Rapid7 PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, and rapid tech change are reshaping Rapid7’s strategic landscape in our concise PESTLE snapshot—designed for investors and strategists who need timely, actionable insight; purchase the full analysis to access exhaustive, ready-to-use findings and strengthen your decisions instantly.

Political factors

Increased Government Cybersecurity Mandates

Governments are tightening cybersecurity mandates—US federal directives (e.g., 2024 CISA guidance) and EU NIS2 affect public agencies and supply-chain partners, driving compliance spend estimated to reach $188B globally in 2025. Rapid7’s vulnerability management and incident response tools map directly to these requirements, positioning the company to capture recurring demand and contribute to subscription revenue, which was 83% of FY2024 revenue.

Geopolitical Tensions and State-Sponsored Threats

Rising geopolitical instability has driven a 45% year‑over‑year rise in state‑sponsored cyber incidents in 2024, forcing Rapid7 to accelerate threat‑intelligence updates to counter nation‑level tactics targeting corporate and government networks.

Rapid7 must continuously evolve its threat intelligence and SOC capabilities to detect APTs and supply chain intrusions, aligning R&D spend—Rapid7's security research investment rose ~20% in 2024—to stay ahead of sophisticated, politically motivated actors.

Heightened geopolitical tensions boosted global cyber defense budgets to an estimated $190B in 2024, creating tailwinds for Rapid7 by increasing demand for visibility into global attack surfaces and managed detection services.

National Security Trade Restrictions

Trade policies and export controls on sensitive technologies limit Rapid7’s operations in markets like China and Russia; US export rules on cyber tools contributed to a 12% reduction in potential enterprise sales in sanctioned regions in 2024.

Rapid7 must navigate complex regulations restricting advanced encryption and detection tool sales to specific jurisdictions, adding compliance costs that rose ~8% to its FY2025 operating expenses.

Shifts in US-China diplomatic tensions can quickly shrink the TAM for American security providers; analysts estimate up to $400M revenue exposure for mid-cap vendors if access to key APAC markets is lost.

Focus on Public-Private Partnerships

Political emphasis on public-private partnerships, led by agencies like CISA, has increased funding and information-sharing mandates; in 2024 CISA expanded its Cybersecurity Advisory program and threat-sharing initiatives reaching hundreds of private partners—Rapid7's active participation enhances its reputation and provides access to critical threat telemetry.

These collaborations are vital to build unified defenses against systemic cyber risks that could threaten national economic stability, with US federal cybersecurity spending projected at over $20B in 2025 supporting such initiatives.

- Rapid7 gains trusted-industry status via CISA partnerships

- Access to shared threat telemetry improves detection and response

- Aligns with >$20B federal cybersecurity investment trajectory

Data Sovereignty and Localization Policies

Many countries now mandate data localization—over 60 nations had laws by 2024—forcing Rapid7 to rework cloud deployments and regional data centers to meet sovereignty rules and preserve revenue streams in markets like EU, India, and China.

Noncompliance risks blocking access to markets that accounted for an estimated 20–30% of global cybersecurity spend in 2024, jeopardizing subscription and managed-services growth.

- 60+ countries with localization laws by 2024

- EU/India/China critical for 20–30% of cybersecurity market

- Requires localized cloud, data processing, and contractual changes

Compliance boom fuels Rapid7 subscriptions amid geopolitical headwinds and $400M APAC risk

Political drivers—stricter US/EU mandates (NIS2, CISA 2024) and 60+ data‑localization laws—boost compliance spend (estimated $188B global 2025) and align with Rapid7’s subscription revenue (83% FY2024), while geopolitics and export controls cut ~12% sales in sanctioned markets and create ~$400M APAC exposure; federal cyber budgets (~$20B US 2025) and $190B global defense spend 2024 expand MSS/visibility demand.

| Metric | Value |

|---|---|

| Subscription revenue (FY2024) | 83% |

| Global compliance spend (2025 est.) | $188B |

| US federal cyber budget (2025 est.) | $20B |

| Global cyber defense spend (2024) | $190B |

| Countries with localization laws (2024) | 60+ |

| Sanctioned-market sales reduction (2024) | 12% |

| Potential APAC revenue exposure | $400M |

What is included in the product

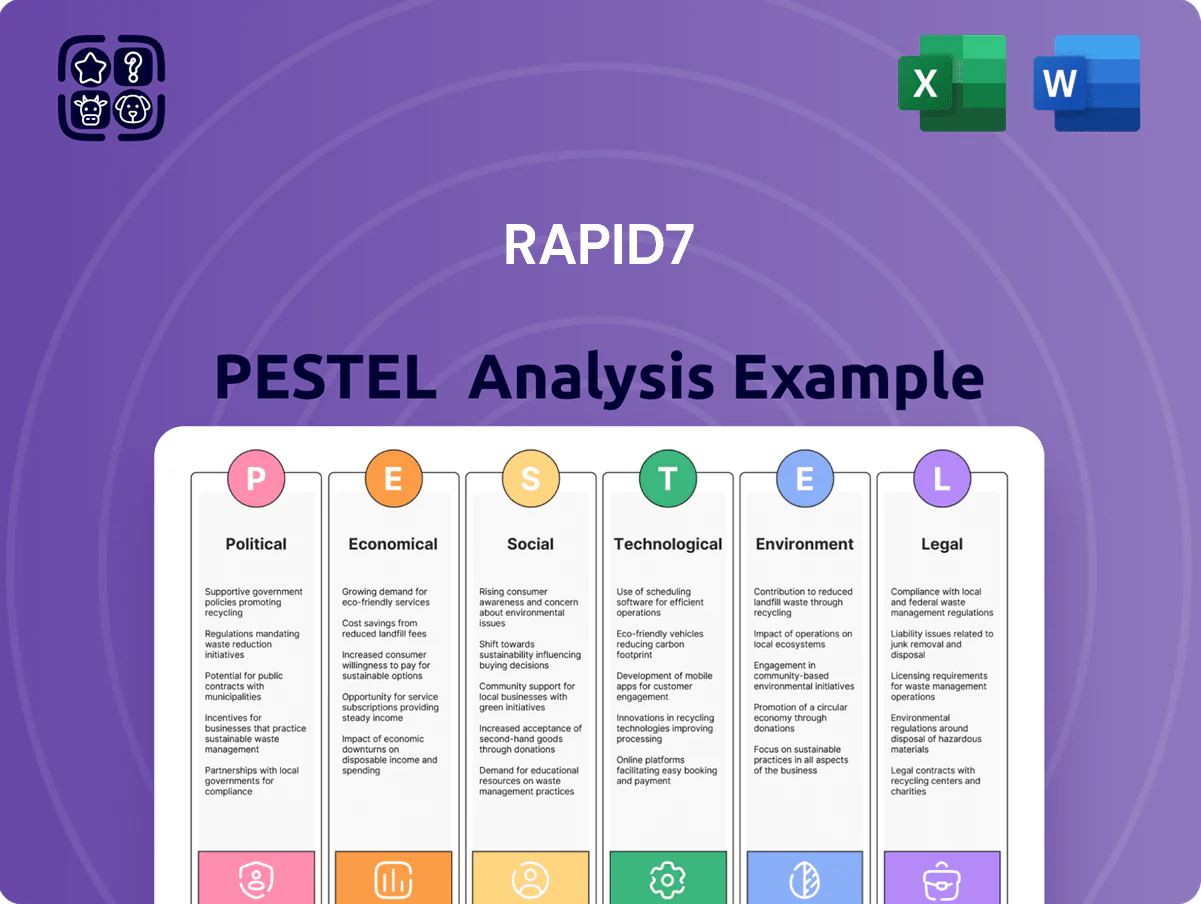

Explores how external macro-environmental factors uniquely affect Rapid7 across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Concise PESTLE summary tailored for Rapid7 that highlights external threats and opportunities in plain language, making it easy to drop into slides or share for quick alignment during security strategy sessions.

Economic factors

Enterprise Cybersecurity Spending Resilience

Despite macro volatility, cybersecurity stayed prioritized: 2024 surveys show 73% of enterprises maintained or increased security budgets and average breach costs reached $4.45M in 2023, supporting non-discretionary spend. Rapid7 benefits as customers treat its services as essential operational spend, boosting subscription renewals. This resilience translated into steadier ARR growth versus cyclical tech peers, with cybersecurity spending forecasted to grow ~9% CAGR through 2026.

Impact of Global Inflation on SaaS Pricing

Persistent global inflation—US CPI 3.4% in 2024 and Eurozone HICP 2.9%—raises cloud, labor, and security operations costs for SaaS vendors, pressuring Rapid7 to consider subscription price increases; in 2024 Rapid7 reported Opex growth of ~18% YoY, narrowing gross margins. Rapid7 must balance margin protection with competitive pricing to retain cost-sensitive mid-market clients, which accounted for roughly half of its ARR growth in FY2024.

Market Consolidation and M&A Activity

The cybersecurity sector saw $61.2B in global M&A value in 2023 with deal volume up 18% year-over-year, driven by large vendors buying niche startups to create integrated platforms; Rapid7 needs to assess acquisitions to close gaps in cloud security and XDR offerings to remain competitive.

Higher U.S. Fed rates and a 40% decline in VC funding to cybersecurity startups in 2023 constrain deal flow and valuations, so Rapid7 must balance cash, debt costs and a $1.2B market cap context when timing deals.

Cybersecurity Talent Shortage Costs

A global shortage of cybersecurity professionals has pushed median security engineer salaries up 18-25% between 2020–2024, raising labor costs for Rapid7 and its customers and contributing to higher churn.

Rapid7 emphasizes automation and intuitive UIs—reducing mean time to detect/respond and enabling smaller teams to manage complex tasks—supporting cost-per-incident savings and product-led growth.

Rising turnover and salary inflation in tech force Rapid7 to prioritize retention programs and continuous product innovation to protect margins and customer ROI.

- Salary inflation 18–25% (2020–2024)

- Automation reduces incident handling headcount

- Retention and product innovation mitigate margin pressure

Shift Toward Platform Consolidation

Economic pressures push firms to consolidate security stacks; 2024 surveys show 68% of enterprises prioritize integrated platforms to cut vendor count and OpEx.

Rapid7’s Insight platform bundles vulnerability management, SIEM, and endpoint detection, aligning with buyers seeking single-vendor suites to lower integration costs.

Analysts estimate consolidated platforms can reduce total security spend by 15–30% vs. fragmented point solutions, favoring vendors proving ROI.

- 68% of enterprises favor integrated security platforms (2024 survey)

- Rapid7 Insight combines VM, SIEM, EDR in one environment

- Consolidation can cut security spend 15–30%

- Vendors showing clear ROI gain market share

Cybersecurity resilience: Budgets hold, breaches cost $4.45M, Rapid7 benefits

Economic resilience in cybersecurity: 73% of firms kept/increased security budgets in 2024; avg breach cost $4.45M (2023) supports steady ARR for Rapid7 and ~9% cybersecurity spend CAGR to 2026. Inflation (US CPI 3.4% 2024) drove Rapid7 Opex +18% YoY, tightening margins; labor inflation raised security engineer pay 18–25% (2020–24). Platform consolidation favored Rapid7—68% of enterprises prefer integrated suites (2024).

| Metric | Value |

|---|---|

| Enterprise budget stance (2024) | 73% maintained/increased |

| Avg breach cost | $4.45M (2023) |

| Cybersecurity spend CAGR | ~9% to 2026 |

| US CPI | 3.4% (2024) |

| Rapid7 Opex growth | ~18% YoY (2024) |

| Security engineer pay rise | 18–25% (2020–24) |

| Preference for integrated platforms | 68% (2024) |

Preview the Actual Deliverable

Rapid7 PESTLE Analysis

The preview shown here is the exact Rapid7 PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressures, and rapid tech change are reshaping Rapid7’s strategic landscape in our concise PESTLE snapshot—designed for investors and strategists who need timely, actionable insight; purchase the full analysis to access exhaustive, ready-to-use findings and strengthen your decisions instantly.

Political factors

Increased Government Cybersecurity Mandates

Governments are tightening cybersecurity mandates—US federal directives (e.g., 2024 CISA guidance) and EU NIS2 affect public agencies and supply-chain partners, driving compliance spend estimated to reach $188B globally in 2025. Rapid7’s vulnerability management and incident response tools map directly to these requirements, positioning the company to capture recurring demand and contribute to subscription revenue, which was 83% of FY2024 revenue.

Geopolitical Tensions and State-Sponsored Threats

Rising geopolitical instability has driven a 45% year‑over‑year rise in state‑sponsored cyber incidents in 2024, forcing Rapid7 to accelerate threat‑intelligence updates to counter nation‑level tactics targeting corporate and government networks.

Rapid7 must continuously evolve its threat intelligence and SOC capabilities to detect APTs and supply chain intrusions, aligning R&D spend—Rapid7's security research investment rose ~20% in 2024—to stay ahead of sophisticated, politically motivated actors.

Heightened geopolitical tensions boosted global cyber defense budgets to an estimated $190B in 2024, creating tailwinds for Rapid7 by increasing demand for visibility into global attack surfaces and managed detection services.

National Security Trade Restrictions

Trade policies and export controls on sensitive technologies limit Rapid7’s operations in markets like China and Russia; US export rules on cyber tools contributed to a 12% reduction in potential enterprise sales in sanctioned regions in 2024.

Rapid7 must navigate complex regulations restricting advanced encryption and detection tool sales to specific jurisdictions, adding compliance costs that rose ~8% to its FY2025 operating expenses.

Shifts in US-China diplomatic tensions can quickly shrink the TAM for American security providers; analysts estimate up to $400M revenue exposure for mid-cap vendors if access to key APAC markets is lost.

Focus on Public-Private Partnerships

Political emphasis on public-private partnerships, led by agencies like CISA, has increased funding and information-sharing mandates; in 2024 CISA expanded its Cybersecurity Advisory program and threat-sharing initiatives reaching hundreds of private partners—Rapid7's active participation enhances its reputation and provides access to critical threat telemetry.

These collaborations are vital to build unified defenses against systemic cyber risks that could threaten national economic stability, with US federal cybersecurity spending projected at over $20B in 2025 supporting such initiatives.

- Rapid7 gains trusted-industry status via CISA partnerships

- Access to shared threat telemetry improves detection and response

- Aligns with >$20B federal cybersecurity investment trajectory

Data Sovereignty and Localization Policies

Many countries now mandate data localization—over 60 nations had laws by 2024—forcing Rapid7 to rework cloud deployments and regional data centers to meet sovereignty rules and preserve revenue streams in markets like EU, India, and China.

Noncompliance risks blocking access to markets that accounted for an estimated 20–30% of global cybersecurity spend in 2024, jeopardizing subscription and managed-services growth.

- 60+ countries with localization laws by 2024

- EU/India/China critical for 20–30% of cybersecurity market

- Requires localized cloud, data processing, and contractual changes

Compliance boom fuels Rapid7 subscriptions amid geopolitical headwinds and $400M APAC risk

Political drivers—stricter US/EU mandates (NIS2, CISA 2024) and 60+ data‑localization laws—boost compliance spend (estimated $188B global 2025) and align with Rapid7’s subscription revenue (83% FY2024), while geopolitics and export controls cut ~12% sales in sanctioned markets and create ~$400M APAC exposure; federal cyber budgets (~$20B US 2025) and $190B global defense spend 2024 expand MSS/visibility demand.

| Metric | Value |

|---|---|

| Subscription revenue (FY2024) | 83% |

| Global compliance spend (2025 est.) | $188B |

| US federal cyber budget (2025 est.) | $20B |

| Global cyber defense spend (2024) | $190B |

| Countries with localization laws (2024) | 60+ |

| Sanctioned-market sales reduction (2024) | 12% |

| Potential APAC revenue exposure | $400M |

What is included in the product

Explores how external macro-environmental factors uniquely affect Rapid7 across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Concise PESTLE summary tailored for Rapid7 that highlights external threats and opportunities in plain language, making it easy to drop into slides or share for quick alignment during security strategy sessions.

Economic factors

Enterprise Cybersecurity Spending Resilience

Despite macro volatility, cybersecurity stayed prioritized: 2024 surveys show 73% of enterprises maintained or increased security budgets and average breach costs reached $4.45M in 2023, supporting non-discretionary spend. Rapid7 benefits as customers treat its services as essential operational spend, boosting subscription renewals. This resilience translated into steadier ARR growth versus cyclical tech peers, with cybersecurity spending forecasted to grow ~9% CAGR through 2026.

Impact of Global Inflation on SaaS Pricing

Persistent global inflation—US CPI 3.4% in 2024 and Eurozone HICP 2.9%—raises cloud, labor, and security operations costs for SaaS vendors, pressuring Rapid7 to consider subscription price increases; in 2024 Rapid7 reported Opex growth of ~18% YoY, narrowing gross margins. Rapid7 must balance margin protection with competitive pricing to retain cost-sensitive mid-market clients, which accounted for roughly half of its ARR growth in FY2024.

Market Consolidation and M&A Activity

The cybersecurity sector saw $61.2B in global M&A value in 2023 with deal volume up 18% year-over-year, driven by large vendors buying niche startups to create integrated platforms; Rapid7 needs to assess acquisitions to close gaps in cloud security and XDR offerings to remain competitive.

Higher U.S. Fed rates and a 40% decline in VC funding to cybersecurity startups in 2023 constrain deal flow and valuations, so Rapid7 must balance cash, debt costs and a $1.2B market cap context when timing deals.

Cybersecurity Talent Shortage Costs

A global shortage of cybersecurity professionals has pushed median security engineer salaries up 18-25% between 2020–2024, raising labor costs for Rapid7 and its customers and contributing to higher churn.

Rapid7 emphasizes automation and intuitive UIs—reducing mean time to detect/respond and enabling smaller teams to manage complex tasks—supporting cost-per-incident savings and product-led growth.

Rising turnover and salary inflation in tech force Rapid7 to prioritize retention programs and continuous product innovation to protect margins and customer ROI.

- Salary inflation 18–25% (2020–2024)

- Automation reduces incident handling headcount

- Retention and product innovation mitigate margin pressure

Shift Toward Platform Consolidation

Economic pressures push firms to consolidate security stacks; 2024 surveys show 68% of enterprises prioritize integrated platforms to cut vendor count and OpEx.

Rapid7’s Insight platform bundles vulnerability management, SIEM, and endpoint detection, aligning with buyers seeking single-vendor suites to lower integration costs.

Analysts estimate consolidated platforms can reduce total security spend by 15–30% vs. fragmented point solutions, favoring vendors proving ROI.

- 68% of enterprises favor integrated security platforms (2024 survey)

- Rapid7 Insight combines VM, SIEM, EDR in one environment

- Consolidation can cut security spend 15–30%

- Vendors showing clear ROI gain market share

Cybersecurity resilience: Budgets hold, breaches cost $4.45M, Rapid7 benefits

Economic resilience in cybersecurity: 73% of firms kept/increased security budgets in 2024; avg breach cost $4.45M (2023) supports steady ARR for Rapid7 and ~9% cybersecurity spend CAGR to 2026. Inflation (US CPI 3.4% 2024) drove Rapid7 Opex +18% YoY, tightening margins; labor inflation raised security engineer pay 18–25% (2020–24). Platform consolidation favored Rapid7—68% of enterprises prefer integrated suites (2024).

| Metric | Value |

|---|---|

| Enterprise budget stance (2024) | 73% maintained/increased |

| Avg breach cost | $4.45M (2023) |

| Cybersecurity spend CAGR | ~9% to 2026 |

| US CPI | 3.4% (2024) |

| Rapid7 Opex growth | ~18% YoY (2024) |

| Security engineer pay rise | 18–25% (2020–24) |

| Preference for integrated platforms | 68% (2024) |

Preview the Actual Deliverable

Rapid7 PESTLE Analysis

The preview shown here is the exact Rapid7 PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.