Ramsay Sante PESTLE Analysis

Your Shortcut to Market Insight Starts Here

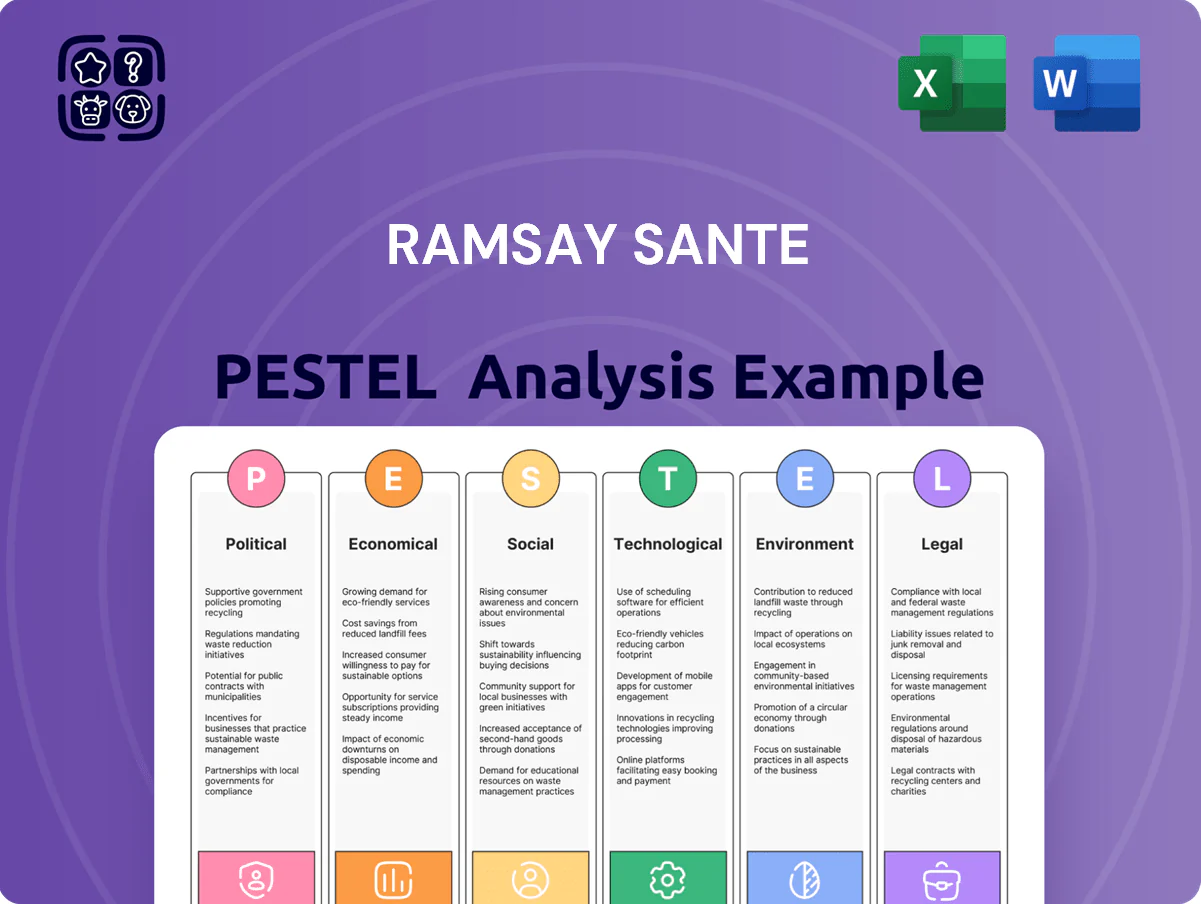

Gain a strategic advantage with our PESTLE Analysis of Ramsay Sante—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s prospects; buy the full version to unlock detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for smarter decisions.

Political factors

Government Reimbursement and Tariff Policies

State funding levels in France and Scandinavia directly dictate revenue potential for private operators like Ramsay Sante, with public reimbursements accounting for roughly 60–70% of group revenues in 2024–25 across core markets.

As of 2025 the French government continues to adjust annual price lists for procedures—FY2025 tariff changes averaged +1.8% for inpatient stays—forcing agile financial planning to protect margins.

Analysts must monitor sovereign health budget allocations closely: France budgeted €240bn for healthcare in 2025 and shifts in regional reimbursements can materially affect cash flows for the network.

Public-Private Partnership Integration

European healthcare systems are increasingly turning to private partners to relieve public hospitals, with private providers handling about 20% of acute care in France and PPPs accounting for €10–15bn annual investment across EU health infrastructure in 2024.

Ramsay Santé gains from political initiatives promoting private participation in emergency services and specialized surgery, contributing to its €5.6bn FY2024 revenue and expansion of capacity by 3.2% year-on-year.

However, moves toward nationalization or tighter private-sector regulation in France, Sweden or the UK—where public spending decisions could alter reimbursement rates—would materially threaten Ramsay Santé’s asset-light and fee-for-service model.

European Union Health Policy Harmonization

The EU push for a European Health Data Space and unified clinical standards compels Ramsay Santé to harmonize IT systems across its 500+ European sites, impacting €5.2bn 2024 revenue through investment in interoperability and cybersecurity.

Political alignment on cross-border healthcare access enables standardized service offerings and potential scale efficiencies, while creating complex compliance demands tied to GDPR and EU certification regimes.

Brussels decisions on workforce mobility—relevant as Ramsay reported 18% clinical staff vacancy rates in 2023—could ease staffing shortages but require adaptation of HR, credentialing and payroll systems across member states.

Geopolitical Stability and Energy Security

Ongoing geopolitical tensions in Eastern Europe have pushed European gas prices up ~60% from 2021 lows, increasing hospital energy bills and creating shortages in medical consumables sourced via disrupted supply chains.

Eurozone political stability is critical for Ramsay Sante to secure ~€500m+ in capital expenditure financing and to avoid variable interest and operational cost shocks that would strain margins.

Government interventions—price caps, subsidies, or strategic reserves—can reduce energy cost volatility for large hospitals or, if poorly targeted, amplify fiscal pressure and pass-through costs to providers.

- Energy price rise ~60% since 2021

- Supply-chain disruptions increasing consumable lead times

- ~€500m+ capex financing reliance on political stability

- Government energy policies can mitigate or worsen cost pressures

National Health Reform Agendas

The 2019–2022 French Ségur de la santé reforms and ongoing Nordic restructuring commit to higher staffing ratios and wage uplifts—France mandated a collective increase equivalent to roughly €7–9bn annually across hospitals in early 2024 estimates—raising Ramsay Santé’s operating costs unless subsidized by the state.

Such political agendas tie funding and licensing to compliance with national priorities; in 2023, ~15–20% of French hospital budgets were conditional on meeting Ségur targets, making alignment critical for Ramsay’s license renewals and preferred-provider status.

- Mandatory wage increases ~€7–9bn (France) impact margins

- 15–20% of budgets conditional on Ségur compliance (2023)

- Nordic restructuring shifts care to public–private collaboration, altering market access

Ramsay Santé faces reimbursement, tariff, wage, energy and €500m+ capex political risks

Political risk for Ramsay Santé centers on reimbursement volatility (60–70% public funding 2024–25), tariff changes (+1.8% FY2025), wage mandates (~€7–9bn France uplift), energy cost shocks (~+60% vs 2021) and €500m+ capex funding sensitivity; EU Health Data Space and cross‑border rules add compliance costs across 500+ sites.

| Factor | Key Metric (2024–25) |

|---|---|

| Public reimbursements | 60–70% revenues |

| FY2025 tariff change | +1.8% |

| France wage uplift | €7–9bn |

| Energy price rise | ~+60% vs 2021 |

| Capex reliance | €500m+ |

| Sites impacted | 500+ European sites |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ramsay Santé across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and investor communications, formatted for direct use in plans, decks, and reports.

Concise PESTLE summary tailored to Ramsay Santé, organized by category for quick reference in meetings or presentations and easily dropped into slides to align teams on external risks and strategic opportunities.

Economic factors

Inflationary Pressure on Operating Costs

Persistent inflation in 2025 has pushed medical supply and pharmaceutical costs up roughly 6–8% year-on-year in Europe, squeezing margins as Ramsay Sante operates under largely fixed government tariffs; specialized equipment inflation exceeded 10% in some categories. Effective procurement and centralized volume-based discounts across its 500+ European facilities are essential to offset a projected €50–120 million annual input cost hit. Strategic supplier contracts and pass-through mechanisms where allowed will be critical to protect operating cash flow.

Labor Market Shortages and Wage Growth

The French healthcare sector faces a structural shortfall of about 70,000 nurses and 10,000 physicians (2024 estimates), intensifying competition for staff and pushing wage growth above national averages (nurse pay up ~5–7% y/y in 2023–24). Personnel costs are ~60–65% of Ramsay Santé’s operating expenses, forcing higher agency fees and turnover costs. Ramsay must scale retention programs and international recruitment—already a growing share of hiring—to control rising labor-related expenditures.

Interest Rate Environment and Debt Servicing

As a capital-intensive operator, Ramsay Santé faces higher debt servicing costs if ECB rates remain elevated; the ECB deposit rate rose to 4.00% by Dec 2025, pushing average euro corporate borrowing spreads to roughly 200–250bps for BBB firms. Financing acquisitions or facility upgrades will hinge on end-2025 policy rates and term premiums, making careful mix of fixed vs floating debt essential. Maintaining a sustainable net debt/EBITDA near sector median (~2.5x in 2024) is critical to preserve ratings and liquidity.

Consumer Spending and Private Insurance Trends

Economic downturns and falling disposable income can reduce demand for elective procedures and premium private rooms; in 2023 elective surgery volumes in Europe fell ~4-6% in some markets, hitting high-margin services.

Private insurance growth drives non-government revenue: private health insurance penetration in France and Germany rose modestly to ~12–15% in 2024, supporting Ramsay Santé’s fee-for-service mix.

Economic stability increases enrollment in top-tier plans, boosting margins—markets with GDP growth >2% saw 3–5% higher private revenue growth in 2024.

- Elective volume sensitivity: -4–6% during downturns

- Private insurance penetration ~12–15% (2024)

- GDP >2% correlated with +3–5% private revenue growth (2024)

Currency Exchange Volatility

Operating across the Eurozone and Nordics exposes Ramsay Santé to EUR/SEK and EUR/NOK swings; EUR lost about 4% vs NOK and gained 2% vs SEK in 2024, affecting 2024 consolidated revenues and reported EBIT margins.

Currency movements can alter the relative cost of cross-border M&A and capex, with a 5% depreciation of EUR vs NOK increasing Norwegian capex in EUR terms by ~5%.

Hedging (forwards, swaps) is essential; Ramsay could reduce FX earnings volatility—industry practice shows hedging can cut reported earnings volatility by up to 60%.

- Exposure: EUR/SEK, EUR/NOK across operations

- 2024 moves: EUR −4% vs NOK, +2% vs SEK

- Impact: 5% FX move ≈ 5% change in foreign capex/costs

- Mitigation: hedging (forwards/swaps) can lower earnings volatility ~60%

Rising costs, tighter rates squeeze hospitals: €50–120m hit, labor 60–65% Opex

Inflation raised medical/pharma costs 6–8% y/y (2025), specialized equipment >10%, creating a €50–120m annual input hit; labor shortages pushed nurse pay +5–7% and personnel costs to ~60–65% of Opex; ECB rates at 4.00% (Dec 2025) lifted borrowing spreads ~200–250bps, stressing capex/deal financing; private insurance penetration ~12–15% (2024) cushions elective volume sensitivity (down 4–6% in downturns).

| Metric | Value |

|---|---|

| Medical cost inflation | 6–8% |

| Equipment inflation | >10% |

| Labour Opex share | 60–65% |

| ECB rate (Dec 2025) | 4.00% |

| Private insurance (2024) | 12–15% |

Full Version Awaits

Ramsay Sante PESTLE Analysis

The preview shown here is the exact Ramsay Santé PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Ramsay Sante—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the company’s prospects; buy the full version to unlock detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for smarter decisions.

Political factors

Government Reimbursement and Tariff Policies

State funding levels in France and Scandinavia directly dictate revenue potential for private operators like Ramsay Sante, with public reimbursements accounting for roughly 60–70% of group revenues in 2024–25 across core markets.

As of 2025 the French government continues to adjust annual price lists for procedures—FY2025 tariff changes averaged +1.8% for inpatient stays—forcing agile financial planning to protect margins.

Analysts must monitor sovereign health budget allocations closely: France budgeted €240bn for healthcare in 2025 and shifts in regional reimbursements can materially affect cash flows for the network.

Public-Private Partnership Integration

European healthcare systems are increasingly turning to private partners to relieve public hospitals, with private providers handling about 20% of acute care in France and PPPs accounting for €10–15bn annual investment across EU health infrastructure in 2024.

Ramsay Santé gains from political initiatives promoting private participation in emergency services and specialized surgery, contributing to its €5.6bn FY2024 revenue and expansion of capacity by 3.2% year-on-year.

However, moves toward nationalization or tighter private-sector regulation in France, Sweden or the UK—where public spending decisions could alter reimbursement rates—would materially threaten Ramsay Santé’s asset-light and fee-for-service model.

European Union Health Policy Harmonization

The EU push for a European Health Data Space and unified clinical standards compels Ramsay Santé to harmonize IT systems across its 500+ European sites, impacting €5.2bn 2024 revenue through investment in interoperability and cybersecurity.

Political alignment on cross-border healthcare access enables standardized service offerings and potential scale efficiencies, while creating complex compliance demands tied to GDPR and EU certification regimes.

Brussels decisions on workforce mobility—relevant as Ramsay reported 18% clinical staff vacancy rates in 2023—could ease staffing shortages but require adaptation of HR, credentialing and payroll systems across member states.

Geopolitical Stability and Energy Security

Ongoing geopolitical tensions in Eastern Europe have pushed European gas prices up ~60% from 2021 lows, increasing hospital energy bills and creating shortages in medical consumables sourced via disrupted supply chains.

Eurozone political stability is critical for Ramsay Sante to secure ~€500m+ in capital expenditure financing and to avoid variable interest and operational cost shocks that would strain margins.

Government interventions—price caps, subsidies, or strategic reserves—can reduce energy cost volatility for large hospitals or, if poorly targeted, amplify fiscal pressure and pass-through costs to providers.

- Energy price rise ~60% since 2021

- Supply-chain disruptions increasing consumable lead times

- ~€500m+ capex financing reliance on political stability

- Government energy policies can mitigate or worsen cost pressures

National Health Reform Agendas

The 2019–2022 French Ségur de la santé reforms and ongoing Nordic restructuring commit to higher staffing ratios and wage uplifts—France mandated a collective increase equivalent to roughly €7–9bn annually across hospitals in early 2024 estimates—raising Ramsay Santé’s operating costs unless subsidized by the state.

Such political agendas tie funding and licensing to compliance with national priorities; in 2023, ~15–20% of French hospital budgets were conditional on meeting Ségur targets, making alignment critical for Ramsay’s license renewals and preferred-provider status.

- Mandatory wage increases ~€7–9bn (France) impact margins

- 15–20% of budgets conditional on Ségur compliance (2023)

- Nordic restructuring shifts care to public–private collaboration, altering market access

Ramsay Santé faces reimbursement, tariff, wage, energy and €500m+ capex political risks

Political risk for Ramsay Santé centers on reimbursement volatility (60–70% public funding 2024–25), tariff changes (+1.8% FY2025), wage mandates (~€7–9bn France uplift), energy cost shocks (~+60% vs 2021) and €500m+ capex funding sensitivity; EU Health Data Space and cross‑border rules add compliance costs across 500+ sites.

| Factor | Key Metric (2024–25) |

|---|---|

| Public reimbursements | 60–70% revenues |

| FY2025 tariff change | +1.8% |

| France wage uplift | €7–9bn |

| Energy price rise | ~+60% vs 2021 |

| Capex reliance | €500m+ |

| Sites impacted | 500+ European sites |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ramsay Santé across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and investor communications, formatted for direct use in plans, decks, and reports.

Concise PESTLE summary tailored to Ramsay Santé, organized by category for quick reference in meetings or presentations and easily dropped into slides to align teams on external risks and strategic opportunities.

Economic factors

Inflationary Pressure on Operating Costs

Persistent inflation in 2025 has pushed medical supply and pharmaceutical costs up roughly 6–8% year-on-year in Europe, squeezing margins as Ramsay Sante operates under largely fixed government tariffs; specialized equipment inflation exceeded 10% in some categories. Effective procurement and centralized volume-based discounts across its 500+ European facilities are essential to offset a projected €50–120 million annual input cost hit. Strategic supplier contracts and pass-through mechanisms where allowed will be critical to protect operating cash flow.

Labor Market Shortages and Wage Growth

The French healthcare sector faces a structural shortfall of about 70,000 nurses and 10,000 physicians (2024 estimates), intensifying competition for staff and pushing wage growth above national averages (nurse pay up ~5–7% y/y in 2023–24). Personnel costs are ~60–65% of Ramsay Santé’s operating expenses, forcing higher agency fees and turnover costs. Ramsay must scale retention programs and international recruitment—already a growing share of hiring—to control rising labor-related expenditures.

Interest Rate Environment and Debt Servicing

As a capital-intensive operator, Ramsay Santé faces higher debt servicing costs if ECB rates remain elevated; the ECB deposit rate rose to 4.00% by Dec 2025, pushing average euro corporate borrowing spreads to roughly 200–250bps for BBB firms. Financing acquisitions or facility upgrades will hinge on end-2025 policy rates and term premiums, making careful mix of fixed vs floating debt essential. Maintaining a sustainable net debt/EBITDA near sector median (~2.5x in 2024) is critical to preserve ratings and liquidity.

Consumer Spending and Private Insurance Trends

Economic downturns and falling disposable income can reduce demand for elective procedures and premium private rooms; in 2023 elective surgery volumes in Europe fell ~4-6% in some markets, hitting high-margin services.

Private insurance growth drives non-government revenue: private health insurance penetration in France and Germany rose modestly to ~12–15% in 2024, supporting Ramsay Santé’s fee-for-service mix.

Economic stability increases enrollment in top-tier plans, boosting margins—markets with GDP growth >2% saw 3–5% higher private revenue growth in 2024.

- Elective volume sensitivity: -4–6% during downturns

- Private insurance penetration ~12–15% (2024)

- GDP >2% correlated with +3–5% private revenue growth (2024)

Currency Exchange Volatility

Operating across the Eurozone and Nordics exposes Ramsay Santé to EUR/SEK and EUR/NOK swings; EUR lost about 4% vs NOK and gained 2% vs SEK in 2024, affecting 2024 consolidated revenues and reported EBIT margins.

Currency movements can alter the relative cost of cross-border M&A and capex, with a 5% depreciation of EUR vs NOK increasing Norwegian capex in EUR terms by ~5%.

Hedging (forwards, swaps) is essential; Ramsay could reduce FX earnings volatility—industry practice shows hedging can cut reported earnings volatility by up to 60%.

- Exposure: EUR/SEK, EUR/NOK across operations

- 2024 moves: EUR −4% vs NOK, +2% vs SEK

- Impact: 5% FX move ≈ 5% change in foreign capex/costs

- Mitigation: hedging (forwards/swaps) can lower earnings volatility ~60%

Rising costs, tighter rates squeeze hospitals: €50–120m hit, labor 60–65% Opex

Inflation raised medical/pharma costs 6–8% y/y (2025), specialized equipment >10%, creating a €50–120m annual input hit; labor shortages pushed nurse pay +5–7% and personnel costs to ~60–65% of Opex; ECB rates at 4.00% (Dec 2025) lifted borrowing spreads ~200–250bps, stressing capex/deal financing; private insurance penetration ~12–15% (2024) cushions elective volume sensitivity (down 4–6% in downturns).

| Metric | Value |

|---|---|

| Medical cost inflation | 6–8% |

| Equipment inflation | >10% |

| Labour Opex share | 60–65% |

| ECB rate (Dec 2025) | 4.00% |

| Private insurance (2024) | 12–15% |

Full Version Awaits

Ramsay Sante PESTLE Analysis

The preview shown here is the exact Ramsay Santé PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same file you’ll download immediately after payment.