RBC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, macroeconomic trends, and tech disruption are reshaping RBC’s competitive landscape in our focused PESTLE Analysis—designed for investors and strategists who need timely, actionable intelligence; buy the full report now to access the complete, editable breakdown and make smarter decisions faster.

Political factors

Canadian Federal Election and Policy Shifts

The 2025 Canadian federal election cycle raises policy uncertainty over corporate taxation and housing initiatives, with polls in late 2025 showing fiscal platform discrepancies that could affect bank levies or capital gains treatment; Canada’s budgetary deficit was C$57.7B in FY2024, indicating room for tax adjustments. RBC must plan for scenarios where changes could alter after-tax ROE—RBC reported CET1 ratio 13.3% and 2024 EPS C$11.70. Strategic alignment with government infrastructure and housing programs (national housing strategy C$72B through 2028) is key to protect market share.

Geopolitical Tensions and Global Trade

Escalating trade frictions and geopolitical instability in Europe and Asia affect RBC Capital Markets and international wealth management, with cross-border revenues—RBC’s capital markets net income was CAD 4.2bn in FY2024—exposed to market volatility and client repositioning.

RBC monitors shifts in global supply chains and sanctions regimes to limit credit and counterparty risk across its CAD 1.5tn balance sheet, adjusting exposures in trade finance and syndicated loans.

U.S. protective trade policies require flexibility for RBC’s American operations, including City National Bank (assets CAD 92bn at YE2024), prompting scenario planning and hedging to protect profit margins.

Housing Market Interventions

Government mandates to cool or stimulate Canada’s housing market directly affect RBC, the country’s largest mortgage lender with C$449 billion in residential mortgages outstanding as of Q4 2025, since changes to foreign ownership rules, OSFI stress-test parameters and first-time buyer incentives shift origination volumes and credit mix.

In 2024–2025 policy moves—tightened stress tests that cut qualifying borrowing power by roughly 10–20% in some scenarios—correlated with a slowdown in mortgage growth, pressuring retail lending revenue and prompting RBC to recalibrate pricing and provisioning.

RBC routinely engages policymakers and participates in industry consultations to argue that abrupt regulatory tightening could raise systemic credit risk by increasing arrears among high-LTV borrowers and concentrating risk in alternative lenders, seeking phased implementation and targeted affordability measures.

Regulatory Relations and Lobbying

RBC engages actively with OSFI to influence prudential standards, reflecting its 2025 regulatory engagements after Canadian banks faced a 15% increase in stress-test stringency since 2020.

This engagement supports RBC’s strategic autonomy by shaping narratives on financial stability and domestic competition amid its CAD 1.4 trillion in assets under management (2024).

Political scrutiny over interest rate spreads and service fees—heightened by public debates after 2023 fee reviews—necessitates transparent PR and stakeholder communication.

- Active OSFI engagement amid tighter stress tests (+15% since 2020)

- CAD 1.4 trillion assets under management (2024)

- Heightened political scrutiny on spreads/fees since 2023

International Diplomatic Relations

As a global bank, RBC is sensitive to Canada’s diplomatic ties with the US and EU; 2024 cross-border banking transactions between Canada and the US exceeded CAD 1.6 trillion, so tensions can materially affect flows.

Diplomatic strains can alter data-sharing, capital controls or tax treaties—RBC monitors treaty changes after 2023 BEPS updates and FATCA/CRS compliance shifts.

RBC uses its international footprint—over 60% of revenue from non-Canadian operations in 2024—to hedge localized political risk while aligning operations to diplomatic protocols.

- US/EU ties affect CAD 1.6T+ cross-border flows (2024)

- Post-2023 BEPS and FATCA/CRS changes drive compliance adjustments

- 60%+ revenue from outside Canada (2024) aids geographic risk diversification

RBC Faces Margin Pressure Amid Political Shifts, Strong Capital and Heavy Mortgage Book

Political shifts (2024–25)—federal election uncertainty, tightened OSFI stress tests (+15% since 2020), housing policy (C$72B to 2028) and potential tax changes—threaten RBC’s margins; CET1 13.3%, EPS C$11.70 (2024), C$449B mortgages (Q4 2025), AUM C$1.4T (2024), capital markets NI C$4.2B (2024).

| Metric | Value |

|---|---|

| CET1 | 13.3% |

| EPS | C$11.70 |

| Mortgages | C$449B |

| AUM | C$1.4T |

What is included in the product

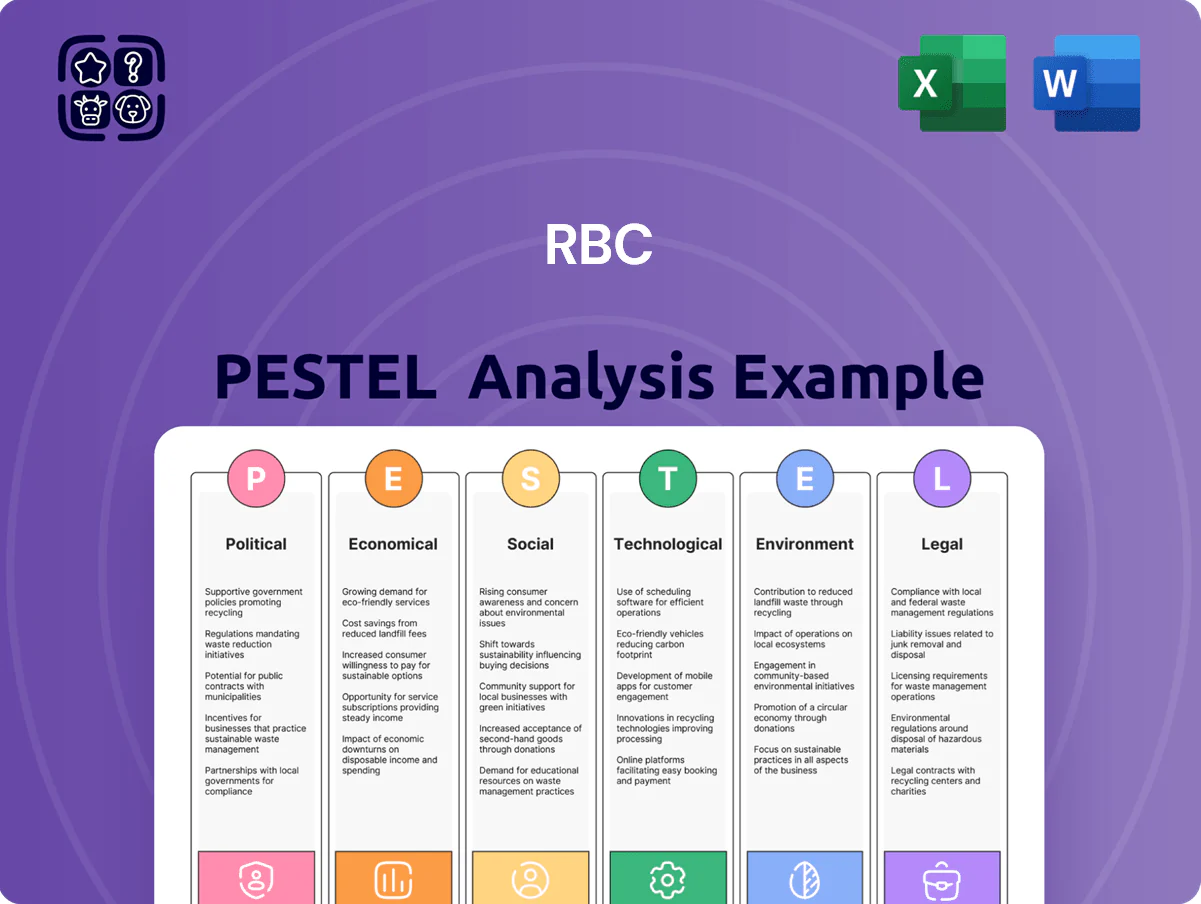

Explores how external macro-environmental factors uniquely affect RBC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven trends and forward-looking insights to inform risk mitigation and strategic opportunities.

Concise, visually segmented PESTLE summary of RBC that can be dropped into presentations or shared across teams for quick alignment, with editable notes to tailor insights by region or business line.

Economic factors

Interest Rate Environment and Net Interest Margin

The shift from peak Bank of Canada rates (overnight peaked at 5.0% in 2023) toward a more stabilized policy by late 2025 pressures RBC’s net interest margin, with Q4 2024 NIM at ~1.89% and management forecasting modest compression if policy rates ease further.

Lower rates could boost loan growth—Canadian household credit rose ~4.2% YoY in 2024—but compress spreads on deposits and short-term lending.

RBC deploys interest-rate swaps and balance-sheet hedges; as of FY2024 RBC reported CAD-denominated derivatives notional in the hundreds of billions, reducing sensitivity to BoC rate moves.

Household Debt and Credit Quality

High Canadian household debt—about 176% of disposable income in Q3 2025 per Bank of Canada—pushes RBC to raise provisions for credit losses as many mortgages renew at higher rates, weighing on net interest margins. The bank closely tracks retail delinquency rates, which stayed near 0.35% for residential mortgages in 2025 H1 but rose in credit cards, signaling early consumer stress in a post-inflation backdrop. Managing commercial real estate credit quality is critical as office vacancy hit ~15% in major metros, raising potential impairment risk for RBC’s CRE exposure.

Inflationary Pressures and Operating Costs

Persistent inflation, with Canada CPI rising 3.4% year-over-year in 2024, increases RBC’s wage and tech procurement costs, pressuring margins and headcount spending.

RBC is accelerating digital transformation—investing C$3.8bn in technology in 2024—to improve automation and reduce per‑customer service costs.

Keeping a competitive cost-to-income ratio (RBC at ~44% FY2024) is vital to fund dividends (yield ~3.5%) and reinvest in growth.

Energy Sector Performance and Transition

The health of Western Canada’s economy and a ~C$200bn energy sector deeply affect RBC’s commercial lending and capital markets fees; Alberta accounted for about 10% of Canada’s GDP in 2024, concentrating credit exposure.

As global investment shifts to renewables, RBC is reallocating capital—reducing oil & gas exposure while financing low-carbon projects, with 2024 sustainable financing commitments surpassing C$70bn.

Commodity price volatility (WTI swung 2023–24 between US$60–90/bbl) remains central to RBC’s macro risk models and stress tests, driving provisioning and hedging strategies.

- Western Canada energy = material credit concentration (~10% national GDP)

- RBC sustainable financing > C$70bn (2024)

- WTI volatility US$60–90/bbl (2023–24) fuels stress-test scenarios

Currency Fluctuations and International Revenue

RBC's sizable U.S. and international revenue exposes results to CAD volatility; a 10% CAD strengthening vs USD would cut translated U.S. dollar revenue by roughly 9% of the U.S. contribution (RBC reported ~35% of 2024 revenue from international/ U.S. businesses).

CAD/USD swings drive translation gains/losses in Wealth Management and Capital Markets—RBC recorded a CA$1.2bn FX translation loss in 2024 trading-related items.

The bank uses dollar-denominated hedges and natural offsets to stabilize CET1 and reported hedging reduced earnings volatility by ~0.6 percentage points of ROE in 2024.

- ~35% revenue from U.S./international (2024)

- CA$1.2bn FX translation loss (2024)

- Hedging reduced ROE volatility by ~0.6 pp (2024)

RBC under margin squeeze: high household debt, tech costs and energy/CRE risk

RBC faces margin pressure as BoC easing from 5.0% (2023 peak) risks NIM compression (Q4 2024 NIM ~1.89%); household debt ~176% disposable income (Q3 2025) raises credit loss provisions; FY2024 tech spend C$3.8bn and cost/income ~44% constrain reinvestment; energy exposure (~10% of Canada GDP) and WTI volatility (US$60–90/bbl 2023–24) drive CRE and commodity risk.

| Metric | Value |

|---|---|

| NIM | ~1.89% Q4 2024 |

| Household debt | 176% disp. income Q3 2025 |

| Tech spend | C$3.8bn FY2024 |

| Cost/Income | ~44% FY2024 |

| Sustainable finance | >C$70bn 2024 |

Preview Before You Purchase

RBC PESTLE Analysis

The preview shown here is the exact RBC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The content, layout, and headings visible in this sample match the downloadable file you’ll get immediately after checkout so you can rely on it for analysis and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, macroeconomic trends, and tech disruption are reshaping RBC’s competitive landscape in our focused PESTLE Analysis—designed for investors and strategists who need timely, actionable intelligence; buy the full report now to access the complete, editable breakdown and make smarter decisions faster.

Political factors

Canadian Federal Election and Policy Shifts

The 2025 Canadian federal election cycle raises policy uncertainty over corporate taxation and housing initiatives, with polls in late 2025 showing fiscal platform discrepancies that could affect bank levies or capital gains treatment; Canada’s budgetary deficit was C$57.7B in FY2024, indicating room for tax adjustments. RBC must plan for scenarios where changes could alter after-tax ROE—RBC reported CET1 ratio 13.3% and 2024 EPS C$11.70. Strategic alignment with government infrastructure and housing programs (national housing strategy C$72B through 2028) is key to protect market share.

Geopolitical Tensions and Global Trade

Escalating trade frictions and geopolitical instability in Europe and Asia affect RBC Capital Markets and international wealth management, with cross-border revenues—RBC’s capital markets net income was CAD 4.2bn in FY2024—exposed to market volatility and client repositioning.

RBC monitors shifts in global supply chains and sanctions regimes to limit credit and counterparty risk across its CAD 1.5tn balance sheet, adjusting exposures in trade finance and syndicated loans.

U.S. protective trade policies require flexibility for RBC’s American operations, including City National Bank (assets CAD 92bn at YE2024), prompting scenario planning and hedging to protect profit margins.

Housing Market Interventions

Government mandates to cool or stimulate Canada’s housing market directly affect RBC, the country’s largest mortgage lender with C$449 billion in residential mortgages outstanding as of Q4 2025, since changes to foreign ownership rules, OSFI stress-test parameters and first-time buyer incentives shift origination volumes and credit mix.

In 2024–2025 policy moves—tightened stress tests that cut qualifying borrowing power by roughly 10–20% in some scenarios—correlated with a slowdown in mortgage growth, pressuring retail lending revenue and prompting RBC to recalibrate pricing and provisioning.

RBC routinely engages policymakers and participates in industry consultations to argue that abrupt regulatory tightening could raise systemic credit risk by increasing arrears among high-LTV borrowers and concentrating risk in alternative lenders, seeking phased implementation and targeted affordability measures.

Regulatory Relations and Lobbying

RBC engages actively with OSFI to influence prudential standards, reflecting its 2025 regulatory engagements after Canadian banks faced a 15% increase in stress-test stringency since 2020.

This engagement supports RBC’s strategic autonomy by shaping narratives on financial stability and domestic competition amid its CAD 1.4 trillion in assets under management (2024).

Political scrutiny over interest rate spreads and service fees—heightened by public debates after 2023 fee reviews—necessitates transparent PR and stakeholder communication.

- Active OSFI engagement amid tighter stress tests (+15% since 2020)

- CAD 1.4 trillion assets under management (2024)

- Heightened political scrutiny on spreads/fees since 2023

International Diplomatic Relations

As a global bank, RBC is sensitive to Canada’s diplomatic ties with the US and EU; 2024 cross-border banking transactions between Canada and the US exceeded CAD 1.6 trillion, so tensions can materially affect flows.

Diplomatic strains can alter data-sharing, capital controls or tax treaties—RBC monitors treaty changes after 2023 BEPS updates and FATCA/CRS compliance shifts.

RBC uses its international footprint—over 60% of revenue from non-Canadian operations in 2024—to hedge localized political risk while aligning operations to diplomatic protocols.

- US/EU ties affect CAD 1.6T+ cross-border flows (2024)

- Post-2023 BEPS and FATCA/CRS changes drive compliance adjustments

- 60%+ revenue from outside Canada (2024) aids geographic risk diversification

RBC Faces Margin Pressure Amid Political Shifts, Strong Capital and Heavy Mortgage Book

Political shifts (2024–25)—federal election uncertainty, tightened OSFI stress tests (+15% since 2020), housing policy (C$72B to 2028) and potential tax changes—threaten RBC’s margins; CET1 13.3%, EPS C$11.70 (2024), C$449B mortgages (Q4 2025), AUM C$1.4T (2024), capital markets NI C$4.2B (2024).

| Metric | Value |

|---|---|

| CET1 | 13.3% |

| EPS | C$11.70 |

| Mortgages | C$449B |

| AUM | C$1.4T |

What is included in the product

Explores how external macro-environmental factors uniquely affect RBC across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven trends and forward-looking insights to inform risk mitigation and strategic opportunities.

Concise, visually segmented PESTLE summary of RBC that can be dropped into presentations or shared across teams for quick alignment, with editable notes to tailor insights by region or business line.

Economic factors

Interest Rate Environment and Net Interest Margin

The shift from peak Bank of Canada rates (overnight peaked at 5.0% in 2023) toward a more stabilized policy by late 2025 pressures RBC’s net interest margin, with Q4 2024 NIM at ~1.89% and management forecasting modest compression if policy rates ease further.

Lower rates could boost loan growth—Canadian household credit rose ~4.2% YoY in 2024—but compress spreads on deposits and short-term lending.

RBC deploys interest-rate swaps and balance-sheet hedges; as of FY2024 RBC reported CAD-denominated derivatives notional in the hundreds of billions, reducing sensitivity to BoC rate moves.

Household Debt and Credit Quality

High Canadian household debt—about 176% of disposable income in Q3 2025 per Bank of Canada—pushes RBC to raise provisions for credit losses as many mortgages renew at higher rates, weighing on net interest margins. The bank closely tracks retail delinquency rates, which stayed near 0.35% for residential mortgages in 2025 H1 but rose in credit cards, signaling early consumer stress in a post-inflation backdrop. Managing commercial real estate credit quality is critical as office vacancy hit ~15% in major metros, raising potential impairment risk for RBC’s CRE exposure.

Inflationary Pressures and Operating Costs

Persistent inflation, with Canada CPI rising 3.4% year-over-year in 2024, increases RBC’s wage and tech procurement costs, pressuring margins and headcount spending.

RBC is accelerating digital transformation—investing C$3.8bn in technology in 2024—to improve automation and reduce per‑customer service costs.

Keeping a competitive cost-to-income ratio (RBC at ~44% FY2024) is vital to fund dividends (yield ~3.5%) and reinvest in growth.

Energy Sector Performance and Transition

The health of Western Canada’s economy and a ~C$200bn energy sector deeply affect RBC’s commercial lending and capital markets fees; Alberta accounted for about 10% of Canada’s GDP in 2024, concentrating credit exposure.

As global investment shifts to renewables, RBC is reallocating capital—reducing oil & gas exposure while financing low-carbon projects, with 2024 sustainable financing commitments surpassing C$70bn.

Commodity price volatility (WTI swung 2023–24 between US$60–90/bbl) remains central to RBC’s macro risk models and stress tests, driving provisioning and hedging strategies.

- Western Canada energy = material credit concentration (~10% national GDP)

- RBC sustainable financing > C$70bn (2024)

- WTI volatility US$60–90/bbl (2023–24) fuels stress-test scenarios

Currency Fluctuations and International Revenue

RBC's sizable U.S. and international revenue exposes results to CAD volatility; a 10% CAD strengthening vs USD would cut translated U.S. dollar revenue by roughly 9% of the U.S. contribution (RBC reported ~35% of 2024 revenue from international/ U.S. businesses).

CAD/USD swings drive translation gains/losses in Wealth Management and Capital Markets—RBC recorded a CA$1.2bn FX translation loss in 2024 trading-related items.

The bank uses dollar-denominated hedges and natural offsets to stabilize CET1 and reported hedging reduced earnings volatility by ~0.6 percentage points of ROE in 2024.

- ~35% revenue from U.S./international (2024)

- CA$1.2bn FX translation loss (2024)

- Hedging reduced ROE volatility by ~0.6 pp (2024)

RBC under margin squeeze: high household debt, tech costs and energy/CRE risk

RBC faces margin pressure as BoC easing from 5.0% (2023 peak) risks NIM compression (Q4 2024 NIM ~1.89%); household debt ~176% disposable income (Q3 2025) raises credit loss provisions; FY2024 tech spend C$3.8bn and cost/income ~44% constrain reinvestment; energy exposure (~10% of Canada GDP) and WTI volatility (US$60–90/bbl 2023–24) drive CRE and commodity risk.

| Metric | Value |

|---|---|

| NIM | ~1.89% Q4 2024 |

| Household debt | 176% disp. income Q3 2025 |

| Tech spend | C$3.8bn FY2024 |

| Cost/Income | ~44% FY2024 |

| Sustainable finance | >C$70bn 2024 |

Preview Before You Purchase

RBC PESTLE Analysis

The preview shown here is the exact RBC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. The content, layout, and headings visible in this sample match the downloadable file you’ll get immediately after checkout so you can rely on it for analysis and presentation.