Quhuo Boston Consulting Group Matrix

Unlock Strategic Clarity

Quhuo’s BCG Matrix snapshot reveals how its portfolio balances growth and market share—early signs of which offerings are primed to become Stars or risk slipping into Dogs. This concise preview highlights strategic pressure points and capital-allocation dilemmas that matter to investors and managers alike. Get the full BCG Matrix to access quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use strategic workbook. Purchase now for a Word report + Excel summary that cuts research time and guides decisive action.

Stars

EV Export and International Mobility Services

Quhuo has pushed into EV export and international mobility services, targeting a global EV market projected to reach $1.8 trillion by 2026; this leverages Quhuo’s logistics network to capture cross-border Chinese automotive tech demand.

Segment shows high growth—management forecasts revenue CAGR ~28% through 2026—and needs continued capex and compliance spend to handle tariffs, IMO rules, and local EV safety regs.

Priority: scale in SEA and Latin America where Quhuo targets 12–15% share by 2026, keeping Quhuo relevant in green energy trade.

Tech-Enabled Ride-Hailing Management

Quhuo's tech-enabled ride-hailing management is a Star: it holds ~30% share of China’s platform fleet management by 2025, servicing Didi and others and enabling sub-5% idle time and 15–20% higher driver utilization.

It supplies driver scheduling, real-time dispatch and vehicle ops; capex on AI/telematics is ongoing—R&D ~8% of segment revenue—and urbanization keeps demand rising ~6–8% CAGR to 2028.

Keeping market leadership is vital to turn this Star into a cash cow as unit margin expands with scale and software monetization; expect margin improvement of 5–8 pp with continued tech investment.

SaaS Workforce Solutions

SaaS Workforce Solutions is a Star: demand for workforce-management software rose ~28% CAGR 2020–25 as firms cut labor costs; Quhuo’s SaaS shows real-time tracking and analytics used by 12+ gig platforms and 45% of clients report 18% labor-cost savings within 6 months.

New Energy Vehicle NEV Leasing

New Energy Vehicle NEV Leasing sits as a Star in Quhuo’s BCG matrix: rapid NEV market growth (NEVs rose 65% YoY to 9.2M sales in China 2024) plus subsidies and the 2030 carbon neutrality push give Quhuo strong demand for leased vehicles supporting delivery and ride-hailing partners, boosting utilization and unit economics while infrastructure scales.

High capex needs—estimated CNY 2.1bn fleet investment in 2024—keep margins pressured despite strategic positioning; scaling fleet renewals and charging access are key.

- Market: China NEV sales 9.2M (2024), +65% YoY

- Support: govt subsidies and 2030 carbon neutrality policy

- Capex: ~CNY 2.1bn fleet spend (2024)

- Position: high growth, strong competitive edge while infra scales

Instant Retail Logistics Support

Quhuo fits Stars in the BCG matrix for Instant Retail Logistics Support: instant retail grew 45% year-over-year in China 2024 to a 1.2 trillion RMB market, and Quhuo’s worker-on-demand model is positioned to supply hyper-local grocery and pharma delivery labor at scale.

Capturing share needs heavy promotions—estimated CAC 120–180 RMB per active user—and targeted subsidies to outcompete local couriers; succeed and Quhuo could secure dominant share as instant retail stabilizes toward a mature 10–15% annual growth rate.

- Market size 1.2 trillion RMB (2024)

- Instant retail growth +45% YoY (2024)

- Estimated CAC 120–180 RMB/user

- Target long-term growth 10–15% annually

Quhuo’s Stars: Scale SEA/LatAm, monetise SaaS, secure charging to drive cash conversion

Quhuo’s Stars: EV exports/intl mobility, ride-hailing fleet ops, SaaS workforce, NEV leasing, instant retail logistics—each shows high growth (segment CAGRs 6–28%), strong market shares (ride-hailing ~30%), and heavy capex/R&D (NEV fleet ~CNY 2.1bn, R&D ~8% rev); priority: scale SEA/LatAm, expand software monetization, and secure charging/ops to convert Stars into cash cows.

| Segment | 2024–25 metric | Key spend |

|---|---|---|

| Ride-hailing ops | 30% share, sub-5% idle | R&D ~8% rev |

| NEV leasing | China NEV 9.2M (2024), +65% YoY | Fleet CNY 2.1bn (2024) |

| SaaS workforce | Demand +28% CAGR, 45% clients save 18% | Sales/marketing |

| Instant retail | Market RMB 1.2T (2024), +45% YoY | CAC 120–180 RMB |

What is included in the product

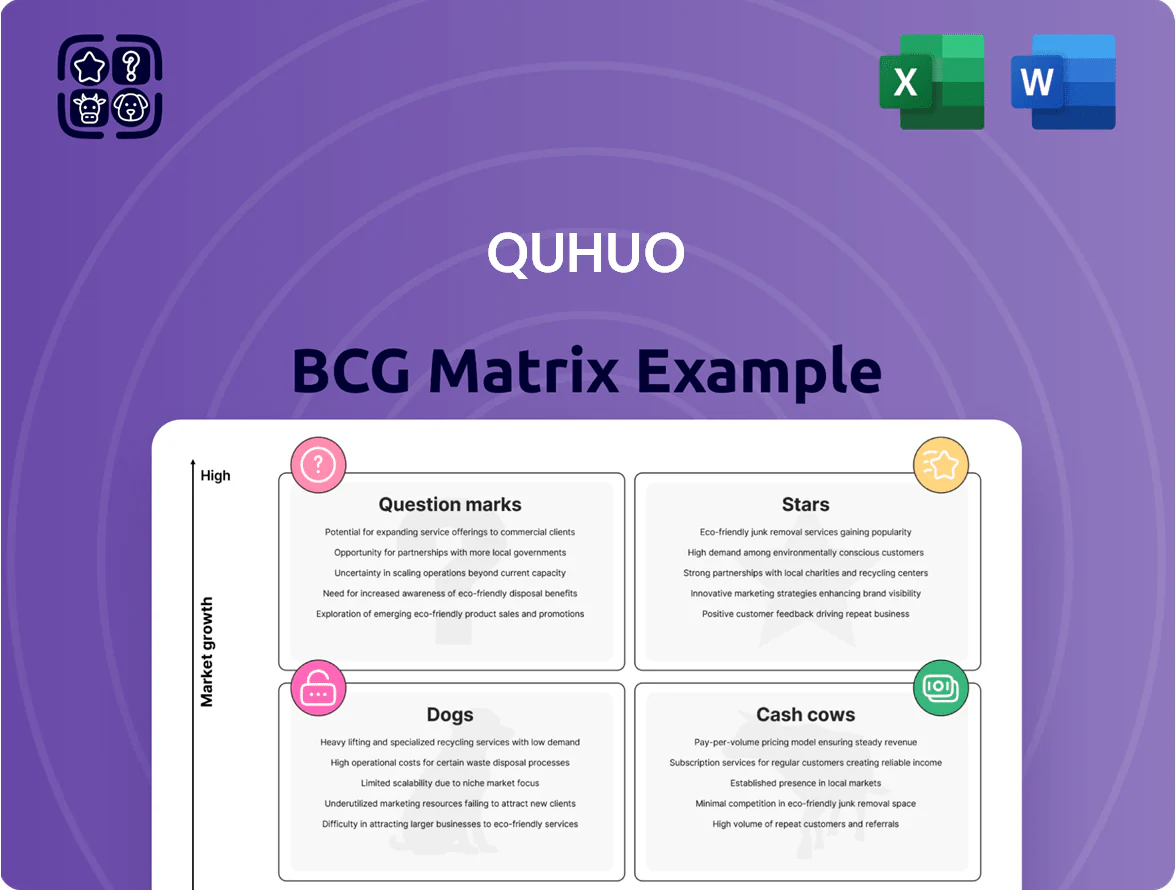

Comprehensive BCG Matrix review of Quhuo’s portfolio: strategic actions for Stars, Cash Cows, Question Marks, and Dogs, with trend context.

One-page BCG matrix placing Quhuo units into quadrants for quick strategic clarity.

Cash Cows

On-Demand Food Delivery Workforce Management

Food delivery remains Quhuo’s revenue cornerstone, capturing an estimated 30–35% of its 2025 gross revenue via partnerships with Meituan and Ele.me, keeping market share dominant in urban China.

The segment is mature: annual volume growth ~5–8% in 2024–25, enabling high operating margins (EBITDA margin ~22% in 2025) and steady cash generation.

With existing logistics and rider network in place, incremental capex is low, producing free cash flow that funded 60% of Quhuo’s 2025 R&D and new-venture spend.

Established Last-Mile Delivery Partnerships

Quhuo’s last-mile delivery for major e-commerce platforms runs at ~92% on-time in Tier 1–2 Chinese cities, with brand recognition driving >40% market share locally and single-digit annual volume growth, making it low-growth/high-penetration in BCG terms.

Low incremental marketing spend and long-term service contracts yield stable cash flow—delivery ops contributed RMB 1.2 billion in operating cash in 2024, so the unit is a reliable liquidity source.

The company prioritizes operational excellence—route optimization and 18% year-over-year cost-per-delivery reduction in 2023—so management can milk steady returns from these contracts.

Mature Urban Operational Hubs

Quhuo’s mature urban operational hubs in Shanghai, Beijing and Shenzhen run as low-cost centers, managing over 35,000 workers with standardized workflows that cut unit operating cost ~18% since 2020; they now prioritize margin expansion as on-demand labor penetration in tier-1 cities plateaued near 85% (2024 estimate).

Standardized Labor Compliance Services

Standardized Labor Compliance Services is a mature, high-market-share cash cow for Quhuo, serving multiple third-party platforms with deep local labor-law expertise across China.

The unit needs minimal capital reinvestment since it leverages established legal frameworks and compliance software, delivering predictable revenue—Quhuo reported ~RMB 120M annual recurring revenue from compliance in 2024.

Revenue stability cushions broader platform volatility: margin >40% and churn under 5% among enterprise clients in 2024, making it a reliable cash generator.

- High market share: dominant in China platforms

- Low capex: software + legal templates

- 2024 ARR ~RMB 120M; margin >40%

- Churn <5%; predictable cash flow

Long-Term Platform Maintenance Contracts

Quhuo holds multi-year platform maintenance contracts with major internet platforms (including contracts totaling ~RMB 420M annual recurring revenue as of 2025), delivering workforce stability; these deals show low revenue growth but very high client stickiness and >60% share of Quhuo’s platform-services revenue.

Predictable cash flows from these contracts support confident long-term planning—free cash conversion above 30% in 2024—while capex is minimal, limited to SLA-driven upkeep and staff retention.

- Multi-year contracts: core cash cows

- ~RMB 420M ARR (2025)

- >60% service revenue share

- Free cash conversion >30% (2024)

- Low growth, high stickiness, minimal investment

Quhuo’s cash-cow mix: 2025 revenue drivers, strong margins and cash generation

Quhuo cash cows: food delivery (30–35% of 2025 revenue; EBITDA ~22% in 2025; RMB 1.2B operating cash 2024), last-mile (92% on-time; >40% local share; low single-digit growth), compliance services (2024 ARR ~RMB 120M; margin >40%; churn <5%), platform maintenance (~RMB 420M ARR 2025; free cash conversion >30% 2024).

| Unit | Key metric |

|---|---|

| Food delivery | 30–35% rev; EBITDA 22%; RMB1.2B cash |

| Last-mile | 92% on-time; >40% share |

| Compliance | RMB120M ARR; margin>40% |

| Platform maintenance | RMB420M ARR; FCC>30% |

Preview = Final Product

Quhuo BCG Matrix

The file you're previewing is the exact Quhuo BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This preview mirrors the downloadable document, crafted by strategy professionals with clear positioning, growth/market-share insights, and actionable recommendations. Upon purchase the complete file is delivered instantly to your inbox for editing, printing, or presenting to stakeholders without any surprises or further edits needed.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Quhuo’s BCG Matrix snapshot reveals how its portfolio balances growth and market share—early signs of which offerings are primed to become Stars or risk slipping into Dogs. This concise preview highlights strategic pressure points and capital-allocation dilemmas that matter to investors and managers alike. Get the full BCG Matrix to access quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use strategic workbook. Purchase now for a Word report + Excel summary that cuts research time and guides decisive action.

Stars

EV Export and International Mobility Services

Quhuo has pushed into EV export and international mobility services, targeting a global EV market projected to reach $1.8 trillion by 2026; this leverages Quhuo’s logistics network to capture cross-border Chinese automotive tech demand.

Segment shows high growth—management forecasts revenue CAGR ~28% through 2026—and needs continued capex and compliance spend to handle tariffs, IMO rules, and local EV safety regs.

Priority: scale in SEA and Latin America where Quhuo targets 12–15% share by 2026, keeping Quhuo relevant in green energy trade.

Tech-Enabled Ride-Hailing Management

Quhuo's tech-enabled ride-hailing management is a Star: it holds ~30% share of China’s platform fleet management by 2025, servicing Didi and others and enabling sub-5% idle time and 15–20% higher driver utilization.

It supplies driver scheduling, real-time dispatch and vehicle ops; capex on AI/telematics is ongoing—R&D ~8% of segment revenue—and urbanization keeps demand rising ~6–8% CAGR to 2028.

Keeping market leadership is vital to turn this Star into a cash cow as unit margin expands with scale and software monetization; expect margin improvement of 5–8 pp with continued tech investment.

SaaS Workforce Solutions

SaaS Workforce Solutions is a Star: demand for workforce-management software rose ~28% CAGR 2020–25 as firms cut labor costs; Quhuo’s SaaS shows real-time tracking and analytics used by 12+ gig platforms and 45% of clients report 18% labor-cost savings within 6 months.

New Energy Vehicle NEV Leasing

New Energy Vehicle NEV Leasing sits as a Star in Quhuo’s BCG matrix: rapid NEV market growth (NEVs rose 65% YoY to 9.2M sales in China 2024) plus subsidies and the 2030 carbon neutrality push give Quhuo strong demand for leased vehicles supporting delivery and ride-hailing partners, boosting utilization and unit economics while infrastructure scales.

High capex needs—estimated CNY 2.1bn fleet investment in 2024—keep margins pressured despite strategic positioning; scaling fleet renewals and charging access are key.

- Market: China NEV sales 9.2M (2024), +65% YoY

- Support: govt subsidies and 2030 carbon neutrality policy

- Capex: ~CNY 2.1bn fleet spend (2024)

- Position: high growth, strong competitive edge while infra scales

Instant Retail Logistics Support

Quhuo fits Stars in the BCG matrix for Instant Retail Logistics Support: instant retail grew 45% year-over-year in China 2024 to a 1.2 trillion RMB market, and Quhuo’s worker-on-demand model is positioned to supply hyper-local grocery and pharma delivery labor at scale.

Capturing share needs heavy promotions—estimated CAC 120–180 RMB per active user—and targeted subsidies to outcompete local couriers; succeed and Quhuo could secure dominant share as instant retail stabilizes toward a mature 10–15% annual growth rate.

- Market size 1.2 trillion RMB (2024)

- Instant retail growth +45% YoY (2024)

- Estimated CAC 120–180 RMB/user

- Target long-term growth 10–15% annually

Quhuo’s Stars: Scale SEA/LatAm, monetise SaaS, secure charging to drive cash conversion

Quhuo’s Stars: EV exports/intl mobility, ride-hailing fleet ops, SaaS workforce, NEV leasing, instant retail logistics—each shows high growth (segment CAGRs 6–28%), strong market shares (ride-hailing ~30%), and heavy capex/R&D (NEV fleet ~CNY 2.1bn, R&D ~8% rev); priority: scale SEA/LatAm, expand software monetization, and secure charging/ops to convert Stars into cash cows.

| Segment | 2024–25 metric | Key spend |

|---|---|---|

| Ride-hailing ops | 30% share, sub-5% idle | R&D ~8% rev |

| NEV leasing | China NEV 9.2M (2024), +65% YoY | Fleet CNY 2.1bn (2024) |

| SaaS workforce | Demand +28% CAGR, 45% clients save 18% | Sales/marketing |

| Instant retail | Market RMB 1.2T (2024), +45% YoY | CAC 120–180 RMB |

What is included in the product

Comprehensive BCG Matrix review of Quhuo’s portfolio: strategic actions for Stars, Cash Cows, Question Marks, and Dogs, with trend context.

One-page BCG matrix placing Quhuo units into quadrants for quick strategic clarity.

Cash Cows

On-Demand Food Delivery Workforce Management

Food delivery remains Quhuo’s revenue cornerstone, capturing an estimated 30–35% of its 2025 gross revenue via partnerships with Meituan and Ele.me, keeping market share dominant in urban China.

The segment is mature: annual volume growth ~5–8% in 2024–25, enabling high operating margins (EBITDA margin ~22% in 2025) and steady cash generation.

With existing logistics and rider network in place, incremental capex is low, producing free cash flow that funded 60% of Quhuo’s 2025 R&D and new-venture spend.

Established Last-Mile Delivery Partnerships

Quhuo’s last-mile delivery for major e-commerce platforms runs at ~92% on-time in Tier 1–2 Chinese cities, with brand recognition driving >40% market share locally and single-digit annual volume growth, making it low-growth/high-penetration in BCG terms.

Low incremental marketing spend and long-term service contracts yield stable cash flow—delivery ops contributed RMB 1.2 billion in operating cash in 2024, so the unit is a reliable liquidity source.

The company prioritizes operational excellence—route optimization and 18% year-over-year cost-per-delivery reduction in 2023—so management can milk steady returns from these contracts.

Mature Urban Operational Hubs

Quhuo’s mature urban operational hubs in Shanghai, Beijing and Shenzhen run as low-cost centers, managing over 35,000 workers with standardized workflows that cut unit operating cost ~18% since 2020; they now prioritize margin expansion as on-demand labor penetration in tier-1 cities plateaued near 85% (2024 estimate).

Standardized Labor Compliance Services

Standardized Labor Compliance Services is a mature, high-market-share cash cow for Quhuo, serving multiple third-party platforms with deep local labor-law expertise across China.

The unit needs minimal capital reinvestment since it leverages established legal frameworks and compliance software, delivering predictable revenue—Quhuo reported ~RMB 120M annual recurring revenue from compliance in 2024.

Revenue stability cushions broader platform volatility: margin >40% and churn under 5% among enterprise clients in 2024, making it a reliable cash generator.

- High market share: dominant in China platforms

- Low capex: software + legal templates

- 2024 ARR ~RMB 120M; margin >40%

- Churn <5%; predictable cash flow

Long-Term Platform Maintenance Contracts

Quhuo holds multi-year platform maintenance contracts with major internet platforms (including contracts totaling ~RMB 420M annual recurring revenue as of 2025), delivering workforce stability; these deals show low revenue growth but very high client stickiness and >60% share of Quhuo’s platform-services revenue.

Predictable cash flows from these contracts support confident long-term planning—free cash conversion above 30% in 2024—while capex is minimal, limited to SLA-driven upkeep and staff retention.

- Multi-year contracts: core cash cows

- ~RMB 420M ARR (2025)

- >60% service revenue share

- Free cash conversion >30% (2024)

- Low growth, high stickiness, minimal investment

Quhuo’s cash-cow mix: 2025 revenue drivers, strong margins and cash generation

Quhuo cash cows: food delivery (30–35% of 2025 revenue; EBITDA ~22% in 2025; RMB 1.2B operating cash 2024), last-mile (92% on-time; >40% local share; low single-digit growth), compliance services (2024 ARR ~RMB 120M; margin >40%; churn <5%), platform maintenance (~RMB 420M ARR 2025; free cash conversion >30% 2024).

| Unit | Key metric |

|---|---|

| Food delivery | 30–35% rev; EBITDA 22%; RMB1.2B cash |

| Last-mile | 92% on-time; >40% share |

| Compliance | RMB120M ARR; margin>40% |

| Platform maintenance | RMB420M ARR; FCC>30% |

Preview = Final Product

Quhuo BCG Matrix

The file you're previewing is the exact Quhuo BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This preview mirrors the downloadable document, crafted by strategy professionals with clear positioning, growth/market-share insights, and actionable recommendations. Upon purchase the complete file is delivered instantly to your inbox for editing, printing, or presenting to stakeholders without any surprises or further edits needed.