Razor Energy PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and environmental regulations are reshaping Razor Energy’s prospects with our concise PESTLE snapshot—designed for investors and strategists who need quick, actionable insight; purchase the full analysis to access the detailed trends, risk scores, and strategic recommendations you can apply immediately.

Political factors

Federal and Provincial Regulatory Friction

The federal-provincial clash over emissions caps, intensified by Alberta's Sovereignty Act and federal methane rules, creates regulatory friction that directly impacts Razor Energy's capital planning; Alberta produced 4.3 million bbl/d of oil in 2024, and sector compliance costs are estimated at CAD 1.5–2.5 billion industry-wide in 2024–25, heightening investment uncertainty.

Green Energy Subsidy Alignment

Razor Energy, via FutEra, captures federal and provincial tax credits—including the federal Clean Technology Investment Tax Credit offering up to 30% ITC for qualifying projects—supporting its co-generation and geothermal CAPEX; in 2024 FutEra secured roughly CAD 25–40m in incentives across projects, materially improving IRRs.

Indigenous Consultation and Participation

By 2025 Western Canada tightened mandates: 78% of major energy project approvals now require documented Indigenous agreements or enhanced consultation records; Razor Energy must align projects with the Duty to Consult framework and negotiate complex land-use agreements covering over 1.2m hectares in Alberta and B.C.

Carbon Pricing Trajectory

The federal carbon tax is on a legislated glide path to C$170/tonne by 2030, imposing rising costs—estimated adds of C$40–C$60m annualized for mid-sized oil producers like Razor without mitigation.

Razor leverages on-site co-generation to cut emissions intensity and avoid a portion of tax exposure, but parliamentary debate and potential leadership changes make future carbon pricing volatile and could rapidly alter cost forecasts.

- 2030 target: C$170/tonne

- Estimated corporate exposure: C$40–C$60m/year

- Mitigation: co-generation reduces taxable emissions share

- Risk: policy shifts from federal leadership changes

Geopolitical Influence on Energy Security

- Domestic political support for production up

- Regulatory scrutiny on emissions and methane intensity

- Alberta oil output ~4.3 million bbl/d (2024)

- Canada 2030 NDC: 40–45% below 2005; carbon price ~CAD 80/t (2025)

Razor faces CAD40–60M/yr carbon hit as Alberta tensions and rising C$170/t price bite

Federal-provincial tensions over emissions caps and Alberta Sovereignty actions raise regulatory risk for Razor; Alberta output ~4.3m bbl/d (2024) and industry compliance costs CAD 1.5–2.5b (2024–25). Carbon pricing on path to C$170/t by 2030 (C$80/t in 2025) could cost Razor ~C$40–60m/yr without mitigation; FutEra captured ~C$25–40m incentives in 2024, easing CAPEX.

| Metric | Value |

|---|---|

| Alberta oil (2024) | 4.3m bbl/d |

| Industry compliance cost (2024–25) | CAD 1.5–2.5b |

| Carbon price (2025) | CAD 80/t |

| Carbon price target (2030) | CAD 170/t |

| Razor exposure | CAD 40–60m/yr |

| FutEra incentives (2024) | CAD 25–40m |

What is included in the product

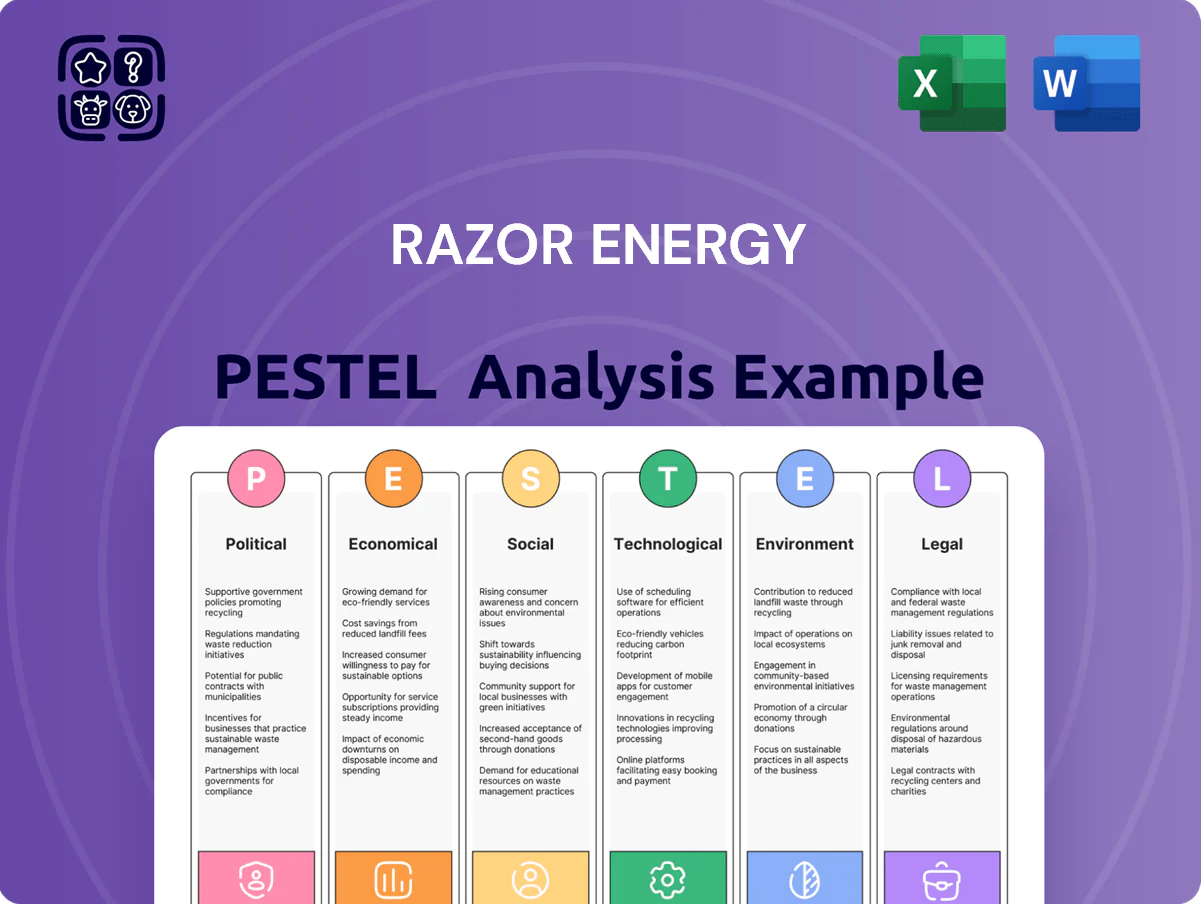

Explores how external macro-environmental factors uniquely affect Razor Energy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for Razor Energy that highlights key external risks and opportunities, ready to drop into presentations or share across teams for fast alignment during strategic planning.

Economic factors

Commodity Price Volatility

Fluctuations in Western Canadian Select (WCS) and AECO natural gas prices remain Razor Energy’s primary economic drivers; AECO averaged about C$2.35/GJ in 2024 versus a five-year pre-2024 average near C$2.90/GJ, stressing revenue sensitivity.

Razor uses hedges covering roughly 40%–60% of production; nevertheless, 2024–25 global supply shifts and recession risks can sharply reduce cash flow despite hedging.

By end-2025, power generation revenue—up ~35% year-over-year in 2024 and comprising ~22% of EBITDA guidance—acts as a growing buffer against commodity cycles.

Capital Market Access for Small-Cap Producers

Access to traditional equity and debt has tightened for mid-to-small-cap oil and gas firms as ESG funds now represent about 40% of global AUM (~US$150 trillion in 2024), pressuring investors to cut fossil-fuel exposure; Razor Energy must show a clear profitability and emissions-reduction roadmap to gain institutional capital. Institutional fossil-fuel allocations fell ~12% from 2019–2023, raising cost of capital for peers by 200–400 bps. Consequently, Razor is pursuing alternative financing and JV structures for green projects, aligning with lenders that reported a 25% increase in green-linked loan issuance in 2024.

Inflationary Pressures on Field Operations

Persistent inflation in labor and equipment has pushed Field Operations costs in the Western Canadian Sedimentary Basin up sharply; WCSB service costs rose about 12%–18% in 2024 versus 2021, increasing maintenance spend on aging assets.

Razor Energy faces higher wages for specialized technicians—average oilfield technician pay grew ~15% 2022–2024—and a 20%+ rise in key materials and rig rental rates.

These pressures elevate OPEX for both oil extraction and green-energy retrofits, squeezing margins on legacy properties and making cost management and targeted capex crucial to preserve cashflow.

Interest Rate Environment

Higher-for-longer rates in late 2025—Bank of Canada at 5.0% and comparable global policy rates—raise Razor Energy’s cost of borrowing, pressuring servicing of its CAD 420m net debt and capital for FutEra expansions and oil-asset buys.

Razor emphasizes deleveraging: cutting capex 18% YoY and targeting net-debt/EBITDA <2.0x to preserve liquidity amid tighter credit and elevated interest expense.

- Bank rates ~5.0% (late 2025)

- Net debt ~CAD 420m

- Capex reduced 18% YoY

- Target net-debt/EBITDA <2.0x

Economic Viability of Green Diversification

The economic viability of Razor Energy's green diversification increasingly depends on revenues from its co-generation and planned geothermal projects, which in 2025 could account for an estimated 12–18% of total EBITDA if merchant power prices average CAD 80–100/MWh in Alberta.

These projects compete with wind, solar and gas-fired plants in Alberta’s market where 2024 merchant power volatility ranged ±30% from the annual mean and spot prices spiked to CAD 999/MWh during extreme winter events, creating upside and downside risk to cash flows.

- Projected contribution to EBITDA: 12–18% (2025 scenario)

- Alberta merchant power average range: CAD 80–100/MWh (2025 estimate)

- Price volatility: ±30% in 2024; spot spikes to CAD 999/MWh observed

- Competition: wind, solar, gas plants affecting dispatch and margins

Balanced hedges, lower capex, green projects to drive EBITDA amid commodity sensitivity

Commodity-price sensitivity (AECO C$2.35/GJ 2024), hedges 40%–60%, power revenue ~22% EBITDA (2024), net debt CAD420m, BoC ~5.0% (late-2025), capex −18% YoY, target net-debt/EBITDA <2.0x; green projects projected 12–18% EBITDA (2025) if merchant power CAD80–100/MWh; service costs +12–18% (2024).

| Metric | Value |

|---|---|

| AECO 2024 | C$2.35/GJ |

| Net debt | CAD420m |

| BoC | ~5.0% |

| Power EBITDA | 22% |

Same Document Delivered

Razor Energy PESTLE Analysis

The preview shown here is the exact Razor Energy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and environmental regulations are reshaping Razor Energy’s prospects with our concise PESTLE snapshot—designed for investors and strategists who need quick, actionable insight; purchase the full analysis to access the detailed trends, risk scores, and strategic recommendations you can apply immediately.

Political factors

Federal and Provincial Regulatory Friction

The federal-provincial clash over emissions caps, intensified by Alberta's Sovereignty Act and federal methane rules, creates regulatory friction that directly impacts Razor Energy's capital planning; Alberta produced 4.3 million bbl/d of oil in 2024, and sector compliance costs are estimated at CAD 1.5–2.5 billion industry-wide in 2024–25, heightening investment uncertainty.

Green Energy Subsidy Alignment

Razor Energy, via FutEra, captures federal and provincial tax credits—including the federal Clean Technology Investment Tax Credit offering up to 30% ITC for qualifying projects—supporting its co-generation and geothermal CAPEX; in 2024 FutEra secured roughly CAD 25–40m in incentives across projects, materially improving IRRs.

Indigenous Consultation and Participation

By 2025 Western Canada tightened mandates: 78% of major energy project approvals now require documented Indigenous agreements or enhanced consultation records; Razor Energy must align projects with the Duty to Consult framework and negotiate complex land-use agreements covering over 1.2m hectares in Alberta and B.C.

Carbon Pricing Trajectory

The federal carbon tax is on a legislated glide path to C$170/tonne by 2030, imposing rising costs—estimated adds of C$40–C$60m annualized for mid-sized oil producers like Razor without mitigation.

Razor leverages on-site co-generation to cut emissions intensity and avoid a portion of tax exposure, but parliamentary debate and potential leadership changes make future carbon pricing volatile and could rapidly alter cost forecasts.

- 2030 target: C$170/tonne

- Estimated corporate exposure: C$40–C$60m/year

- Mitigation: co-generation reduces taxable emissions share

- Risk: policy shifts from federal leadership changes

Geopolitical Influence on Energy Security

- Domestic political support for production up

- Regulatory scrutiny on emissions and methane intensity

- Alberta oil output ~4.3 million bbl/d (2024)

- Canada 2030 NDC: 40–45% below 2005; carbon price ~CAD 80/t (2025)

Razor faces CAD40–60M/yr carbon hit as Alberta tensions and rising C$170/t price bite

Federal-provincial tensions over emissions caps and Alberta Sovereignty actions raise regulatory risk for Razor; Alberta output ~4.3m bbl/d (2024) and industry compliance costs CAD 1.5–2.5b (2024–25). Carbon pricing on path to C$170/t by 2030 (C$80/t in 2025) could cost Razor ~C$40–60m/yr without mitigation; FutEra captured ~C$25–40m incentives in 2024, easing CAPEX.

| Metric | Value |

|---|---|

| Alberta oil (2024) | 4.3m bbl/d |

| Industry compliance cost (2024–25) | CAD 1.5–2.5b |

| Carbon price (2025) | CAD 80/t |

| Carbon price target (2030) | CAD 170/t |

| Razor exposure | CAD 40–60m/yr |

| FutEra incentives (2024) | CAD 25–40m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Razor Energy across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by relevant data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for Razor Energy that highlights key external risks and opportunities, ready to drop into presentations or share across teams for fast alignment during strategic planning.

Economic factors

Commodity Price Volatility

Fluctuations in Western Canadian Select (WCS) and AECO natural gas prices remain Razor Energy’s primary economic drivers; AECO averaged about C$2.35/GJ in 2024 versus a five-year pre-2024 average near C$2.90/GJ, stressing revenue sensitivity.

Razor uses hedges covering roughly 40%–60% of production; nevertheless, 2024–25 global supply shifts and recession risks can sharply reduce cash flow despite hedging.

By end-2025, power generation revenue—up ~35% year-over-year in 2024 and comprising ~22% of EBITDA guidance—acts as a growing buffer against commodity cycles.

Capital Market Access for Small-Cap Producers

Access to traditional equity and debt has tightened for mid-to-small-cap oil and gas firms as ESG funds now represent about 40% of global AUM (~US$150 trillion in 2024), pressuring investors to cut fossil-fuel exposure; Razor Energy must show a clear profitability and emissions-reduction roadmap to gain institutional capital. Institutional fossil-fuel allocations fell ~12% from 2019–2023, raising cost of capital for peers by 200–400 bps. Consequently, Razor is pursuing alternative financing and JV structures for green projects, aligning with lenders that reported a 25% increase in green-linked loan issuance in 2024.

Inflationary Pressures on Field Operations

Persistent inflation in labor and equipment has pushed Field Operations costs in the Western Canadian Sedimentary Basin up sharply; WCSB service costs rose about 12%–18% in 2024 versus 2021, increasing maintenance spend on aging assets.

Razor Energy faces higher wages for specialized technicians—average oilfield technician pay grew ~15% 2022–2024—and a 20%+ rise in key materials and rig rental rates.

These pressures elevate OPEX for both oil extraction and green-energy retrofits, squeezing margins on legacy properties and making cost management and targeted capex crucial to preserve cashflow.

Interest Rate Environment

Higher-for-longer rates in late 2025—Bank of Canada at 5.0% and comparable global policy rates—raise Razor Energy’s cost of borrowing, pressuring servicing of its CAD 420m net debt and capital for FutEra expansions and oil-asset buys.

Razor emphasizes deleveraging: cutting capex 18% YoY and targeting net-debt/EBITDA <2.0x to preserve liquidity amid tighter credit and elevated interest expense.

- Bank rates ~5.0% (late 2025)

- Net debt ~CAD 420m

- Capex reduced 18% YoY

- Target net-debt/EBITDA <2.0x

Economic Viability of Green Diversification

The economic viability of Razor Energy's green diversification increasingly depends on revenues from its co-generation and planned geothermal projects, which in 2025 could account for an estimated 12–18% of total EBITDA if merchant power prices average CAD 80–100/MWh in Alberta.

These projects compete with wind, solar and gas-fired plants in Alberta’s market where 2024 merchant power volatility ranged ±30% from the annual mean and spot prices spiked to CAD 999/MWh during extreme winter events, creating upside and downside risk to cash flows.

- Projected contribution to EBITDA: 12–18% (2025 scenario)

- Alberta merchant power average range: CAD 80–100/MWh (2025 estimate)

- Price volatility: ±30% in 2024; spot spikes to CAD 999/MWh observed

- Competition: wind, solar, gas plants affecting dispatch and margins

Balanced hedges, lower capex, green projects to drive EBITDA amid commodity sensitivity

Commodity-price sensitivity (AECO C$2.35/GJ 2024), hedges 40%–60%, power revenue ~22% EBITDA (2024), net debt CAD420m, BoC ~5.0% (late-2025), capex −18% YoY, target net-debt/EBITDA <2.0x; green projects projected 12–18% EBITDA (2025) if merchant power CAD80–100/MWh; service costs +12–18% (2024).

| Metric | Value |

|---|---|

| AECO 2024 | C$2.35/GJ |

| Net debt | CAD420m |

| BoC | ~5.0% |

| Power EBITDA | 22% |

Same Document Delivered

Razor Energy PESTLE Analysis

The preview shown here is the exact Razor Energy PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.