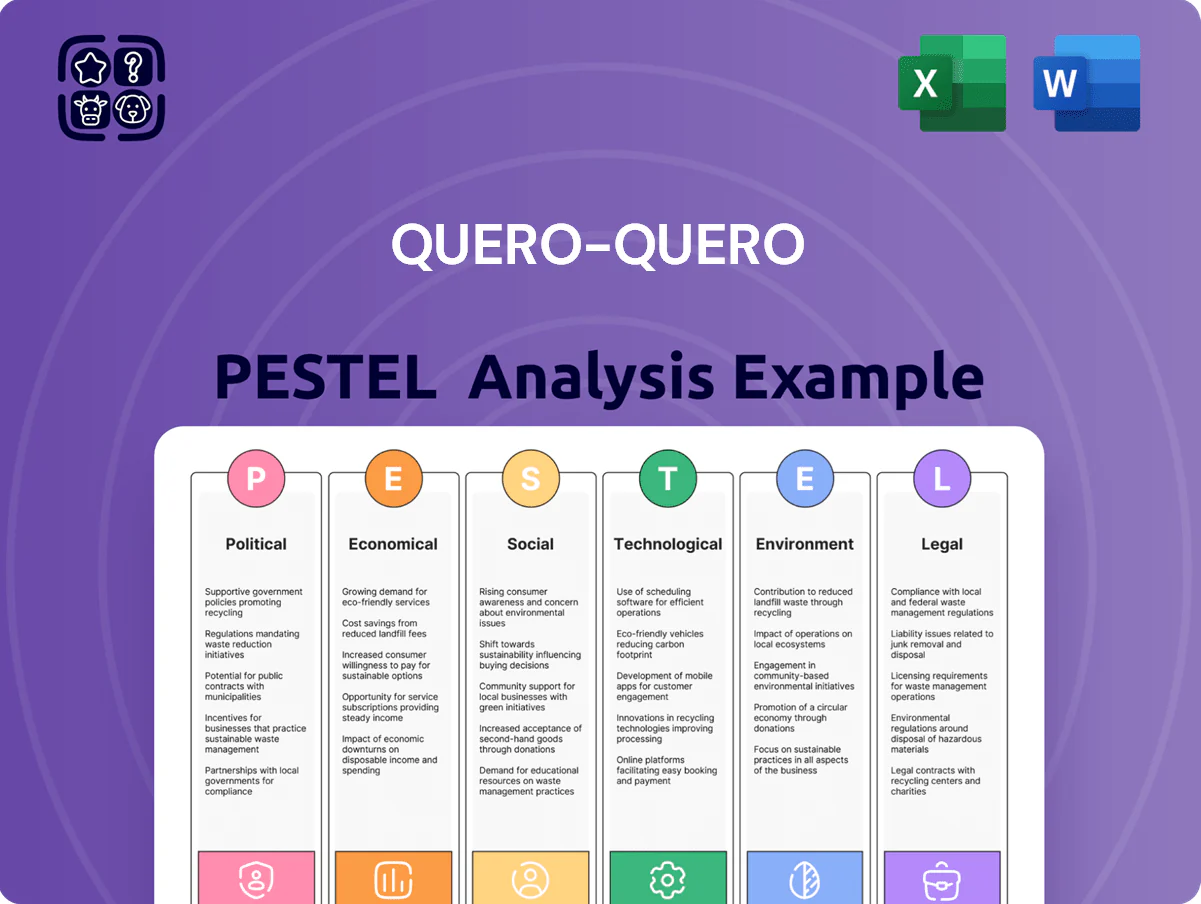

Quero-Quero PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Quickly grasp how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures shape Quero-Quero’s strategic outlook—our concise PESTLE preview highlights key risks and opportunities to inform your next move. Purchase the full PESTLE analysis for a complete, actionable breakdown with editable charts and recommendations, ready to use in investor decks, strategy sessions, or market research.

Political factors

Government Housing Incentives

The federal government's housing programs such as Minha Casa, Minha Vida—which funded roughly 1.2 million units between 2016–2023 and sustained R$15–20 billion annual credit flows in 2023–2024—remain a primary driver of construction material demand for Quero-Quero in small and medium towns.

These subsidies directly affect purchasing power of Quero-Quero’s core customers; in 2024 housing credit to low-income segments grew 8.5% YoY, supporting volume sales in building materials.

Any policy shift by late 2025—reductions in subsidy levels or tighter eligibility—could cut accessible demand by an estimated 10–25% for Quero-Quero’s building-materials segment, materially affecting sales volume.

Regional Tax Policy Stability

Trade Relations and Import Tariffs

Labor Market Regulations

Ongoing debates on labor flexibility and social security in Brazil could raise Quero-Quero’s labor costs; changes since 2024 include proposals to increase mandatory benefits and tighter rules on weekend/shift premiums, potentially adding 5–10% to wage bills for a retailer with ~1,200 stores and ~25,000 employees.

Legislative shifts on weekend hours or compulsory benefits directly impact overhead for service-heavy operations in small municipalities, where labor is 30–40% of operating expenses and margins are thin.

- Potential 5–10% rise in wage-related costs

- ~25,000 employees across ~1,200 stores exposed

- Labor = 30–40% of operating expenses in local stores

Infrastructure Investment Plans

Public investment in regional infrastructure and logistics—Brazil pledged BRL 200 billion for transport in 2024–2025—improves Quero-Quero’s supply chain efficiency by shortening lead times and reducing spoilage of construction inputs.

Political prioritization of roads in South and Midwest states cut trucking costs ~8–12% and average delivery times by 15% for heavy materials, lowering unit logistics cost for Quero-Quero.

Quero-Quero’s expansion plans are synchronized with government regional projects; aligning new depots with 2025 federal road upgrades captures higher market share where freight capacity grows.

- BRL 200bn federal transport plan (2024–25)

- 8–12% reduction in trucking costs in prioritized regions

- 15% faster deliveries for heavy construction materials

- Depot expansion timed to 2025 road upgrades

Housing stimulus boosts demand; tariffs, taxes and wages squeeze margins

Federal housing subsidies (Minha Casa, Minha Vida: ~1.2M units 2016–23; R$15–20bn annual credit 2023–24) and 8.5% YoY housing-credit growth in 2024 underpin demand; policy cuts could trim 10–25% volume. State ICMS (12–18%) and 2024 proposals +2pp raise costs; federal import tariffs lifted COGS 3.5–5% in 2024. Labor reforms may add 5–10% wage costs; BRL200bn transport plan (2024–25) cuts trucking costs 8–12%.

| Metric | Value/Impact |

|---|---|

| Housing units (2016–23) | ~1.2M |

| Annual housing credit | R$15–20bn (2023–24) |

| Housing-credit growth 2024 | +8.5% YoY |

| COGS impact (tariffs) | +3.5–5% |

| Wage cost risk | +5–10% |

| Transport plan | BRL200bn; trucking -8–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Quero-Quero, with each section backed by data and trends to reveal specific threats and opportunities for strategy and funding.

A concise, visually segmented Quero-Quero PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning during planning sessions.

Economic factors

Interest Rate and Credit Access

The SELIC rate, which averaged 12.75% in 2023 and was 11.75% by Dec 2024, drives consumer financing costs crucial to Quero-Quero’s credit-heavy sales model; higher SELIC raises monthly installments and compresses demand for long-term construction projects and high-ticket furniture.

Inflationary Pressure on Building Materials

Fluctuations in commodities—steel up ~18% and cement up ~12% in Brazil during 2024—push Quero-Quero to raise construction-material prices, compressing retail margins. Persistent inflation (Brazil CPI ~5.7% in 2024) has reduced real household discretionary spending, shifting demand from renovations toward essential maintenance. Quero-Quero’s inventory cost management during inflationary cycles directly affects gross margin volatility, with working-capital efficiency key to protecting 2024 margins.

Agricultural Sector Performance

The economic health of Southern Brazil is closely tied to agribusiness: in 2024 Rio Grande do Sul’s soybean and corn output rose 7.8% year‑on‑year, supporting rural incomes and boosting Quero‑Quero’s customer spending; soy prices averaged about US$520/ton in 2024, lifting farm cash flows. Conversely, climate shocks in 2023 cut regional ag GDP by an estimated 3.2%, immediately contracting local retail sales and store traffic for Quero‑Quero.

Consumer Debt and Delinquency Rates

- Household debt-to-income ~47% (2024)

- Retail credit delinquency 4.5% (Q4 2024)

- Unemployment ~8.0% (2024 avg)

- Implication: higher provisions, tighter approvals, moderated growth

Currency Exchange Rate Volatility

The BRL/USD rate rose ~12% in 2024 (from 5.20 to ~5.83), increasing import costs; imported white goods and electronics saw price pressure as global component prices rose ~8% YoY, raising replacement-cycle hesitancy among consumers.

Quero-Quero should pivot toward domestic appliances and source local suppliers, as domestic-sourced products can cut imported-cost exposure by an estimated 10–18%.

- BRL down ~12% in 2024 vs USD

- Global component costs +8% YoY

- Domestic sourcing reduces import exposure 10–18%

High rates, rising costs and weaker BRL squeeze demand—VerdeCard tightens underwriting

High SELIC (11.75% Dec 2024) and ~5.7% CPI in 2024 squeeze demand for financed purchases and compress margins; commodity cost rises (steel +18%, cement +12% 2024) raised construction and inventory costs. Household debt-to-income ~47% and retail delinquency 4.5% (Q4 2024) force tighter VerdeCard underwriting amid ~8.0% unemployment. BRL down ~12% (2024) increased import costs, justifying 10–18% savings via local sourcing.

| Metric | 2024 |

|---|---|

| SELIC | 11.75% |

| CPI | 5.7% |

| Household DTI | 47% |

| Retail delinquency | 4.5% |

| Unemployment | 8.0% |

| BRL change vs USD | -12% |

Preview Before You Purchase

Quero-Quero PESTLE Analysis

The preview shown here is the exact Quero-Quero PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll be able to download instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Quickly grasp how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures shape Quero-Quero’s strategic outlook—our concise PESTLE preview highlights key risks and opportunities to inform your next move. Purchase the full PESTLE analysis for a complete, actionable breakdown with editable charts and recommendations, ready to use in investor decks, strategy sessions, or market research.

Political factors

Government Housing Incentives

The federal government's housing programs such as Minha Casa, Minha Vida—which funded roughly 1.2 million units between 2016–2023 and sustained R$15–20 billion annual credit flows in 2023–2024—remain a primary driver of construction material demand for Quero-Quero in small and medium towns.

These subsidies directly affect purchasing power of Quero-Quero’s core customers; in 2024 housing credit to low-income segments grew 8.5% YoY, supporting volume sales in building materials.

Any policy shift by late 2025—reductions in subsidy levels or tighter eligibility—could cut accessible demand by an estimated 10–25% for Quero-Quero’s building-materials segment, materially affecting sales volume.

Regional Tax Policy Stability

Trade Relations and Import Tariffs

Labor Market Regulations

Ongoing debates on labor flexibility and social security in Brazil could raise Quero-Quero’s labor costs; changes since 2024 include proposals to increase mandatory benefits and tighter rules on weekend/shift premiums, potentially adding 5–10% to wage bills for a retailer with ~1,200 stores and ~25,000 employees.

Legislative shifts on weekend hours or compulsory benefits directly impact overhead for service-heavy operations in small municipalities, where labor is 30–40% of operating expenses and margins are thin.

- Potential 5–10% rise in wage-related costs

- ~25,000 employees across ~1,200 stores exposed

- Labor = 30–40% of operating expenses in local stores

Infrastructure Investment Plans

Public investment in regional infrastructure and logistics—Brazil pledged BRL 200 billion for transport in 2024–2025—improves Quero-Quero’s supply chain efficiency by shortening lead times and reducing spoilage of construction inputs.

Political prioritization of roads in South and Midwest states cut trucking costs ~8–12% and average delivery times by 15% for heavy materials, lowering unit logistics cost for Quero-Quero.

Quero-Quero’s expansion plans are synchronized with government regional projects; aligning new depots with 2025 federal road upgrades captures higher market share where freight capacity grows.

- BRL 200bn federal transport plan (2024–25)

- 8–12% reduction in trucking costs in prioritized regions

- 15% faster deliveries for heavy construction materials

- Depot expansion timed to 2025 road upgrades

Housing stimulus boosts demand; tariffs, taxes and wages squeeze margins

Federal housing subsidies (Minha Casa, Minha Vida: ~1.2M units 2016–23; R$15–20bn annual credit 2023–24) and 8.5% YoY housing-credit growth in 2024 underpin demand; policy cuts could trim 10–25% volume. State ICMS (12–18%) and 2024 proposals +2pp raise costs; federal import tariffs lifted COGS 3.5–5% in 2024. Labor reforms may add 5–10% wage costs; BRL200bn transport plan (2024–25) cuts trucking costs 8–12%.

| Metric | Value/Impact |

|---|---|

| Housing units (2016–23) | ~1.2M |

| Annual housing credit | R$15–20bn (2023–24) |

| Housing-credit growth 2024 | +8.5% YoY |

| COGS impact (tariffs) | +3.5–5% |

| Wage cost risk | +5–10% |

| Transport plan | BRL200bn; trucking -8–12% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Quero-Quero, with each section backed by data and trends to reveal specific threats and opportunities for strategy and funding.

A concise, visually segmented Quero-Quero PESTLE summary that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks and market positioning during planning sessions.

Economic factors

Interest Rate and Credit Access

The SELIC rate, which averaged 12.75% in 2023 and was 11.75% by Dec 2024, drives consumer financing costs crucial to Quero-Quero’s credit-heavy sales model; higher SELIC raises monthly installments and compresses demand for long-term construction projects and high-ticket furniture.

Inflationary Pressure on Building Materials

Fluctuations in commodities—steel up ~18% and cement up ~12% in Brazil during 2024—push Quero-Quero to raise construction-material prices, compressing retail margins. Persistent inflation (Brazil CPI ~5.7% in 2024) has reduced real household discretionary spending, shifting demand from renovations toward essential maintenance. Quero-Quero’s inventory cost management during inflationary cycles directly affects gross margin volatility, with working-capital efficiency key to protecting 2024 margins.

Agricultural Sector Performance

The economic health of Southern Brazil is closely tied to agribusiness: in 2024 Rio Grande do Sul’s soybean and corn output rose 7.8% year‑on‑year, supporting rural incomes and boosting Quero‑Quero’s customer spending; soy prices averaged about US$520/ton in 2024, lifting farm cash flows. Conversely, climate shocks in 2023 cut regional ag GDP by an estimated 3.2%, immediately contracting local retail sales and store traffic for Quero‑Quero.

Consumer Debt and Delinquency Rates

- Household debt-to-income ~47% (2024)

- Retail credit delinquency 4.5% (Q4 2024)

- Unemployment ~8.0% (2024 avg)

- Implication: higher provisions, tighter approvals, moderated growth

Currency Exchange Rate Volatility

The BRL/USD rate rose ~12% in 2024 (from 5.20 to ~5.83), increasing import costs; imported white goods and electronics saw price pressure as global component prices rose ~8% YoY, raising replacement-cycle hesitancy among consumers.

Quero-Quero should pivot toward domestic appliances and source local suppliers, as domestic-sourced products can cut imported-cost exposure by an estimated 10–18%.

- BRL down ~12% in 2024 vs USD

- Global component costs +8% YoY

- Domestic sourcing reduces import exposure 10–18%

High rates, rising costs and weaker BRL squeeze demand—VerdeCard tightens underwriting

High SELIC (11.75% Dec 2024) and ~5.7% CPI in 2024 squeeze demand for financed purchases and compress margins; commodity cost rises (steel +18%, cement +12% 2024) raised construction and inventory costs. Household debt-to-income ~47% and retail delinquency 4.5% (Q4 2024) force tighter VerdeCard underwriting amid ~8.0% unemployment. BRL down ~12% (2024) increased import costs, justifying 10–18% savings via local sourcing.

| Metric | 2024 |

|---|---|

| SELIC | 11.75% |

| CPI | 5.7% |

| Household DTI | 47% |

| Retail delinquency | 4.5% |

| Unemployment | 8.0% |

| BRL change vs USD | -12% |

Preview Before You Purchase

Quero-Quero PESTLE Analysis

The preview shown here is the exact Quero-Quero PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are the same file you’ll be able to download instantly after payment.