annually by year 3 per industry estimates.

Qantas and partners are backing heavy infrastructure and terminal investment—over A$5bn committed across airport precinct projects—to capture emerging market share and hub-related ancillary revenues.

Sustainable Aviation Fuel (SAF) Partnerships

Qantas leads Australian decarbonization via its AUD 1.5bn Climate Fund (announced 2020) and partnerships with domestic SAF producers targeting commercial volumes by 2026; SAF demand could hit ~1.5–2% of jet fuel by 2025 and 10%+ by 2030 under policy pushes.

Regulatory mandates and corporate ESG buying drive rapid growth; Qantas’s first-mover SAF contracts improve brand premium and route decarbonization, boosting long-term yield despite near-term costs.

High capital needs for SAF blending infrastructure and feedstock procurement make this a high-consumption, high-potential Star with significant margin upside if production scales and SAF price premium narrows from ~2–5x jet fuel today.

- Qantas Climate Fund: AUD 1.5bn

- Target commercial SAF by 2026

- SAF price premium today ~2–5x

- Demand scenario: 1.5–2% (2025), 10%+ (2030)

Digital Transformation and Personalization

Qantas is scaling AI-driven customer platforms and a modern booking engine to win direct bookings; direct channel revenue rose to A$2.1bn in FY2024 (up 18% vs FY2023), showing high user growth and conversion gains.

Usage of digital assets is growing rapidly—mobile app monthly active users exceeded 3.2m in 2024—and travelers demand seamless, personalized end-to-end journeys, pushing feature rollout cadence.

Continuous software refreshes and upgraded cybersecurity keep this unit in a high-investment phase; Qantas Group capital expenditure was A$1.5bn in FY2024 with a growing share to digital and IT.

- Direct channel revenue A$2.1bn FY2024 (+18%)

- App MAU 3.2m+ (2024)

- Group capex A$1.5bn FY2024; rising IT share

- High recurring spend: software, AI, cybersecurity

Qantas: High-Capex A350s, Loyalty A$1.1bn & Direct A$2.1bn Drive Premium Growth

Stars: Project Sunrise (A350-1000s) and Loyalty/digital units demand high capex but deliver premium yields, strong growth, and market share; FY2024 Loyalty revenue A$1.1bn, direct channel A$2.1bn, group capex A$1.5bn. SAF/Climate Fund and WSI airport expand capacity and brand, with SAF price premium 2–5x and Qantas Climate Fund A$1.5bn.

| Metric | Value |

|---|---|

| Loyalty Rev FY24 | A$1.1bn |

| Direct Rev FY24 | A$2.1bn |

| Group Capex FY24 | A$1.5bn |

| Climate Fund | A$1.5bn |

What is included in the product

Comprehensive BCG analysis of Qantas units: Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance.

One-page Qantas BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

Domestic Mainline Operations

Qantas Domestic remains Australia’s market leader, holding roughly 60% domestic corporate/govt share and operating 70% of peak intra‑state frequencies (FY2024 ASX filings). This mature segment delivers steady margins—operating margin ~10% in FY2024—thanks to network density and schedule frequency. Cash flow from domestic ops funded A$4.2bn of fleet renewal capex through 2023–25 plans and supported A$300m+ in dividends in FY2024.

Jetstar Domestic Australia

Jetstar Domestic Australia, the leading low-cost carrier with ~40% domestic seat share in FY2024, generates steady cash flow by serving price-sensitive travelers and posting an estimated AUD 650–750m EBITDA contribution to Qantas Group in 2024.

With unit costs ~20–30% below Qantas Domestic full service and lower marketing spend per RPK, Jetstar needs less reinvestment, freeing capital for growth or debt reduction.

It forms a defensive moat—capturing leisure and budget segments and helping Qantas hold ~70% combined market share on key trunk routes.

Qantas Freight

Qantas Freight holds about 45% share of Australia’s air cargo market as of FY2024, using a dedicated fleet plus belly space on 85% of Qantas passenger flights to move e-commerce and perishables.

The division sits in a mature market with ~3% annual cargo volume growth and generated AUD 650m revenue and ~AUD 120m EBIT in FY2024, providing steady cash flow with low marketing spend to support group liquidity.

Frequent Flyer Points Accrual

Qantas Frequent Flyer point sales to banks and retailers are a mature, high-margin cash cow, generating roughly AU$400–450 million EBITDA annually (2024 reported segment trends) with low capital needs.

With ~10.5 million active members in 2024 and dominant card partnerships covering ~40% of Australian credit card co-branded spend, the unit needs minimal reinvestment to hold market lead and funds the group’s cash reserves.

- ~AU$400–450m EBITDA (2024 range)

- ~10.5m active members (2024)

- ~40% co-branded card spend share in Australia

- Low capex, high free cash flow

Corporate Travel Management

Qantas Corporate Travel Management holds deep, long-term contracts with Australia’s top corporates and federal/state governments, generating stable, high-margin revenue—Qantas reported AUD 1.2bn in corporate and freight revenue in FY2024, with corporate travel accounting for an estimated 30–35% of that stream.

The segment is mature and predictable across the fiscal year, showing low churn and steady yields; operating leverage and established account teams keep incremental costs low, sustaining high EBITDA margins versus retail leisure fares.

- Stable contracts with top corporates and governments

- FY2024 corporate-related revenue ~AUD 360–420m (est.)

- High margin, low churn, strong operating leverage

- Well-established account infrastructure enables efficient cash generation

Qantas FY24 cash cows: Domestic, Jetstar, Freight & FFlyr fuel strong high‑margin cashflow

Qantas cash cows (FY2024): Qantas Domestic (~60% corporate share) and Jetstar Domestic (~40% seat share) deliver steady margins and funded A$4.2bn capex; Qantas Freight (45% cargo share) and Qantas Frequent Flyer (~10.5m members) supply recurring high-margin cash; Corporate travel adds stable contracted revenue (~AUD 360–420m).

| Unit | Key 2024 metrics |

|---|---|

| Qantas Domestic | 60% corp share; OM ~10%; funded A$4.2bn capex |

| Jetstar Dom. | ~40% seat share; EBITDA A$650–750m |

| Freight | 45% share; revenue A$650m; EBIT A$120m |

| Frequent Flyer | 10.5m members; EBITDA A$400–450m |

| Corporate Travel | Revenue est. A$360–420m |

What You’re Viewing Is Included

Qantas Airways BCG Matrix

The file you're previewing is the exact Qantas Airways BCG Matrix report you'll receive after purchase—fully formatted, market-informed, and free of watermarks or demo content for immediate use in presentations or strategy sessions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Qantas Airways sits at the intersection of legacy strength and emerging challenges—its domestic network and loyalty program act like Cash Cows while international recovery and low-cost ventures show Question Mark potential; fuel volatility and competitive LCC pressure are persistent threats. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Project Sunrise Ultra-Long-Haul Routes

Project Sunrise launches direct Sydney/Melbourne–London and –New York services with Airbus A350-1000s starting late 2025–early 2026, targeting premium non-stop travel and positioning as Stars in Qantas’s BCG matrix.

These ultra-long-haul routes require ~A$2–2.5bn fleet-related capex (10–12 A350-1000s), but Qantas expects >30% yield premium versus one-stop competitors and aiming for >40% share of premium nonstop demand on these city pairs.

Qantas Loyalty Program Expansion

Qantas Loyalty, the Stars quadrant performer, grew revenue 12% to A$1.1bn in FY2024 and now counts over 13 million active members, keeping a dominant share of Australia’s loyalty market.

It has diversified into credit cards, insurance, and retail partnerships, with non-air redemption now 55% of earnings and higher margin contribution.

Qantas is investing A$150m through 2025 in new tech and analytics platforms to boost personalization and lifetime value, supporting continued growth.

Western Sydney International Airport Operations

The new 24-hour Western Sydney International Airport, due late 2026, is a major growth lever for Qantas as it plans to be a primary anchor tenant, unlocking capacity for ~10m passengers annually in initial phases and reducing Sydney CBD congestion by ~15% per NSW Transport forecasts.

Positioning there expands Qantas’s domestic and international slots in a high-demand catchment that was previously underserved, supporting network growth and potential incremental revenue of A$200–350m annually by year 3 per industry estimates.

Qantas and partners are backing heavy infrastructure and terminal investment—over A$5bn committed across airport precinct projects—to capture emerging market share and hub-related ancillary revenues.

Sustainable Aviation Fuel (SAF) Partnerships

Qantas leads Australian decarbonization via its AUD 1.5bn Climate Fund (announced 2020) and partnerships with domestic SAF producers targeting commercial volumes by 2026; SAF demand could hit ~1.5–2% of jet fuel by 2025 and 10%+ by 2030 under policy pushes.

Regulatory mandates and corporate ESG buying drive rapid growth; Qantas’s first-mover SAF contracts improve brand premium and route decarbonization, boosting long-term yield despite near-term costs.

High capital needs for SAF blending infrastructure and feedstock procurement make this a high-consumption, high-potential Star with significant margin upside if production scales and SAF price premium narrows from ~2–5x jet fuel today.

- Qantas Climate Fund: AUD 1.5bn

- Target commercial SAF by 2026

- SAF price premium today ~2–5x

- Demand scenario: 1.5–2% (2025), 10%+ (2030)

Digital Transformation and Personalization

Qantas is scaling AI-driven customer platforms and a modern booking engine to win direct bookings; direct channel revenue rose to A$2.1bn in FY2024 (up 18% vs FY2023), showing high user growth and conversion gains.

Usage of digital assets is growing rapidly—mobile app monthly active users exceeded 3.2m in 2024—and travelers demand seamless, personalized end-to-end journeys, pushing feature rollout cadence.

Continuous software refreshes and upgraded cybersecurity keep this unit in a high-investment phase; Qantas Group capital expenditure was A$1.5bn in FY2024 with a growing share to digital and IT.

- Direct channel revenue A$2.1bn FY2024 (+18%)

- App MAU 3.2m+ (2024)

- Group capex A$1.5bn FY2024; rising IT share

- High recurring spend: software, AI, cybersecurity

Qantas: High-Capex A350s, Loyalty A$1.1bn & Direct A$2.1bn Drive Premium Growth

Stars: Project Sunrise (A350-1000s) and Loyalty/digital units demand high capex but deliver premium yields, strong growth, and market share; FY2024 Loyalty revenue A$1.1bn, direct channel A$2.1bn, group capex A$1.5bn. SAF/Climate Fund and WSI airport expand capacity and brand, with SAF price premium 2–5x and Qantas Climate Fund A$1.5bn.

| Metric | Value |

|---|---|

| Loyalty Rev FY24 | A$1.1bn |

| Direct Rev FY24 | A$2.1bn |

| Group Capex FY24 | A$1.5bn |

| Climate Fund | A$1.5bn |

What is included in the product

Comprehensive BCG analysis of Qantas units: Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance.

One-page Qantas BCG Matrix placing each business unit in a quadrant for clear strategic prioritization

Cash Cows

Domestic Mainline Operations

Qantas Domestic remains Australia’s market leader, holding roughly 60% domestic corporate/govt share and operating 70% of peak intra‑state frequencies (FY2024 ASX filings). This mature segment delivers steady margins—operating margin ~10% in FY2024—thanks to network density and schedule frequency. Cash flow from domestic ops funded A$4.2bn of fleet renewal capex through 2023–25 plans and supported A$300m+ in dividends in FY2024.

Jetstar Domestic Australia

Jetstar Domestic Australia, the leading low-cost carrier with ~40% domestic seat share in FY2024, generates steady cash flow by serving price-sensitive travelers and posting an estimated AUD 650–750m EBITDA contribution to Qantas Group in 2024.

With unit costs ~20–30% below Qantas Domestic full service and lower marketing spend per RPK, Jetstar needs less reinvestment, freeing capital for growth or debt reduction.

It forms a defensive moat—capturing leisure and budget segments and helping Qantas hold ~70% combined market share on key trunk routes.

Qantas Freight

Qantas Freight holds about 45% share of Australia’s air cargo market as of FY2024, using a dedicated fleet plus belly space on 85% of Qantas passenger flights to move e-commerce and perishables.

The division sits in a mature market with ~3% annual cargo volume growth and generated AUD 650m revenue and ~AUD 120m EBIT in FY2024, providing steady cash flow with low marketing spend to support group liquidity.

Frequent Flyer Points Accrual

Qantas Frequent Flyer point sales to banks and retailers are a mature, high-margin cash cow, generating roughly AU$400–450 million EBITDA annually (2024 reported segment trends) with low capital needs.

With ~10.5 million active members in 2024 and dominant card partnerships covering ~40% of Australian credit card co-branded spend, the unit needs minimal reinvestment to hold market lead and funds the group’s cash reserves.

- ~AU$400–450m EBITDA (2024 range)

- ~10.5m active members (2024)

- ~40% co-branded card spend share in Australia

- Low capex, high free cash flow

Corporate Travel Management

Qantas Corporate Travel Management holds deep, long-term contracts with Australia’s top corporates and federal/state governments, generating stable, high-margin revenue—Qantas reported AUD 1.2bn in corporate and freight revenue in FY2024, with corporate travel accounting for an estimated 30–35% of that stream.

The segment is mature and predictable across the fiscal year, showing low churn and steady yields; operating leverage and established account teams keep incremental costs low, sustaining high EBITDA margins versus retail leisure fares.

- Stable contracts with top corporates and governments

- FY2024 corporate-related revenue ~AUD 360–420m (est.)

- High margin, low churn, strong operating leverage

- Well-established account infrastructure enables efficient cash generation

Qantas FY24 cash cows: Domestic, Jetstar, Freight & FFlyr fuel strong high‑margin cashflow

Qantas cash cows (FY2024): Qantas Domestic (~60% corporate share) and Jetstar Domestic (~40% seat share) deliver steady margins and funded A$4.2bn capex; Qantas Freight (45% cargo share) and Qantas Frequent Flyer (~10.5m members) supply recurring high-margin cash; Corporate travel adds stable contracted revenue (~AUD 360–420m).

| Unit | Key 2024 metrics |

|---|---|

| Qantas Domestic | 60% corp share; OM ~10%; funded A$4.2bn capex |

| Jetstar Dom. | ~40% seat share; EBITDA A$650–750m |

| Freight | 45% share; revenue A$650m; EBIT A$120m |

| Frequent Flyer | 10.5m members; EBITDA A$400–450m |

| Corporate Travel | Revenue est. A$360–420m |

What You’re Viewing Is Included

Qantas Airways BCG Matrix

The file you're previewing is the exact Qantas Airways BCG Matrix report you'll receive after purchase—fully formatted, market-informed, and free of watermarks or demo content for immediate use in presentations or strategy sessions.