Reach Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

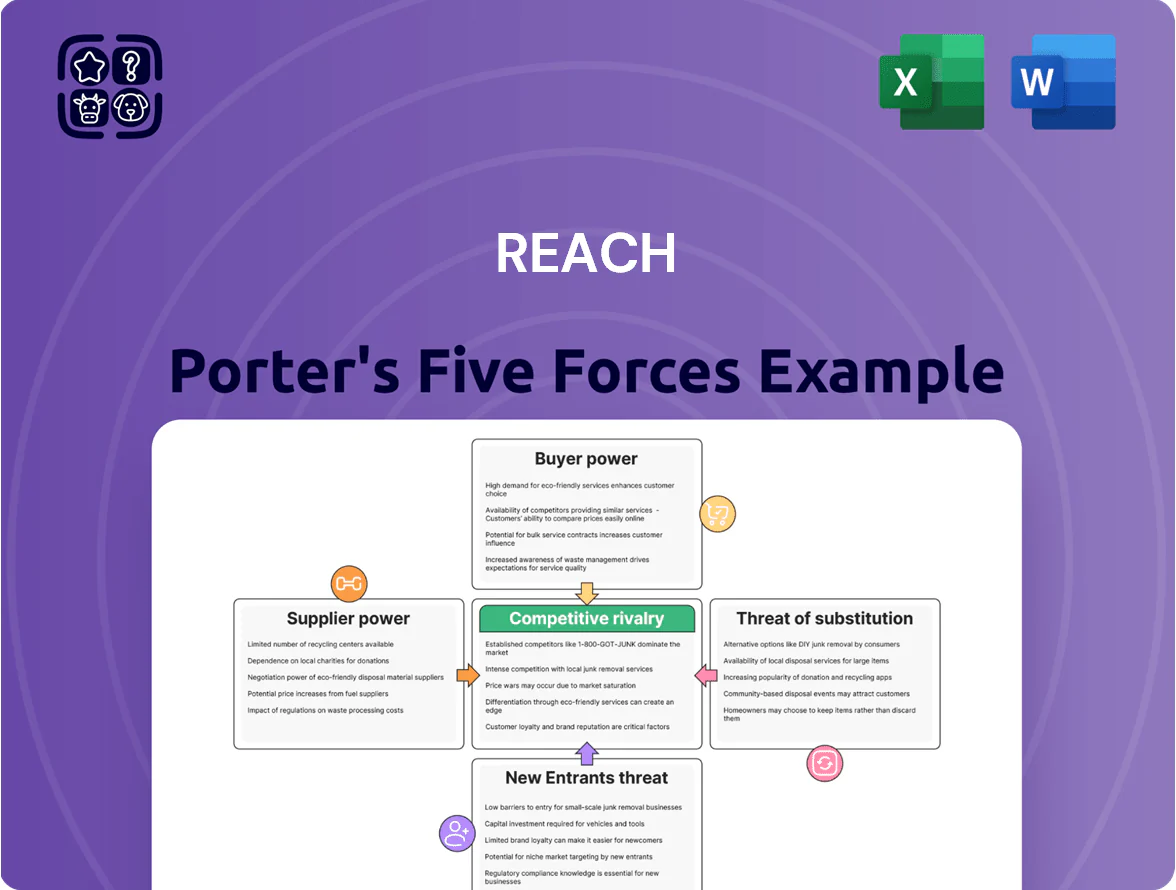

Reach faces a mix of competitive pressures—from evolving buyer expectations to disruptive substitutes—and this snapshot highlights key tension points shaping its strategy and margins; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Reach’s market position.

Suppliers Bargaining Power

Concentration of Newsprint Manufacturers

By late 2025, global newsprint capacity fell ~25% since 2018, concentrating supply among five major mills, leaving Reach PLC with markedly fewer paper vendors for its print titles.

Print still produced roughly 30% of Reach’s 2024 revenue, so price shocks from dominant mills can quickly erode margins and cash flow.

Limited suppliers give manufacturers leverage to tighten contract terms, and recent 2024–25 spot-price rises of ~18% highlight Reach’s exposure to raw-material cost volatility.

Reliance on Major Tech Infrastructure

Reach PLC relies on a few global tech providers for cloud hosting, analytics and ad delivery, creating high supplier power since switching costs and migration time are large; in 2024 Reach spent an estimated £35–45m on cloud and ad platform fees, roughly 6–8% of digital revenue. Any API access limits or fee increases by these giants would cut digital margins and slow product rollout, so supplier moves directly affect operational efficiency and customer-value delivery.

Specialized Editorial and Freelance Talent

By end-2025 demand for investigative journalism and niche digital creators has driven talent competition: global freelance newsroom vacancies rose 18% in 2024–25, boosting bargaining power for specialists.

Reach’s large staff cushions supply risk, but reliance on specialized freelancers and marquee columnists gives those individuals leverage to push fees up 12–30% versus staff rates.

Independent platforms like Substack and Patreon saw creator earnings grow ~25% in 2024, forcing Reach to raise freelance pay and project-based retainers to stay competitive.

Energy Costs for Printing Operations

Operating large-scale printing facilities makes Reach PLC highly sensitive to energy utility pricing; in 2024 electricity accounted for roughly 6–8% of printing cost inputs, so a 10% tariff rise would raise COGS by ~0.6–0.8 percentage points.

Volatility has eased since 2022–23 gas shocks, but suppliers still set terms that materially affect print margins—fixed-price contracts covered only ~30% of Reach’s print demand in 2024.

Few viable alternatives exist for high-energy industrial presses, so supplier leverage remains high and limits Reach’s ability to cut variable costs quickly.

- Electricity = ~6–8% of print input costs (2024)

- Fixed-price supply covers ~30% of demand (2024)

- 10% energy price rise → ~0.6–0.8ppt COGS increase

Content Syndication and News Agencies

Reach PLC depends on PA Media and similar agencies for national/international feeds, avoiding the prohibitive cost of full in-house coverage across ~180 regional titles.

Agency consolidation boosts supplier power; PA Media raised licence revenue by ~6% in 2023 while industry-wide agency subscription margins averaged ~25% in 2024, forcing Reach to accept higher fees to stay competitive.

- Critical service: national/international feeds

- Cost to replicate: prohibitive for ~180 titles

- Supplier leverage: consolidation → higher fees

- 2023–24 data: PA Media +6% revenue; agency margins ~25%

Supply squeeze, rising costs and platform fees threaten Reach’s margins

Supplier power is high: paper capacity fell ~25% since 2018, concentrating supply and causing ~18% spot-price rises in 2024–25 that threaten Reach’s ~30% print revenue; cloud/ad platform fees (~£35–45m in 2024, 6–8% of digital revenue) and agency consolidation (PA Media +6% revenue in 2023) add leverage; energy (electricity 6–8% of print inputs) and scarce specialist talent (freelance pay +12–30%) further tighten margins.

| Metric | Value |

|---|---|

| Paper capacity change (2018–2025) | −25% |

| Print share of revenue (2024) | ~30% |

| Paper spot-price rise (2024–25) | ~18% |

| Cloud/ad fees (2024) | £35–45m |

| Cloud/ad share of digital rev (2024) | 6–8% |

| Electricity share of print inputs (2024) | 6–8% |

| Fixed-price print coverage (2024) | ~30% |

| PA Media revenue change (2023) | +6% |

| Freelance pay premium vs staff | +12–30% |

What is included in the product

Tailored Five Forces analysis for Reach that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform pricing, positioning, and risk mitigation.

One-sheet Porter's Five Forces summary that turns complex competitive dynamics into actionable insights for faster, confident strategy decisions.

Customers Bargaining Power

Advertiser Shift to Programmatic and Big Tech

Corporate advertisers can reallocate budgets to Google, Meta, or Amazon, giving them strong bargaining power; Google and Meta took 54% of global ad spend in 2024, squeezing Reach’s share.

By 2025 demand for hyper-targeted, data-driven ads means Reach must prove ROI—advertisers expect CPA drops of 10–25%—or face churn.

Reach must keep CPMs competitive and invest in first-party data: firms spent $12B on identity solutions in 2024, a benchmarket for Reach’s needs.

Low Switching Costs for Digital Readers

Digital readers face near-zero switching costs and access thousands of free sources; UK online news reach hit 88% weekly in 2024, so bargaining power is very high.

If Reach raises paywalls or runs intrusive ads, users can move instantly to BBC Online, independent sites, or social feeds—Reach’s UK digital subscribers fell 3% in 2024, showing monetisation limits.

Price Sensitivity in Regional Print Markets

Regional print readers show high price sensitivity: after UK consumer inflation peaked at 10.1% in Oct 2022 and eased to ~3.7% in 2024, a 10–15% cover-price rise in 2023 cut circulation by ~6–9% at comparable titles, so Reach faces direct demand drops if it raises prices.

Data Privacy and Consent Trends

- 28% opt-out rate (UK, 2024–25)

- ~12% drop in CPMs for targeted ads

- 40%+ opt-out threshold risks major yield loss

Corporate Social Responsibility Expectations

Large advertisers and institutional investors now demand strict brand safety and ESG reporting; in 2024, 72% of global CMOs said they’d pull ad spend over ethical breaches, per WARC/BCG.

These customers can withdraw support, risking Reach’s ad revenue and share placements, so Reach must keep tight editorial controls and transparent operations to retain high-value clients.

- 72% of CMOs would pull spend (WARC/BCG, 2024)

- Top 10 advertisers often >30% ad revenue concentration

- Institutional ESG mandates grew 18% in 2023

Ad giants dominate as privacy opt-outs and easy switching squeeze Reach’s digital revenue

Advertisers hold strong leverage: Google and Meta took 54% of global ad spend in 2024, and top 10 advertisers often account for >30% of Reach’s ad revenue. User switching is easy—UK online news reach 88% weekly (2024) and Reach’s digital subs fell 3% in 2024. Privacy cuts addressable audiences (28% opt-out 2024–25), lowering CPMs ~12% and risking major yield if opt-outs exceed 40%.

| Metric | Value |

|---|---|

| Google+Meta ad share (2024) | 54% |

| UK weekly online news reach (2024) | 88% |

| Reach digital subs change (2024) | -3% |

| Opt-out rate (UK, 2024–25) | 28% |

| CPM drop (targeted) | ~12% |

Preview Before You Purchase

Reach Porter's Five Forces Analysis

This preview displays the exact Reach Porter’s Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready for immediate download.

No placeholders or samples: the file shown is the final deliverable you’ll get instantly upon payment, fully prepared for use in reports or presentations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Reach faces a mix of competitive pressures—from evolving buyer expectations to disruptive substitutes—and this snapshot highlights key tension points shaping its strategy and margins; unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Reach’s market position.

Suppliers Bargaining Power

Concentration of Newsprint Manufacturers

By late 2025, global newsprint capacity fell ~25% since 2018, concentrating supply among five major mills, leaving Reach PLC with markedly fewer paper vendors for its print titles.

Print still produced roughly 30% of Reach’s 2024 revenue, so price shocks from dominant mills can quickly erode margins and cash flow.

Limited suppliers give manufacturers leverage to tighten contract terms, and recent 2024–25 spot-price rises of ~18% highlight Reach’s exposure to raw-material cost volatility.

Reliance on Major Tech Infrastructure

Reach PLC relies on a few global tech providers for cloud hosting, analytics and ad delivery, creating high supplier power since switching costs and migration time are large; in 2024 Reach spent an estimated £35–45m on cloud and ad platform fees, roughly 6–8% of digital revenue. Any API access limits or fee increases by these giants would cut digital margins and slow product rollout, so supplier moves directly affect operational efficiency and customer-value delivery.

Specialized Editorial and Freelance Talent

By end-2025 demand for investigative journalism and niche digital creators has driven talent competition: global freelance newsroom vacancies rose 18% in 2024–25, boosting bargaining power for specialists.

Reach’s large staff cushions supply risk, but reliance on specialized freelancers and marquee columnists gives those individuals leverage to push fees up 12–30% versus staff rates.

Independent platforms like Substack and Patreon saw creator earnings grow ~25% in 2024, forcing Reach to raise freelance pay and project-based retainers to stay competitive.

Energy Costs for Printing Operations

Operating large-scale printing facilities makes Reach PLC highly sensitive to energy utility pricing; in 2024 electricity accounted for roughly 6–8% of printing cost inputs, so a 10% tariff rise would raise COGS by ~0.6–0.8 percentage points.

Volatility has eased since 2022–23 gas shocks, but suppliers still set terms that materially affect print margins—fixed-price contracts covered only ~30% of Reach’s print demand in 2024.

Few viable alternatives exist for high-energy industrial presses, so supplier leverage remains high and limits Reach’s ability to cut variable costs quickly.

- Electricity = ~6–8% of print input costs (2024)

- Fixed-price supply covers ~30% of demand (2024)

- 10% energy price rise → ~0.6–0.8ppt COGS increase

Content Syndication and News Agencies

Reach PLC depends on PA Media and similar agencies for national/international feeds, avoiding the prohibitive cost of full in-house coverage across ~180 regional titles.

Agency consolidation boosts supplier power; PA Media raised licence revenue by ~6% in 2023 while industry-wide agency subscription margins averaged ~25% in 2024, forcing Reach to accept higher fees to stay competitive.

- Critical service: national/international feeds

- Cost to replicate: prohibitive for ~180 titles

- Supplier leverage: consolidation → higher fees

- 2023–24 data: PA Media +6% revenue; agency margins ~25%

Supply squeeze, rising costs and platform fees threaten Reach’s margins

Supplier power is high: paper capacity fell ~25% since 2018, concentrating supply and causing ~18% spot-price rises in 2024–25 that threaten Reach’s ~30% print revenue; cloud/ad platform fees (~£35–45m in 2024, 6–8% of digital revenue) and agency consolidation (PA Media +6% revenue in 2023) add leverage; energy (electricity 6–8% of print inputs) and scarce specialist talent (freelance pay +12–30%) further tighten margins.

| Metric | Value |

|---|---|

| Paper capacity change (2018–2025) | −25% |

| Print share of revenue (2024) | ~30% |

| Paper spot-price rise (2024–25) | ~18% |

| Cloud/ad fees (2024) | £35–45m |

| Cloud/ad share of digital rev (2024) | 6–8% |

| Electricity share of print inputs (2024) | 6–8% |

| Fixed-price print coverage (2024) | ~30% |

| PA Media revenue change (2023) | +6% |

| Freelance pay premium vs staff | +12–30% |

What is included in the product

Tailored Five Forces analysis for Reach that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic commentary to inform pricing, positioning, and risk mitigation.

One-sheet Porter's Five Forces summary that turns complex competitive dynamics into actionable insights for faster, confident strategy decisions.

Customers Bargaining Power

Advertiser Shift to Programmatic and Big Tech

Corporate advertisers can reallocate budgets to Google, Meta, or Amazon, giving them strong bargaining power; Google and Meta took 54% of global ad spend in 2024, squeezing Reach’s share.

By 2025 demand for hyper-targeted, data-driven ads means Reach must prove ROI—advertisers expect CPA drops of 10–25%—or face churn.

Reach must keep CPMs competitive and invest in first-party data: firms spent $12B on identity solutions in 2024, a benchmarket for Reach’s needs.

Low Switching Costs for Digital Readers

Digital readers face near-zero switching costs and access thousands of free sources; UK online news reach hit 88% weekly in 2024, so bargaining power is very high.

If Reach raises paywalls or runs intrusive ads, users can move instantly to BBC Online, independent sites, or social feeds—Reach’s UK digital subscribers fell 3% in 2024, showing monetisation limits.

Price Sensitivity in Regional Print Markets

Regional print readers show high price sensitivity: after UK consumer inflation peaked at 10.1% in Oct 2022 and eased to ~3.7% in 2024, a 10–15% cover-price rise in 2023 cut circulation by ~6–9% at comparable titles, so Reach faces direct demand drops if it raises prices.

Data Privacy and Consent Trends

- 28% opt-out rate (UK, 2024–25)

- ~12% drop in CPMs for targeted ads

- 40%+ opt-out threshold risks major yield loss

Corporate Social Responsibility Expectations

Large advertisers and institutional investors now demand strict brand safety and ESG reporting; in 2024, 72% of global CMOs said they’d pull ad spend over ethical breaches, per WARC/BCG.

These customers can withdraw support, risking Reach’s ad revenue and share placements, so Reach must keep tight editorial controls and transparent operations to retain high-value clients.

- 72% of CMOs would pull spend (WARC/BCG, 2024)

- Top 10 advertisers often >30% ad revenue concentration

- Institutional ESG mandates grew 18% in 2023

Ad giants dominate as privacy opt-outs and easy switching squeeze Reach’s digital revenue

Advertisers hold strong leverage: Google and Meta took 54% of global ad spend in 2024, and top 10 advertisers often account for >30% of Reach’s ad revenue. User switching is easy—UK online news reach 88% weekly (2024) and Reach’s digital subs fell 3% in 2024. Privacy cuts addressable audiences (28% opt-out 2024–25), lowering CPMs ~12% and risking major yield if opt-outs exceed 40%.

| Metric | Value |

|---|---|

| Google+Meta ad share (2024) | 54% |

| UK weekly online news reach (2024) | 88% |

| Reach digital subs change (2024) | -3% |

| Opt-out rate (UK, 2024–25) | 28% |

| CPM drop (targeted) | ~12% |

Preview Before You Purchase

Reach Porter's Five Forces Analysis

This preview displays the exact Reach Porter’s Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready for immediate download.

No placeholders or samples: the file shown is the final deliverable you’ll get instantly upon payment, fully prepared for use in reports or presentations.