Rapid7 Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

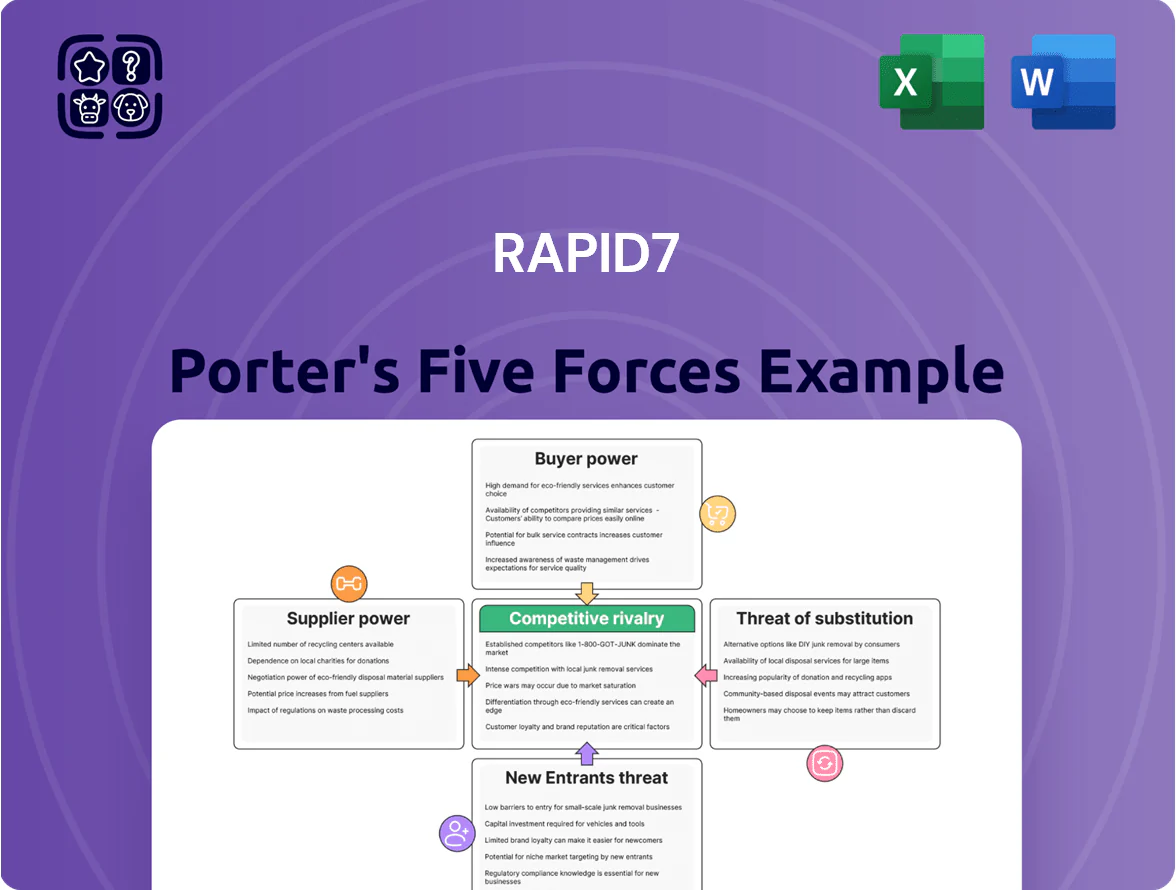

Rapid7 faces intense rivalry in cybersecurity, balancing strong product differentiation with pressure from agile startups and powerful buyers demanding integrated solutions.

This snapshot highlights supplier, buyer, entrant, substitute, and rivalry dynamics but only scratches the surface—unlock the full Porter's Five Forces Analysis to reveal force-by-force ratings, visuals, and strategic implications tailored to Rapid7.

Suppliers Bargaining Power

Cloud Infrastructure Dependencies

Rapid7 depends on AWS and Microsoft Azure to host its Insight platform and process petabyte-scale telemetry; moving a global security stack is technically complex and costly, creating supplier leverage.

Cloud concentration is high: by Q4 2025 AWS and Azure held about 58% of global cloud IaaS/PaaS revenue, so Rapid7 is effectively a price-taker for key compute and storage.

Cybersecurity Talent Scarcity

Third-party Threat Intelligence Feeds

Rapid7 augments its native research with third-party threat-intel feeds to sustain detection and response coverage; in 2025 it reported threat feed spend near $18–25m across platform partnerships to cover 200+ countries. Some vendors hold proprietary telemetry—like exclusive darknet or ISP datasets—giving them moderate bargaining power to set licensing fees and access terms that can raise COGS and restrict time-to-value. Rapid7 negotiates multi-year contracts and volume discounts to mitigate price volatility and ensure SLA-backed delivery.

Specialized Hardware Component Costs

Software Licensing and Integration Partners

Rapid7 relies on integrations with hundreds of third-party platforms—Windows, Linux, Oracle, SAP—to run accurate vulnerability scans; in 2024 Rapid7 reported integrations with 250+ vendors, so API or license shifts by key vendors can disrupt deployments.

Vendors’ API restrictions or fee increases give suppliers strategic leverage over Rapid7’s functionality and costs; a 15–30% rise in connector licensing would raise support costs and time-to-patch for customers.

Suppliers Grip Margins: Cloud duopoly, pricey security talent & 250+ integration risks

Suppliers wield moderate-to-high power: cloud giants (AWS/Azure ~58% IaaS/PaaS by Q4 2025) set pricing for compute/storage; specialized security talent costs (US median sec engineer ~$160,000 in 2025) and exclusive threat feeds (Rapid7 spend ~$18–25m in 2025) raise COGS and R&D spend; hardware/chip supply and 250+ third-party integrations add disruption risk and margin pressure.

| Metric | Value (2025) |

|---|---|

| AWS+Azure share | ~58% |

| Median sec engineer (US) | $160,000 |

| Threat feed spend | $18–25m |

| Third-party integrations | 250+ |

What is included in the product

Tailored Porter's Five Forces analysis for Rapid7 that uncovers competitive drivers, customer and supplier influence, barriers to entry, substitutes, and emerging threats—actionable for strategy, investor materials, or academic use.

Rapid7 Porter's Five Forces condensed into one actionable sheet—quickly assess competitive pressures and identify relief strategies to protect margins and accelerate secure growth.

Customers Bargaining Power

Demand for Platform Consolidation

By end-2025, 68% of enterprises surveyed prefer platform consolidation over 15+ point tools, boosting buyer leverage to demand bundled pricing; large accounts now negotiate discounts averaging 18% on unified suites. Rapid7 must prove its platform delivers lower total cost of ownership and 22% faster incident response versus stitching best-of-breed tools to justify full-suite pricing. If Rapid7 can’t show these metrics, churn and deal-size compression risk rising.

Enterprise Procurement Leverage

Large enterprises wield strong procurement leverage, using multi-vendor bake-offs and pushing for SLAs and volume discounts; Gartner reported 48% of security deals in 2024 involved competitive RFPs where price was primary.

Rapid7’s margin pressure hinges on proving ROI: automation and reduced breach risk—IBM’s 2023 Cost of a Data Breach found average savings of 3.58M when breaches were contained by automation—so Rapid7 must quantify similar savings to defend pricing.

Low Switching Costs for SaaS Solutions

The shift to cloud-native security lowers physical switching barriers between vulnerability management and XDR vendors; SaaS models mean no hardware lock-in and vendors like Rapid7 face churn risk—industry SaaS median annual churn ~15% (2024); data migration and retraining still add cost but often under 3 months. Rapid7 must therefore invest in customer success and monthly product releases to keep net retention above 100% and limit defections.

Availability of Alternative Information

In 2025 IT buyers use peer reviews, analyst reports (Gartner, Forrester) and real-time benchmarks to compare Rapid7 to Tenable and CrowdStrike, raising information symmetry and lowering seller informational advantage.

Customers leverage public telemetry and third-party tests—e.g., MITRE ATT&CK evaluations and NSS Labs-style reports—to dispute claims and extract discounts; 42% of enterprises reported negotiating security vendor pricing in 2024.

- High info symmetry vs rivals

- Use of MITRE/NSS-style benchmarks

- 42% of enterprises negotiated pricing in 2024

- Stronger demands for feature SLAs

Influence of Managed Service Providers

MSSPs (managed security service providers) control day-to-day security for ~40–50% of mid-market firms; their platform choices can therefore steer large blocks of customers toward or away from Rapid7.

If a major MSSP standardizes on a rival stack, Rapid7 could lose simultaneous access to thousands of endpoints and a meaningful share of ARR—industry reports estimate MSSP-influenced dealflow represents ~25% of mid-market security spend.

That concentration raises negotiation leverage for MSSPs on pricing, integration and roadmap priorities, increasing churn risk if Rapid7 fails to align with MSSP requirements.

- MSSPs cover ~40–50% mid-market

- MSSP-driven deals ≈25% of mid-market security spend

- Standardization risk: mass customer loss

- Gives MSSPs pricing and roadmap leverage

Rapid7 must prove 22% faster IRR and clear TCO to defend pricing or risk churn

Buyers hold strong leverage: 68% prefer consolidated platforms (end-2025) and large accounts secure ~18% discounts on suites, while 42% negotiated security vendor pricing in 2024; SaaS churn median ~15% (2024) and MSSPs influence ~25% of mid-market spend. Rapid7 must prove 22% faster IRR (incident response) and clear TCO savings to defend pricing and keep net retention >100% or face deal-size compression and churn.

| Metric | Value |

|---|---|

| Platform preference (end-2025) | 68% |

| Avg suite discount (large accounts) | 18% |

| Enterprises negotiating price (2024) | 42% |

| SaaS median churn (2024) | 15% |

| MSSP-influenced spend (mid-market) | 25% |

Full Version Awaits

Rapid7 Porter's Five Forces Analysis

This preview shows the exact Rapid7 Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the final deliverable: the same professionally written file available for instant download upon payment, with comprehensive force-by-force evaluation tailored to Rapid7.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Rapid7 faces intense rivalry in cybersecurity, balancing strong product differentiation with pressure from agile startups and powerful buyers demanding integrated solutions.

This snapshot highlights supplier, buyer, entrant, substitute, and rivalry dynamics but only scratches the surface—unlock the full Porter's Five Forces Analysis to reveal force-by-force ratings, visuals, and strategic implications tailored to Rapid7.

Suppliers Bargaining Power

Cloud Infrastructure Dependencies

Rapid7 depends on AWS and Microsoft Azure to host its Insight platform and process petabyte-scale telemetry; moving a global security stack is technically complex and costly, creating supplier leverage.

Cloud concentration is high: by Q4 2025 AWS and Azure held about 58% of global cloud IaaS/PaaS revenue, so Rapid7 is effectively a price-taker for key compute and storage.

Cybersecurity Talent Scarcity

Third-party Threat Intelligence Feeds

Rapid7 augments its native research with third-party threat-intel feeds to sustain detection and response coverage; in 2025 it reported threat feed spend near $18–25m across platform partnerships to cover 200+ countries. Some vendors hold proprietary telemetry—like exclusive darknet or ISP datasets—giving them moderate bargaining power to set licensing fees and access terms that can raise COGS and restrict time-to-value. Rapid7 negotiates multi-year contracts and volume discounts to mitigate price volatility and ensure SLA-backed delivery.

Specialized Hardware Component Costs

Software Licensing and Integration Partners

Rapid7 relies on integrations with hundreds of third-party platforms—Windows, Linux, Oracle, SAP—to run accurate vulnerability scans; in 2024 Rapid7 reported integrations with 250+ vendors, so API or license shifts by key vendors can disrupt deployments.

Vendors’ API restrictions or fee increases give suppliers strategic leverage over Rapid7’s functionality and costs; a 15–30% rise in connector licensing would raise support costs and time-to-patch for customers.

Suppliers Grip Margins: Cloud duopoly, pricey security talent & 250+ integration risks

Suppliers wield moderate-to-high power: cloud giants (AWS/Azure ~58% IaaS/PaaS by Q4 2025) set pricing for compute/storage; specialized security talent costs (US median sec engineer ~$160,000 in 2025) and exclusive threat feeds (Rapid7 spend ~$18–25m in 2025) raise COGS and R&D spend; hardware/chip supply and 250+ third-party integrations add disruption risk and margin pressure.

| Metric | Value (2025) |

|---|---|

| AWS+Azure share | ~58% |

| Median sec engineer (US) | $160,000 |

| Threat feed spend | $18–25m |

| Third-party integrations | 250+ |

What is included in the product

Tailored Porter's Five Forces analysis for Rapid7 that uncovers competitive drivers, customer and supplier influence, barriers to entry, substitutes, and emerging threats—actionable for strategy, investor materials, or academic use.

Rapid7 Porter's Five Forces condensed into one actionable sheet—quickly assess competitive pressures and identify relief strategies to protect margins and accelerate secure growth.

Customers Bargaining Power

Demand for Platform Consolidation

By end-2025, 68% of enterprises surveyed prefer platform consolidation over 15+ point tools, boosting buyer leverage to demand bundled pricing; large accounts now negotiate discounts averaging 18% on unified suites. Rapid7 must prove its platform delivers lower total cost of ownership and 22% faster incident response versus stitching best-of-breed tools to justify full-suite pricing. If Rapid7 can’t show these metrics, churn and deal-size compression risk rising.

Enterprise Procurement Leverage

Large enterprises wield strong procurement leverage, using multi-vendor bake-offs and pushing for SLAs and volume discounts; Gartner reported 48% of security deals in 2024 involved competitive RFPs where price was primary.

Rapid7’s margin pressure hinges on proving ROI: automation and reduced breach risk—IBM’s 2023 Cost of a Data Breach found average savings of 3.58M when breaches were contained by automation—so Rapid7 must quantify similar savings to defend pricing.

Low Switching Costs for SaaS Solutions

The shift to cloud-native security lowers physical switching barriers between vulnerability management and XDR vendors; SaaS models mean no hardware lock-in and vendors like Rapid7 face churn risk—industry SaaS median annual churn ~15% (2024); data migration and retraining still add cost but often under 3 months. Rapid7 must therefore invest in customer success and monthly product releases to keep net retention above 100% and limit defections.

Availability of Alternative Information

In 2025 IT buyers use peer reviews, analyst reports (Gartner, Forrester) and real-time benchmarks to compare Rapid7 to Tenable and CrowdStrike, raising information symmetry and lowering seller informational advantage.

Customers leverage public telemetry and third-party tests—e.g., MITRE ATT&CK evaluations and NSS Labs-style reports—to dispute claims and extract discounts; 42% of enterprises reported negotiating security vendor pricing in 2024.

- High info symmetry vs rivals

- Use of MITRE/NSS-style benchmarks

- 42% of enterprises negotiated pricing in 2024

- Stronger demands for feature SLAs

Influence of Managed Service Providers

MSSPs (managed security service providers) control day-to-day security for ~40–50% of mid-market firms; their platform choices can therefore steer large blocks of customers toward or away from Rapid7.

If a major MSSP standardizes on a rival stack, Rapid7 could lose simultaneous access to thousands of endpoints and a meaningful share of ARR—industry reports estimate MSSP-influenced dealflow represents ~25% of mid-market security spend.

That concentration raises negotiation leverage for MSSPs on pricing, integration and roadmap priorities, increasing churn risk if Rapid7 fails to align with MSSP requirements.

- MSSPs cover ~40–50% mid-market

- MSSP-driven deals ≈25% of mid-market security spend

- Standardization risk: mass customer loss

- Gives MSSPs pricing and roadmap leverage

Rapid7 must prove 22% faster IRR and clear TCO to defend pricing or risk churn

Buyers hold strong leverage: 68% prefer consolidated platforms (end-2025) and large accounts secure ~18% discounts on suites, while 42% negotiated security vendor pricing in 2024; SaaS churn median ~15% (2024) and MSSPs influence ~25% of mid-market spend. Rapid7 must prove 22% faster IRR (incident response) and clear TCO savings to defend pricing and keep net retention >100% or face deal-size compression and churn.

| Metric | Value |

|---|---|

| Platform preference (end-2025) | 68% |

| Avg suite discount (large accounts) | 18% |

| Enterprises negotiating price (2024) | 42% |

| SaaS median churn (2024) | 15% |

| MSSP-influenced spend (mid-market) | 25% |

Full Version Awaits

Rapid7 Porter's Five Forces Analysis

This preview shows the exact Rapid7 Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the final deliverable: the same professionally written file available for instant download upon payment, with comprehensive force-by-force evaluation tailored to Rapid7.