Quadient Boston Consulting Group Matrix

Actionable Strategy Starts Here

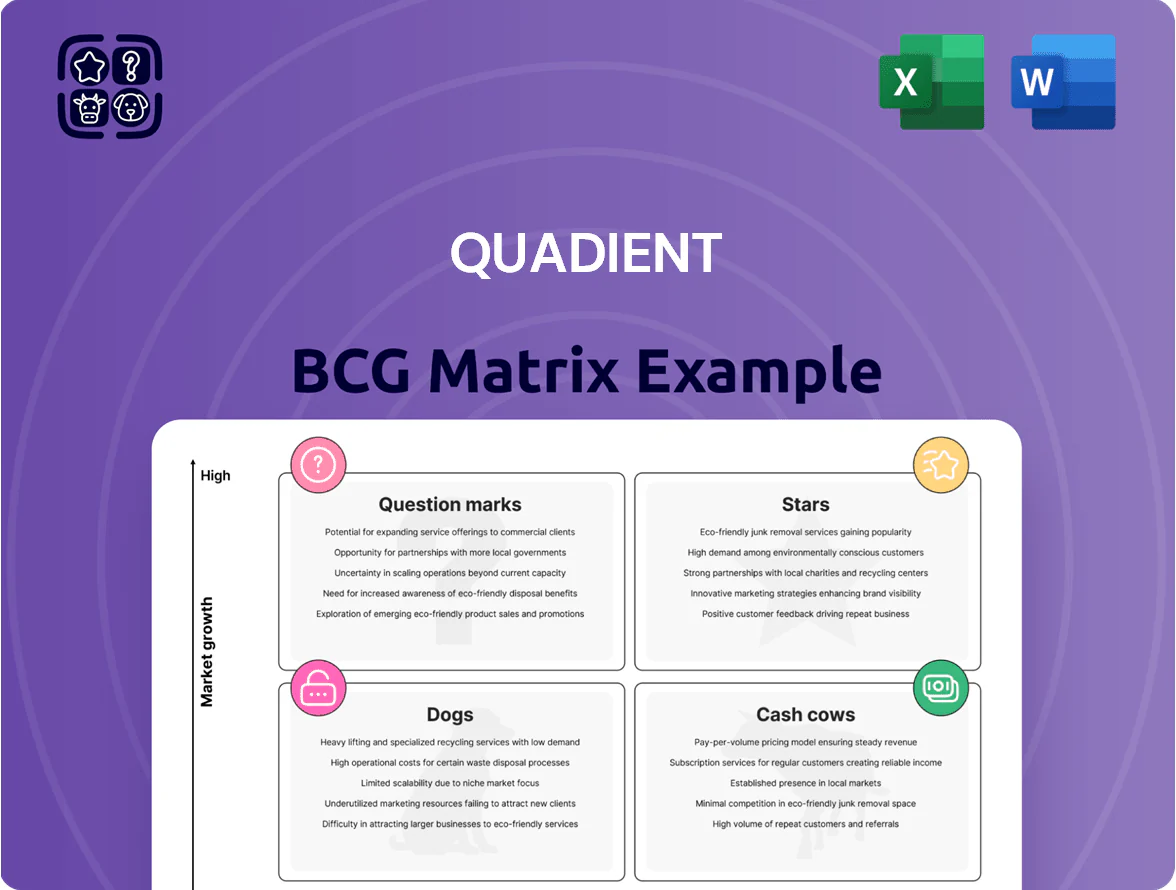

Quadient’s BCG Matrix preview shows how its product lines map across growth and market share—spotting potential Stars in digital parcel lockers, Cash Cows in mailing solutions, and Question Marks in emerging software services. This snapshot highlights strategic pressure points and capital allocation choices that matter to investors and managers. This preview is just the beginning. Get the full BCG Matrix report to uncover detailed quadrant placements, data-backed recommendations, and a roadmap to smart investment and product decisions.

Stars

Digital Customer Communications Management

Quadient holds the number one global market share in Customer Communications Management (CCM) as of late 2025, with an 11% share of the $6.8B worldwide CCM market (source: industry tracker, 2025).

The CCM segment is high-growth, led by enterprise shifts to AI-powered, cloud platforms that unify digital and human touchpoints, growing ~14% CAGR in 2023–25.

Quadient’s Elevate to 2030 strategy moved its CCM suite into a high-growth leader, producing double-digit organic subscription revenue growth across 2025 and lifting CCM recurring revenue to ~62% of total CCM sales.

Ongoing investment in AI-assisted authoring and journey orchestration is required to hold leadership against emerging SaaS rivals and protect margin expansion.

Intelligent Parcel Locker Systems

Parcel Pending by Quadient is a Star, hitting over 100 million euros in annual revenue by mid-2025 and growing double digits year-over-year.

It rides e-commerce tailwinds—North America and Europe demand secure, contactless last-mile delivery—driving an installed base above 25,000 units after acquiring Package Concierge.

Quadient launched open locker networks in Italy and other markets; capital intensity for deployment and maintenance is high, but margin expansion and scale make it a top investment focus.

Business Process Automation Software

Quadient's accounts receivable and accounts payable automation solutions sit in the Star quadrant—part of a global financial workflow automation market worth over 6 billion USD in 2025—driven by rapid enterprise digitization.

These SaaS tools show 30% year‑on‑year cross‑sell growth into existing mail customers, signaling strong demand and expanding customer lifetime value.

Recognition in the 2024 Gartner Magic Quadrant for Accounts Payable Applications highlights Quadient's competitive strength and market momentum.

To sustain Star status, Quadient is adding advanced AI and real‑time payment rails to target larger enterprise accounts and lift average contract value.

SaaS Subscription-Related Revenue

Takeaway: Quadient’s SaaS subscription-related revenue, driving ~75% of group sales by end-2025, is the Star in the BCG matrix due to double-digit organic growth and expanding market share.

Recurring cloud subscriptions replaced one-time licenses, stabilizing cash flow and margins while capturing digital automation demand; this pathway supports the 2030 target of €1.0bn in recurring revenue.

Here’s the quick math: ~75% of 2025 group revenue, double-digit organic CAGR, and multi-year ARR expansion underpin Star status.

- ~75% of group revenue from subscriptions (end-2025)

- Double-digit organic growth in recurring revenue

- Shift to cloud subscriptions stabilized financials

- Target: €1bn recurring revenue by 2030

North American Digital Market

North America is a Star for Quadient, delivering over 50% of revenue in 2024 with digital solution placements growing ~18% year-over-year and driving most SaaS ARR gains.

US and Canada demand for digital transformation kept automation platforms on a high-growth path despite weak traditional sectors; Q4 2024 bookings rose ~15% vs. prior year.

Customer satisfaction exceeds 90% NPS-equivalent, creating a moat; localized R&D and targeted US acquisitions remain key to sustain this region as the primary revenue engine.

- >50% revenue share (2024)

- Digital placements +18% YoY (2024)

- Q4 2024 bookings +15% YoY

- Customer satisfaction >90%

- Focus: localized innovation + US M&A

Quadient targets €1B recurring by 2030 as CCM, Parcel Pending & AP/AR fuel double‑digit growth

Quadient’s Stars: CCM leadership (11% share of $6.8B market, 2025), Parcel Pending >€100M revenue (mid-2025) and AP/AR SaaS (30% YoY cross‑sell; market >$6B, 2025) drive ~75% subscription mix and double‑digit recurring growth; target €1.0B recurring by 2030.

| Metric | 2025 |

|---|---|

| CCM share | 11% |

| Parcel Pending rev | €100M+ |

| Subscription mix | ~75% |

What is included in the product

Comprehensive BCG Matrix review of Quadient’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Quadient BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Traditional Mail-Related Solutions

Mail-related solutions, including franking machines and folding/inserting systems, are Quadient’s primary cash cow, holding high market share in a mature, slowly declining market.

As the world’s second-largest franking-machine provider, Quadient serves ~350,000 installed-base customers, producing predictable cash flow and recurring supply/maintenance revenue.

The segment reported ~86 million euros EBITDA in H1 2025, high profit margins, and funds R&D for digital growth; customer satisfaction sits at ~95% despite organic revenue declines.

Main European Mail Operations

Quadient’s Main European Mail Operations sit in a mature market where it holds leading shares—about 30% in France and 18% in the UK (2024 estimates)—making it a classic cash cow within the BCG matrix.

These mail services need relatively low new marketing spend versus digital products, generating steady free cash flow: Quadient reported €240m operating cash from mail-related activities in 2024.

Although physical mail volumes fell ~6% YoY in Western Europe (2023–24), Quadient’s cost control and scale let it sustain margins and “milk” profits.

Management redeploys this cash to grow parcel lockers (targeting 25k units by 2026) and expand digital automation suites, funding growth without equity dilution.

Mail Equipment Leasing and Maintenance

A large share of Quadient’s mail revenue—about 55% in 2024—comes from long-term leasing and maintenance contracts that deliver stable, recurring cash inflows, supporting 2024 mail segment EBITDA margins near 28%.

These services rest on a mature installed base and established competitive advantages, producing high margins with low capex; hardware renewals fluctuate, but leasing and maintenance remained resilient, providing predictable free cash flow of roughly €120–€150 million annually in 2024.

That steady cash generation helps Quadient service corporate debt (net debt/EBITDA ~1.6x in FY 2024) and fund consistent dividends, underpinning shareholder returns even when device sales cycle.

Legacy Document Generation Software

Legacy on-premise document generation tools still hold ~40–55% installed share in regulated banking and insurance accounts for Quadient as of 2025, producing steady, high-margin maintenance revenue while clients migrate slowly to cloud CCM.

These mature products need minimal promo spend—focus is retention and staged cloud migration—so operating margins on legacy lines run 25–35%, funding R&D for AI-driven communication platforms launched in 2024–25.

- Installed share in regulated sectors: ~40–55%

- Maintenance margin: ~25–35%

- Low promotional spend; retention-focused

- Funds AI CCM R&D (2024–25 initiatives)

International Mail Segment

Quadient’s International Mail segment outside North America and Europe acts as a small, stable cash cow, generating steady margins—about 8–10% operating margin in 2024—and consistent free cash flow that supports group liquidity.

These markets track developed-region trends, add geographic diversification, and are served via Quadient’s global supply chain and existing tech with minimal extra capex, contributing roughly 5–7% of 2024 revenue.

The cash flow backs Quadient’s strategic pivot to intelligent automation in higher-growth markets, funding R&D and M&A without raising net debt (net debt/EBITDA ~1.2x in 2024).

- Stable margins: 8–10% operating margin (2024)

- Revenue share: ~5–7% of Group revenue (2024)

- Low incremental capex: uses existing supply chain

- Supports pivot: funds R&D/M&A; net debt/EBITDA ~1.2x (2024)

Quadient: €240m mail cash engine funds locker scale-up & AI CCM while holding low leverage

Quadient’s mail-related cash cows (franking, folding/inserting, legacy CCM) deliver predictable high-margin cash: ~€240m operating cash (2024), mail EBITDA ~€86m (H1 2025), maintenance margins 25–35%, installed bases 350k devices and 40–55% share in regulated CCM; funds parcel locker scale-up (25k target by 2026) and AI CCM R&D while keeping net debt/EBITDA ~1.2–1.6x (2024).

| Metric | Value |

|---|---|

| Operating cash (mail) | €240m (2024) |

| Mail EBITDA | €86m (H1 2025) |

| Installed base | ~350,000 |

| CCM regulated share | 40–55% (2025) |

| Maintenance margin | 25–35% (2024) |

| Net debt/EBITDA | ~1.2–1.6x (2024) |

Delivered as Shown

Quadient BCG Matrix

The file you're previewing on this page is the final Quadient BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use strategic report built for clarity and decision-making.

This preview reflects the exact same Quadient BCG Matrix report downloadable post-purchase, crafted with market-backed analysis and professional design—ready to present or edit immediately.

What you see is the actual Quadient BCG Matrix file that becomes yours after a one-time purchase; no mockups, no surprises—just an analysis-ready deliverable.

The report you're reviewing is precisely what you'll get after buying: expert-designed, formatted for business planning, and instantly available for printing or sharing.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Quadient’s BCG Matrix preview shows how its product lines map across growth and market share—spotting potential Stars in digital parcel lockers, Cash Cows in mailing solutions, and Question Marks in emerging software services. This snapshot highlights strategic pressure points and capital allocation choices that matter to investors and managers. This preview is just the beginning. Get the full BCG Matrix report to uncover detailed quadrant placements, data-backed recommendations, and a roadmap to smart investment and product decisions.

Stars

Digital Customer Communications Management

Quadient holds the number one global market share in Customer Communications Management (CCM) as of late 2025, with an 11% share of the $6.8B worldwide CCM market (source: industry tracker, 2025).

The CCM segment is high-growth, led by enterprise shifts to AI-powered, cloud platforms that unify digital and human touchpoints, growing ~14% CAGR in 2023–25.

Quadient’s Elevate to 2030 strategy moved its CCM suite into a high-growth leader, producing double-digit organic subscription revenue growth across 2025 and lifting CCM recurring revenue to ~62% of total CCM sales.

Ongoing investment in AI-assisted authoring and journey orchestration is required to hold leadership against emerging SaaS rivals and protect margin expansion.

Intelligent Parcel Locker Systems

Parcel Pending by Quadient is a Star, hitting over 100 million euros in annual revenue by mid-2025 and growing double digits year-over-year.

It rides e-commerce tailwinds—North America and Europe demand secure, contactless last-mile delivery—driving an installed base above 25,000 units after acquiring Package Concierge.

Quadient launched open locker networks in Italy and other markets; capital intensity for deployment and maintenance is high, but margin expansion and scale make it a top investment focus.

Business Process Automation Software

Quadient's accounts receivable and accounts payable automation solutions sit in the Star quadrant—part of a global financial workflow automation market worth over 6 billion USD in 2025—driven by rapid enterprise digitization.

These SaaS tools show 30% year‑on‑year cross‑sell growth into existing mail customers, signaling strong demand and expanding customer lifetime value.

Recognition in the 2024 Gartner Magic Quadrant for Accounts Payable Applications highlights Quadient's competitive strength and market momentum.

To sustain Star status, Quadient is adding advanced AI and real‑time payment rails to target larger enterprise accounts and lift average contract value.

SaaS Subscription-Related Revenue

Takeaway: Quadient’s SaaS subscription-related revenue, driving ~75% of group sales by end-2025, is the Star in the BCG matrix due to double-digit organic growth and expanding market share.

Recurring cloud subscriptions replaced one-time licenses, stabilizing cash flow and margins while capturing digital automation demand; this pathway supports the 2030 target of €1.0bn in recurring revenue.

Here’s the quick math: ~75% of 2025 group revenue, double-digit organic CAGR, and multi-year ARR expansion underpin Star status.

- ~75% of group revenue from subscriptions (end-2025)

- Double-digit organic growth in recurring revenue

- Shift to cloud subscriptions stabilized financials

- Target: €1bn recurring revenue by 2030

North American Digital Market

North America is a Star for Quadient, delivering over 50% of revenue in 2024 with digital solution placements growing ~18% year-over-year and driving most SaaS ARR gains.

US and Canada demand for digital transformation kept automation platforms on a high-growth path despite weak traditional sectors; Q4 2024 bookings rose ~15% vs. prior year.

Customer satisfaction exceeds 90% NPS-equivalent, creating a moat; localized R&D and targeted US acquisitions remain key to sustain this region as the primary revenue engine.

- >50% revenue share (2024)

- Digital placements +18% YoY (2024)

- Q4 2024 bookings +15% YoY

- Customer satisfaction >90%

- Focus: localized innovation + US M&A

Quadient targets €1B recurring by 2030 as CCM, Parcel Pending & AP/AR fuel double‑digit growth

Quadient’s Stars: CCM leadership (11% share of $6.8B market, 2025), Parcel Pending >€100M revenue (mid-2025) and AP/AR SaaS (30% YoY cross‑sell; market >$6B, 2025) drive ~75% subscription mix and double‑digit recurring growth; target €1.0B recurring by 2030.

| Metric | 2025 |

|---|---|

| CCM share | 11% |

| Parcel Pending rev | €100M+ |

| Subscription mix | ~75% |

What is included in the product

Comprehensive BCG Matrix review of Quadient’s portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Quadient BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Traditional Mail-Related Solutions

Mail-related solutions, including franking machines and folding/inserting systems, are Quadient’s primary cash cow, holding high market share in a mature, slowly declining market.

As the world’s second-largest franking-machine provider, Quadient serves ~350,000 installed-base customers, producing predictable cash flow and recurring supply/maintenance revenue.

The segment reported ~86 million euros EBITDA in H1 2025, high profit margins, and funds R&D for digital growth; customer satisfaction sits at ~95% despite organic revenue declines.

Main European Mail Operations

Quadient’s Main European Mail Operations sit in a mature market where it holds leading shares—about 30% in France and 18% in the UK (2024 estimates)—making it a classic cash cow within the BCG matrix.

These mail services need relatively low new marketing spend versus digital products, generating steady free cash flow: Quadient reported €240m operating cash from mail-related activities in 2024.

Although physical mail volumes fell ~6% YoY in Western Europe (2023–24), Quadient’s cost control and scale let it sustain margins and “milk” profits.

Management redeploys this cash to grow parcel lockers (targeting 25k units by 2026) and expand digital automation suites, funding growth without equity dilution.

Mail Equipment Leasing and Maintenance

A large share of Quadient’s mail revenue—about 55% in 2024—comes from long-term leasing and maintenance contracts that deliver stable, recurring cash inflows, supporting 2024 mail segment EBITDA margins near 28%.

These services rest on a mature installed base and established competitive advantages, producing high margins with low capex; hardware renewals fluctuate, but leasing and maintenance remained resilient, providing predictable free cash flow of roughly €120–€150 million annually in 2024.

That steady cash generation helps Quadient service corporate debt (net debt/EBITDA ~1.6x in FY 2024) and fund consistent dividends, underpinning shareholder returns even when device sales cycle.

Legacy Document Generation Software

Legacy on-premise document generation tools still hold ~40–55% installed share in regulated banking and insurance accounts for Quadient as of 2025, producing steady, high-margin maintenance revenue while clients migrate slowly to cloud CCM.

These mature products need minimal promo spend—focus is retention and staged cloud migration—so operating margins on legacy lines run 25–35%, funding R&D for AI-driven communication platforms launched in 2024–25.

- Installed share in regulated sectors: ~40–55%

- Maintenance margin: ~25–35%

- Low promotional spend; retention-focused

- Funds AI CCM R&D (2024–25 initiatives)

International Mail Segment

Quadient’s International Mail segment outside North America and Europe acts as a small, stable cash cow, generating steady margins—about 8–10% operating margin in 2024—and consistent free cash flow that supports group liquidity.

These markets track developed-region trends, add geographic diversification, and are served via Quadient’s global supply chain and existing tech with minimal extra capex, contributing roughly 5–7% of 2024 revenue.

The cash flow backs Quadient’s strategic pivot to intelligent automation in higher-growth markets, funding R&D and M&A without raising net debt (net debt/EBITDA ~1.2x in 2024).

- Stable margins: 8–10% operating margin (2024)

- Revenue share: ~5–7% of Group revenue (2024)

- Low incremental capex: uses existing supply chain

- Supports pivot: funds R&D/M&A; net debt/EBITDA ~1.2x (2024)

Quadient: €240m mail cash engine funds locker scale-up & AI CCM while holding low leverage

Quadient’s mail-related cash cows (franking, folding/inserting, legacy CCM) deliver predictable high-margin cash: ~€240m operating cash (2024), mail EBITDA ~€86m (H1 2025), maintenance margins 25–35%, installed bases 350k devices and 40–55% share in regulated CCM; funds parcel locker scale-up (25k target by 2026) and AI CCM R&D while keeping net debt/EBITDA ~1.2–1.6x (2024).

| Metric | Value |

|---|---|

| Operating cash (mail) | €240m (2024) |

| Mail EBITDA | €86m (H1 2025) |

| Installed base | ~350,000 |

| CCM regulated share | 40–55% (2025) |

| Maintenance margin | 25–35% (2024) |

| Net debt/EBITDA | ~1.2–1.6x (2024) |

Delivered as Shown

Quadient BCG Matrix

The file you're previewing on this page is the final Quadient BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, ready-to-use strategic report built for clarity and decision-making.

This preview reflects the exact same Quadient BCG Matrix report downloadable post-purchase, crafted with market-backed analysis and professional design—ready to present or edit immediately.

What you see is the actual Quadient BCG Matrix file that becomes yours after a one-time purchase; no mockups, no surprises—just an analysis-ready deliverable.

The report you're reviewing is precisely what you'll get after buying: expert-designed, formatted for business planning, and instantly available for printing or sharing.