RCL Foods Porter's Five Forces Analysis

Don't Miss the Bigger Picture

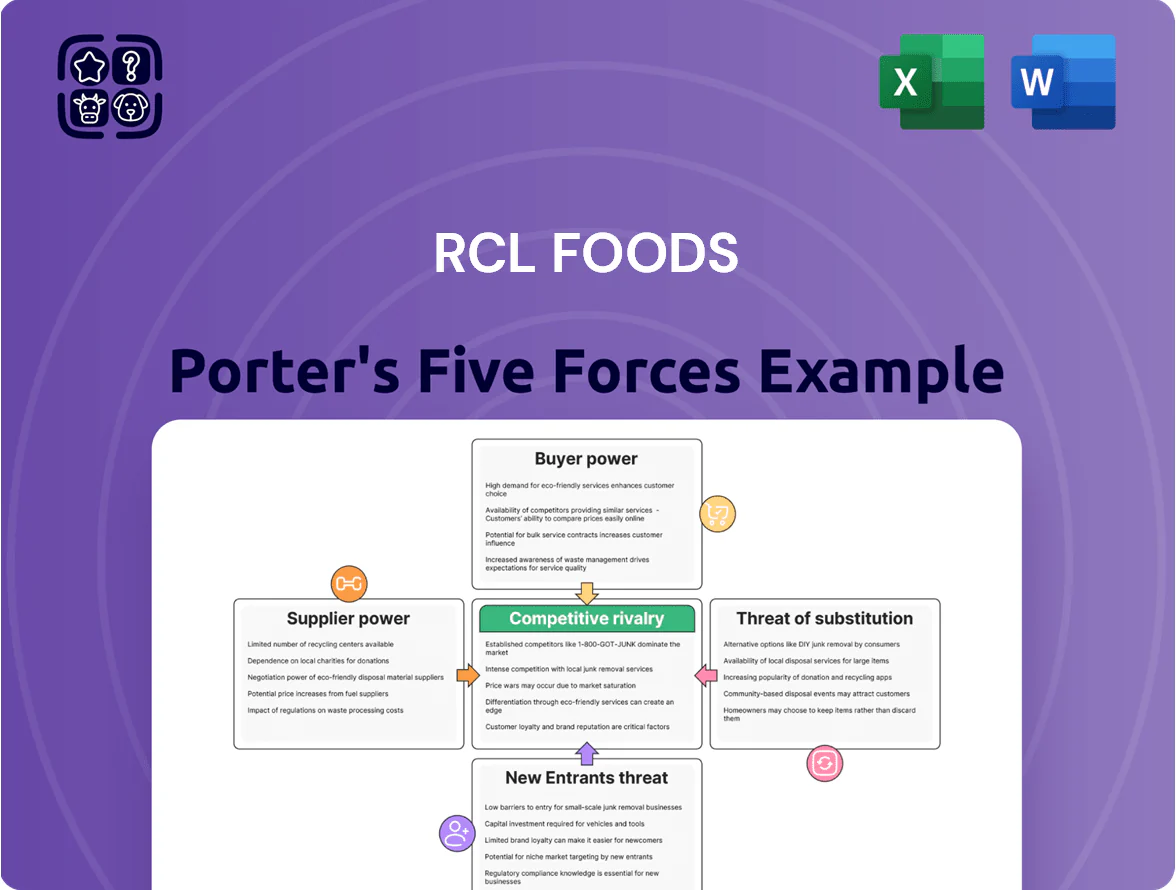

RCL Foods faces intense buyer power and moderate supplier influence amid price-sensitive South African markets, while new entrants are deterred by scale and distribution advantages but substitutes and competitive rivalry remain significant risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RCL Foods’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

RCL Foods reduces supplier power via deep vertical integration, owning key sugar and poultry farms and processing plants; by FY2024 the group reported circa 60% of poultry volumes sourced internally and integrated sugar capacity covering roughly 70% of its cane requirements.

Commodity Price Volatility

RCL Foods remains exposed to global commodity swings for maize and soya—used in animal feed—so international exchange pricing drives local supplier rates, constraining RCL’s negotiating power; maize futures rose ~28% in 2024 and soya oilseed gained ~22% (2024 Y/Y), making feed costs a large, externally dictated input expense and creating a balanced supplier power where market forces set primary input costs.

Energy and Utility Dependence

State-owned utilities in South Africa, notably Eskom (electricity) and Rand Water, exert strong leverage over RCL Foods because food processing is energy and water intensive; Eskom recorded 8 000+ MW of load-shedding capacity in 2024, forcing firms to invest in backups.

Frequent outages pushed South African manufacturers to spend on self-generation; RCL’s peers report capex rises of 5–12% for gensets and solar between 2022–2024, so RCL faces higher operating costs and capital needs.

Few large-scale private alternatives exist for grid-scale power and bulk water, so these utilities retain high bargaining power, increasing supply risk and margin pressure for RCL Foods.

Specialized Packaging Requirements

- Fewer than 30 certified regional suppliers

- Top 5 cover ~60% of demand

- Extended Producer Responsibility effective 2024

- Packaging disruptions can cut margins 3–6%

Concentrated Logistics Networks

RCL Foods depends heavily on third-party logistics and fuel suppliers for cold-chain distribution, exposing it to price hikes; South African diesel excise and transport tariffs rose ~8-12% in 2024, pressuring margins.

Logistics giants can pass rising costs—fuel levies plus a ~15-25% premium for refrigerated transport—to manufacturers, giving them bargaining leverage when specialized poultry and dairy handling is required.

- Third-party logistics dependency raises cost exposure

- 2024 diesel/transport increases ~8-12% hit margins

- Refrigerated transport premiums ~15-25%

- Concentrated providers hold pricing leverage

RCL Foods: strong vertical cover but maize/soya shocks, utility and supplier margin risks

RCL Foods limits supplier power through vertical integration (≈60% poultry internal, ≈70% sugar cane coverage FY2024) but remains exposed to maize/soya price swings (2024: maize +28%, soya +22%), utility leverage (Eskom load‑shedding 2024) and concentrated packaging/logistics suppliers causing 3–6% margin risk.

| Factor | Key number |

|---|---|

| Poultry vertical supply | ≈60% FY2024 |

| Sugar cane coverage | ≈70% FY2024 |

| Maize price change 2024 | +28% |

| Soya price change 2024 | +22% |

| Packaging supplier concentration | Top 5 ≈60% |

| Packaging margin hit risk | 3–6% |

| Diesel/transport rise 2024 | ≈8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for RCL Foods, uncovering competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers to assess pricing pressure and profitability within its South African food and agribusiness landscape.

A concise Porter's Five Forces one-sheet for RCL Foods—quickly highlights supplier, buyer, rivalry, substitution, and entry pressures to streamline strategic decisions.

Customers Bargaining Power

Retailer Consolidation

The South African grocery market is concentrated: Shoprite, Pick n Pay and Spar together held about 60% of formal grocery share in 2024, giving them huge buying power over suppliers like RCL Foods. These retailers buy massive volumes and routinely extract double-digit trade discounts and extended payment terms; for example, reported supplier rebates averaged 6–12% industry-wide in 2023. Control of scarce shelf space lets them demand promotional funding and private-label slots, weakening RCL Foods’ pricing power.

Growth of Private Label Brands

Major South African retailers like Shoprite and Pick n Pay raised private-label share to about 20–30% of food sales by 2024, directly competing with RCL Foods’ branded lines and boosting retailer bargaining power. Retailers can favor higher-margin house brands, pressuring RCL on pricing and shelf space; in 2024 RCL reported FY2024 revenue of ZAR 20.7bn, so margin erosion would materially hit results. RCL must keep investing in product innovation and brand equity to defend placement and premium pricing.

Low Switching Costs

For end consumers switching from RCL Foods to rivals costs near zero, especially in staples like sugar, flour and poultry where brands are shelf-substitutable; NielsenIQ (2024) shows 62% of South African grocery shoppers prioritize price. This drives RCL to keep margins tight—gross margin for Food reported 12.8% in FY2024—and sustain quality and promotions to retain a price-sensitive, fickle customer base.

Consumer Economic Pressure

High 2025 South African inflation of 5.9% (Q4 2025 y/y) and unemployment at ~32.9% (Q3 2025) raise price sensitivity, so consumers shift to bulk formats and cheaper brands, constraining RCL Foods’ ability to pass on input-cost inflation.

Price becomes the dominant purchase driver, increasing buyer power and forcing RCL to protect volume via promotions or lower-margin SKUs, squeezing gross margins.

- Inflation 5.9% (2025 Q4)

- Unemployment ~32.9% (2025 Q3)

- Higher trade-down to bulk/cheaper SKUs

- Limits on passing input costs → margin pressure

Information Symmetry

Information symmetry is high: by 2025 over 80% of South African consumers use smartphones for price checks, and platforms show real-time prices and nutrition, eroding RCL Foods’ ability to charge premiums.

Professional buyers use global benchmarks—bulk poultry and maize prices fell ~12% in 2024—so RCL must run tight margins and improve supply-chain efficiency.

Well-informed demand forces faster product updates and transparent labeling to retain market share.

- ~80% smartphone price-check penetration (2025)

- Global bulk input prices down ~12% in 2024

- Need for lean supply chain and transparent labeling

Retail concentration, private labels squeeze RCL Foods—margins under price pressure

Retail concentration (Shoprite, Pick n Pay, Spar ~60% share) and rising private-label (20–30% of food sales) give buyers strong leverage, forcing RCL Foods into discounts, promotional funding and margin pressure; FY2024 food gross margin 12.8% vs revenue ZAR 20.7bn. High price sensitivity (62% prioritize price), inflation 5.9% (Q4 2025) and smartphone price checks (~80%) further limit pass-through of input costs.

| Metric | Value |

|---|---|

| Retail share | ~60% |

| Private-label | 20–30% |

| RCL FY2024 revenue | ZAR 20.7bn |

| Food gross margin FY2024 | 12.8% |

| Price-sensitive shoppers | 62% |

| Inflation Q4 2025 | 5.9% |

| Smartphone price checks 2025 | ~80% |

What You See Is What You Get

RCL Foods Porter's Five Forces Analysis

This preview shows the exact RCL Foods Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s fully formatted and ready to use.

You're looking at the actual deliverable: a complete, professionally written assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, available for instant download once you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

RCL Foods faces intense buyer power and moderate supplier influence amid price-sensitive South African markets, while new entrants are deterred by scale and distribution advantages but substitutes and competitive rivalry remain significant risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RCL Foods’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration Strategy

RCL Foods reduces supplier power via deep vertical integration, owning key sugar and poultry farms and processing plants; by FY2024 the group reported circa 60% of poultry volumes sourced internally and integrated sugar capacity covering roughly 70% of its cane requirements.

Commodity Price Volatility

RCL Foods remains exposed to global commodity swings for maize and soya—used in animal feed—so international exchange pricing drives local supplier rates, constraining RCL’s negotiating power; maize futures rose ~28% in 2024 and soya oilseed gained ~22% (2024 Y/Y), making feed costs a large, externally dictated input expense and creating a balanced supplier power where market forces set primary input costs.

Energy and Utility Dependence

State-owned utilities in South Africa, notably Eskom (electricity) and Rand Water, exert strong leverage over RCL Foods because food processing is energy and water intensive; Eskom recorded 8 000+ MW of load-shedding capacity in 2024, forcing firms to invest in backups.

Frequent outages pushed South African manufacturers to spend on self-generation; RCL’s peers report capex rises of 5–12% for gensets and solar between 2022–2024, so RCL faces higher operating costs and capital needs.

Few large-scale private alternatives exist for grid-scale power and bulk water, so these utilities retain high bargaining power, increasing supply risk and margin pressure for RCL Foods.

Specialized Packaging Requirements

- Fewer than 30 certified regional suppliers

- Top 5 cover ~60% of demand

- Extended Producer Responsibility effective 2024

- Packaging disruptions can cut margins 3–6%

Concentrated Logistics Networks

RCL Foods depends heavily on third-party logistics and fuel suppliers for cold-chain distribution, exposing it to price hikes; South African diesel excise and transport tariffs rose ~8-12% in 2024, pressuring margins.

Logistics giants can pass rising costs—fuel levies plus a ~15-25% premium for refrigerated transport—to manufacturers, giving them bargaining leverage when specialized poultry and dairy handling is required.

- Third-party logistics dependency raises cost exposure

- 2024 diesel/transport increases ~8-12% hit margins

- Refrigerated transport premiums ~15-25%

- Concentrated providers hold pricing leverage

RCL Foods: strong vertical cover but maize/soya shocks, utility and supplier margin risks

RCL Foods limits supplier power through vertical integration (≈60% poultry internal, ≈70% sugar cane coverage FY2024) but remains exposed to maize/soya price swings (2024: maize +28%, soya +22%), utility leverage (Eskom load‑shedding 2024) and concentrated packaging/logistics suppliers causing 3–6% margin risk.

| Factor | Key number |

|---|---|

| Poultry vertical supply | ≈60% FY2024 |

| Sugar cane coverage | ≈70% FY2024 |

| Maize price change 2024 | +28% |

| Soya price change 2024 | +22% |

| Packaging supplier concentration | Top 5 ≈60% |

| Packaging margin hit risk | 3–6% |

| Diesel/transport rise 2024 | ≈8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for RCL Foods, uncovering competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers to assess pricing pressure and profitability within its South African food and agribusiness landscape.

A concise Porter's Five Forces one-sheet for RCL Foods—quickly highlights supplier, buyer, rivalry, substitution, and entry pressures to streamline strategic decisions.

Customers Bargaining Power

Retailer Consolidation

The South African grocery market is concentrated: Shoprite, Pick n Pay and Spar together held about 60% of formal grocery share in 2024, giving them huge buying power over suppliers like RCL Foods. These retailers buy massive volumes and routinely extract double-digit trade discounts and extended payment terms; for example, reported supplier rebates averaged 6–12% industry-wide in 2023. Control of scarce shelf space lets them demand promotional funding and private-label slots, weakening RCL Foods’ pricing power.

Growth of Private Label Brands

Major South African retailers like Shoprite and Pick n Pay raised private-label share to about 20–30% of food sales by 2024, directly competing with RCL Foods’ branded lines and boosting retailer bargaining power. Retailers can favor higher-margin house brands, pressuring RCL on pricing and shelf space; in 2024 RCL reported FY2024 revenue of ZAR 20.7bn, so margin erosion would materially hit results. RCL must keep investing in product innovation and brand equity to defend placement and premium pricing.

Low Switching Costs

For end consumers switching from RCL Foods to rivals costs near zero, especially in staples like sugar, flour and poultry where brands are shelf-substitutable; NielsenIQ (2024) shows 62% of South African grocery shoppers prioritize price. This drives RCL to keep margins tight—gross margin for Food reported 12.8% in FY2024—and sustain quality and promotions to retain a price-sensitive, fickle customer base.

Consumer Economic Pressure

High 2025 South African inflation of 5.9% (Q4 2025 y/y) and unemployment at ~32.9% (Q3 2025) raise price sensitivity, so consumers shift to bulk formats and cheaper brands, constraining RCL Foods’ ability to pass on input-cost inflation.

Price becomes the dominant purchase driver, increasing buyer power and forcing RCL to protect volume via promotions or lower-margin SKUs, squeezing gross margins.

- Inflation 5.9% (2025 Q4)

- Unemployment ~32.9% (2025 Q3)

- Higher trade-down to bulk/cheaper SKUs

- Limits on passing input costs → margin pressure

Information Symmetry

Information symmetry is high: by 2025 over 80% of South African consumers use smartphones for price checks, and platforms show real-time prices and nutrition, eroding RCL Foods’ ability to charge premiums.

Professional buyers use global benchmarks—bulk poultry and maize prices fell ~12% in 2024—so RCL must run tight margins and improve supply-chain efficiency.

Well-informed demand forces faster product updates and transparent labeling to retain market share.

- ~80% smartphone price-check penetration (2025)

- Global bulk input prices down ~12% in 2024

- Need for lean supply chain and transparent labeling

Retail concentration, private labels squeeze RCL Foods—margins under price pressure

Retail concentration (Shoprite, Pick n Pay, Spar ~60% share) and rising private-label (20–30% of food sales) give buyers strong leverage, forcing RCL Foods into discounts, promotional funding and margin pressure; FY2024 food gross margin 12.8% vs revenue ZAR 20.7bn. High price sensitivity (62% prioritize price), inflation 5.9% (Q4 2025) and smartphone price checks (~80%) further limit pass-through of input costs.

| Metric | Value |

|---|---|

| Retail share | ~60% |

| Private-label | 20–30% |

| RCL FY2024 revenue | ZAR 20.7bn |

| Food gross margin FY2024 | 12.8% |

| Price-sensitive shoppers | 62% |

| Inflation Q4 2025 | 5.9% |

| Smartphone price checks 2025 | ~80% |

What You See Is What You Get

RCL Foods Porter's Five Forces Analysis

This preview shows the exact RCL Foods Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; it’s fully formatted and ready to use.

You're looking at the actual deliverable: a complete, professionally written assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, available for instant download once you buy.