RBC Porter's Five Forces Analysis

Don't Miss the Bigger Picture

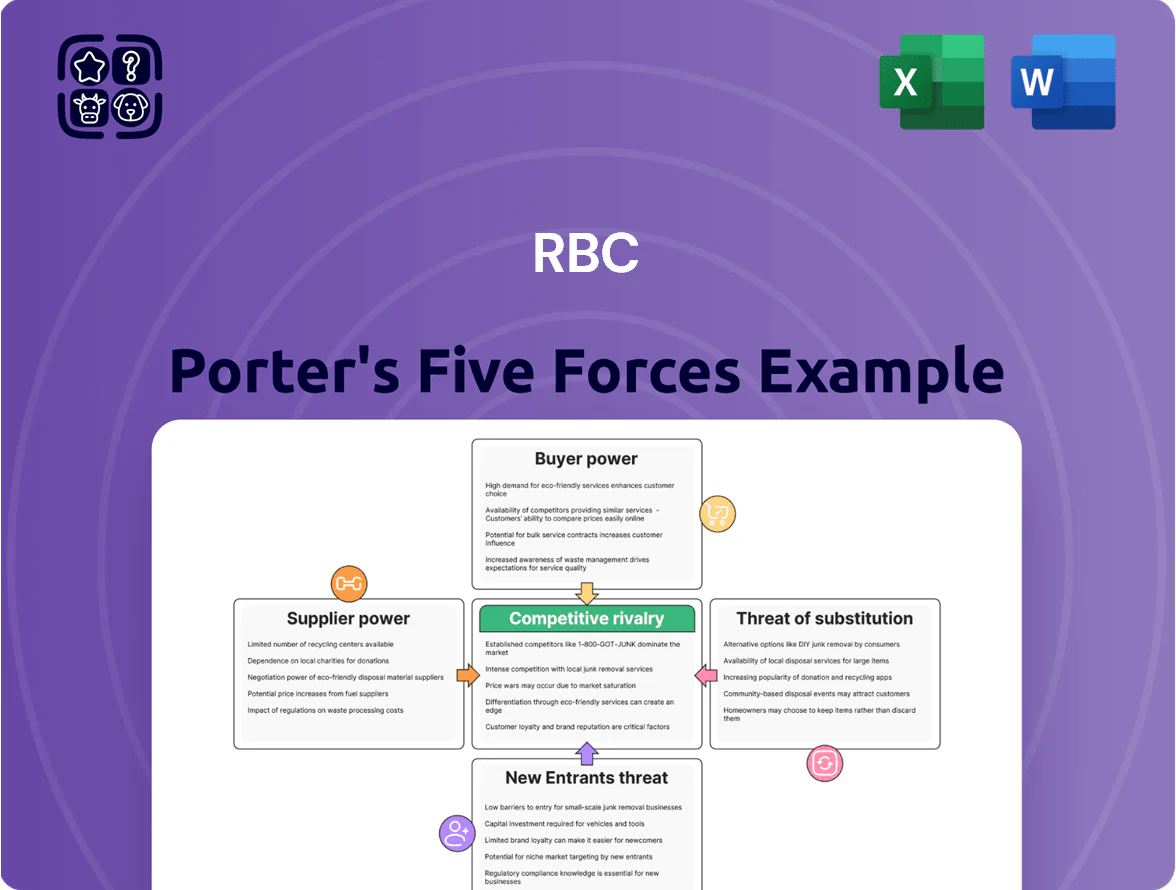

RBC's Porter's Five Forces snapshot highlights competitive rivalry, regulatory barriers, and evolving buyer expectations shaping its banking moat—yet only scratches the surface.

The full report quantifies each force, maps supplier and substitute risks, and reveals strategic levers RBC can use to defend market share and margins.

Unlock the complete, consultant-grade analysis with visuals, force ratings, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of Specialized Labor and Fintech Talent

RBC relies on specialized suppliers—finance, data science, and cybersecurity professionals—whose scarcity gives them bargaining power; by Q4 2025 AI specialists commanded median Canadian salaries of CAD 140k–180k and cloud engineers CAD 130k–160k, pressuring firms to raise pay.

To keep digital transformation on track, RBC must match market offers with competitive total-compensation packages and upskilling budgets; turnover among tech roles rose ~12% in 2024, so retention spending directly affects project timelines and costs.

Dependency on Global Technology and Cloud Providers

RBC depends on a few dominant cloud and tech providers—Microsoft, Amazon Web Services, and Google Cloud—for core banking, risking supplier power; Gartner estimated enterprise cloud spending grew 22% in 2024, concentrating bargaining leverage with hyperscalers.

Switching costs are high: migrating petabytes, regulatory recertification, and multi-year contracts drive lock-in; a 2023 Accenture survey found 68% of banks cite cloud migration risk as a top operational concern.

Cost of Capital and Regulatory Liquidity Requirements

Suppliers of capital, notably central banks and institutional depositors, push RBC's margins via interest-rate swings and liquidity access; Bank of Canada terminal-rate guidance at 4.5% in late 2025 sets benchmark funding costs for RBC's wholesale borrowing.

Regulatory liquidity rules—LCR (liquidity coverage ratio) >100% and CET1 ratio target ~12.5% for Canadian banks—constrain RBC's funding mix and reduce yield-enhancing risk-taking.

Reliance on Specialized Financial Data and Infrastructure

Market data vendors Bloomberg, Refinitiv (Reuters), and S&P/Moody’s are core inputs for RBC’s capital markets and wealth units; Bloomberg’s terminal revenue reached about $11.7B in 2023, showing vendor scale and pricing leverage.

These suppliers sit in an oligopoly, giving RBC few substitutes for high-quality, real-time price feeds and credit data; switching costs and integration make alternatives costly.

Because regulators and trading systems require these feeds for compliance and execution, suppliers keep steady pricing power—vendor fees rose mid-single digits annually through 2024.

- Critical vendors: Bloomberg, Refinitiv, S&P, Moody’s

- Bloomberg 2023 revenue ~11.7B, signalling scale

- Oligopoly => limited substitutes, high switching costs

- Compliance/trading needs sustain steady vendor pricing

Outsourced Operational and Professional Services

RBC uses third-party vendors for back-office operations, legal counsel, and audits; global scale and regulatory expertise limit suitable suppliers to a handful of elite firms, raising switching costs.

Dependence on integrated services creates moderate supplier bargaining power: large vendors can command premium fees, though RBC’s scale and ~$1.6 trillion AUM (2025) give it negotiation leverage.

- Few elite global providers

- High switching costs due to integration

- Moderate supplier leverage vs RBC scale

RBC Faces Rising Supplier Power: Talent, Hyperscalers & Data Vendors Squeeze Costs

RBC faces moderate-to-high supplier power: scarce tech talent (AI median CAD140–180k in 2025) and hyperscaler dependence (AWS/Google/Microsoft; enterprise cloud spend +22% in 2024) raise costs; market-data vendors (Bloomberg rev ~$11.7B 2023) and elite service firms command premiums, though RBC’s ~CAD1.6T AUM (2025) gives negotiation leverage.

| Supplier | Key stat | Impact |

|---|---|---|

| AI/Cloud talent | CAD140–180k; cloud eng CAD130–160k (2025) | Higher wage/retention costs |

| Hyperscalers | Cloud spend +22% (2024) | Concentration risk |

| Market data | Bloomberg rev ~$11.7B (2023) | Pricing power |

| RBC scale | ~CAD1.6T AUM (2025) | Negotiation leverage |

What is included in the product

Provides a focused Porter's Five Forces assessment tailored to RBC, revealing competitive pressures, buyer and supplier influence, entry barriers, substitute risks, and strategic levers to safeguard market position.

A concise Porter's Five Forces one-sheet for RBC that highlights competitive pressures and strategic levers—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

Low Switching Costs in Retail Banking

Individual consumers in 2025 use digital tools and open banking APIs to move funds quickly; Canada’s Open Banking readiness index rose to 72/100 in 2024, and 38% of Canadians used account aggregation in 2024, so switching friction is low. This forces RBC to match market rates—its 2025 savings rates must remain within ~20–50 bps of peers—and keep service quality high to avoid churn.

High Price Sensitivity in Mortgage and Loan Products

Borrowers show high price sensitivity: a 2024 J.D. Power survey found 62% of mortgage shoppers prioritized lowest APR, so a 50 bps rate gap can swing applications away from RBC Royal Bank of Canada. In Canada’s 2025 market, average posted mortgage spreads narrowed to ~120 bps, limiting RBC’s premium pricing power. To compete, RBC often deploys promotional rates, cashback offers, or bundled advice services to retain volume and protect NIM.

Demands of High-Net-Worth Wealth Management Clients

Wealth management and institutional clients wield strong bargaining power at RBC because the top 1% of clients often hold >40% of private-client AUM; in 2024 RBC reported C$1.6 trillion in total AUM across wealth and asset management, concentrating negotiating leverage. These sophisticated investors demand tailored service, fee discounts (often 25–50 bps lower for large mandates), and access to private equity, real estate, and hedge funds. RBC must keep adding bespoke products and lower-cost fee tiers or risk migration to boutiques that won 12–18% market share gains in H1 2024.

Influence of Corporate and Institutional Borrowers

Large corporates access capital markets or multiple banks, letting them force down arranger fees; RBC lost share in global loan syndication to U.S. peers in 2024, dropping to 5.1% of global bookrunner volume (Refinitiv).

RBC often accepts thinner margins to keep strategic relationships—corporate clients generated ~28% of RBC Capital Markets revenue in FY2024, so retention trumps short-term fee gains.

- Clients can avoid banks via markets

- Competition squeezes arranger fees

- RBC accepts lower margins to retain top clients

Impact of Consumer Advocacy and Transparency

In 2025 increased transparency via social media and comparison sites lets customers spot and challenge RBC fees and policies quickly; a 2024 J.D. Power Canadian banking survey found fee transparency scored 62/100, pressuring banks to act.

ESG sentiment now drives deposits—62% of Canadian retail investors in a 2025 Statista poll said ESG influences banking choice—so RBC must align strategy to retain deposits and brand equity.

Collective customer power forces faster policy changes, public reporting, and fee adjustments to avoid reputational and deposit outflows.

- 2024 J.D. Power fee transparency 62/100

- 2025 Statista: 62% say ESG affects bank choice

- Higher social-media visibility shortens response time

2025 Customers Wield Power: Low Friction, Price-Driven, ESG & Fee-Savvy

Customers in 2025 have high bargaining power: low switching friction (Canada Open Banking readiness 72/100, 38% used account aggregation in 2024), strong price sensitivity (62% mortgage shoppers seek lowest APR in 2024), concentrated wealth clients (RBC AUM C$1.6T in 2024; top 1% hold >40% of private-client AUM), and ESG/fee transparency driving rapid reputational risk and fee pressure.

| Metric | Value |

|---|---|

| Open Banking readiness (2024) | 72/100 |

| Account aggregation (2024) | 38% |

| Mortgage shoppers lowest APR (2024) | 62% |

| RBC AUM (FY2024) | C$1.6T |

| Top 1% private-client AUM share | >40% |

| Fee transparency score (J.D. Power 2024) | 62/100 |

| ESG influence (2025 Statista) | 62% |

Full Version Awaits

RBC Porter's Five Forces Analysis

This preview shows the exact RBC Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you complete your order.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

RBC's Porter's Five Forces snapshot highlights competitive rivalry, regulatory barriers, and evolving buyer expectations shaping its banking moat—yet only scratches the surface.

The full report quantifies each force, maps supplier and substitute risks, and reveals strategic levers RBC can use to defend market share and margins.

Unlock the complete, consultant-grade analysis with visuals, force ratings, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of Specialized Labor and Fintech Talent

RBC relies on specialized suppliers—finance, data science, and cybersecurity professionals—whose scarcity gives them bargaining power; by Q4 2025 AI specialists commanded median Canadian salaries of CAD 140k–180k and cloud engineers CAD 130k–160k, pressuring firms to raise pay.

To keep digital transformation on track, RBC must match market offers with competitive total-compensation packages and upskilling budgets; turnover among tech roles rose ~12% in 2024, so retention spending directly affects project timelines and costs.

Dependency on Global Technology and Cloud Providers

RBC depends on a few dominant cloud and tech providers—Microsoft, Amazon Web Services, and Google Cloud—for core banking, risking supplier power; Gartner estimated enterprise cloud spending grew 22% in 2024, concentrating bargaining leverage with hyperscalers.

Switching costs are high: migrating petabytes, regulatory recertification, and multi-year contracts drive lock-in; a 2023 Accenture survey found 68% of banks cite cloud migration risk as a top operational concern.

Cost of Capital and Regulatory Liquidity Requirements

Suppliers of capital, notably central banks and institutional depositors, push RBC's margins via interest-rate swings and liquidity access; Bank of Canada terminal-rate guidance at 4.5% in late 2025 sets benchmark funding costs for RBC's wholesale borrowing.

Regulatory liquidity rules—LCR (liquidity coverage ratio) >100% and CET1 ratio target ~12.5% for Canadian banks—constrain RBC's funding mix and reduce yield-enhancing risk-taking.

Reliance on Specialized Financial Data and Infrastructure

Market data vendors Bloomberg, Refinitiv (Reuters), and S&P/Moody’s are core inputs for RBC’s capital markets and wealth units; Bloomberg’s terminal revenue reached about $11.7B in 2023, showing vendor scale and pricing leverage.

These suppliers sit in an oligopoly, giving RBC few substitutes for high-quality, real-time price feeds and credit data; switching costs and integration make alternatives costly.

Because regulators and trading systems require these feeds for compliance and execution, suppliers keep steady pricing power—vendor fees rose mid-single digits annually through 2024.

- Critical vendors: Bloomberg, Refinitiv, S&P, Moody’s

- Bloomberg 2023 revenue ~11.7B, signalling scale

- Oligopoly => limited substitutes, high switching costs

- Compliance/trading needs sustain steady vendor pricing

Outsourced Operational and Professional Services

RBC uses third-party vendors for back-office operations, legal counsel, and audits; global scale and regulatory expertise limit suitable suppliers to a handful of elite firms, raising switching costs.

Dependence on integrated services creates moderate supplier bargaining power: large vendors can command premium fees, though RBC’s scale and ~$1.6 trillion AUM (2025) give it negotiation leverage.

- Few elite global providers

- High switching costs due to integration

- Moderate supplier leverage vs RBC scale

RBC Faces Rising Supplier Power: Talent, Hyperscalers & Data Vendors Squeeze Costs

RBC faces moderate-to-high supplier power: scarce tech talent (AI median CAD140–180k in 2025) and hyperscaler dependence (AWS/Google/Microsoft; enterprise cloud spend +22% in 2024) raise costs; market-data vendors (Bloomberg rev ~$11.7B 2023) and elite service firms command premiums, though RBC’s ~CAD1.6T AUM (2025) gives negotiation leverage.

| Supplier | Key stat | Impact |

|---|---|---|

| AI/Cloud talent | CAD140–180k; cloud eng CAD130–160k (2025) | Higher wage/retention costs |

| Hyperscalers | Cloud spend +22% (2024) | Concentration risk |

| Market data | Bloomberg rev ~$11.7B (2023) | Pricing power |

| RBC scale | ~CAD1.6T AUM (2025) | Negotiation leverage |

What is included in the product

Provides a focused Porter's Five Forces assessment tailored to RBC, revealing competitive pressures, buyer and supplier influence, entry barriers, substitute risks, and strategic levers to safeguard market position.

A concise Porter's Five Forces one-sheet for RBC that highlights competitive pressures and strategic levers—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

Low Switching Costs in Retail Banking

Individual consumers in 2025 use digital tools and open banking APIs to move funds quickly; Canada’s Open Banking readiness index rose to 72/100 in 2024, and 38% of Canadians used account aggregation in 2024, so switching friction is low. This forces RBC to match market rates—its 2025 savings rates must remain within ~20–50 bps of peers—and keep service quality high to avoid churn.

High Price Sensitivity in Mortgage and Loan Products

Borrowers show high price sensitivity: a 2024 J.D. Power survey found 62% of mortgage shoppers prioritized lowest APR, so a 50 bps rate gap can swing applications away from RBC Royal Bank of Canada. In Canada’s 2025 market, average posted mortgage spreads narrowed to ~120 bps, limiting RBC’s premium pricing power. To compete, RBC often deploys promotional rates, cashback offers, or bundled advice services to retain volume and protect NIM.

Demands of High-Net-Worth Wealth Management Clients

Wealth management and institutional clients wield strong bargaining power at RBC because the top 1% of clients often hold >40% of private-client AUM; in 2024 RBC reported C$1.6 trillion in total AUM across wealth and asset management, concentrating negotiating leverage. These sophisticated investors demand tailored service, fee discounts (often 25–50 bps lower for large mandates), and access to private equity, real estate, and hedge funds. RBC must keep adding bespoke products and lower-cost fee tiers or risk migration to boutiques that won 12–18% market share gains in H1 2024.

Influence of Corporate and Institutional Borrowers

Large corporates access capital markets or multiple banks, letting them force down arranger fees; RBC lost share in global loan syndication to U.S. peers in 2024, dropping to 5.1% of global bookrunner volume (Refinitiv).

RBC often accepts thinner margins to keep strategic relationships—corporate clients generated ~28% of RBC Capital Markets revenue in FY2024, so retention trumps short-term fee gains.

- Clients can avoid banks via markets

- Competition squeezes arranger fees

- RBC accepts lower margins to retain top clients

Impact of Consumer Advocacy and Transparency

In 2025 increased transparency via social media and comparison sites lets customers spot and challenge RBC fees and policies quickly; a 2024 J.D. Power Canadian banking survey found fee transparency scored 62/100, pressuring banks to act.

ESG sentiment now drives deposits—62% of Canadian retail investors in a 2025 Statista poll said ESG influences banking choice—so RBC must align strategy to retain deposits and brand equity.

Collective customer power forces faster policy changes, public reporting, and fee adjustments to avoid reputational and deposit outflows.

- 2024 J.D. Power fee transparency 62/100

- 2025 Statista: 62% say ESG affects bank choice

- Higher social-media visibility shortens response time

2025 Customers Wield Power: Low Friction, Price-Driven, ESG & Fee-Savvy

Customers in 2025 have high bargaining power: low switching friction (Canada Open Banking readiness 72/100, 38% used account aggregation in 2024), strong price sensitivity (62% mortgage shoppers seek lowest APR in 2024), concentrated wealth clients (RBC AUM C$1.6T in 2024; top 1% hold >40% of private-client AUM), and ESG/fee transparency driving rapid reputational risk and fee pressure.

| Metric | Value |

|---|---|

| Open Banking readiness (2024) | 72/100 |

| Account aggregation (2024) | 38% |

| Mortgage shoppers lowest APR (2024) | 62% |

| RBC AUM (FY2024) | C$1.6T |

| Top 1% private-client AUM share | >40% |

| Fee transparency score (J.D. Power 2024) | 62/100 |

| ESG influence (2025 Statista) | 62% |

Full Version Awaits

RBC Porter's Five Forces Analysis

This preview shows the exact RBC Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you complete your order.