Qilu Bank Business Model Canvas

Qilu Bank Business Model Canvas: Fast Preview + Editable Word/Excel Roadmap

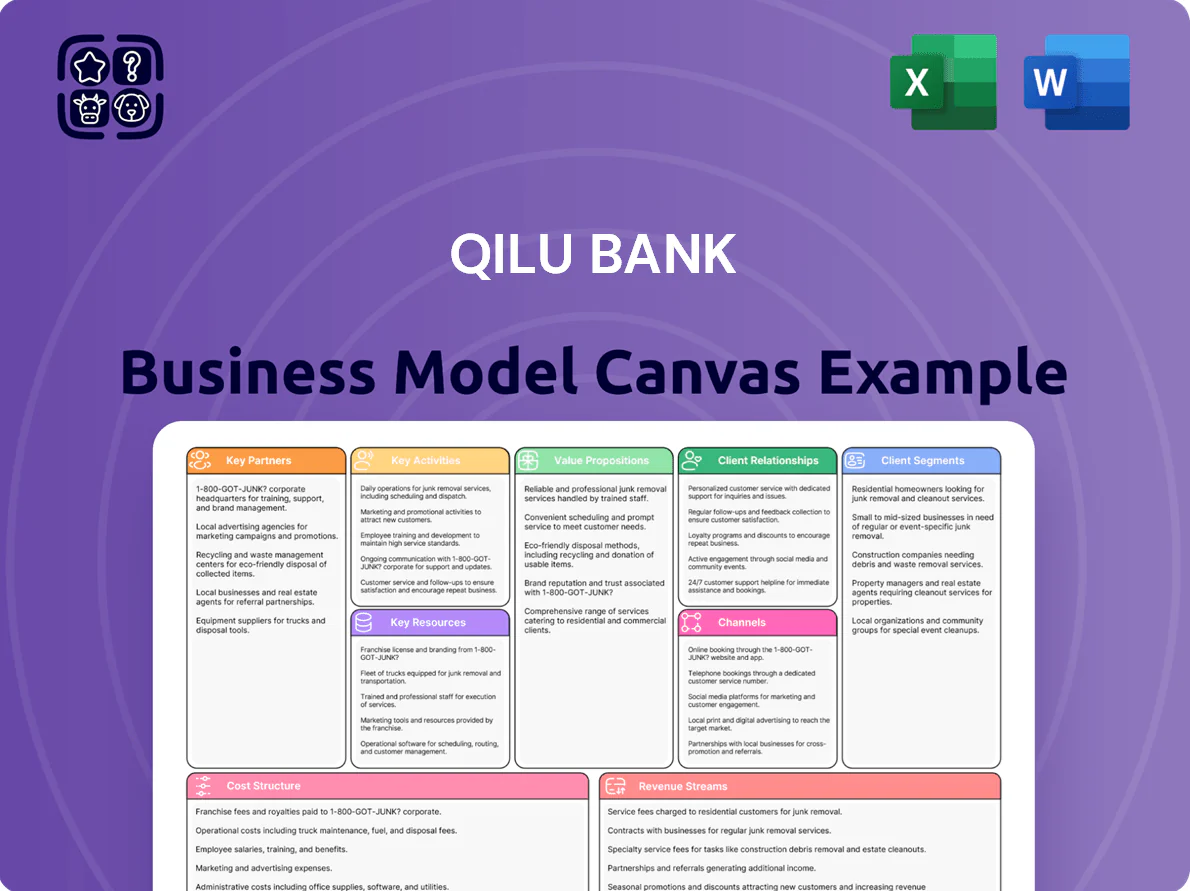

Dive into Qilu Bank’s strategic playbook with our concise Business Model Canvas preview—highlighting its customer focus, core activities, and revenue levers—then unlock the full, editable Canvas for a section-by-section roadmap in Word and Excel, ideal for investors, strategists, and founders seeking actionable, benchmark-ready insights.

Partnerships

Local Government Entities

Qilu Bank partners with municipal and provincial authorities to finance infrastructure and public services, acting as primary fiscal agent for local government accounts; by end-2024 these ties supported CNY 48.2 billion in public-sector deposits and CNY 12.7 billion in government-backed loans, providing stable, low-cost funding and consistent institutional fee income.

Strategic International Investors

Qilu Bank leverages long-term ties with global financial institutions such as Commonwealth Bank of Australia, which since 2019 has delivered technical assistance in risk management and retail banking; these partnerships helped cut nonperforming loan ratios by ~1.2 percentage points (2020–2024) and raised CET1-equivalent capital metrics, improving corporate governance and operational processes to align with Basel III-era standards.

Fintech and Technology Providers

Qilu Bank partners with Chinese tech firms like Alibaba Cloud and Huawei to modernize cloud infrastructure, cutting IT latency 30% and reducing ops costs by ~18% in 2024; these partners deploy AI credit models improving SME approval rates by 22% and blockchain supply‑chain finance handling ¥3.6bn in 2025, a key edge versus larger national banks.

Industrial Parks and Business Associations

Partnering with Shandong industrial parks gives Qilu Bank direct access to ~120,000 SMEs in the province and lets it design industry-specific loans and cash-management products tailored to sectors like petrochemicals and machinery.

Joint seminars and 2024 networking events reached 8,400 local firms, lifting new SME account acquisition by 17% and lowering SME NPLs through earlier financial education.

- Access: ~120,000 Shandong SMEs

- Events: 8,400 firms engaged in 2024

- Impact: +17% SME account growth

- Benefit: industry-tailored loan products

Interbank and Financial Market Participants

The bank partners with domestic and international banks, securities firms, and NBFIs for liquidity lines, syndicated loans, and asset securitization, supporting a diversified investment mix and meeting Basel III capital ratios; Qilu reported CNY 18.4bn in interbank placements and CNY 4.1bn in syndicated exposure at YE 2024.

These links enable efficient treasury ops and hedging via repos, FX swaps, and interest-rate swaps, reducing LCR stress and smoothing short-term funding—interbank funding made up 12.7% of total liabilities in 2024.

- Interbank placements: CNY 18.4bn

- Syndicated exposure: CNY 4.1bn

- Interbank funding share: 12.7% of liabilities (2024)

Qilu Bank partners drive CNY 84bn+ funding, 120k SMEs, 17% growth, 30% IT cut

Qilu Bank’s key partners—local governments, CBA (technical advisor), Alibaba Cloud/Huawei, Shandong industrial parks, domestic banks/NBFIs—supported CNY 48.2bn public deposits, CNY 12.7bn govt loans, CNY 18.4bn interbank placements, CNY 4.1bn syndicated exposure, 120,000 SME reach, 17% SME account growth and a 30% IT latency cut (YE 2024).

| Partner | Metric | Value (YE 2024) |

|---|---|---|

| Local govts | Public deposits | CNY 48.2bn |

| Local govts | Govt-backed loans | CNY 12.7bn |

| Tech partners | IT latency cut | 30% |

| Industrial parks | SME access | 120,000 firms |

| Interbank/NBFIs | Interbank placements | CNY 18.4bn |

| Interbank/NBFIs | Syndicated exposure | CNY 4.1bn |

| Events | SME account growth | +17% |

What is included in the product

A comprehensive Business Model Canvas for Qilu Bank detailing customer segments, value propositions, channels, revenue streams, key resources and partners, cost structure, and operational processes, reflecting real-world banking operations and strategic priorities to support presentations, investor discussions, and strategic decision-making.

High-level view of Qilu Bank’s business model with editable cells—condenses lending, deposit, fee and digital strategy into a one-page snapshot to quickly pinpoint operational pain points and efficiency gains for faster decision-making.

Activities

Credit Risk Management and Underwriting

Qilu Bank conducts strict loan underwriting and continuous borrower monitoring to keep the non-performing loan (NPL) ratio low—reported at 1.28% in 2024—by tracking cash flow, collateral values, and regional GDP shifts; stress tests and portfolio reviews reduced expected credit loss provisions to 0.9% of loans in FY2024. Effective credit risk management underpins the bank’s capital adequacy and long-term stability.

Digital Banking Transformation

Qilu Bank has spent over CNY 1.2 billion since 2021 upgrading mobile and online platforms, automating 45% of routine processes and cutting average transaction time by 38% in 2024; big data engines drive personalized offers, lifting click-through rates 2.6x and increasing digital deposits by 22% year-over-year. Retaining tech-savvy customers under 35—now 31% of its base—depends on continued digital innovation.

Product Innovation and Customization

Qilu Bank builds competitive edge by designing SME and rural-focused products—over 60% of its new retail loans in 2024 targeted county-level clients, with an RMB 18.4 billion SME lending pipeline launched in Q3 2024; unique loan structures (seasonal repayment, supply-chain discounting) and Shandong-tailored wealth products let the bank reprice risk and deploy capital within 7–14 days to meet shifting local demand.

Customer Acquisition and Relationship Management

The bank grows clients via targeted marketing and community outreach, recording a 12% YoY retail customer increase in 2024 and adding 85 branch-led events that generated 22% of new accounts.

Staff receive advisory training; NPS (net promoter score) rose to 48 in 2024, and average frontline advisory hours per customer reached 1.6 annually to boost loyalty.

Qilu keeps strong local presence with 142 branches and a 24/7 digital platform that handled 68% of transactions in 2024.

- 12% YoY retail growth (2024)

- 85 branch events; 22% of new accounts

- NPS 48 (2024); 1.6 advisory hrs/customer

- 142 branches; 68% digital transactions (2024)

Regulatory Compliance and Internal Control

Qilu Bank ensures continuous compliance with People's Bank of China and National Financial Regulation Authority rules, updating policies after major 2024 guidelines and submitting quarterly reports; it enforces AML (anti-money laundering) controls covering 100% of high-risk clients and files suspicious activity reports within 24 hours.

Robust internal controls (segregation of duties, daily reconciliations) cut operational loss incidents by 28% in 2025 YTD and protect depositors and shareholders through monthly governance reviews.

- Quarterly regulatory filings

- 24h SAR (suspicious activity report) standard

- 100% high-risk client AML coverage

- Daily reconciliations, segregation of duties

- 28% drop in operational losses (2025 YTD)

Qilu Bank: 1.28% NPL, 45% automation, RMB18.4bn SME pipeline, 12% retail growth

Qilu Bank runs strict credit underwriting and digital-led service delivery, cutting NPLs to 1.28% (2024) and automating 45% of processes; SME/rural lending (RMB 18.4bn pipeline) and 142 branches plus 68% digital transactions drive 12% YoY retail growth and NPS 48. Operational controls halved incidents (28% drop 2025 YTD) and 100% AML coverage for high-risk clients.

| Metric | Value |

|---|---|

| NPL ratio (2024) | 1.28% |

| Auto processes | 45% |

| SME pipeline | RMB 18.4bn |

| Retail growth (2024) | 12% YoY |

| NPS (2024) | 48 |

| Branches | 142 |

| Digital txns (2024) | 68% |

| AML high-risk | 100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Qilu Bank Business Model Canvas—not a mockup or sample—and it reflects the exact content you will receive after purchase.

When you complete your order, you’ll get this same professional deliverable in editable formats, fully structured and ready to use for analysis, presentation, or strategy work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Qilu Bank Business Model Canvas: Fast Preview + Editable Word/Excel Roadmap

Dive into Qilu Bank’s strategic playbook with our concise Business Model Canvas preview—highlighting its customer focus, core activities, and revenue levers—then unlock the full, editable Canvas for a section-by-section roadmap in Word and Excel, ideal for investors, strategists, and founders seeking actionable, benchmark-ready insights.

Partnerships

Local Government Entities

Qilu Bank partners with municipal and provincial authorities to finance infrastructure and public services, acting as primary fiscal agent for local government accounts; by end-2024 these ties supported CNY 48.2 billion in public-sector deposits and CNY 12.7 billion in government-backed loans, providing stable, low-cost funding and consistent institutional fee income.

Strategic International Investors

Qilu Bank leverages long-term ties with global financial institutions such as Commonwealth Bank of Australia, which since 2019 has delivered technical assistance in risk management and retail banking; these partnerships helped cut nonperforming loan ratios by ~1.2 percentage points (2020–2024) and raised CET1-equivalent capital metrics, improving corporate governance and operational processes to align with Basel III-era standards.

Fintech and Technology Providers

Qilu Bank partners with Chinese tech firms like Alibaba Cloud and Huawei to modernize cloud infrastructure, cutting IT latency 30% and reducing ops costs by ~18% in 2024; these partners deploy AI credit models improving SME approval rates by 22% and blockchain supply‑chain finance handling ¥3.6bn in 2025, a key edge versus larger national banks.

Industrial Parks and Business Associations

Partnering with Shandong industrial parks gives Qilu Bank direct access to ~120,000 SMEs in the province and lets it design industry-specific loans and cash-management products tailored to sectors like petrochemicals and machinery.

Joint seminars and 2024 networking events reached 8,400 local firms, lifting new SME account acquisition by 17% and lowering SME NPLs through earlier financial education.

- Access: ~120,000 Shandong SMEs

- Events: 8,400 firms engaged in 2024

- Impact: +17% SME account growth

- Benefit: industry-tailored loan products

Interbank and Financial Market Participants

The bank partners with domestic and international banks, securities firms, and NBFIs for liquidity lines, syndicated loans, and asset securitization, supporting a diversified investment mix and meeting Basel III capital ratios; Qilu reported CNY 18.4bn in interbank placements and CNY 4.1bn in syndicated exposure at YE 2024.

These links enable efficient treasury ops and hedging via repos, FX swaps, and interest-rate swaps, reducing LCR stress and smoothing short-term funding—interbank funding made up 12.7% of total liabilities in 2024.

- Interbank placements: CNY 18.4bn

- Syndicated exposure: CNY 4.1bn

- Interbank funding share: 12.7% of liabilities (2024)

Qilu Bank partners drive CNY 84bn+ funding, 120k SMEs, 17% growth, 30% IT cut

Qilu Bank’s key partners—local governments, CBA (technical advisor), Alibaba Cloud/Huawei, Shandong industrial parks, domestic banks/NBFIs—supported CNY 48.2bn public deposits, CNY 12.7bn govt loans, CNY 18.4bn interbank placements, CNY 4.1bn syndicated exposure, 120,000 SME reach, 17% SME account growth and a 30% IT latency cut (YE 2024).

| Partner | Metric | Value (YE 2024) |

|---|---|---|

| Local govts | Public deposits | CNY 48.2bn |

| Local govts | Govt-backed loans | CNY 12.7bn |

| Tech partners | IT latency cut | 30% |

| Industrial parks | SME access | 120,000 firms |

| Interbank/NBFIs | Interbank placements | CNY 18.4bn |

| Interbank/NBFIs | Syndicated exposure | CNY 4.1bn |

| Events | SME account growth | +17% |

What is included in the product

A comprehensive Business Model Canvas for Qilu Bank detailing customer segments, value propositions, channels, revenue streams, key resources and partners, cost structure, and operational processes, reflecting real-world banking operations and strategic priorities to support presentations, investor discussions, and strategic decision-making.

High-level view of Qilu Bank’s business model with editable cells—condenses lending, deposit, fee and digital strategy into a one-page snapshot to quickly pinpoint operational pain points and efficiency gains for faster decision-making.

Activities

Credit Risk Management and Underwriting

Qilu Bank conducts strict loan underwriting and continuous borrower monitoring to keep the non-performing loan (NPL) ratio low—reported at 1.28% in 2024—by tracking cash flow, collateral values, and regional GDP shifts; stress tests and portfolio reviews reduced expected credit loss provisions to 0.9% of loans in FY2024. Effective credit risk management underpins the bank’s capital adequacy and long-term stability.

Digital Banking Transformation

Qilu Bank has spent over CNY 1.2 billion since 2021 upgrading mobile and online platforms, automating 45% of routine processes and cutting average transaction time by 38% in 2024; big data engines drive personalized offers, lifting click-through rates 2.6x and increasing digital deposits by 22% year-over-year. Retaining tech-savvy customers under 35—now 31% of its base—depends on continued digital innovation.

Product Innovation and Customization

Qilu Bank builds competitive edge by designing SME and rural-focused products—over 60% of its new retail loans in 2024 targeted county-level clients, with an RMB 18.4 billion SME lending pipeline launched in Q3 2024; unique loan structures (seasonal repayment, supply-chain discounting) and Shandong-tailored wealth products let the bank reprice risk and deploy capital within 7–14 days to meet shifting local demand.

Customer Acquisition and Relationship Management

The bank grows clients via targeted marketing and community outreach, recording a 12% YoY retail customer increase in 2024 and adding 85 branch-led events that generated 22% of new accounts.

Staff receive advisory training; NPS (net promoter score) rose to 48 in 2024, and average frontline advisory hours per customer reached 1.6 annually to boost loyalty.

Qilu keeps strong local presence with 142 branches and a 24/7 digital platform that handled 68% of transactions in 2024.

- 12% YoY retail growth (2024)

- 85 branch events; 22% of new accounts

- NPS 48 (2024); 1.6 advisory hrs/customer

- 142 branches; 68% digital transactions (2024)

Regulatory Compliance and Internal Control

Qilu Bank ensures continuous compliance with People's Bank of China and National Financial Regulation Authority rules, updating policies after major 2024 guidelines and submitting quarterly reports; it enforces AML (anti-money laundering) controls covering 100% of high-risk clients and files suspicious activity reports within 24 hours.

Robust internal controls (segregation of duties, daily reconciliations) cut operational loss incidents by 28% in 2025 YTD and protect depositors and shareholders through monthly governance reviews.

- Quarterly regulatory filings

- 24h SAR (suspicious activity report) standard

- 100% high-risk client AML coverage

- Daily reconciliations, segregation of duties

- 28% drop in operational losses (2025 YTD)

Qilu Bank: 1.28% NPL, 45% automation, RMB18.4bn SME pipeline, 12% retail growth

Qilu Bank runs strict credit underwriting and digital-led service delivery, cutting NPLs to 1.28% (2024) and automating 45% of processes; SME/rural lending (RMB 18.4bn pipeline) and 142 branches plus 68% digital transactions drive 12% YoY retail growth and NPS 48. Operational controls halved incidents (28% drop 2025 YTD) and 100% AML coverage for high-risk clients.

| Metric | Value |

|---|---|

| NPL ratio (2024) | 1.28% |

| Auto processes | 45% |

| SME pipeline | RMB 18.4bn |

| Retail growth (2024) | 12% YoY |

| NPS (2024) | 48 |

| Branches | 142 |

| Digital txns (2024) | 68% |

| AML high-risk | 100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Qilu Bank Business Model Canvas—not a mockup or sample—and it reflects the exact content you will receive after purchase.

When you complete your order, you’ll get this same professional deliverable in editable formats, fully structured and ready to use for analysis, presentation, or strategy work.