Ranpak PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Ranpak’s prospects in our concise PESTLE overview—perfect for investors and strategists who need quick, actionable context. Buy the full PESTLE to access a detailed, exportable analysis with regulatory, environmental, and social insights you can use immediately to inform decisions and uncover growth opportunities.

Political factors

Plastic reduction mandates

Governments are tightening single-use plastic bans—EU’s SUP Directive and 2025 targets are cutting plastic packaging by up to 30% in some markets—boosting demand for Ranpak’s paper void-fill. Ranpak gains as companies shift to fiber-based systems to meet landfill-reduction laws; global bans and extended producer responsibility rules helped paper protective packaging grow ~6–8% CAGR (2020–2024), favoring Ranpak’s revenue mix.

Trade protectionism and tariffs

Fluctuating trade relations and tariffs—such as recent U.S. steel and aluminum tariffs and EU tariff reviews—raise input costs for Ranpak, where paperboard accounts for roughly 40–50% of COGS in packaging peers; a 5–10% tariff on raw paper could raise packaging costs materially. Political instability in Vietnam and parts of Eastern Europe, which together contributed to an estimated 20% of global contract manufacturing capacity for packaging in 2024, forces Ranpak to maintain agile sourcing and contingency inventories. In 2024–25, increases in import duties on industrial equipment (ranging 3–12% in key markets) can lift total cost of ownership for Ranpak’s automated systems, potentially extending payback periods by 6–18 months depending on model and local incentives.

Government green subsidies

Government green subsidies and tax credits—such as the EU’s 2024 Green Deal Industrial Plan allocating €30bn for decarbonization—lower upfront costs for buyers of Ranpak’s fiber-based packaging machines, boosting market penetration.

Geopolitical supply chain stability

Regional conflicts (e.g., Red Sea shipping disruptions in 2023 pushed container rates up ~50%) threaten Ranpak’s delivery of heavy machinery and paper volumes, increasing logistics costs and lead times.

Monitoring political climates in wood-pulp producing countries (Brazil, Canada, Sweden) is crucial; pulp price volatility rose ~18% in 2024, impacting input costs.

Political shifts affecting energy policy can spike manufacturing costs — global industrial electricity prices varied up to 30% across key markets in 2024, raising paper production expenses.

- Red Sea disruptions → container rates +50% (2023)

- Pulp price volatility +18% (2024)

- Industrial electricity price variance up to 30% (2024)

International shipping regulations

- Regulatory push: IMO/EU CO2 targets to 2030

- Impact: dimensional weight drives higher freight charges

- Ranpak fit: reduces volume/weight 10–25%

- Financial effect: lowers fuel surcharges and carbon levy exposure

Policy-driven surge in Ranpak demand vs. rising pulp, container and energy costs

Political shifts—single-use plastic bans (EU SUP Directive), green subsidies (EU Green Deal €30bn), trade tariffs (5–10% raw paper risk), and shipping rules (IMO/EU CO2 −20% by 2030)—boost Ranpak demand but raise input/logistics costs; pulp volatility +18% and container rates +50% (2023) heighten sourcing and pricing risk.

| Factor | 2023–25 Data |

|---|---|

| Container rates | +50% (2023) |

| Pulp volatility | +18% (2024) |

| Electricity variance | ±30% (2024) |

What is included in the product

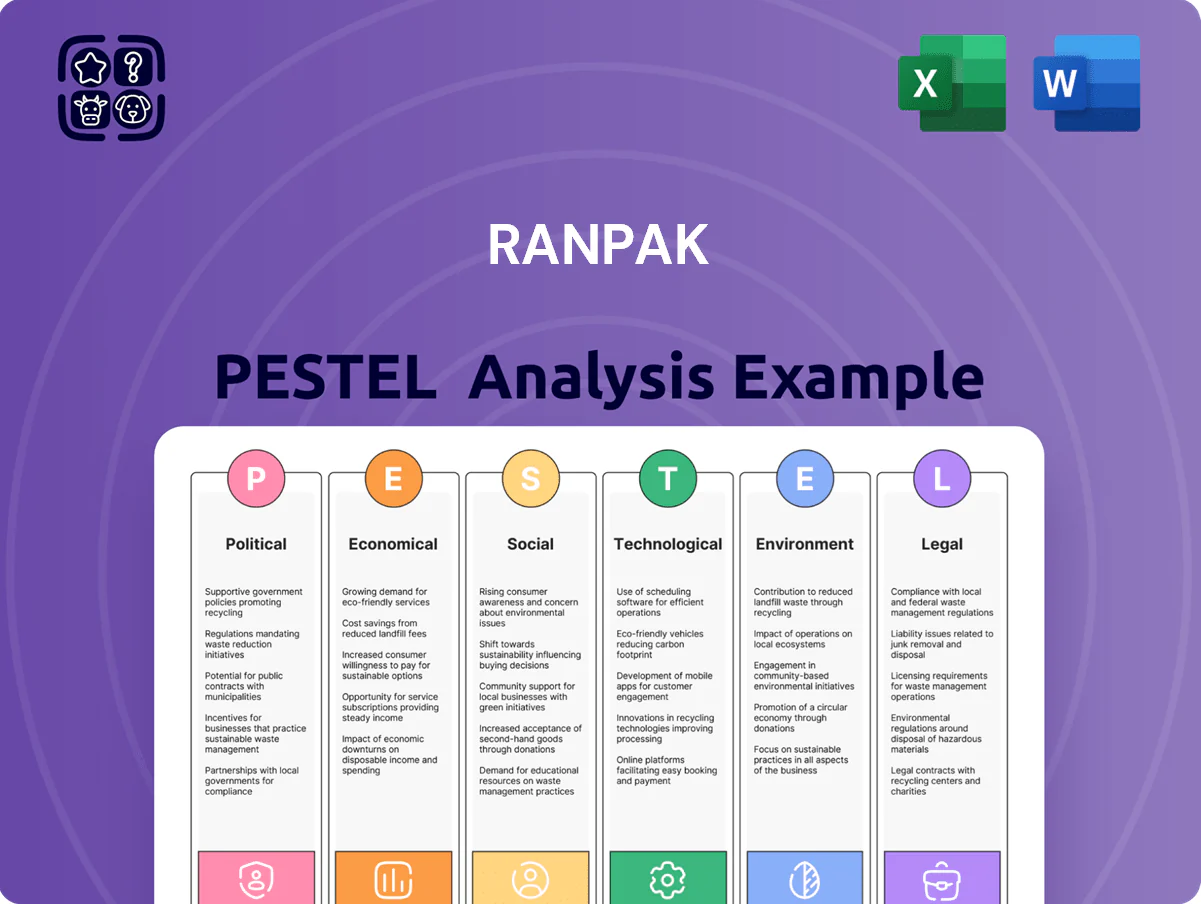

Explores how external macro-environmental factors uniquely affect Ranpak across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities relevant to its industry and region, delivered in clean, investor-ready formatting and including forward-looking insights for scenario planning and strategy design.

Visually segmented by PESTLE categories for rapid interpretation, the Ranpak PESTLE Analysis offers a concise, shareable summary ideal for meetings, presentations, and cross-team alignment.

Economic factors

E-commerce market expansion

The global e-commerce market reached about 5.7 trillion USD in 2024 and is projected to top 7 trillion by 2027, keeping shipping volumes high and directly boosting demand for Ranpak’s cushioning and paper-based wrapping solutions.

With e-commerce returns and fragile items growing, protective packaging demand rose ~6–8% annualized in 2023–25, enabling Ranpak to scale across SMBs and 3PLs and capture peak-season volume surges.

Raw material price volatility

Paper pulp prices rose ~18% year-over-year in 2024, driven by strong global packaging demand and higher energy costs, raising Ranpak’s input costs given paper accounts for ~60% of its COGS; sustained spikes could compress margins if price increases are not passed to customers.

Ranpak’s 2024 gross margin of ~28% is sensitive to pulp volatility, so the firm relies on multi-year supply contracts and inventory buffers to hedge short-term swings.

Global interest rate environment

High global interest rates—with US policy rates averaging around 5.25–5.50% in 2024 and ECB rates near 4%—can constrain Ranpak clients’ capex, delaying purchases or leasing of new packaging machinery.

Conversely, if rates stabilize or fall (markets priced ~55% chance of a Fed cut by end-2025 as of Dec 2024), firms are likelier to fund warehouse automation and long-term upgrades.

Ranpak’s revenue and margins are tied to industrial firms’ access to credit for operational improvements, with industrial capex growth moderating to ~2–3% YoY in 2024 affecting demand.

Labor market automation trends

Rising U.S. warehouse wages—up about 12% from 2020–2024 to a median of roughly $17–18/hr in 2024—and chronic labor shortages boost demand for Ranpak’s automated/semi-automated packaging, lowering labor hours per package and cutting operating costs while increasing throughput by 20–40% in pilot studies.

Switching from manual plastic wrap to Ranpak automated paper systems shows payback periods often under 18 months as wage-driven savings and reduced material/landfill fees improve ROI.

- Median warehouse wage ~ $17–18/hr (2024)

- Throughput gains 20–40% in trials

- Typical payback < 18 months

- Lower material and disposal costs vs plastic

Currency exchange rate fluctuations

As a global supplier, Ranpak faces currency translation risk—roughly 25–35% of 2024 revenue derived from non-USD/EUR markets can swing reported results when converting local sales into USD; a 5% euro-dollar move altered comparable operating margins by ~30–50 basis points for peers in 2024.

Volatility in EUR/USD and other major currencies affects regional price competitiveness, potentially compressing margins in price-sensitive markets; localized production and pricing help mitigate pass-through lag.

Ranpak uses hedging and local cost centers; effective FX hedges and production near demand reduce exposure to unfavorable FX shifts and protect EBITDA.

- ~25–35% revenue from non-USD/EUR markets (2024)

- 5% FX move ≈ 30–50 bps margin impact (peer data, 2024)

- Mitigations: hedging, localized production, local pricing

Ranpak: E‑commerce boom and rising wages boost automated paper demand despite pulp cost hit

Strong e-commerce (USD 5.7T in 2024, >7T by 2027) and rising warehouse wages (~$17–18/hr) drive demand for Ranpak’s automated paper solutions; pulp prices +18% YoY (2024) raise COGS (paper ≈60% of COGS) and press margins (2024 gross margin ~28%). FX exposure (25–35% revenue non-USD/EUR) and high rates (US ~5.25–5.50% in 2024) influence capex and pricing.

| Metric | 2024 |

|---|---|

| E‑commerce GMV | USD 5.7T |

| Pulp price change | +18% YoY |

| Gross margin | ~28% |

| Warehouse wage | $17–18/hr |

| FX exposure | 25–35% rev |

Preview Before You Purchase

Ranpak PESTLE Analysis

The preview shown here is the exact Ranpak PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with the same layout, content, and structure visible in the preview. No placeholders or teasers—what you see is what you’ll download immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Ranpak’s prospects in our concise PESTLE overview—perfect for investors and strategists who need quick, actionable context. Buy the full PESTLE to access a detailed, exportable analysis with regulatory, environmental, and social insights you can use immediately to inform decisions and uncover growth opportunities.

Political factors

Plastic reduction mandates

Governments are tightening single-use plastic bans—EU’s SUP Directive and 2025 targets are cutting plastic packaging by up to 30% in some markets—boosting demand for Ranpak’s paper void-fill. Ranpak gains as companies shift to fiber-based systems to meet landfill-reduction laws; global bans and extended producer responsibility rules helped paper protective packaging grow ~6–8% CAGR (2020–2024), favoring Ranpak’s revenue mix.

Trade protectionism and tariffs

Fluctuating trade relations and tariffs—such as recent U.S. steel and aluminum tariffs and EU tariff reviews—raise input costs for Ranpak, where paperboard accounts for roughly 40–50% of COGS in packaging peers; a 5–10% tariff on raw paper could raise packaging costs materially. Political instability in Vietnam and parts of Eastern Europe, which together contributed to an estimated 20% of global contract manufacturing capacity for packaging in 2024, forces Ranpak to maintain agile sourcing and contingency inventories. In 2024–25, increases in import duties on industrial equipment (ranging 3–12% in key markets) can lift total cost of ownership for Ranpak’s automated systems, potentially extending payback periods by 6–18 months depending on model and local incentives.

Government green subsidies

Government green subsidies and tax credits—such as the EU’s 2024 Green Deal Industrial Plan allocating €30bn for decarbonization—lower upfront costs for buyers of Ranpak’s fiber-based packaging machines, boosting market penetration.

Geopolitical supply chain stability

Regional conflicts (e.g., Red Sea shipping disruptions in 2023 pushed container rates up ~50%) threaten Ranpak’s delivery of heavy machinery and paper volumes, increasing logistics costs and lead times.

Monitoring political climates in wood-pulp producing countries (Brazil, Canada, Sweden) is crucial; pulp price volatility rose ~18% in 2024, impacting input costs.

Political shifts affecting energy policy can spike manufacturing costs — global industrial electricity prices varied up to 30% across key markets in 2024, raising paper production expenses.

- Red Sea disruptions → container rates +50% (2023)

- Pulp price volatility +18% (2024)

- Industrial electricity price variance up to 30% (2024)

International shipping regulations

- Regulatory push: IMO/EU CO2 targets to 2030

- Impact: dimensional weight drives higher freight charges

- Ranpak fit: reduces volume/weight 10–25%

- Financial effect: lowers fuel surcharges and carbon levy exposure

Policy-driven surge in Ranpak demand vs. rising pulp, container and energy costs

Political shifts—single-use plastic bans (EU SUP Directive), green subsidies (EU Green Deal €30bn), trade tariffs (5–10% raw paper risk), and shipping rules (IMO/EU CO2 −20% by 2030)—boost Ranpak demand but raise input/logistics costs; pulp volatility +18% and container rates +50% (2023) heighten sourcing and pricing risk.

| Factor | 2023–25 Data |

|---|---|

| Container rates | +50% (2023) |

| Pulp volatility | +18% (2024) |

| Electricity variance | ±30% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ranpak across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities relevant to its industry and region, delivered in clean, investor-ready formatting and including forward-looking insights for scenario planning and strategy design.

Visually segmented by PESTLE categories for rapid interpretation, the Ranpak PESTLE Analysis offers a concise, shareable summary ideal for meetings, presentations, and cross-team alignment.

Economic factors

E-commerce market expansion

The global e-commerce market reached about 5.7 trillion USD in 2024 and is projected to top 7 trillion by 2027, keeping shipping volumes high and directly boosting demand for Ranpak’s cushioning and paper-based wrapping solutions.

With e-commerce returns and fragile items growing, protective packaging demand rose ~6–8% annualized in 2023–25, enabling Ranpak to scale across SMBs and 3PLs and capture peak-season volume surges.

Raw material price volatility

Paper pulp prices rose ~18% year-over-year in 2024, driven by strong global packaging demand and higher energy costs, raising Ranpak’s input costs given paper accounts for ~60% of its COGS; sustained spikes could compress margins if price increases are not passed to customers.

Ranpak’s 2024 gross margin of ~28% is sensitive to pulp volatility, so the firm relies on multi-year supply contracts and inventory buffers to hedge short-term swings.

Global interest rate environment

High global interest rates—with US policy rates averaging around 5.25–5.50% in 2024 and ECB rates near 4%—can constrain Ranpak clients’ capex, delaying purchases or leasing of new packaging machinery.

Conversely, if rates stabilize or fall (markets priced ~55% chance of a Fed cut by end-2025 as of Dec 2024), firms are likelier to fund warehouse automation and long-term upgrades.

Ranpak’s revenue and margins are tied to industrial firms’ access to credit for operational improvements, with industrial capex growth moderating to ~2–3% YoY in 2024 affecting demand.

Labor market automation trends

Rising U.S. warehouse wages—up about 12% from 2020–2024 to a median of roughly $17–18/hr in 2024—and chronic labor shortages boost demand for Ranpak’s automated/semi-automated packaging, lowering labor hours per package and cutting operating costs while increasing throughput by 20–40% in pilot studies.

Switching from manual plastic wrap to Ranpak automated paper systems shows payback periods often under 18 months as wage-driven savings and reduced material/landfill fees improve ROI.

- Median warehouse wage ~ $17–18/hr (2024)

- Throughput gains 20–40% in trials

- Typical payback < 18 months

- Lower material and disposal costs vs plastic

Currency exchange rate fluctuations

As a global supplier, Ranpak faces currency translation risk—roughly 25–35% of 2024 revenue derived from non-USD/EUR markets can swing reported results when converting local sales into USD; a 5% euro-dollar move altered comparable operating margins by ~30–50 basis points for peers in 2024.

Volatility in EUR/USD and other major currencies affects regional price competitiveness, potentially compressing margins in price-sensitive markets; localized production and pricing help mitigate pass-through lag.

Ranpak uses hedging and local cost centers; effective FX hedges and production near demand reduce exposure to unfavorable FX shifts and protect EBITDA.

- ~25–35% revenue from non-USD/EUR markets (2024)

- 5% FX move ≈ 30–50 bps margin impact (peer data, 2024)

- Mitigations: hedging, localized production, local pricing

Ranpak: E‑commerce boom and rising wages boost automated paper demand despite pulp cost hit

Strong e-commerce (USD 5.7T in 2024, >7T by 2027) and rising warehouse wages (~$17–18/hr) drive demand for Ranpak’s automated paper solutions; pulp prices +18% YoY (2024) raise COGS (paper ≈60% of COGS) and press margins (2024 gross margin ~28%). FX exposure (25–35% revenue non-USD/EUR) and high rates (US ~5.25–5.50% in 2024) influence capex and pricing.

| Metric | 2024 |

|---|---|

| E‑commerce GMV | USD 5.7T |

| Pulp price change | +18% YoY |

| Gross margin | ~28% |

| Warehouse wage | $17–18/hr |

| FX exposure | 25–35% rev |

Preview Before You Purchase

Ranpak PESTLE Analysis

The preview shown here is the exact Ranpak PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version, with the same layout, content, and structure visible in the preview. No placeholders or teasers—what you see is what you’ll download immediately after checkout.