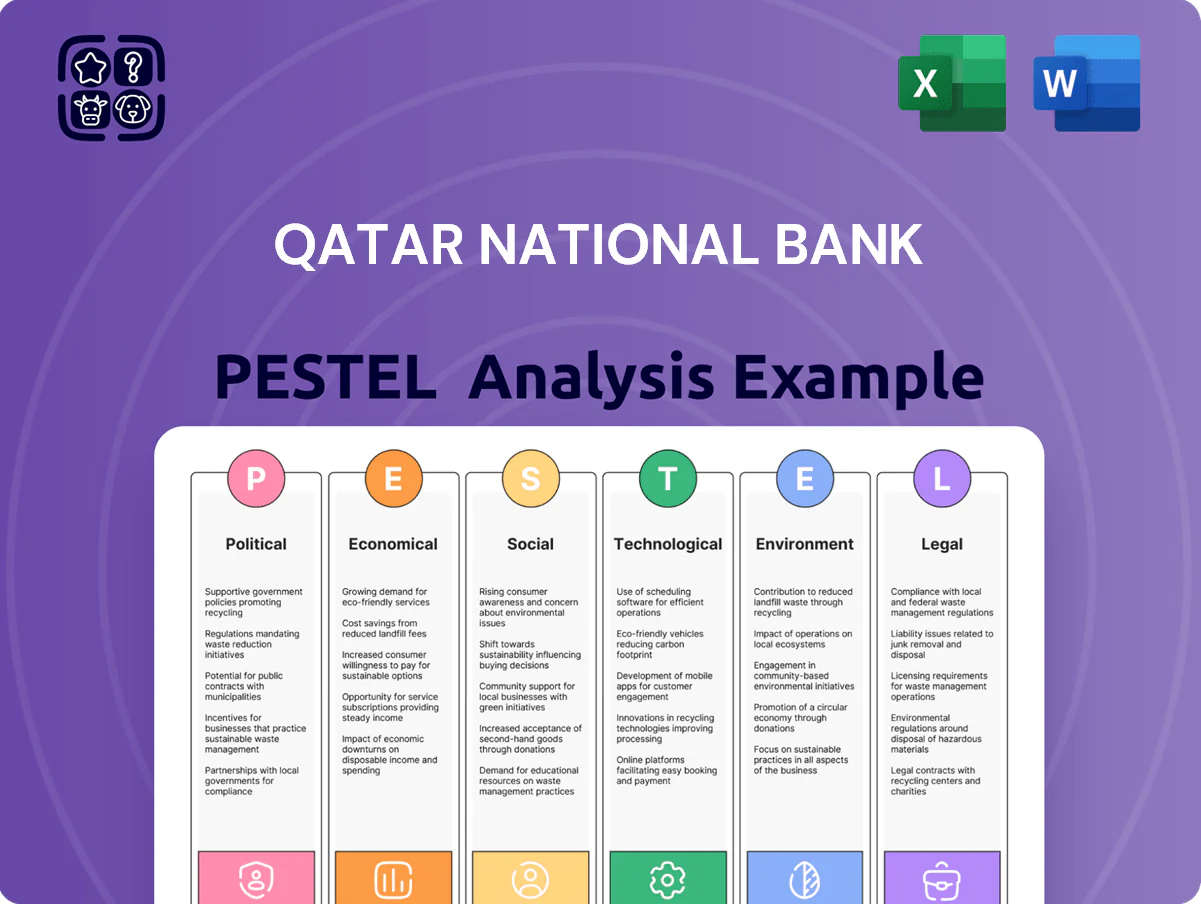

Qatar National Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Navigate the strategic landscape of Qatar National Bank with our concise PESTLE snapshot—spot regulatory, economic, and technological forces shaping its growth and risk profile; purchase the full PESTLE to unlock detailed, actionable insights and downloadable templates for investment decisions and strategic planning.

Political factors

Government Ownership and Strategic Support

QNB is 50 percent owned by the Qatar Investment Authority, creating a sovereign safety net that aligns the bank with national development goals and supports a Moody’s/Aa2-equivalent credit profile; this backing bolstered QNB’s resilience during the 2023–2025 market turbulence. As of late 2025, the partnership underpinned over $20bn in government-linked infrastructure financing, sustaining liquidity and strategic lending capacity.

Regional Geopolitical Stability and GCC Integration

The stabilization of GCC relations has created a more predictable environment for cross-border banking, supporting QNB’s regional operations as intra-GCC trade rose 7.5% in 2024 and bank cross-border flows increased by an estimated $12bn in the first half of 2025. QNB benefited from higher investment activity, reflected in a 6% rise in regional loan growth year-on-year to Q3 2025. Nevertheless, ongoing Middle East tensions kept risk premiums elevated, contributing to occasional liquidity tightening and a 40–60bp widening in regional sovereign spreads during flare-ups. The bank must continue balancing expanded regional exposure with heightened geopolitical risk management.

International Expansion and Sovereign Risk

QNBs large footprints in Turkey (market share via QNB Finansbank; Turkey assets ~USD 16.2bn in 2024) and Egypt (QNB Alahli; Egypt assets ~USD 17.5bn in 2024) expose the group to sovereign risk; Turkey lira volatility (TL fell ~18% vs USD in 2024) and Egypt’s 2024 inflation ~38% can erode earnings and prompt local currency translation losses.

Alignment with Qatar National Vision 2030

- Primary financier for Vision 2030-aligned projects

- QAR 507bn group loans (2024)

- Steady pipeline in healthcare, education, tourism

- Preferred partner for state strategic initiatives

Global Trade Policy and Sanctions Compliance

As a global financial hub, QNB must navigate a complex web of international trade policies and sanctions; in 2024 banks in the Gulf faced a 15–25% rise in compliance costs, pressuring QNB to scale monitoring and reporting systems.

Shifts in Western policy toward regional neighbors have forced rapid adjustments in correspondent relationships; QNB reported maintaining correspondent lines with over 70 international banks in 2024 to preserve liquidity corridors.

Rigorous standards are essential to avoid political friction and secure market access; QNB’s 2024 AML/CFT investments exceeded QAR 400 million to meet evolving regulator expectations and protect capital market access.

- 2024 compliance costs up 15–25%

- 70+ correspondent banks maintained

- QAR 400m+ AML/CFT investments in 2024

QNB: State-backed Aa2-like strength, QAR507bn loans, $20bn+ infra, Turkey/Egypt risks

QNB’s 50% QIA ownership and state backing supported liquidity and a Moody’s/Aa2-style profile; group loans QAR 507bn (2024) with >$20bn government-linked infrastructure financing (2023–25). Regional stability lifted intra-GCC flows +7.5% (2024) but geopolitical flare-ups widened sovereign spreads 40–60bp; Turkey/Egypt exposures (assets ~USD16.2bn, USD17.5bn in 2024) and FX/inflation risks persist.

| Metric | Value |

|---|---|

| Group loans (2024) | QAR 507bn |

| Govt-linked infra financing (2023–25) | >USD 20bn |

| Intra-GCC trade growth (2024) | +7.5% |

| Turkey assets (2024) | USD 16.2bn |

| Egypt assets (2024) | USD 17.5bn |

| Regional sovereign spread widening | 40–60bp |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Qatar National Bank, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented PESTLE summary for Qatar National Bank that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning.

Economic factors

Hydrocarbon Market Influence and LNG Expansion

Qatar's economy remains heavily dependent on LNG exports, with North Field expansion (Phase I+II) targeting ~110 mtpa by 2027 and adding over $28 billion CAPEX through 2025, sustaining GDP growth around 3.8% in 2024–25. QNB, as a lead financier, benefits from elevated loan book growth and liquidity inflows tied to project financing and contractor cashflows. Volatile global gas prices (Henry Hub/TTF swings of 30–60% in 2022–24) materially affect government revenues, the deposit base and sovereign credit metrics that underpin QNB's asset quality.

Interest Rate Environment and Monetary Policy

Because the Qatari Riyal is pegged to the US Dollar, QNB’s lending and deposit rates track US Federal Reserve moves; after Fed tightening pushed US policy rates to a 5.25–5.50% range in 2023–24, QNB saw NIM compression and higher funding costs.

High US rates reduced corporate and retail borrowing; by end-2025 the bank managed a shift toward a more stabilized/declining cycle—helping restore loan growth and modestly improving profitability forecasts compared with 2024.

Inflationary Pressures and Operational Costs

Global inflation eased to 3.2% in 2024 while Qatar's CPI averaged 4.7% in 2024–25, raising QNB's wage and IT spending as talent costs rose ~6% and tech CAPEX climbed 9% year-on-year.

Higher living costs trimmed household real incomes, slowing retail loan growth to 2.8% in 2024 and moderating mortgage originations versus 2023.

QNB offsets pressures via hedging and strict cost-management: efficiency ratio improved to ~29% in 2024 and interest-rate and FX hedges reduced volatility in net interest margin.

Diversification of Revenue Streams

QNB reduced domestic concentration by growing international subsidiaries and non-interest income: by 2025 non-funded income rose to ~38% of total revenue and overseas operations contributed 46% of group net profit, lowering sensitivity to Qatar GDP shocks.

Wealth management, investment banking and insurance now account for roughly 22% of revenue, strengthening resilience against localized downturns across Gulf and North African markets.

- Non-interest income ~38% of revenue (2025)

Currency Volatility in Subsidiary Markets

While the Qatari Riyal remains pegged to the US dollar, QNB carries notable economic exposure from Turkish Lira and Egyptian Pound volatility; TL fell about 25% vs USD in 2023–2024 and EGP saw c.15% devaluation in 2024, creating translation risk on subsidiary earnings.

Devaluations lead to translation losses when converting subsidiary profits into QAR; QNB reported FX translation impacts of several hundred million QAR in recent annuals, affecting consolidated net profit.

QNB uses advanced treasury hedging, netting and currency swaps to mitigate exposure, yet residual risk from rapidly shifting EM rates remains a key driver of group performance.

- TL down ~25% (2023–24), EGP down ~15% (2024)

- Translation losses amounted to several hundred million QAR (recent years)

- Treasury hedges, swaps, netting reduce but do not eliminate risk

QNB rides Qatar LNG boom as overseas profits offset FX hits, NII mix strengthens

QNB benefits from Qatar LNG-led growth (North Field ~110 mtpa by 2027; CAPEX >$28bn to 2025) supporting 3.8% GDP growth (2024–25), driving loan and liquidity inflows; NIM was pressured by US rate hikes (Fed 5.25–5.50% in 2023–24) but stabilized in 2025. Non-interest income rose to ~38% of revenue and overseas ops contributed 46% of group profit (2025), partially offsetting FX translation hits from TL -25% and EGP -15% (2023–24).

| Metric | Value |

|---|---|

| Qatar GDP growth (2024–25) | 3.8% |

| North Field capacity target | ~110 mtpa by 2027 |

| Project CAPEX to 2025 | >$28bn |

| Fed policy rate (peak) | 5.25–5.50% (2023–24) |

| Non-interest income | ~38% (2025) |

| Overseas profit contribution | 46% (2025) |

| TL / EGP moves | TL -25%, EGP -15% (2023–24) |

Full Version Awaits

Qatar National Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Qatar National Bank PESTLE analysis includes detailed political, economic, social, technological, legal, and environmental insights, structured for immediate application. No placeholders or teasers—what you see is the final, professionally formatted file. You’ll be able to download this exact document instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Navigate the strategic landscape of Qatar National Bank with our concise PESTLE snapshot—spot regulatory, economic, and technological forces shaping its growth and risk profile; purchase the full PESTLE to unlock detailed, actionable insights and downloadable templates for investment decisions and strategic planning.

Political factors

Government Ownership and Strategic Support

QNB is 50 percent owned by the Qatar Investment Authority, creating a sovereign safety net that aligns the bank with national development goals and supports a Moody’s/Aa2-equivalent credit profile; this backing bolstered QNB’s resilience during the 2023–2025 market turbulence. As of late 2025, the partnership underpinned over $20bn in government-linked infrastructure financing, sustaining liquidity and strategic lending capacity.

Regional Geopolitical Stability and GCC Integration

The stabilization of GCC relations has created a more predictable environment for cross-border banking, supporting QNB’s regional operations as intra-GCC trade rose 7.5% in 2024 and bank cross-border flows increased by an estimated $12bn in the first half of 2025. QNB benefited from higher investment activity, reflected in a 6% rise in regional loan growth year-on-year to Q3 2025. Nevertheless, ongoing Middle East tensions kept risk premiums elevated, contributing to occasional liquidity tightening and a 40–60bp widening in regional sovereign spreads during flare-ups. The bank must continue balancing expanded regional exposure with heightened geopolitical risk management.

International Expansion and Sovereign Risk

QNBs large footprints in Turkey (market share via QNB Finansbank; Turkey assets ~USD 16.2bn in 2024) and Egypt (QNB Alahli; Egypt assets ~USD 17.5bn in 2024) expose the group to sovereign risk; Turkey lira volatility (TL fell ~18% vs USD in 2024) and Egypt’s 2024 inflation ~38% can erode earnings and prompt local currency translation losses.

Alignment with Qatar National Vision 2030

- Primary financier for Vision 2030-aligned projects

- QAR 507bn group loans (2024)

- Steady pipeline in healthcare, education, tourism

- Preferred partner for state strategic initiatives

Global Trade Policy and Sanctions Compliance

As a global financial hub, QNB must navigate a complex web of international trade policies and sanctions; in 2024 banks in the Gulf faced a 15–25% rise in compliance costs, pressuring QNB to scale monitoring and reporting systems.

Shifts in Western policy toward regional neighbors have forced rapid adjustments in correspondent relationships; QNB reported maintaining correspondent lines with over 70 international banks in 2024 to preserve liquidity corridors.

Rigorous standards are essential to avoid political friction and secure market access; QNB’s 2024 AML/CFT investments exceeded QAR 400 million to meet evolving regulator expectations and protect capital market access.

- 2024 compliance costs up 15–25%

- 70+ correspondent banks maintained

- QAR 400m+ AML/CFT investments in 2024

QNB: State-backed Aa2-like strength, QAR507bn loans, $20bn+ infra, Turkey/Egypt risks

QNB’s 50% QIA ownership and state backing supported liquidity and a Moody’s/Aa2-style profile; group loans QAR 507bn (2024) with >$20bn government-linked infrastructure financing (2023–25). Regional stability lifted intra-GCC flows +7.5% (2024) but geopolitical flare-ups widened sovereign spreads 40–60bp; Turkey/Egypt exposures (assets ~USD16.2bn, USD17.5bn in 2024) and FX/inflation risks persist.

| Metric | Value |

|---|---|

| Group loans (2024) | QAR 507bn |

| Govt-linked infra financing (2023–25) | >USD 20bn |

| Intra-GCC trade growth (2024) | +7.5% |

| Turkey assets (2024) | USD 16.2bn |

| Egypt assets (2024) | USD 17.5bn |

| Regional sovereign spread widening | 40–60bp |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Qatar National Bank, with data-backed trends and region-specific examples to identify threats and opportunities.

A concise, visually segmented PESTLE summary for Qatar National Bank that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market positioning.

Economic factors

Hydrocarbon Market Influence and LNG Expansion

Qatar's economy remains heavily dependent on LNG exports, with North Field expansion (Phase I+II) targeting ~110 mtpa by 2027 and adding over $28 billion CAPEX through 2025, sustaining GDP growth around 3.8% in 2024–25. QNB, as a lead financier, benefits from elevated loan book growth and liquidity inflows tied to project financing and contractor cashflows. Volatile global gas prices (Henry Hub/TTF swings of 30–60% in 2022–24) materially affect government revenues, the deposit base and sovereign credit metrics that underpin QNB's asset quality.

Interest Rate Environment and Monetary Policy

Because the Qatari Riyal is pegged to the US Dollar, QNB’s lending and deposit rates track US Federal Reserve moves; after Fed tightening pushed US policy rates to a 5.25–5.50% range in 2023–24, QNB saw NIM compression and higher funding costs.

High US rates reduced corporate and retail borrowing; by end-2025 the bank managed a shift toward a more stabilized/declining cycle—helping restore loan growth and modestly improving profitability forecasts compared with 2024.

Inflationary Pressures and Operational Costs

Global inflation eased to 3.2% in 2024 while Qatar's CPI averaged 4.7% in 2024–25, raising QNB's wage and IT spending as talent costs rose ~6% and tech CAPEX climbed 9% year-on-year.

Higher living costs trimmed household real incomes, slowing retail loan growth to 2.8% in 2024 and moderating mortgage originations versus 2023.

QNB offsets pressures via hedging and strict cost-management: efficiency ratio improved to ~29% in 2024 and interest-rate and FX hedges reduced volatility in net interest margin.

Diversification of Revenue Streams

QNB reduced domestic concentration by growing international subsidiaries and non-interest income: by 2025 non-funded income rose to ~38% of total revenue and overseas operations contributed 46% of group net profit, lowering sensitivity to Qatar GDP shocks.

Wealth management, investment banking and insurance now account for roughly 22% of revenue, strengthening resilience against localized downturns across Gulf and North African markets.

- Non-interest income ~38% of revenue (2025)

Currency Volatility in Subsidiary Markets

While the Qatari Riyal remains pegged to the US dollar, QNB carries notable economic exposure from Turkish Lira and Egyptian Pound volatility; TL fell about 25% vs USD in 2023–2024 and EGP saw c.15% devaluation in 2024, creating translation risk on subsidiary earnings.

Devaluations lead to translation losses when converting subsidiary profits into QAR; QNB reported FX translation impacts of several hundred million QAR in recent annuals, affecting consolidated net profit.

QNB uses advanced treasury hedging, netting and currency swaps to mitigate exposure, yet residual risk from rapidly shifting EM rates remains a key driver of group performance.

- TL down ~25% (2023–24), EGP down ~15% (2024)

- Translation losses amounted to several hundred million QAR (recent years)

- Treasury hedges, swaps, netting reduce but do not eliminate risk

QNB rides Qatar LNG boom as overseas profits offset FX hits, NII mix strengthens

QNB benefits from Qatar LNG-led growth (North Field ~110 mtpa by 2027; CAPEX >$28bn to 2025) supporting 3.8% GDP growth (2024–25), driving loan and liquidity inflows; NIM was pressured by US rate hikes (Fed 5.25–5.50% in 2023–24) but stabilized in 2025. Non-interest income rose to ~38% of revenue and overseas ops contributed 46% of group profit (2025), partially offsetting FX translation hits from TL -25% and EGP -15% (2023–24).

| Metric | Value |

|---|---|

| Qatar GDP growth (2024–25) | 3.8% |

| North Field capacity target | ~110 mtpa by 2027 |

| Project CAPEX to 2025 | >$28bn |

| Fed policy rate (peak) | 5.25–5.50% (2023–24) |

| Non-interest income | ~38% (2025) |

| Overseas profit contribution | 46% (2025) |

| TL / EGP moves | TL -25%, EGP -15% (2023–24) |

Full Version Awaits

Qatar National Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Qatar National Bank PESTLE analysis includes detailed political, economic, social, technological, legal, and environmental insights, structured for immediate application. No placeholders or teasers—what you see is the final, professionally formatted file. You’ll be able to download this exact document instantly after payment.