Quest Diagnostics Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

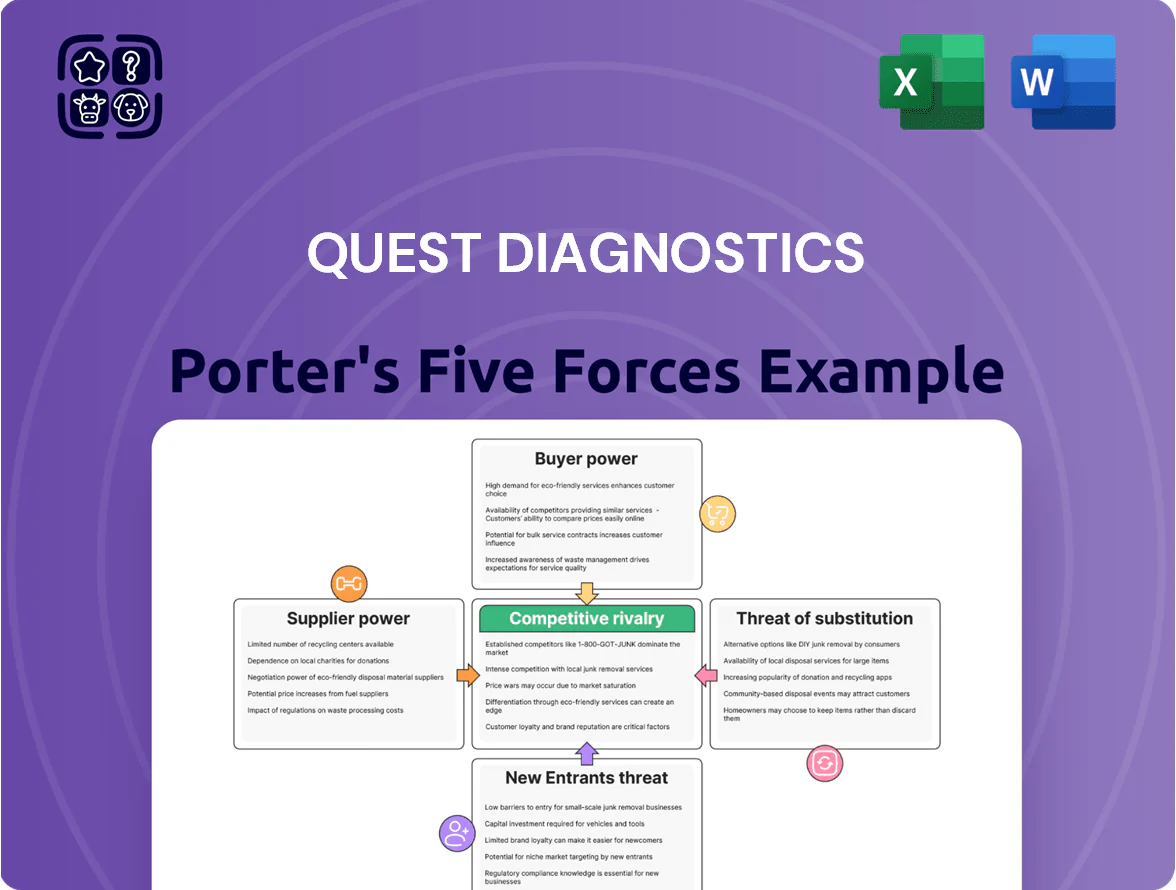

Quest Diagnostics faces moderate buyer power and high competitive rivalry amid consolidation and pricing pressure, while supplier power and threat of substitutes remain manageable due to scale and specialized services; regulatory and technological shifts add entry barriers and shape margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Quest Diagnostics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-Tech Equipment Vendors

The market for advanced diagnostic platforms and specialized reagents is concentrated among Roche, Danaher, and Thermo Fisher, which together held roughly 60–70% of the clinical diagnostics and reagents market in 2024. Quest Diagnostics depends on these vendors for PCR, NGS, and immunoassay platforms, so supplier concentration gives them pricing power and limited discounting. Switching vendors would likely require capital outlays of tens to hundreds of millions and months of staff retraining, raising effective switching costs. In 2024 Quest reported 6%–8% capital expenditure growth tied to lab automation upgrades.

Specialized Pathologist and Technician Labor

The limited supply of board-certified pathologists and skilled lab technicians forces Quest Diagnostics to compete tightly for talent, giving workers and unions strong bargaining power over pay and schedules.

By end-2025 healthcare labor shortages raised median clinical lab technologist wages about 8–12% year-over-year, and Quest reported rising labor costs that pressured 2025 operating margins.

Rising Costs of Logistics and Cold Chain Supply

Maintaining Quest Diagnostics’ 2,200+ patient service centers and nationwide courier network depends heavily on refrigerated transport and fuel; in 2024 US diesel averaged $4.05/gal, raising specimen logistics costs by an estimated 6–9% of transport spend. Because sample integrity is critical for diagnostic accuracy, Quest has little room to switch to lower‑cost carriers, giving specialized cold‑chain providers measurable bargaining power over prices and service terms.

Proprietary Genomic and Proteomic Technologies

As diagnostics shift to personalized medicine, Quest Diagnostics must license proprietary genomic and proteomic methods from biotech firms that hold patents on key biomarkers and sequencing techniques, driving up costs for high-margin specialized tests.

These suppliers exert exceptionally high bargaining power in niche areas—no legal or technical substitutes exist—so Quest faces pricing pressure and margin risk; in 2024, >30% of molecular test price increases were tied to patented reagents and IP licensing fees.

- High supplier power: patented biomarkers, no substitutes

- Impact: higher COGS and reduced margins on specialty tests

- 2024 data point: >30% of molecular test price rises linked to IP costs

Dependency on IT and Cloud Infrastructure Providers

Quest’s shift to AI-driven diagnostics ties it closely to major cloud providers such as AWS and Microsoft Azure, who in 2025 collectively control over 60% of global cloud IaaS market share; they supply the compute and encrypted storage needed for genomic datasets and PHI.

High regulatory and cybersecurity stakes (HIPAA, 2023 OCR fines still guiding 2025 practices) create switching costs — migrating petabytes of compressed genomic data and revalidating models can cost tens of millions and months of downtime, weakening Quest’s leverage in SLAs.

High supplier power: concentrated platforms, patent price hikes, cloud & labor squeeze

Supplier power is high: concentrated suppliers (Roche/Danaher/Thermo ~60–70% 2024), patented reagents driving >30% molecular test price rises (2024), cloud providers (AWS+Azure >60% IaaS 2025) and scarce lab talent (wages +8–12% YoY 2025) raise switching costs, COGS, and margin pressure.

| Factor | 2024–25 data |

|---|---|

| Platform concentration | 60–70% |

| IP-linked price rise | >30% |

| Cloud share | AWS+Azure >60% |

| Lab wages YoY | +8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Quest Diagnostics that uncovers competitive intensity, buyer and supplier power, substitution risks, and entry barriers to assess pricing pressure and long-term profitability.

One-sheet Porter's Five Forces for Quest Diagnostics—quickly spot competitive threats, supplier and buyer leverage, and regulatory risks to inform diagnostics strategy.

Customers Bargaining Power

Consolidation of Managed Care Organizations

Increased Leverage of Integrated Health Systems

Large hospital networks and integrated delivery systems now control ~40% of U.S. hospital beds after 2015–2023 consolidation, creating regional buyers that can internalize routine lab work or demand bulk pricing from Quest Diagnostics.

Many systems perform routine assays in-house and use Quest mainly for high-complexity send-out testing, cutting Quest’s margin mix and pressuring prices.

To retain contracts, Quest offers discounted rates, population-health analytics, and EHR integrations; in 2024 Quest reported about 18% of revenue tied to institutional clients, underscoring the leverage these systems wield.

Governmental Influence through Medicare and Medicaid

The Centers for Medicare and Medicaid Services (CMS) sets reimbursement via the Clinical Laboratory Fee Schedule, effectively fixing prices across the diagnostics market and constraining Quest Diagnostics’ price setting. The 2014 PAMA (Protecting Access to Medicare Act) and subsequent rate updates cut some routine test reimbursements by ~10–25%, lowering Medicare lab payments by roughly $390 million industry-wide in early years. Quest cannot negotiate CMS rates, so government buying exerts top-down bargaining power that directly pressures margins and revenue growth.

Consumerization of Healthcare and Patient Choice

Patients now act like informed consumers—51% of US insured adults had high-deductible plans in 2024, pushing choices toward lower out-of-pocket costs and convenient care, so Quest must compete on price transparency and patient experience.

By end-2025, 68% of patients expect digital results and same-day scheduling; that demand elevates individual patients as stronger stakeholders in the diagnostic value chain, shifting bargaining power away from labs.

- 51% US insured adults in high-deductible plans (2024)

- 68% expect digital results and seamless scheduling (2025)

- Quest faces pressure on price transparency and patient experience

Direct Contracting by Large Self-Insured Employers

Major corporations increasingly bypass insurers to contract directly with diagnostic providers for employee screening; by 2024 about 20% of Fortune 500 firms used direct contracting for health services, offering Quest high-volume prospects.

These self-insured buyers demand customized analytics and price cuts—contracts often require ≥15% cost savings and outcome-based KPIs tied to utilization and disease detection rates.

Quest must demonstrate clear ROI—showing per-employee savings (example: $120–$300 annually) and measurable clinical impact—to win and keep large accounts in this competitive market.

- ~20% Fortune 500 use direct contracting (2024)

- Contracts often require ≥15% cost cuts

- Expected per-employee savings $120–$300/yr

- Demand for customized reporting and ROI metrics

Buyer power crushes Quest margins—payers, hospitals, and patients force discounts & integrations

| Buyer | 2024–25 stat |

|---|---|

| Commercial lives (top payers) | ~70M |

| Hospital bed share | ~40% |

| High-deductible insured | 51% |

| Patients expecting digital | 68% |

| Fortune 500 direct-contract | ~20% |

What You See Is What You Get

Quest Diagnostics Porter's Five Forces Analysis

This preview shows the exact Quest Diagnostics Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: what you see is the complete, ready-to-use deliverable available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Quest Diagnostics faces moderate buyer power and high competitive rivalry amid consolidation and pricing pressure, while supplier power and threat of substitutes remain manageable due to scale and specialized services; regulatory and technological shifts add entry barriers and shape margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Quest Diagnostics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-Tech Equipment Vendors

The market for advanced diagnostic platforms and specialized reagents is concentrated among Roche, Danaher, and Thermo Fisher, which together held roughly 60–70% of the clinical diagnostics and reagents market in 2024. Quest Diagnostics depends on these vendors for PCR, NGS, and immunoassay platforms, so supplier concentration gives them pricing power and limited discounting. Switching vendors would likely require capital outlays of tens to hundreds of millions and months of staff retraining, raising effective switching costs. In 2024 Quest reported 6%–8% capital expenditure growth tied to lab automation upgrades.

Specialized Pathologist and Technician Labor

The limited supply of board-certified pathologists and skilled lab technicians forces Quest Diagnostics to compete tightly for talent, giving workers and unions strong bargaining power over pay and schedules.

By end-2025 healthcare labor shortages raised median clinical lab technologist wages about 8–12% year-over-year, and Quest reported rising labor costs that pressured 2025 operating margins.

Rising Costs of Logistics and Cold Chain Supply

Maintaining Quest Diagnostics’ 2,200+ patient service centers and nationwide courier network depends heavily on refrigerated transport and fuel; in 2024 US diesel averaged $4.05/gal, raising specimen logistics costs by an estimated 6–9% of transport spend. Because sample integrity is critical for diagnostic accuracy, Quest has little room to switch to lower‑cost carriers, giving specialized cold‑chain providers measurable bargaining power over prices and service terms.

Proprietary Genomic and Proteomic Technologies

As diagnostics shift to personalized medicine, Quest Diagnostics must license proprietary genomic and proteomic methods from biotech firms that hold patents on key biomarkers and sequencing techniques, driving up costs for high-margin specialized tests.

These suppliers exert exceptionally high bargaining power in niche areas—no legal or technical substitutes exist—so Quest faces pricing pressure and margin risk; in 2024, >30% of molecular test price increases were tied to patented reagents and IP licensing fees.

- High supplier power: patented biomarkers, no substitutes

- Impact: higher COGS and reduced margins on specialty tests

- 2024 data point: >30% of molecular test price rises linked to IP costs

Dependency on IT and Cloud Infrastructure Providers

Quest’s shift to AI-driven diagnostics ties it closely to major cloud providers such as AWS and Microsoft Azure, who in 2025 collectively control over 60% of global cloud IaaS market share; they supply the compute and encrypted storage needed for genomic datasets and PHI.

High regulatory and cybersecurity stakes (HIPAA, 2023 OCR fines still guiding 2025 practices) create switching costs — migrating petabytes of compressed genomic data and revalidating models can cost tens of millions and months of downtime, weakening Quest’s leverage in SLAs.

High supplier power: concentrated platforms, patent price hikes, cloud & labor squeeze

Supplier power is high: concentrated suppliers (Roche/Danaher/Thermo ~60–70% 2024), patented reagents driving >30% molecular test price rises (2024), cloud providers (AWS+Azure >60% IaaS 2025) and scarce lab talent (wages +8–12% YoY 2025) raise switching costs, COGS, and margin pressure.

| Factor | 2024–25 data |

|---|---|

| Platform concentration | 60–70% |

| IP-linked price rise | >30% |

| Cloud share | AWS+Azure >60% |

| Lab wages YoY | +8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Quest Diagnostics that uncovers competitive intensity, buyer and supplier power, substitution risks, and entry barriers to assess pricing pressure and long-term profitability.

One-sheet Porter's Five Forces for Quest Diagnostics—quickly spot competitive threats, supplier and buyer leverage, and regulatory risks to inform diagnostics strategy.

Customers Bargaining Power

Consolidation of Managed Care Organizations

Increased Leverage of Integrated Health Systems

Large hospital networks and integrated delivery systems now control ~40% of U.S. hospital beds after 2015–2023 consolidation, creating regional buyers that can internalize routine lab work or demand bulk pricing from Quest Diagnostics.

Many systems perform routine assays in-house and use Quest mainly for high-complexity send-out testing, cutting Quest’s margin mix and pressuring prices.

To retain contracts, Quest offers discounted rates, population-health analytics, and EHR integrations; in 2024 Quest reported about 18% of revenue tied to institutional clients, underscoring the leverage these systems wield.

Governmental Influence through Medicare and Medicaid

The Centers for Medicare and Medicaid Services (CMS) sets reimbursement via the Clinical Laboratory Fee Schedule, effectively fixing prices across the diagnostics market and constraining Quest Diagnostics’ price setting. The 2014 PAMA (Protecting Access to Medicare Act) and subsequent rate updates cut some routine test reimbursements by ~10–25%, lowering Medicare lab payments by roughly $390 million industry-wide in early years. Quest cannot negotiate CMS rates, so government buying exerts top-down bargaining power that directly pressures margins and revenue growth.

Consumerization of Healthcare and Patient Choice

Patients now act like informed consumers—51% of US insured adults had high-deductible plans in 2024, pushing choices toward lower out-of-pocket costs and convenient care, so Quest must compete on price transparency and patient experience.

By end-2025, 68% of patients expect digital results and same-day scheduling; that demand elevates individual patients as stronger stakeholders in the diagnostic value chain, shifting bargaining power away from labs.

- 51% US insured adults in high-deductible plans (2024)

- 68% expect digital results and seamless scheduling (2025)

- Quest faces pressure on price transparency and patient experience

Direct Contracting by Large Self-Insured Employers

Major corporations increasingly bypass insurers to contract directly with diagnostic providers for employee screening; by 2024 about 20% of Fortune 500 firms used direct contracting for health services, offering Quest high-volume prospects.

These self-insured buyers demand customized analytics and price cuts—contracts often require ≥15% cost savings and outcome-based KPIs tied to utilization and disease detection rates.

Quest must demonstrate clear ROI—showing per-employee savings (example: $120–$300 annually) and measurable clinical impact—to win and keep large accounts in this competitive market.

- ~20% Fortune 500 use direct contracting (2024)

- Contracts often require ≥15% cost cuts

- Expected per-employee savings $120–$300/yr

- Demand for customized reporting and ROI metrics

Buyer power crushes Quest margins—payers, hospitals, and patients force discounts & integrations

| Buyer | 2024–25 stat |

|---|---|

| Commercial lives (top payers) | ~70M |

| Hospital bed share | ~40% |

| High-deductible insured | 51% |

| Patients expecting digital | 68% |

| Fortune 500 direct-contract | ~20% |

What You See Is What You Get

Quest Diagnostics Porter's Five Forces Analysis

This preview shows the exact Quest Diagnostics Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: what you see is the complete, ready-to-use deliverable available instantly after payment.