RCBC Business Model Canvas

RCBC's Business Model Canvas: Your concise roadmap to banking growth and investor-ready insights

Unlock RCBC’s strategic playbook with our concise Business Model Canvas—discover how customer segments, key partnerships, and revenue streams align to drive growth and resilience in banking; download the full Word/Excel canvas for a section-by-section roadmap, practical benchmarking tools, and investor-ready insights to apply immediately.

Partnerships

Strategic Bancassurance Alliance

RCBC’s long-standing bancassurance joint venture with Sun Life Grepa Financial lets the bank sell life and investment-linked products directly to depositors, driving fee income — bancassurance contributed about PHP 3.2 billion in premiums distributed via RCBC in 2024, boosting non-interest income by ~6% year-over-year. By using Sun Life’s global underwriting and product design, RCBC strengthens retention and cross-sell, improving customer lifetime value.

Yuchengco Group of Companies Ecosystem

As part of the Yuchengco Group, RCBC leverages affiliates in construction, education and non-life insurance to access a built-in corporate client base and shared services, enabling cross-selling of loans, cash management and insurance products; in 2024 the group’s conglomerate-related exposures accounted for roughly 12% of RCBC’s corporate loan book (about PHP60B).

Fintech and Digital Payment Partners

RCBC partners with global and local fintechs to boost its digital payment stack and open API capabilities, enabling integrations with e-wallets, payment gateways, and remittance providers; in 2024 RCBC reported 38% YoY growth in digital transactions on RCBC Pulz and DiskarTech, processing over PHP 420 billion in digital payments. These tie-ups cut settlement times and broaden rails for cross-border remittances, keeping RCBC competitive in the Philippines’ fast-growing digital-payments market.

Government and Regulatory Bodies

RCBC partners with the Bangko Sentral ng Pilipinas and agencies like the Department of Social Welfare and Development to advance financial inclusion, supporting BSP targets that lifted the Philippines' adult account ownership to 70% in 2021 and aimed 80% by 2025.

These ties keep RCBC compliant with evolving digital-banking rules and AML laws and let RCBC handle government disbursements—reaching remote, previously unbanked areas via cashless payouts and pay-out points.

- Supports BSP inclusion targets (70% in 2021; 80% target by 2025)

- Ensures compliance with digital-banking and AML rules

- Enables government disbursements to remote/unbanked populations

Merchant and Retail Networks

RCBC partners with 12,000+ retail merchants and service providers to support its credit card and loyalty programs, enabling point-of-sale financing and exclusive discounts that drove a 15% YoY rise in card transaction volume in 2024.

These alliances boost merchant-acquired fees and card usage, increasing net interest and fee income from consumer finance products by an estimated PHP 1.2 billion in 2024.

- 12,000+ merchant partners

- 15% YoY card transaction growth (2024)

- PHP 1.2B incremental consumer finance income (2024)

RCBC’s partnerships fuel fee growth, digital scale and cross-sell momentum

RCBC’s key partnerships—Sun Life bancassurance (PHP 3.2B premiums, +6% NII YoY 2024), Yuchengco affiliates (12% of corporate loans ≈ PHP 60B 2024), fintechs (PHP 420B digital payments, +38% digital txns YoY 2024), BSP/government (supports 80% inclusion target for 2025), and 12,000+ merchants (15% card txn growth; PHP 1.2B consumer income)—drive fee income, cross-sell, digital scale, and compliance.

| Partner | Key metric (2024) | Impact |

|---|---|---|

| Sun Life | PHP 3.2B premiums | +6% NII YoY |

| Yuchengco Group | PHP 60B (12% corp loans) | Cross-sell corporate clients |

| Fintechs | PHP 420B payments (+38% txns) | Faster settlements, remittances |

| BSP/Govt | Supports 80% inclusion target | Compliance, govt disbursements |

| Merchants | 12,000+ partners; 15% card growth; PHP 1.2B | Higher card fees, consumer income |

What is included in the product

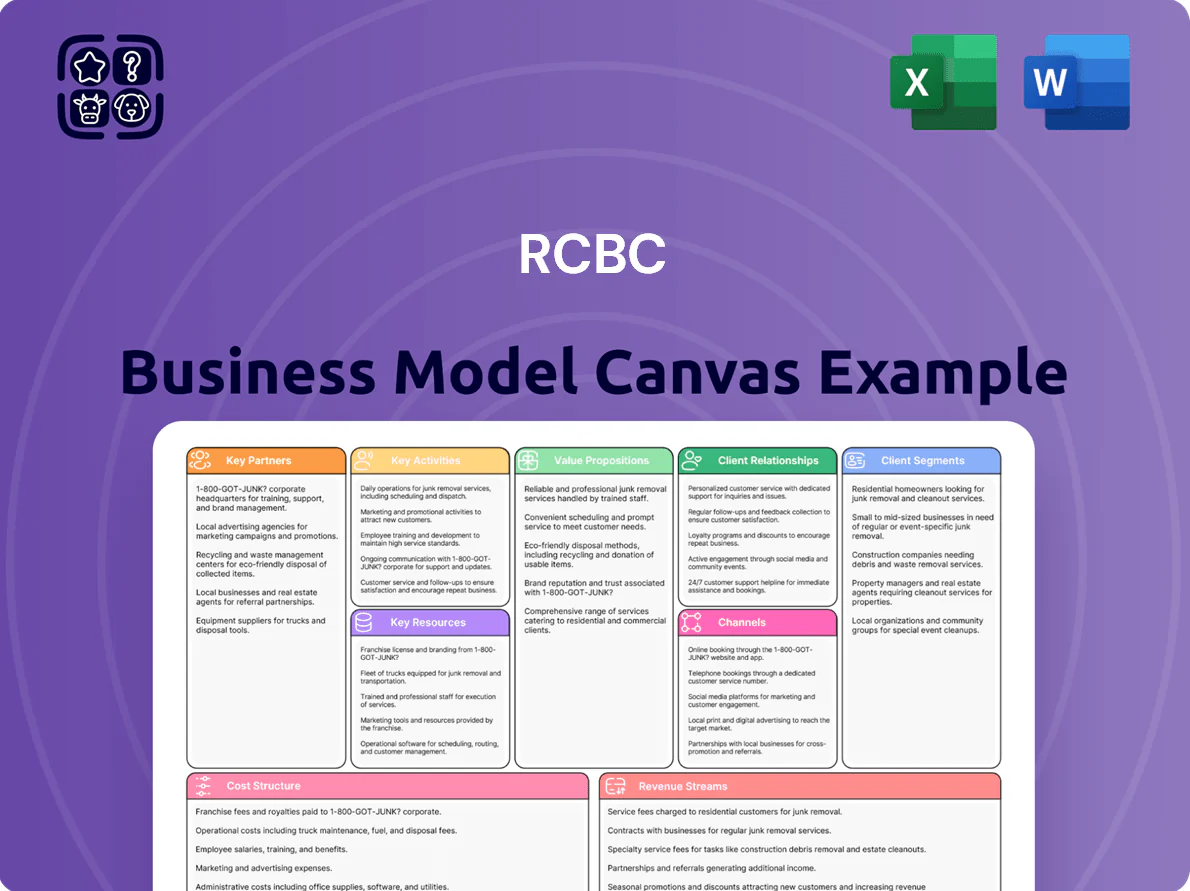

A concise, pre-built Business Model Canvas for RCBC detailing nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting real-world banking operations and strategic plans, with competitive analysis, SWOT linkage, and polished presentation for investor discussions and internal decision-making.

High-level view of RCBC’s business model with editable cells—quickly pinpoint revenue drivers, risk areas, and customer segments to streamline strategic decisions and presentations.

Activities

Digital Banking Transformation

RCBC continuously upgrades RCBC Pulz and DiskarTech, scaling back-end systems to handle millions of monthly transactions—Pulz reported over 2.3M active users in 2024—and invests in advanced cybersecurity (zero-trust and 24/7 SOC) to protect ₱ hundreds of billions in customer assets.

Credit Evaluation and Lending

RCBC rigorously assesses creditworthiness across retail, SME, and corporate segments, combining financial models with data analytics; as of 2024 loans grew 6.2% YoY to PHP 634.5B, so risk scoring steers portfolio expansion. Efficient origination, underwriting, and monitoring keep NPLs at 1.7% in 2024 and sustain interest income, which made up ~62% of net revenue in FY2024.

Wealth and Asset Management

RCBC’s Trust and Investments Group manages portfolios for HNW and institutional clients, running Unit Investment Trust Funds and tailored vehicles with Php 48.2 billion AUM as of Dec 2025; activities include daily market analysis, risk profiling, and personalized financial plans to hit client targets and regulatory requirements and aiming for net returns above benchmark by 150–250 bps.

Marketing and Customer Acquisition

RCBC runs strategic marketing to grow customers and push new products, mixing digital ads, social-media leads, and community outreach for financial inclusion; in 2024 digital acquisitions rose ~18% year-on-year while credit-card origination grew 12%.

Targeted promos for cards and loans focus on segmented offers and partnerships, keeping customer-acquisition cost (CAC) controlled so RCBC can defend growth in the Philippine banking market where net interest income rose 7.5% in 2024.

- Digital acquisition +18% (2024)

- Credit-card originations +12% (2024)

- CAC management to support NII +7.5% (2024)

Risk Management and Compliance

The bank allocates substantial resources to monitor market, credit, and operational risks—conducting quarterly stress tests and annual internal audits to uphold solvency; as of 2024 RCBC maintained a CET1 ratio near 12% and nonperforming loan (NPL) ratio around 1.8%, cushions aligned with Basel III buffers.

Robust compliance prevents fines and reputational damage; RCBC follows AML/CFT rules and reported zero material regulatory sanctions in 2023 while investing in transaction-monitoring tech and staff training.

- Quarterly stress tests

- Annual internal audits

- CET1 ≈ 12% (2024)

- NPL ≈ 1.8% (2024)

- No material sanctions (2023)

RCBC: Digital growth (2.3M Pulz) fuels PHP634.5B loans, strong CET1 ~12% & low NPL

RCBC runs digital platforms (Pulz 2.3M users in 2024), credit origination (loans PHP 634.5B, +6.2% YoY 2024), trust AUM PHP 48.2B (Dec 2025), and strong risk/compliance (CET1 ~12%, NPL ~1.8% 2024) while marketing boosts digital acquisition +18% and card originations +12% (2024).

| Metric | Value |

|---|---|

| Pulz users (2024) | 2.3M |

| Loans (2024) | PHP 634.5B |

| Trust AUM (Dec 2025) | PHP 48.2B |

| CET1 / NPL (2024) | ~12% / ~1.8% |

| Digital acquisition (2024) | +18% |

Full Version Awaits

Business Model Canvas

The RCBC Business Model Canvas preview you see is the exact deliverable—not a mockup or sample—and reflects the same structure, content, and formatting you will receive after purchase.

When you complete your order, you’ll get the full document in editable formats (Word and Excel), instantly downloadable and ready for presentation, editing, or sharing.

No placeholders or omissions: this preview is a direct snapshot of the final file, so what you see is precisely what you’ll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

RCBC's Business Model Canvas: Your concise roadmap to banking growth and investor-ready insights

Unlock RCBC’s strategic playbook with our concise Business Model Canvas—discover how customer segments, key partnerships, and revenue streams align to drive growth and resilience in banking; download the full Word/Excel canvas for a section-by-section roadmap, practical benchmarking tools, and investor-ready insights to apply immediately.

Partnerships

Strategic Bancassurance Alliance

RCBC’s long-standing bancassurance joint venture with Sun Life Grepa Financial lets the bank sell life and investment-linked products directly to depositors, driving fee income — bancassurance contributed about PHP 3.2 billion in premiums distributed via RCBC in 2024, boosting non-interest income by ~6% year-over-year. By using Sun Life’s global underwriting and product design, RCBC strengthens retention and cross-sell, improving customer lifetime value.

Yuchengco Group of Companies Ecosystem

As part of the Yuchengco Group, RCBC leverages affiliates in construction, education and non-life insurance to access a built-in corporate client base and shared services, enabling cross-selling of loans, cash management and insurance products; in 2024 the group’s conglomerate-related exposures accounted for roughly 12% of RCBC’s corporate loan book (about PHP60B).

Fintech and Digital Payment Partners

RCBC partners with global and local fintechs to boost its digital payment stack and open API capabilities, enabling integrations with e-wallets, payment gateways, and remittance providers; in 2024 RCBC reported 38% YoY growth in digital transactions on RCBC Pulz and DiskarTech, processing over PHP 420 billion in digital payments. These tie-ups cut settlement times and broaden rails for cross-border remittances, keeping RCBC competitive in the Philippines’ fast-growing digital-payments market.

Government and Regulatory Bodies

RCBC partners with the Bangko Sentral ng Pilipinas and agencies like the Department of Social Welfare and Development to advance financial inclusion, supporting BSP targets that lifted the Philippines' adult account ownership to 70% in 2021 and aimed 80% by 2025.

These ties keep RCBC compliant with evolving digital-banking rules and AML laws and let RCBC handle government disbursements—reaching remote, previously unbanked areas via cashless payouts and pay-out points.

- Supports BSP inclusion targets (70% in 2021; 80% target by 2025)

- Ensures compliance with digital-banking and AML rules

- Enables government disbursements to remote/unbanked populations

Merchant and Retail Networks

RCBC partners with 12,000+ retail merchants and service providers to support its credit card and loyalty programs, enabling point-of-sale financing and exclusive discounts that drove a 15% YoY rise in card transaction volume in 2024.

These alliances boost merchant-acquired fees and card usage, increasing net interest and fee income from consumer finance products by an estimated PHP 1.2 billion in 2024.

- 12,000+ merchant partners

- 15% YoY card transaction growth (2024)

- PHP 1.2B incremental consumer finance income (2024)

RCBC’s partnerships fuel fee growth, digital scale and cross-sell momentum

RCBC’s key partnerships—Sun Life bancassurance (PHP 3.2B premiums, +6% NII YoY 2024), Yuchengco affiliates (12% of corporate loans ≈ PHP 60B 2024), fintechs (PHP 420B digital payments, +38% digital txns YoY 2024), BSP/government (supports 80% inclusion target for 2025), and 12,000+ merchants (15% card txn growth; PHP 1.2B consumer income)—drive fee income, cross-sell, digital scale, and compliance.

| Partner | Key metric (2024) | Impact |

|---|---|---|

| Sun Life | PHP 3.2B premiums | +6% NII YoY |

| Yuchengco Group | PHP 60B (12% corp loans) | Cross-sell corporate clients |

| Fintechs | PHP 420B payments (+38% txns) | Faster settlements, remittances |

| BSP/Govt | Supports 80% inclusion target | Compliance, govt disbursements |

| Merchants | 12,000+ partners; 15% card growth; PHP 1.2B | Higher card fees, consumer income |

What is included in the product

A concise, pre-built Business Model Canvas for RCBC detailing nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting real-world banking operations and strategic plans, with competitive analysis, SWOT linkage, and polished presentation for investor discussions and internal decision-making.

High-level view of RCBC’s business model with editable cells—quickly pinpoint revenue drivers, risk areas, and customer segments to streamline strategic decisions and presentations.

Activities

Digital Banking Transformation

RCBC continuously upgrades RCBC Pulz and DiskarTech, scaling back-end systems to handle millions of monthly transactions—Pulz reported over 2.3M active users in 2024—and invests in advanced cybersecurity (zero-trust and 24/7 SOC) to protect ₱ hundreds of billions in customer assets.

Credit Evaluation and Lending

RCBC rigorously assesses creditworthiness across retail, SME, and corporate segments, combining financial models with data analytics; as of 2024 loans grew 6.2% YoY to PHP 634.5B, so risk scoring steers portfolio expansion. Efficient origination, underwriting, and monitoring keep NPLs at 1.7% in 2024 and sustain interest income, which made up ~62% of net revenue in FY2024.

Wealth and Asset Management

RCBC’s Trust and Investments Group manages portfolios for HNW and institutional clients, running Unit Investment Trust Funds and tailored vehicles with Php 48.2 billion AUM as of Dec 2025; activities include daily market analysis, risk profiling, and personalized financial plans to hit client targets and regulatory requirements and aiming for net returns above benchmark by 150–250 bps.

Marketing and Customer Acquisition

RCBC runs strategic marketing to grow customers and push new products, mixing digital ads, social-media leads, and community outreach for financial inclusion; in 2024 digital acquisitions rose ~18% year-on-year while credit-card origination grew 12%.

Targeted promos for cards and loans focus on segmented offers and partnerships, keeping customer-acquisition cost (CAC) controlled so RCBC can defend growth in the Philippine banking market where net interest income rose 7.5% in 2024.

- Digital acquisition +18% (2024)

- Credit-card originations +12% (2024)

- CAC management to support NII +7.5% (2024)

Risk Management and Compliance

The bank allocates substantial resources to monitor market, credit, and operational risks—conducting quarterly stress tests and annual internal audits to uphold solvency; as of 2024 RCBC maintained a CET1 ratio near 12% and nonperforming loan (NPL) ratio around 1.8%, cushions aligned with Basel III buffers.

Robust compliance prevents fines and reputational damage; RCBC follows AML/CFT rules and reported zero material regulatory sanctions in 2023 while investing in transaction-monitoring tech and staff training.

- Quarterly stress tests

- Annual internal audits

- CET1 ≈ 12% (2024)

- NPL ≈ 1.8% (2024)

- No material sanctions (2023)

RCBC: Digital growth (2.3M Pulz) fuels PHP634.5B loans, strong CET1 ~12% & low NPL

RCBC runs digital platforms (Pulz 2.3M users in 2024), credit origination (loans PHP 634.5B, +6.2% YoY 2024), trust AUM PHP 48.2B (Dec 2025), and strong risk/compliance (CET1 ~12%, NPL ~1.8% 2024) while marketing boosts digital acquisition +18% and card originations +12% (2024).

| Metric | Value |

|---|---|

| Pulz users (2024) | 2.3M |

| Loans (2024) | PHP 634.5B |

| Trust AUM (Dec 2025) | PHP 48.2B |

| CET1 / NPL (2024) | ~12% / ~1.8% |

| Digital acquisition (2024) | +18% |

Full Version Awaits

Business Model Canvas

The RCBC Business Model Canvas preview you see is the exact deliverable—not a mockup or sample—and reflects the same structure, content, and formatting you will receive after purchase.

When you complete your order, you’ll get the full document in editable formats (Word and Excel), instantly downloadable and ready for presentation, editing, or sharing.

No placeholders or omissions: this preview is a direct snapshot of the final file, so what you see is precisely what you’ll own.