Quantum Porter's Five Forces Analysis

From Overview to Strategy Blueprint

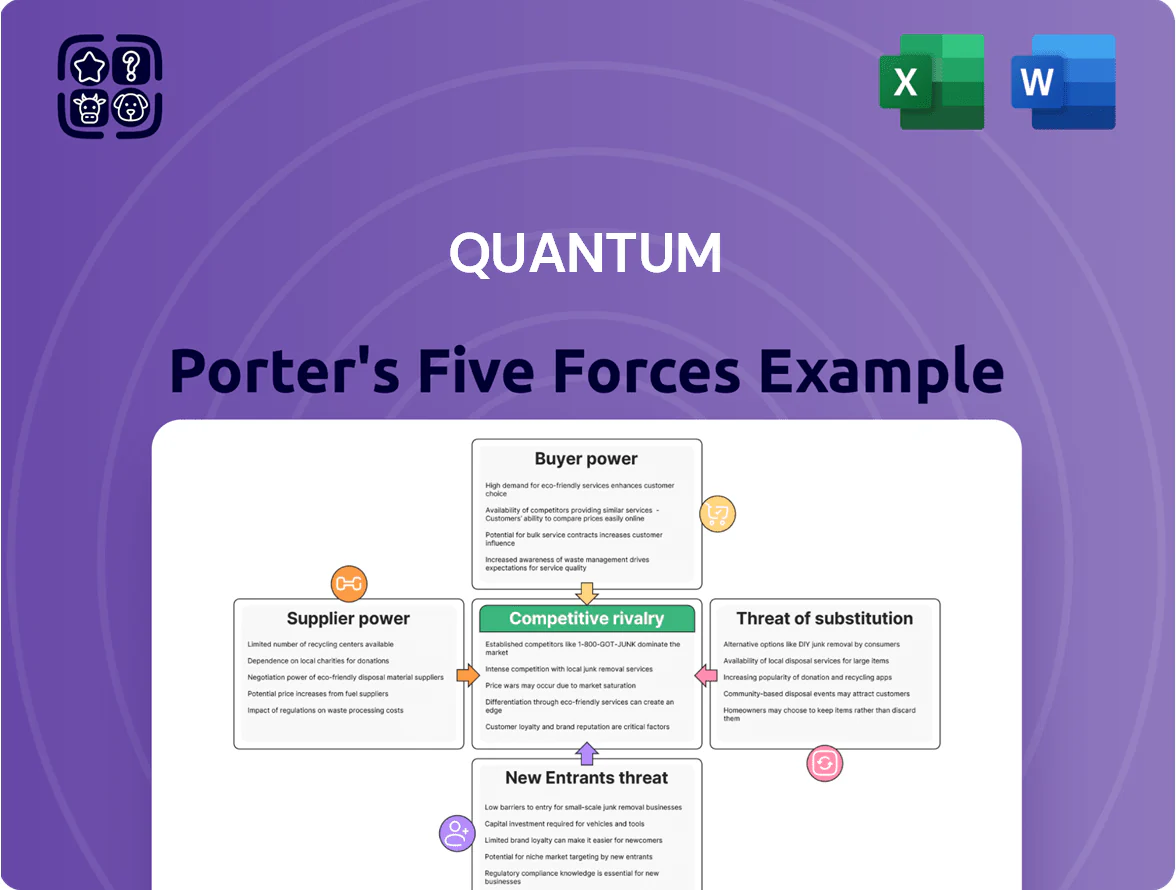

Quantum’s Porter's Five Forces snapshot highlights how supplier leverage, buyer power, competitive rivalry, threat of substitutes, and barriers to entry shape its strategic posture—revealing key pressures and potential vulnerabilities for investors and managers alike.

Suppliers Bargaining Power

Concentration of HDD and SSD Manufacturers

Quantum depends on a small set of HDD and SSD makers, which gives suppliers strong leverage because high-capacity media for unstructured data is specialized; top four vendors controlled about 78% of enterprise SSD/HDD shipments in 2025.

Supplier pricing power rose after 2024–25 semiconductor consolidation—major vendors increased ASPs (average selling prices) by ~12% YoY in H1 2025, squeezing margins for smaller hardware integrators like Quantum.

Long lead times (12–20 weeks) for high-capacity drives and limited alternative fabs raise switching costs and increase supply risk for Quantum, forcing reliance on vendor contracts and inventory buffers.

Dependency on LTO Tape Technology

Quantum depends on the LTO consortium for technology direction; as of 2025 the consortium includes IBM, HPE, and others who set roadmaps that Quantum must follow.

Only a handful of vendors produce LTO media and drive heads; supply concentration means a 1–3% rise in licensing or component costs can cut tape margins materially—Quantum reported 2024 gross margin on tape products near 22%.

This supplier concentration limits Quantum’s negotiating leverage, constraining price cuts for long-term preservation solutions and raising exposure to production delays and licensing shifts.

Specialized Semiconductor and Controller Supply

The shift to AI-driven metadata tagging and high-speed indexing needs advanced controllers and AI accelerators; 2025 market data shows top 5 silicon vendors (TSMC fabs plus Nvidia, Broadcom, Samsung foundry partners) control ~80% of advanced node capacity, concentrating supplier power.

Smartphone and automotive orders drove a 22% jump in 5nm+ wafer demand in 2024, so Quantum risks supply volatility and 10–25% premium pricing during peak cycles, squeezing margins unless it secures long-term supply agreements or pays wafer-priority premiums.

Proprietary Software Component Licensing

Quantum embeds third-party security and interoperability modules under multi-year licenses; these suppliers hold leverage via essential IP and renewal terms, and 2025 industry reports show enterprise software OEMs capturing 15–25% gross margin uplift from license renewals.

If a supplier hikes fees, Quantum faces either absorbing higher costs—compressing EBITDA—or removing features and losing clients; a 2024 vendor-concentration study found 40% of platforms rely on three or fewer critical vendors.

- Multi-year licenses concentrate supplier power

- Critical IP creates switching friction

- License fee hikes hit EBITDA or product scope

- 40% platforms depend on ≤3 key vendors

- Renewal margins typically add 15–25%

Global Logistics and Material Costs

Global logistics and material-cost swings leave Quantum exposed: chassis, PSUs, and cooling systems saw input-cost inflation of ~14% from 2020–2024, and average ocean freight rates remained 3x pre‑pandemic levels into 2024, raising BOM (bill of materials) costs materially.

Regionalized 2025 supply chains increased lead times by 25% and added 6–9% procurement premium versus global sourcing, while trade barriers (tariffs, export controls) raise supplier leverage.

- Input inflation ~14% (2020–2024)

- Ocean freight ~3x pre‑2019 rates

- Lead times +25% (regionalization)

- Procurement premium +6–9% (2025)

Supplier dominance, rising ASPs and constrained wafers threaten Quantum’s tape EBITDA

Suppliers hold strong leverage: top HDD/SSD vendors controlled ~78% shipments in 2025, ASPs rose ~12% YoY H1 2025, lead times 12–20 weeks, and 5nm+ wafer capacity concentrated (~80% control), so component/licensing hikes (1–3%) or license renewals (+15–25% margins) materially compress Quantum’s tape and appliance EBITDA.

| Metric | Value (2024–25) |

|---|---|

| Top SSD/HDD share | ~78% |

| ASPs change H1 2025 | +12% YoY |

| Drive lead times | 12–20 weeks |

| Advanced node capacity control | ~80% |

| Input inflation (2020–24) | ~14% |

| Ocean freight vs pre‑2019 | ~3x |

| Tape gross margin (Quantum 2024) | ~22% |

What is included in the product

Tailored Five Forces analysis for Quantum that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary for use in investor materials and strategy decks.

Quantum Porter's Five Forces condenses strategic pressure into a single, dynamic view—adjust force weights, swap scenarios, and export clean visuals for decks to speed confident decisions.

Customers Bargaining Power

Consolidation of Media and Entertainment Clients

Major media conglomerates account for roughly 35–45% of Quantum’s annual revenue, and recent mega-mergers (e.g., 2023–2024 deals) concentrate buying power, raising their negotiation leverage. Large buyers demand double-digit discounts and bespoke SLAs because they handle petabytes of content; switching to alternative storage or cloud architectures can save them 10–30% in TCO, so their growing scale significantly pressures Quantum’s pricing and contract terms.

Availability of Hyperscale Cloud Alternatives

Customers can shift unstructured workloads to AWS, Azure, or Google Cloud, giving them leverage; public cloud IaaS revenue hit about $680B in 2025, so buyers compare Quantum’s on‑prem/hybrid prices to that scale.

This alternative caps Quantum’s pricing power—enterprises cite cloud TCO reductions of 20–40% in 2024–25, so procurement teams push for lower on‑prem storage fees.

Ease of migration and cloud‑first policies make customers price‑sensitive: surveys show 58% of large firms favored cloud‑first terms in 2025 negotiations, raising churn risk if Quantum’s pricing exceeds cloud parity.

Low Switching Costs for Software-Defined Storage

The move to software-defined storage lets customers run Quantum’s management layer on commodity servers from Dell, HPE, or Supermicro, cutting hardware lock-in; IDC reported 2024 SDS deployments grew 18% YoY, reaching $9.6B, which raises buyer leverage.

Budget Constraints in Government and Research Sectors

These buyers use formal competitive tenders and RFPs, so vendors compete heavily on price and service levels; public procurement transparency (EU Open Contracting, US SAM) lets buyers benchmark offers and push for best performance-per-dollar.

That combination raises buyer bargaining power, often shrinking contract margins by 5–12% versus commercial deals.

- ~38% revenue from public/research (2024)

- Competitive tenders common—lowers prices

- Procurement transparency enables benchmarking

- Margins cut 5–12% vs commercial sales

Demand for Flexible Consumption Models

- 62% of IT budgets to OpEx (2024)

- As-a-service contracts +28% YoY (2024)

- Revenue timing delayed; vendor bears capacity risk

Cloud TCO cuts, mega‑buyers squeeze Quantum—double‑digit discounts, margin pressure

Major buyers (35–45% revenue) and 2023–24 mega‑mergers concentrate leverage, pushing double‑digit discounts; cloud alternatives (public cloud IaaS ~$680B in 2025) and reported cloud TCO cuts of 20–40% tighten Quantum’s pricing power, while 38% public/research mix and OpEx demand (62% IT budgets to OpEx in 2024) drive tendering, subscription pressure, and margin compression (~5–12%).

| Metric | Value |

|---|---|

| Buyer revenue share | 35–45% |

| Public/research share (2024) | 38% |

| Cloud IaaS market (2025) | $680B |

| Cloud TCO reduction cited | 20–40% |

| IT budgets to OpEx (2024) | 62% |

| Margin compression vs commercial | 5–12% |

What You See Is What You Get

Quantum Porter's Five Forces Analysis

This preview shows the exact Quantum Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; the final, fully formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Quantum’s Porter's Five Forces snapshot highlights how supplier leverage, buyer power, competitive rivalry, threat of substitutes, and barriers to entry shape its strategic posture—revealing key pressures and potential vulnerabilities for investors and managers alike.

Suppliers Bargaining Power

Concentration of HDD and SSD Manufacturers

Quantum depends on a small set of HDD and SSD makers, which gives suppliers strong leverage because high-capacity media for unstructured data is specialized; top four vendors controlled about 78% of enterprise SSD/HDD shipments in 2025.

Supplier pricing power rose after 2024–25 semiconductor consolidation—major vendors increased ASPs (average selling prices) by ~12% YoY in H1 2025, squeezing margins for smaller hardware integrators like Quantum.

Long lead times (12–20 weeks) for high-capacity drives and limited alternative fabs raise switching costs and increase supply risk for Quantum, forcing reliance on vendor contracts and inventory buffers.

Dependency on LTO Tape Technology

Quantum depends on the LTO consortium for technology direction; as of 2025 the consortium includes IBM, HPE, and others who set roadmaps that Quantum must follow.

Only a handful of vendors produce LTO media and drive heads; supply concentration means a 1–3% rise in licensing or component costs can cut tape margins materially—Quantum reported 2024 gross margin on tape products near 22%.

This supplier concentration limits Quantum’s negotiating leverage, constraining price cuts for long-term preservation solutions and raising exposure to production delays and licensing shifts.

Specialized Semiconductor and Controller Supply

The shift to AI-driven metadata tagging and high-speed indexing needs advanced controllers and AI accelerators; 2025 market data shows top 5 silicon vendors (TSMC fabs plus Nvidia, Broadcom, Samsung foundry partners) control ~80% of advanced node capacity, concentrating supplier power.

Smartphone and automotive orders drove a 22% jump in 5nm+ wafer demand in 2024, so Quantum risks supply volatility and 10–25% premium pricing during peak cycles, squeezing margins unless it secures long-term supply agreements or pays wafer-priority premiums.

Proprietary Software Component Licensing

Quantum embeds third-party security and interoperability modules under multi-year licenses; these suppliers hold leverage via essential IP and renewal terms, and 2025 industry reports show enterprise software OEMs capturing 15–25% gross margin uplift from license renewals.

If a supplier hikes fees, Quantum faces either absorbing higher costs—compressing EBITDA—or removing features and losing clients; a 2024 vendor-concentration study found 40% of platforms rely on three or fewer critical vendors.

- Multi-year licenses concentrate supplier power

- Critical IP creates switching friction

- License fee hikes hit EBITDA or product scope

- 40% platforms depend on ≤3 key vendors

- Renewal margins typically add 15–25%

Global Logistics and Material Costs

Global logistics and material-cost swings leave Quantum exposed: chassis, PSUs, and cooling systems saw input-cost inflation of ~14% from 2020–2024, and average ocean freight rates remained 3x pre‑pandemic levels into 2024, raising BOM (bill of materials) costs materially.

Regionalized 2025 supply chains increased lead times by 25% and added 6–9% procurement premium versus global sourcing, while trade barriers (tariffs, export controls) raise supplier leverage.

- Input inflation ~14% (2020–2024)

- Ocean freight ~3x pre‑2019 rates

- Lead times +25% (regionalization)

- Procurement premium +6–9% (2025)

Supplier dominance, rising ASPs and constrained wafers threaten Quantum’s tape EBITDA

Suppliers hold strong leverage: top HDD/SSD vendors controlled ~78% shipments in 2025, ASPs rose ~12% YoY H1 2025, lead times 12–20 weeks, and 5nm+ wafer capacity concentrated (~80% control), so component/licensing hikes (1–3%) or license renewals (+15–25% margins) materially compress Quantum’s tape and appliance EBITDA.

| Metric | Value (2024–25) |

|---|---|

| Top SSD/HDD share | ~78% |

| ASPs change H1 2025 | +12% YoY |

| Drive lead times | 12–20 weeks |

| Advanced node capacity control | ~80% |

| Input inflation (2020–24) | ~14% |

| Ocean freight vs pre‑2019 | ~3x |

| Tape gross margin (Quantum 2024) | ~22% |

What is included in the product

Tailored Five Forces analysis for Quantum that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats—supported by industry data and strategic commentary for use in investor materials and strategy decks.

Quantum Porter's Five Forces condenses strategic pressure into a single, dynamic view—adjust force weights, swap scenarios, and export clean visuals for decks to speed confident decisions.

Customers Bargaining Power

Consolidation of Media and Entertainment Clients

Major media conglomerates account for roughly 35–45% of Quantum’s annual revenue, and recent mega-mergers (e.g., 2023–2024 deals) concentrate buying power, raising their negotiation leverage. Large buyers demand double-digit discounts and bespoke SLAs because they handle petabytes of content; switching to alternative storage or cloud architectures can save them 10–30% in TCO, so their growing scale significantly pressures Quantum’s pricing and contract terms.

Availability of Hyperscale Cloud Alternatives

Customers can shift unstructured workloads to AWS, Azure, or Google Cloud, giving them leverage; public cloud IaaS revenue hit about $680B in 2025, so buyers compare Quantum’s on‑prem/hybrid prices to that scale.

This alternative caps Quantum’s pricing power—enterprises cite cloud TCO reductions of 20–40% in 2024–25, so procurement teams push for lower on‑prem storage fees.

Ease of migration and cloud‑first policies make customers price‑sensitive: surveys show 58% of large firms favored cloud‑first terms in 2025 negotiations, raising churn risk if Quantum’s pricing exceeds cloud parity.

Low Switching Costs for Software-Defined Storage

The move to software-defined storage lets customers run Quantum’s management layer on commodity servers from Dell, HPE, or Supermicro, cutting hardware lock-in; IDC reported 2024 SDS deployments grew 18% YoY, reaching $9.6B, which raises buyer leverage.

Budget Constraints in Government and Research Sectors

These buyers use formal competitive tenders and RFPs, so vendors compete heavily on price and service levels; public procurement transparency (EU Open Contracting, US SAM) lets buyers benchmark offers and push for best performance-per-dollar.

That combination raises buyer bargaining power, often shrinking contract margins by 5–12% versus commercial deals.

- ~38% revenue from public/research (2024)

- Competitive tenders common—lowers prices

- Procurement transparency enables benchmarking

- Margins cut 5–12% vs commercial sales

Demand for Flexible Consumption Models

- 62% of IT budgets to OpEx (2024)

- As-a-service contracts +28% YoY (2024)

- Revenue timing delayed; vendor bears capacity risk

Cloud TCO cuts, mega‑buyers squeeze Quantum—double‑digit discounts, margin pressure

Major buyers (35–45% revenue) and 2023–24 mega‑mergers concentrate leverage, pushing double‑digit discounts; cloud alternatives (public cloud IaaS ~$680B in 2025) and reported cloud TCO cuts of 20–40% tighten Quantum’s pricing power, while 38% public/research mix and OpEx demand (62% IT budgets to OpEx in 2024) drive tendering, subscription pressure, and margin compression (~5–12%).

| Metric | Value |

|---|---|

| Buyer revenue share | 35–45% |

| Public/research share (2024) | 38% |

| Cloud IaaS market (2025) | $680B |

| Cloud TCO reduction cited | 20–40% |

| IT budgets to OpEx (2024) | 62% |

| Margin compression vs commercial | 5–12% |

What You See Is What You Get

Quantum Porter's Five Forces Analysis

This preview shows the exact Quantum Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; the final, fully formatted document is ready for download and use the moment you buy.