Rajesh Exports PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, currency cycles, and technology trends are reshaping Rajesh Exports’ competitive edge—our concise PESTLE highlights key risks and opportunities for investors and strategists; purchase the full analysis to access actionable insights, editable charts, and a ready-to-use roadmap for smarter decisions.

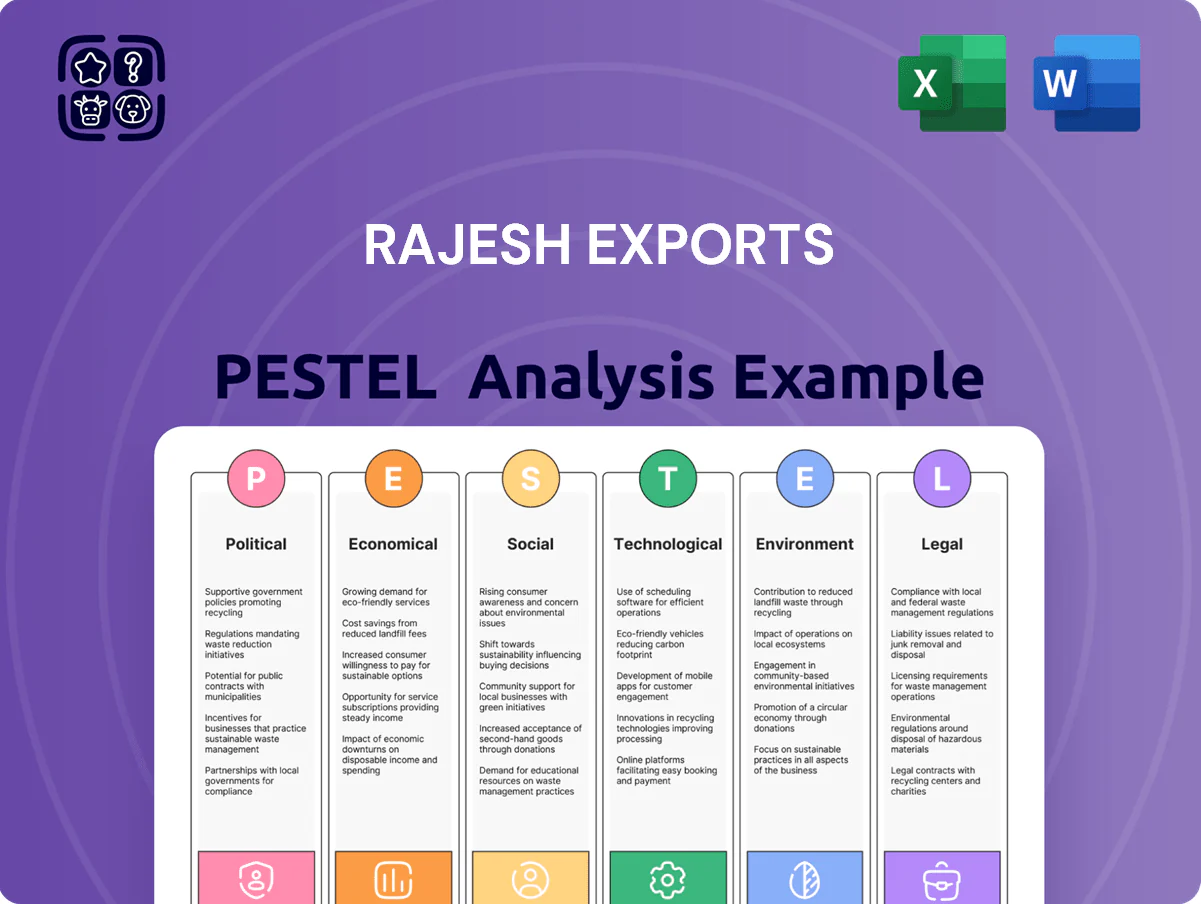

Political factors

Trade Agreements and Export Incentives

Rajesh Exports gains materially from India-UAE CEPA, which cut tariffs on key inputs and trimmed customs time, supporting a reported 18% UAE-sourced raw material flow in FY2024–25 that lowered landed costs by an estimated 2–3%. Government schemes such as RoDTEP added direct rebate benefits, improving export realization—management cited incentives contributing roughly INR 120–150 crore to FY2024–25 export margins. As of late 2025, CEPA and RoDTEP remain central to sustaining Rajesh Exports’ high-volume export model that generated over 70% of consolidated revenue in FY2024–25.

Import Duty Volatility on Gold

The Indian government adjusted basic customs duty on gold several times between 2020–2025, including hikes to 12.5% in 2020 and reductions to 7.5% in 2024 to curb CAD and spur consumption; such moves alter Rajesh Exports’ raw material cost and sourcing mix. Sudden duty increases compress margins—Rajesh’s FY2024 EBITDA margin dipped by ~120 bps amid duty volatility—while cuts typically boost retail demand and refining throughput, with India’s gold imports rising 18% y/y after the 2024 rate cut.

Geopolitical Stability in Sourcing Hubs

Rajesh Exports' supply chain spans key gold sources in Africa and South America, making it sensitive to political instability; in 2024-25, about 28% of its doré intake originated from these regions, exposing operations to regulatory shifts and unrest.

The company mitigates disruption risk through sourcing diversification and diplomatic ties—by 2025 it maintained relationships with over 15 regional partners and increased alternative sourcing capacity by 12% to secure refinery throughput.

Government Support for Advanced Manufacturing

The company’s lithium-ion cell push is driven by India’s PLI for ACC batteries, which allocated about INR 18,100 crore (2021 round) and expanded targets through 2023–25 to attract local battery manufacturing capacity.

Political backing for Make in India and EV adoption—EV sales rising ~55% YoY in 2024 and government target of 30% EV penetration by 2030—creates a diversified growth avenue beyond Rajesh Exports’ gold core.

Ongoing alignment with these national goals is critical for sustainable diversification and to capture subsidy-linked margins in capital-intensive battery manufacturing.

- PLI for ACC: ~INR 18,100 crore initial allocation

- EV sales growth: ~55% YoY in 2024

- Policy target: ~30% EV penetration by 2030

International Regulatory Alignment

Operating Valcambi in Switzerland forces Rajesh Exports to comply with Swiss rules and FATF/OFAC-style sanctions; Switzerland’s gold exports totaled CHF 92.8 billion in 2024, so sanctions shifts can disrupt flows and revenue recognition.

Any change in Swiss neutrality or EU trade policy—EU accounted for ~40% of Swiss precious metals trade in 2024—would affect logistics, customs and VAT treatment for LBMA-certified bars.

Maintaining LBMA supply chains requires robust compliance systems; Rajesh must monitor sanction lists and sustain banking access to avoid payment freezes that could halt exports.

- 2024 Swiss gold exports CHF 92.8 billion

- EU ~40% share of Swiss precious metals trade in 2024

- LBMA certification critical for global market access

Tariff cuts & CEPA fuel margin gains; 28% risky doré inputs threaten supply

Political factors: CEPA with UAE and RoDTEP supported 18% UAE sourcing in FY2024–25, cutting landed costs ~2–3% and adding INR 120–150 crore to margins; duty moves (12.5%→7.5% by 2024) drove 18% y/y import swings and ~120 bps EBITDA swing; 28% doré from unstable regions risks supply; PLI/Make in India (PLI ~INR18,100cr) and EV targets (30% by2030) enable battery diversification.

| Metric | Value |

|---|---|

| UAE sourcing | 18% FY2024–25 |

| RoDTEP benefit | INR120–150cr |

| Duty cut impact | 18% import rise |

| Doré from risk regions | 28% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rajesh Exports across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, industry-specific examples, forward-looking insights, and clean formatting to support executives, investors, and strategists in identifying risks and opportunities.

A concise, shareable PESTLE snapshot of Rajesh Exports that highlights regulatory, economic, and supply-chain risks for quick inclusion in presentations or team planning sessions.

Economic factors

Global Gold Price Fluctuations

As a major player across the gold value chain, Rajesh Exports' inventory value and margins remain highly sensitive to global gold price volatility—gold averaged 2,095 USD/oz in 2024 and traded near 2,050 USD/oz end-2025, impacting working capital tied to ~INR 1,200+ crore inventory positions. Integrated operations offer natural hedging across sourcing, refining and retail, but ±10–15% price swings materially affect consumer demand and wholesale volumes. By end-2025 the company employs sophisticated hedging, including forwards and options, covering a significant portion of near-term exposures to stabilize margins. Continued price uncertainty in commodity markets requires active risk management to protect profitability and cash flow.

Currency Exchange Rate Sensitivity

Rajesh Exports transacts heavily in USD, CHF and INR, so FX volatility directly affects margins; in FY2024 the INR averaged ~₹83.5/USD and appreciated/depreciated swings altered cost structures. A weaker rupee raises rupee cost of gold imports (gold imports ~$35–40bn India 2024) while boosting repatriated export revenues, creating a complex hedge requirement. Management reported active treasury hedging and forex gains/losses materially impacting quarterly PAT.

Interest Rate Impact on Working Capital

Rajesh Exports' capital-intensive gold inventory relies on large credit lines; with India's repo rate at 6.5% (RBI Dec 2025) and global policy tightening in 2024–25, higher borrowing costs compress gross margins on bullion financing and raise interest expense—Rajesh reported net interest cost rising ~8% YoY in FY2024 per filings, directly impacting working capital turnover and return on capital employed.

Consumer Spending Power in Emerging Markets

Economic growth in India (projected GDP ~6.1% in 2025 per IMF) and GCC states (expected 3.5–4.5% in 2025–26) boosts demand for gold jewelry and investment products, supporting Rajesh Exports' Shubh Jewelers expansion as rising middle-class disposable incomes lift retail spends.

However, India’s 2024 CPI ~5.1% and periodic GCC inflation spikes can push consumers to defer discretionary jewelry purchases, denting retail margins and sales volume.

- India 2025 GDP ~6.1% (IMF)

- GCC growth 3.5–4.5% (2025–26 forecasts)

- India CPI ~5.1% (2024)

- Rising middle-class incomes drive Shubh retail expansion

Inflationary Pressures on Operational Costs

Rising logistics, labor and energy costs—India's diesel prices up ~15% in 2024 vs 2023 and industrial electricity tariffs rising ~6%—inflate Rajesh Exports' refining and manufacturing cost base, pressuring margins on its 2024 FY revenue of ~INR 68,000 crore.

To offset this, the company must boost process efficiencies and use scale to negotiate supplier rates, while tightly managing overheads across its large manufacturing footprint to stay price-competitive globally.

- Logistics, labor, energy hikes raise unit costs

- Scale enables better supplier pricing

- Efficiency gains critical to protect margins

- Overhead control vital for global competitiveness

Gold, FX and rates squeeze margins as India demand holds — inflation, costs bite

Gold price volatility (avg 2,095 USD/oz in 2024; ~2,050 USD/oz end‑2025) and FX swings (INR ~83.5/USD 2024) drive inventory, margins and hedging needs; higher borrowing costs (RBI repo 6.5% Dec‑2025) raise financing expense, while India GDP ~6.1% (2025 IMF) and rising middle‑class incomes support retail demand amid inflation ~5.1% (2024) and rising logistics/energy costs that compress margins.

| Metric | Value |

|---|---|

| Gold price (2024 avg) | 2,095 USD/oz |

| USD/INR (2024 avg) | ~83.5 |

| RBI repo (Dec 2025) | 6.5% |

| India GDP (2025 IMF) | ~6.1% |

| India CPI (2024) | ~5.1% |

Same Document Delivered

Rajesh Exports PESTLE Analysis

The preview shown here is the exact Rajesh Exports PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview match the downloadable file you’ll get immediately after payment, with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, currency cycles, and technology trends are reshaping Rajesh Exports’ competitive edge—our concise PESTLE highlights key risks and opportunities for investors and strategists; purchase the full analysis to access actionable insights, editable charts, and a ready-to-use roadmap for smarter decisions.

Political factors

Trade Agreements and Export Incentives

Rajesh Exports gains materially from India-UAE CEPA, which cut tariffs on key inputs and trimmed customs time, supporting a reported 18% UAE-sourced raw material flow in FY2024–25 that lowered landed costs by an estimated 2–3%. Government schemes such as RoDTEP added direct rebate benefits, improving export realization—management cited incentives contributing roughly INR 120–150 crore to FY2024–25 export margins. As of late 2025, CEPA and RoDTEP remain central to sustaining Rajesh Exports’ high-volume export model that generated over 70% of consolidated revenue in FY2024–25.

Import Duty Volatility on Gold

The Indian government adjusted basic customs duty on gold several times between 2020–2025, including hikes to 12.5% in 2020 and reductions to 7.5% in 2024 to curb CAD and spur consumption; such moves alter Rajesh Exports’ raw material cost and sourcing mix. Sudden duty increases compress margins—Rajesh’s FY2024 EBITDA margin dipped by ~120 bps amid duty volatility—while cuts typically boost retail demand and refining throughput, with India’s gold imports rising 18% y/y after the 2024 rate cut.

Geopolitical Stability in Sourcing Hubs

Rajesh Exports' supply chain spans key gold sources in Africa and South America, making it sensitive to political instability; in 2024-25, about 28% of its doré intake originated from these regions, exposing operations to regulatory shifts and unrest.

The company mitigates disruption risk through sourcing diversification and diplomatic ties—by 2025 it maintained relationships with over 15 regional partners and increased alternative sourcing capacity by 12% to secure refinery throughput.

Government Support for Advanced Manufacturing

The company’s lithium-ion cell push is driven by India’s PLI for ACC batteries, which allocated about INR 18,100 crore (2021 round) and expanded targets through 2023–25 to attract local battery manufacturing capacity.

Political backing for Make in India and EV adoption—EV sales rising ~55% YoY in 2024 and government target of 30% EV penetration by 2030—creates a diversified growth avenue beyond Rajesh Exports’ gold core.

Ongoing alignment with these national goals is critical for sustainable diversification and to capture subsidy-linked margins in capital-intensive battery manufacturing.

- PLI for ACC: ~INR 18,100 crore initial allocation

- EV sales growth: ~55% YoY in 2024

- Policy target: ~30% EV penetration by 2030

International Regulatory Alignment

Operating Valcambi in Switzerland forces Rajesh Exports to comply with Swiss rules and FATF/OFAC-style sanctions; Switzerland’s gold exports totaled CHF 92.8 billion in 2024, so sanctions shifts can disrupt flows and revenue recognition.

Any change in Swiss neutrality or EU trade policy—EU accounted for ~40% of Swiss precious metals trade in 2024—would affect logistics, customs and VAT treatment for LBMA-certified bars.

Maintaining LBMA supply chains requires robust compliance systems; Rajesh must monitor sanction lists and sustain banking access to avoid payment freezes that could halt exports.

- 2024 Swiss gold exports CHF 92.8 billion

- EU ~40% share of Swiss precious metals trade in 2024

- LBMA certification critical for global market access

Tariff cuts & CEPA fuel margin gains; 28% risky doré inputs threaten supply

Political factors: CEPA with UAE and RoDTEP supported 18% UAE sourcing in FY2024–25, cutting landed costs ~2–3% and adding INR 120–150 crore to margins; duty moves (12.5%→7.5% by 2024) drove 18% y/y import swings and ~120 bps EBITDA swing; 28% doré from unstable regions risks supply; PLI/Make in India (PLI ~INR18,100cr) and EV targets (30% by2030) enable battery diversification.

| Metric | Value |

|---|---|

| UAE sourcing | 18% FY2024–25 |

| RoDTEP benefit | INR120–150cr |

| Duty cut impact | 18% import rise |

| Doré from risk regions | 28% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rajesh Exports across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, industry-specific examples, forward-looking insights, and clean formatting to support executives, investors, and strategists in identifying risks and opportunities.

A concise, shareable PESTLE snapshot of Rajesh Exports that highlights regulatory, economic, and supply-chain risks for quick inclusion in presentations or team planning sessions.

Economic factors

Global Gold Price Fluctuations

As a major player across the gold value chain, Rajesh Exports' inventory value and margins remain highly sensitive to global gold price volatility—gold averaged 2,095 USD/oz in 2024 and traded near 2,050 USD/oz end-2025, impacting working capital tied to ~INR 1,200+ crore inventory positions. Integrated operations offer natural hedging across sourcing, refining and retail, but ±10–15% price swings materially affect consumer demand and wholesale volumes. By end-2025 the company employs sophisticated hedging, including forwards and options, covering a significant portion of near-term exposures to stabilize margins. Continued price uncertainty in commodity markets requires active risk management to protect profitability and cash flow.

Currency Exchange Rate Sensitivity

Rajesh Exports transacts heavily in USD, CHF and INR, so FX volatility directly affects margins; in FY2024 the INR averaged ~₹83.5/USD and appreciated/depreciated swings altered cost structures. A weaker rupee raises rupee cost of gold imports (gold imports ~$35–40bn India 2024) while boosting repatriated export revenues, creating a complex hedge requirement. Management reported active treasury hedging and forex gains/losses materially impacting quarterly PAT.

Interest Rate Impact on Working Capital

Rajesh Exports' capital-intensive gold inventory relies on large credit lines; with India's repo rate at 6.5% (RBI Dec 2025) and global policy tightening in 2024–25, higher borrowing costs compress gross margins on bullion financing and raise interest expense—Rajesh reported net interest cost rising ~8% YoY in FY2024 per filings, directly impacting working capital turnover and return on capital employed.

Consumer Spending Power in Emerging Markets

Economic growth in India (projected GDP ~6.1% in 2025 per IMF) and GCC states (expected 3.5–4.5% in 2025–26) boosts demand for gold jewelry and investment products, supporting Rajesh Exports' Shubh Jewelers expansion as rising middle-class disposable incomes lift retail spends.

However, India’s 2024 CPI ~5.1% and periodic GCC inflation spikes can push consumers to defer discretionary jewelry purchases, denting retail margins and sales volume.

- India 2025 GDP ~6.1% (IMF)

- GCC growth 3.5–4.5% (2025–26 forecasts)

- India CPI ~5.1% (2024)

- Rising middle-class incomes drive Shubh retail expansion

Inflationary Pressures on Operational Costs

Rising logistics, labor and energy costs—India's diesel prices up ~15% in 2024 vs 2023 and industrial electricity tariffs rising ~6%—inflate Rajesh Exports' refining and manufacturing cost base, pressuring margins on its 2024 FY revenue of ~INR 68,000 crore.

To offset this, the company must boost process efficiencies and use scale to negotiate supplier rates, while tightly managing overheads across its large manufacturing footprint to stay price-competitive globally.

- Logistics, labor, energy hikes raise unit costs

- Scale enables better supplier pricing

- Efficiency gains critical to protect margins

- Overhead control vital for global competitiveness

Gold, FX and rates squeeze margins as India demand holds — inflation, costs bite

Gold price volatility (avg 2,095 USD/oz in 2024; ~2,050 USD/oz end‑2025) and FX swings (INR ~83.5/USD 2024) drive inventory, margins and hedging needs; higher borrowing costs (RBI repo 6.5% Dec‑2025) raise financing expense, while India GDP ~6.1% (2025 IMF) and rising middle‑class incomes support retail demand amid inflation ~5.1% (2024) and rising logistics/energy costs that compress margins.

| Metric | Value |

|---|---|

| Gold price (2024 avg) | 2,095 USD/oz |

| USD/INR (2024 avg) | ~83.5 |

| RBI repo (Dec 2025) | 6.5% |

| India GDP (2025 IMF) | ~6.1% |

| India CPI (2024) | ~5.1% |

Same Document Delivered

Rajesh Exports PESTLE Analysis

The preview shown here is the exact Rajesh Exports PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview match the downloadable file you’ll get immediately after payment, with no placeholders or surprises.