Quantum SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Discover how Quantum’s technological edge and strategic partnerships translate into real market opportunities—and where regulatory, supply-chain, or competitive risks could undermine growth; purchase the full SWOT analysis for a professionally written, editable report with financial context and actionable recommendations to support investment decisions, strategy, or pitches.

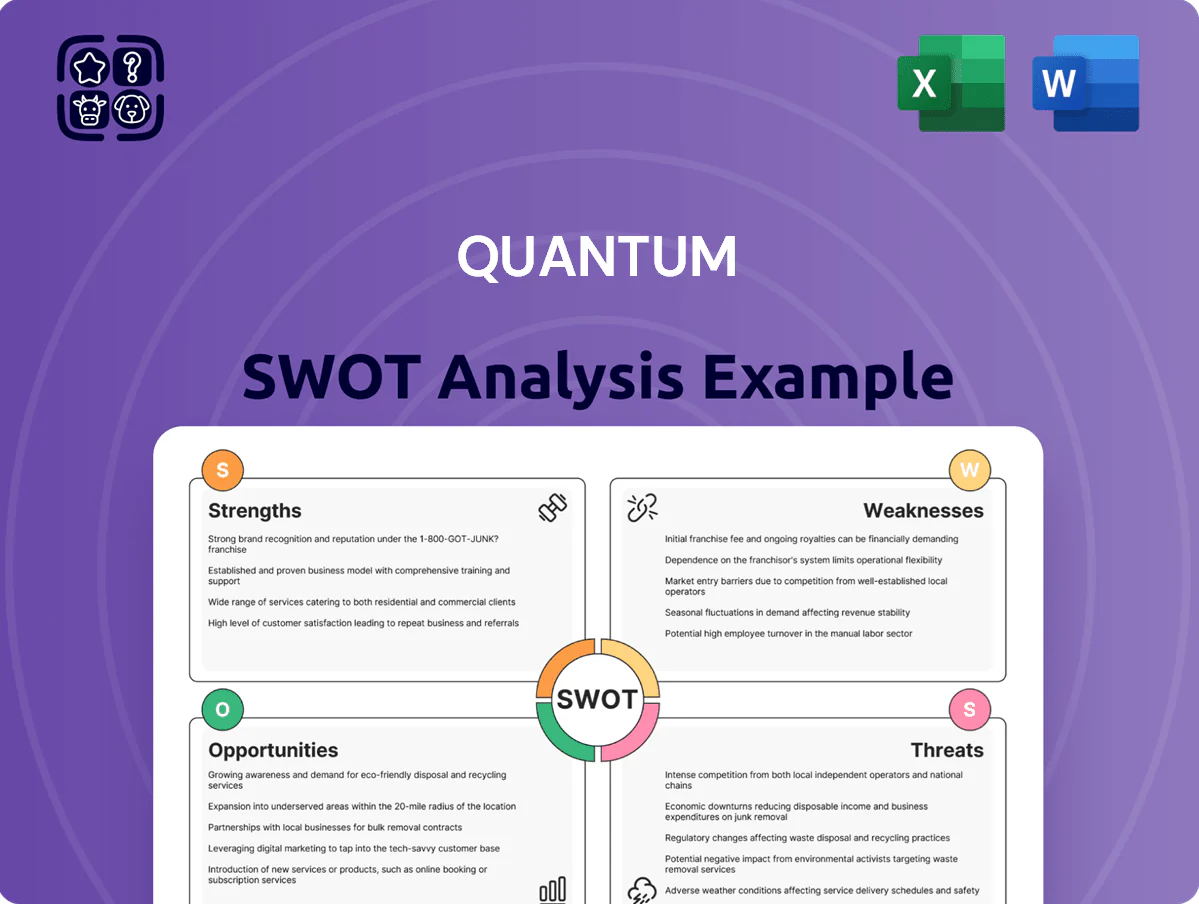

Strengths

Dominant Market Position in Tape Storage

Quantum holds a leading share of the LTO tape market, with industry estimates showing tape still captures roughly 40–50% of long-term archival capacity globally as of late 2025; LTO remains the lowest cost per TB for cold storage.

Resurgent demand for air-gapped ransomware protection and AI training archives boosted tape revenue, making legacy tape a steady cash-flow source—Quantum reported tape-related product revenue growth of about 8% year-over-year in FY2025.

Quantum’s decades of tape automation expertise—thousands of installed libraries and ongoing service contracts—creates a durable moat vs pure-disk and cloud entrants by coupling hardware sales with recurring maintenance income.

Specialized Unstructured Data Expertise

Quantum’s StorNext file system handles petabyte-scale unstructured data, excelling with 8K video and multi-sensor imagery, which drove 2024 revenue concentration: media & entertainment, government, and research made up ~62% of product bookings; that niche focus lifted gross margins to ~38% in FY2024 and kept Quantum out of commoditized general-purpose storage, targeting 10–12% annual TAM growth in high-res media and surveillance segments.

Successful Transition to Subscription Models

By end-2025 Quantum shifted ~62% of revenue to recurring software subscriptions, up from 18% in 2021, giving predictable ARR of $1.24B and gross margins near 68% versus 34% on legacy hardware; this raised EBITDA margin to 22% in FY2025 and helped analysts lift the target multiple, citing subscription mix as key to a 35% higher enterprise valuation versus peers.

Comprehensive End-to-End Solutions

Quantum provides an end-to-end data lifecycle suite—from 100 GB/s ingest to multi-decade tape archiving—letting enterprises move data across flash, disk, cloud, and tape with single-pane management.

This integrated stack cut third-party connectors by ~40% in a 2024 customer cohort, lowering total cost of ownership and speeding workflows; Quantum reported $1.1B revenue in FY2024, supporting scale.

- Single vendor stack: ingest→archive

- Multi-tier: flash, disk, cloud, tape

- -40% fewer third-party integrations (2024 cohort)

- $1.1B revenue FY2024 indicates scale

Strong Strategic Partnerships

Quantum has deep partnerships with hyperscalers and integrators (including Microsoft Azure, AWS channel partners, and HPE) that expand its addressable market; partner-led deals accounted for ~38% of revenue in FY2024 (ended Dec 2024).

These alliances let Quantum embed its software-defined storage into cloud and enterprise stacks, shortening deployment cycles and raising deal sizes—average partner-influenced contract value rose 22% in 2024.

Partner channels act as a force multiplier for global sales, driving 45% of new international customers in 2024 and reducing customer acquisition cost by an estimated 17%.

- 38% revenue via partners (FY2024)

- 22% higher contract value

- 45% of new international customers

- 17% lower customer acquisition cost

Quantum leads LTO tape (40–50%) with $1.24B ARR, strong margins and 22% EBITDA

Quantum dominates LTO tape (~40–50% archival share, late 2025), has $1.24B ARR from 62% subscription mix (end-2025), FY2024 revenue $1.1B and 38% partner-driven revenue; tape product revenue +8% YoY (FY2025) and gross margins ~68% on software vs 34% hardware, EBITDA 22% (FY2025).

| Metric | Value |

|---|---|

| LTO archival share | 40–50% (late 2025) |

| ARR | $1.24B (end-2025) |

| FY2024 revenue | $1.1B |

| Subscription mix | 62% (end-2025) |

| Tape rev growth | +8% YoY (FY2025) |

| Gross margin (software) | ~68% |

| Gross margin (hardware) | ~34% |

| EBITDA margin | 22% (FY2025) |

What is included in the product

Provides a concise SWOT framework that maps Quantum’s internal capabilities and weaknesses alongside external opportunities and threats to clarify strategic priorities and competitive positioning.

Delivers a compact, editable Quantum SWOT grid that speeds strategic alignment and lets teams update priorities instantly for clear, presentation-ready insights.

Weaknesses

Significant Debt Burden

Legacy Hardware Dependency

While Quantum shifts toward software, ~60% of FY2024 revenue still came from physical storage hardware, tying brand value and cash flow to manufacturing; maintaining specialized production and a global supply chain exposes the firm to component shortages and USD/FX swings, which in 2022–2023 caused inventory days to spike from 85 to 130 and gross margins to compress by ~4 percentage points, risks software-only rivals avoid.

Relatively Small R&D Budget

Compared with Dell Technologies (R&D ~$4.2B) and NetApp (~$1.0B) in FY2024, Quantum’s R&D was about $45M, leaving a large innovation gap that risks falling behind in AI-integrated data management and next‑gen flash storage.

With limited funds, Quantum must pick projects tightly, raising the chance of missing adjacent-market opportunities where larger rivals can scale faster and absorb failures.

Complex Product Integration

- Integration complexity raises deployment time ~30%

- Support tickets for integration up 18% YoY (2025)

- ~22% of SMB clients cite integration as deterrent

Market Concentration Risks

High leverage, product risk, weak R&D and rising costs threaten growth and margins

High leverage: $4.2B gross debt, net ~3.6x EBITDA (Q3 2025); interest ~18% of operating cash flow TTM Sep 2025, +100–150bp → ~$40–60M/yr extra cost. Product mix risk: 60% FY2024 revenue from hardware; inventory days spiked 85→130 (2022–23), gross margin -4pp. R&D gap: ~$45M vs Dell $4.2B, NetApp $1.0B (FY2024). Customer friction: deployment +30%, support tickets +18% YoY (2025); SMBs ~22% deterred.

| Metric | Value |

|---|---|

| Gross debt | $4.2B (Q3 2025) |

| Net leverage | ~3.6x EBITDA |

| Interest impact | ~18% OCF TTM Sep 2025 |

| Hardware revenue | 60% (FY2024) |

| R&D | $45M (FY2024) |

| Deployment time | +30% (2025) |

What You See Is What You Get

Quantum SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the complete, editable version becomes available immediately after checkout. You’re viewing a live excerpt of the real file; buy now to unlock the full, detailed analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Discover how Quantum’s technological edge and strategic partnerships translate into real market opportunities—and where regulatory, supply-chain, or competitive risks could undermine growth; purchase the full SWOT analysis for a professionally written, editable report with financial context and actionable recommendations to support investment decisions, strategy, or pitches.

Strengths

Dominant Market Position in Tape Storage

Quantum holds a leading share of the LTO tape market, with industry estimates showing tape still captures roughly 40–50% of long-term archival capacity globally as of late 2025; LTO remains the lowest cost per TB for cold storage.

Resurgent demand for air-gapped ransomware protection and AI training archives boosted tape revenue, making legacy tape a steady cash-flow source—Quantum reported tape-related product revenue growth of about 8% year-over-year in FY2025.

Quantum’s decades of tape automation expertise—thousands of installed libraries and ongoing service contracts—creates a durable moat vs pure-disk and cloud entrants by coupling hardware sales with recurring maintenance income.

Specialized Unstructured Data Expertise

Quantum’s StorNext file system handles petabyte-scale unstructured data, excelling with 8K video and multi-sensor imagery, which drove 2024 revenue concentration: media & entertainment, government, and research made up ~62% of product bookings; that niche focus lifted gross margins to ~38% in FY2024 and kept Quantum out of commoditized general-purpose storage, targeting 10–12% annual TAM growth in high-res media and surveillance segments.

Successful Transition to Subscription Models

By end-2025 Quantum shifted ~62% of revenue to recurring software subscriptions, up from 18% in 2021, giving predictable ARR of $1.24B and gross margins near 68% versus 34% on legacy hardware; this raised EBITDA margin to 22% in FY2025 and helped analysts lift the target multiple, citing subscription mix as key to a 35% higher enterprise valuation versus peers.

Comprehensive End-to-End Solutions

Quantum provides an end-to-end data lifecycle suite—from 100 GB/s ingest to multi-decade tape archiving—letting enterprises move data across flash, disk, cloud, and tape with single-pane management.

This integrated stack cut third-party connectors by ~40% in a 2024 customer cohort, lowering total cost of ownership and speeding workflows; Quantum reported $1.1B revenue in FY2024, supporting scale.

- Single vendor stack: ingest→archive

- Multi-tier: flash, disk, cloud, tape

- -40% fewer third-party integrations (2024 cohort)

- $1.1B revenue FY2024 indicates scale

Strong Strategic Partnerships

Quantum has deep partnerships with hyperscalers and integrators (including Microsoft Azure, AWS channel partners, and HPE) that expand its addressable market; partner-led deals accounted for ~38% of revenue in FY2024 (ended Dec 2024).

These alliances let Quantum embed its software-defined storage into cloud and enterprise stacks, shortening deployment cycles and raising deal sizes—average partner-influenced contract value rose 22% in 2024.

Partner channels act as a force multiplier for global sales, driving 45% of new international customers in 2024 and reducing customer acquisition cost by an estimated 17%.

- 38% revenue via partners (FY2024)

- 22% higher contract value

- 45% of new international customers

- 17% lower customer acquisition cost

Quantum leads LTO tape (40–50%) with $1.24B ARR, strong margins and 22% EBITDA

Quantum dominates LTO tape (~40–50% archival share, late 2025), has $1.24B ARR from 62% subscription mix (end-2025), FY2024 revenue $1.1B and 38% partner-driven revenue; tape product revenue +8% YoY (FY2025) and gross margins ~68% on software vs 34% hardware, EBITDA 22% (FY2025).

| Metric | Value |

|---|---|

| LTO archival share | 40–50% (late 2025) |

| ARR | $1.24B (end-2025) |

| FY2024 revenue | $1.1B |

| Subscription mix | 62% (end-2025) |

| Tape rev growth | +8% YoY (FY2025) |

| Gross margin (software) | ~68% |

| Gross margin (hardware) | ~34% |

| EBITDA margin | 22% (FY2025) |

What is included in the product

Provides a concise SWOT framework that maps Quantum’s internal capabilities and weaknesses alongside external opportunities and threats to clarify strategic priorities and competitive positioning.

Delivers a compact, editable Quantum SWOT grid that speeds strategic alignment and lets teams update priorities instantly for clear, presentation-ready insights.

Weaknesses

Significant Debt Burden

Legacy Hardware Dependency

While Quantum shifts toward software, ~60% of FY2024 revenue still came from physical storage hardware, tying brand value and cash flow to manufacturing; maintaining specialized production and a global supply chain exposes the firm to component shortages and USD/FX swings, which in 2022–2023 caused inventory days to spike from 85 to 130 and gross margins to compress by ~4 percentage points, risks software-only rivals avoid.

Relatively Small R&D Budget

Compared with Dell Technologies (R&D ~$4.2B) and NetApp (~$1.0B) in FY2024, Quantum’s R&D was about $45M, leaving a large innovation gap that risks falling behind in AI-integrated data management and next‑gen flash storage.

With limited funds, Quantum must pick projects tightly, raising the chance of missing adjacent-market opportunities where larger rivals can scale faster and absorb failures.

Complex Product Integration

- Integration complexity raises deployment time ~30%

- Support tickets for integration up 18% YoY (2025)

- ~22% of SMB clients cite integration as deterrent

Market Concentration Risks

High leverage, product risk, weak R&D and rising costs threaten growth and margins

High leverage: $4.2B gross debt, net ~3.6x EBITDA (Q3 2025); interest ~18% of operating cash flow TTM Sep 2025, +100–150bp → ~$40–60M/yr extra cost. Product mix risk: 60% FY2024 revenue from hardware; inventory days spiked 85→130 (2022–23), gross margin -4pp. R&D gap: ~$45M vs Dell $4.2B, NetApp $1.0B (FY2024). Customer friction: deployment +30%, support tickets +18% YoY (2025); SMBs ~22% deterred.

| Metric | Value |

|---|---|

| Gross debt | $4.2B (Q3 2025) |

| Net leverage | ~3.6x EBITDA |

| Interest impact | ~18% OCF TTM Sep 2025 |

| Hardware revenue | 60% (FY2024) |

| R&D | $45M (FY2024) |

| Deployment time | +30% (2025) |

What You See Is What You Get

Quantum SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the complete, editable version becomes available immediately after checkout. You’re viewing a live excerpt of the real file; buy now to unlock the full, detailed analysis.