Radware Ltd. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

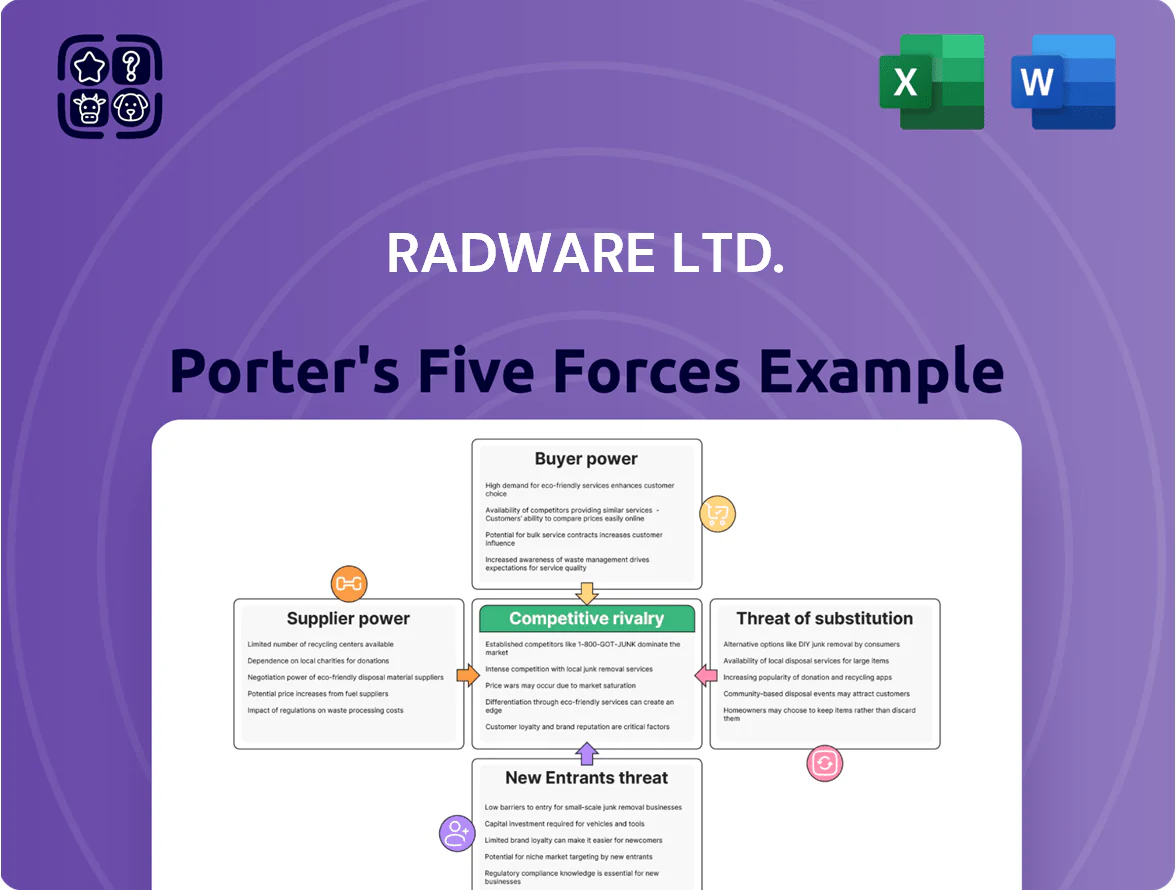

Radware operates in a competitive, technology-driven cybersecurity and application delivery market where strong supplier relationships, moderate buyer bargaining power, and rapid innovation shape margins and growth.

Threats from agile new entrants and cloud-native substitutes increase competitive intensity, while Radware’s differentiated solutions and channel partnerships support defensibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Radware Ltd. ’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Hardware Component Standardization

Radware relies on third-party manufacturers for standard components like CPUs and DDR memory; global suppliers such as Intel, AMD, Samsung, and SK Hynix produced over 90% of those markets in 2024, so no single vendor controls supply.

Commoditization means Radware can switch suppliers if prices rise; in 2024 server CPU spot prices fell ~5% YoY and DRAM contract prices were down ~12%, giving Radware negotiating leverage and limited supplier power.

Cloud Infrastructure Dependence

As Radware shifts toward cloud-native SaaS, dependency on AWS, Microsoft Azure, and Google Cloud grows; in 2024 hyperscalers held ~65% of global cloud IaaS/PaaS market, giving them price and integration leverage. Technical coupling and data egress fees raise switching costs—estimates show multi-cloud migration can cost 5–20% of annual cloud spend—creating supplier stickiness Radware must actively negotiate and architect around.

Specialized Cybersecurity Talent

The primary resource for Radware Ltd is its specialized developers and security researchers; global cybersecurity roles grew 32% from 2019–2024 and demand outpaces supply, giving these employees strong bargaining power over pay and remote/flex terms. Radware reported R&D expenses of $64.7m in FY2024, so it must keep investing in retention, upskilling, and compensation to sustain innovation and reduce costly turnover.

Proprietary Software Licensing

Radware develops much of its core tech but uses third-party libraries and security feeds; niche IP providers can pressure via licensing fees and renewal terms—vendor concentration in threat intelligence can raise costs up to mid-single-digit millions annually for enterprise vendors (2024 market patterns).

Diverse open-source alternatives (e.g., Suricata, OpenSSL) and multiple commercial feeds limit supplier leverage, keeping switching costs and margin impact moderate.

- Third-party feeds can cost millions yearly

- Open-source reduces dependence

- License renewals create periodic negotiating points

- Supplier power is present but contained

Global Logistics and Assembly Partners

Radware outsources assembly of Application Delivery Controllers and security appliances to contract manufacturers, tapping global EMS firms to scale production while keeping fixed costs low.

Because electronics manufacturing services are competitive—top 10 EMS firms held roughly 45% global market share in 2024—individual suppliers have limited leverage, letting Radware negotiate favorable pricing and SLAs by threatening to switch vendors.

This sourcing flexibility reduces supplier power but raises supply-chain risk: semiconductor shortages in 2021–22 showed how component constraints can still spike costs and lead times.

- Uses EMS partners for scale and lower fixed costs

- Top EMS firms ~45% market share in 2024 → low individual bargaining power

- Can renegotiate terms by switching vendors

- Component shortages remain a key risk

Moderate supplier power: concentrated CPUs/DRAM, hyperscaler influence, rising cyber costs

Supplier power is moderate: commodity components (CPUs/DRAM) give Radware switching leverage—Intel/AMD/Samsung/SK Hynix >90% share in 2024—while hyperscalers (AWS/Azure/GCP ~65% IaaS/PaaS share in 2024) and scarce cybersecurity talent raise costs and stickiness; FY2024 R&D $64.7m. Niche feeds can cost mid-single-digit millions; EMS top‑10 ~45% share, limiting EMS leverage.

| Item | 2024 data |

|---|---|

| CPU/DRAM supplier concentration | >90% |

| Hyperscaler IaaS/PaaS share | ~65% |

| DRAM/CPU price trend | DRAM -12% YoY, CPU spot -5% YoY |

| R&D expense (Radware FY2024) | $64.7m |

| Top‑10 EMS market share | ~45% |

| Threat‑feed cost | Mid‑single‑digit $m/year |

What is included in the product

Tailored exclusively for Radware Ltd., this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and disruptive threats shaping its cybersecurity and application delivery market positioning.

A concise Porter's Five Forces snapshot for Radware Ltd.—instantly highlights competitive intensity, supplier/customer leverage, threat of substitutes, and barriers to entry to speed strategic decisions.

Customers Bargaining Power

High Switching Costs for Enterprises

Large enterprise clients and service providers often embed Radware Ltd. (RADW) appliances and cloud WAF/DDOS controls into core networks and security stacks; Radware reported 2024 enterprise ARR growth of 11%, showing sticky contracts. Migrating vendors risks multi-week downtime and retraining costs—IDC estimates enterprise security migrations average 6–12 weeks and $150k–$500k in direct costs. This technical lock-in trims customers’ bargaining power at renewals.

Availability of Competitive Alternatives

Customers face many alternatives to Radware in DDoS protection and application delivery controllers, including F5 Networks, Akamai Technologies, and Cloudflare, with the enterprise DDoS market projected at $3.6B in 2025 (IDC). High vendor choice lets buyers negotiate aggressively; procurement teams often run RFIs that cut prices 10–25% in RFPs. Clear feature/pricing transparency in cybersecurity marketplaces further strengthens buyer leverage.

Consolidation of Service Providers

Consolidation among telcos and ISPs has shrunk buyers to a handful of high-volume accounts; the top 10 global carriers now represent an estimated 40–50% of enterprise traffic demand, so they can extract steep volume discounts from Radware Ltd. (RDWR) and push for custom roadmaps. In 2024 Radware reported large-account deals making up roughly 35% of product revenue, which means single customers can sway pricing and product priorities. This concentration raises negotiation leverage and strategic exposure for Radware.

SaaS and Subscription Model Flexibility

The shift to OpEx SaaS lets customers avoid CapEx hardware buys, increasing switching leverage versus Radware’s on-prem appliances; global SaaS security spending rose ~18% in 2024 to $46B, boosting buyer options.

Shorter subscriptions and easier exits mean customers renegotiate more often—Radware reported ~40% recurring revenue in FY2024, so retention pressure is constant.

Radware must prove ROI each renewal to keep churn low; industry median SaaS gross retention was ~92% in 2024, a target benchmark.

- OpEx model increases customer bargaining

- 2024 SaaS security spend ~$46B (up 18%)

- Radware FY2024 ~40% recurring revenue

- Industry gross retention ~92% (2024)

Price Sensitivity in Mid-Market Segments

Mid-market customers show high price sensitivity, often favoring lower-cost cloud-native security from ISPs or cloud hosts; Radware reported 2024 revenue of $268m, with cloud security growing 18% YoY, so aggressive pricing risks losing this segment.

Radware must balance premium pricing and modular offerings—e.g., tiered cloud modules under $1k/month—to compete while preserving margins; migration risk rises as cloud host native protections improve.

- Mid-market cost-driven; choose host/ISP bundles

- Radware 2024 revenue $268m; cloud +18% YoY

- Offer tiered pricing (~$1k/mo) to win share

- Risk: cloud-native feature parity fuels churn

Radware: Sticky ARR vs. SaaS Shift—High Migration Costs, Strong Buyer Leverage

Customers hold moderate-to-high bargaining power: technical lock-in (6–12 week migrations, $150k–$500k) and Radware’s sticky enterprise ARR (+11% 2024) reduce leverage, but wide vendor choice (F5, Akamai, Cloudflare), concentrated big buyers (top carriers = 40–50% demand), OpEx SaaS shift ($46B security SaaS, +18% 2024), and Radware’s 40% recurring revenue raise negotiation pressure; retention target ~92% gross.

| Metric | Value |

|---|---|

| Radware revenue 2024 | $268m |

| Cloud growth 2024 | +18% YoY |

| Enterprise ARR growth 2024 | +11% |

| Security SaaS spend 2024 | $46B (+18%) |

| Migration cost/time | $150k–$500k; 6–12 weeks |

| Recurr. revenue share FY2024 | ~40% |

| Industry gross retention (2024) | ~92% |

What You See Is What You Get

Radware Ltd. Porter's Five Forces Analysis

This preview shows the exact Radware Ltd. Porter’s Five Forces analysis you'll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for use.

You're looking at the same professionally written document that will be available for instant download once you complete your purchase, with complete assessments of rivalry, supplier and buyer power, barriers to entry, and threat of substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Radware operates in a competitive, technology-driven cybersecurity and application delivery market where strong supplier relationships, moderate buyer bargaining power, and rapid innovation shape margins and growth.

Threats from agile new entrants and cloud-native substitutes increase competitive intensity, while Radware’s differentiated solutions and channel partnerships support defensibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Radware Ltd. ’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Hardware Component Standardization

Radware relies on third-party manufacturers for standard components like CPUs and DDR memory; global suppliers such as Intel, AMD, Samsung, and SK Hynix produced over 90% of those markets in 2024, so no single vendor controls supply.

Commoditization means Radware can switch suppliers if prices rise; in 2024 server CPU spot prices fell ~5% YoY and DRAM contract prices were down ~12%, giving Radware negotiating leverage and limited supplier power.

Cloud Infrastructure Dependence

As Radware shifts toward cloud-native SaaS, dependency on AWS, Microsoft Azure, and Google Cloud grows; in 2024 hyperscalers held ~65% of global cloud IaaS/PaaS market, giving them price and integration leverage. Technical coupling and data egress fees raise switching costs—estimates show multi-cloud migration can cost 5–20% of annual cloud spend—creating supplier stickiness Radware must actively negotiate and architect around.

Specialized Cybersecurity Talent

The primary resource for Radware Ltd is its specialized developers and security researchers; global cybersecurity roles grew 32% from 2019–2024 and demand outpaces supply, giving these employees strong bargaining power over pay and remote/flex terms. Radware reported R&D expenses of $64.7m in FY2024, so it must keep investing in retention, upskilling, and compensation to sustain innovation and reduce costly turnover.

Proprietary Software Licensing

Radware develops much of its core tech but uses third-party libraries and security feeds; niche IP providers can pressure via licensing fees and renewal terms—vendor concentration in threat intelligence can raise costs up to mid-single-digit millions annually for enterprise vendors (2024 market patterns).

Diverse open-source alternatives (e.g., Suricata, OpenSSL) and multiple commercial feeds limit supplier leverage, keeping switching costs and margin impact moderate.

- Third-party feeds can cost millions yearly

- Open-source reduces dependence

- License renewals create periodic negotiating points

- Supplier power is present but contained

Global Logistics and Assembly Partners

Radware outsources assembly of Application Delivery Controllers and security appliances to contract manufacturers, tapping global EMS firms to scale production while keeping fixed costs low.

Because electronics manufacturing services are competitive—top 10 EMS firms held roughly 45% global market share in 2024—individual suppliers have limited leverage, letting Radware negotiate favorable pricing and SLAs by threatening to switch vendors.

This sourcing flexibility reduces supplier power but raises supply-chain risk: semiconductor shortages in 2021–22 showed how component constraints can still spike costs and lead times.

- Uses EMS partners for scale and lower fixed costs

- Top EMS firms ~45% market share in 2024 → low individual bargaining power

- Can renegotiate terms by switching vendors

- Component shortages remain a key risk

Moderate supplier power: concentrated CPUs/DRAM, hyperscaler influence, rising cyber costs

Supplier power is moderate: commodity components (CPUs/DRAM) give Radware switching leverage—Intel/AMD/Samsung/SK Hynix >90% share in 2024—while hyperscalers (AWS/Azure/GCP ~65% IaaS/PaaS share in 2024) and scarce cybersecurity talent raise costs and stickiness; FY2024 R&D $64.7m. Niche feeds can cost mid-single-digit millions; EMS top‑10 ~45% share, limiting EMS leverage.

| Item | 2024 data |

|---|---|

| CPU/DRAM supplier concentration | >90% |

| Hyperscaler IaaS/PaaS share | ~65% |

| DRAM/CPU price trend | DRAM -12% YoY, CPU spot -5% YoY |

| R&D expense (Radware FY2024) | $64.7m |

| Top‑10 EMS market share | ~45% |

| Threat‑feed cost | Mid‑single‑digit $m/year |

What is included in the product

Tailored exclusively for Radware Ltd., this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and disruptive threats shaping its cybersecurity and application delivery market positioning.

A concise Porter's Five Forces snapshot for Radware Ltd.—instantly highlights competitive intensity, supplier/customer leverage, threat of substitutes, and barriers to entry to speed strategic decisions.

Customers Bargaining Power

High Switching Costs for Enterprises

Large enterprise clients and service providers often embed Radware Ltd. (RADW) appliances and cloud WAF/DDOS controls into core networks and security stacks; Radware reported 2024 enterprise ARR growth of 11%, showing sticky contracts. Migrating vendors risks multi-week downtime and retraining costs—IDC estimates enterprise security migrations average 6–12 weeks and $150k–$500k in direct costs. This technical lock-in trims customers’ bargaining power at renewals.

Availability of Competitive Alternatives

Customers face many alternatives to Radware in DDoS protection and application delivery controllers, including F5 Networks, Akamai Technologies, and Cloudflare, with the enterprise DDoS market projected at $3.6B in 2025 (IDC). High vendor choice lets buyers negotiate aggressively; procurement teams often run RFIs that cut prices 10–25% in RFPs. Clear feature/pricing transparency in cybersecurity marketplaces further strengthens buyer leverage.

Consolidation of Service Providers

Consolidation among telcos and ISPs has shrunk buyers to a handful of high-volume accounts; the top 10 global carriers now represent an estimated 40–50% of enterprise traffic demand, so they can extract steep volume discounts from Radware Ltd. (RDWR) and push for custom roadmaps. In 2024 Radware reported large-account deals making up roughly 35% of product revenue, which means single customers can sway pricing and product priorities. This concentration raises negotiation leverage and strategic exposure for Radware.

SaaS and Subscription Model Flexibility

The shift to OpEx SaaS lets customers avoid CapEx hardware buys, increasing switching leverage versus Radware’s on-prem appliances; global SaaS security spending rose ~18% in 2024 to $46B, boosting buyer options.

Shorter subscriptions and easier exits mean customers renegotiate more often—Radware reported ~40% recurring revenue in FY2024, so retention pressure is constant.

Radware must prove ROI each renewal to keep churn low; industry median SaaS gross retention was ~92% in 2024, a target benchmark.

- OpEx model increases customer bargaining

- 2024 SaaS security spend ~$46B (up 18%)

- Radware FY2024 ~40% recurring revenue

- Industry gross retention ~92% (2024)

Price Sensitivity in Mid-Market Segments

Mid-market customers show high price sensitivity, often favoring lower-cost cloud-native security from ISPs or cloud hosts; Radware reported 2024 revenue of $268m, with cloud security growing 18% YoY, so aggressive pricing risks losing this segment.

Radware must balance premium pricing and modular offerings—e.g., tiered cloud modules under $1k/month—to compete while preserving margins; migration risk rises as cloud host native protections improve.

- Mid-market cost-driven; choose host/ISP bundles

- Radware 2024 revenue $268m; cloud +18% YoY

- Offer tiered pricing (~$1k/mo) to win share

- Risk: cloud-native feature parity fuels churn

Radware: Sticky ARR vs. SaaS Shift—High Migration Costs, Strong Buyer Leverage

Customers hold moderate-to-high bargaining power: technical lock-in (6–12 week migrations, $150k–$500k) and Radware’s sticky enterprise ARR (+11% 2024) reduce leverage, but wide vendor choice (F5, Akamai, Cloudflare), concentrated big buyers (top carriers = 40–50% demand), OpEx SaaS shift ($46B security SaaS, +18% 2024), and Radware’s 40% recurring revenue raise negotiation pressure; retention target ~92% gross.

| Metric | Value |

|---|---|

| Radware revenue 2024 | $268m |

| Cloud growth 2024 | +18% YoY |

| Enterprise ARR growth 2024 | +11% |

| Security SaaS spend 2024 | $46B (+18%) |

| Migration cost/time | $150k–$500k; 6–12 weeks |

| Recurr. revenue share FY2024 | ~40% |

| Industry gross retention (2024) | ~92% |

What You See Is What You Get

Radware Ltd. Porter's Five Forces Analysis

This preview shows the exact Radware Ltd. Porter’s Five Forces analysis you'll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for use.

You're looking at the same professionally written document that will be available for instant download once you complete your purchase, with complete assessments of rivalry, supplier and buyer power, barriers to entry, and threat of substitutes.